1. The payback period method ignores the time value of money and cash flows expected after the cutoff period. This can lead to Type I errors where projects with negative NPV are accepted.

2. Misestimating the discount rate can lead a firm to reject projects that actually have positive NPV.

3. The NPV profile shows the project's IRR is 0%, 10%, 20% and 30% due to cash flows changing signs at those points.

1. The payback period method ignores the time value of money and cash flows expected after the cutoff period. This can lead to Type I errors where projects with negative NPV are accepted.

2. Misestimating the discount rate can lead a firm to reject projects that actually have positive NPV.

3. The NPV profile shows the project's IRR is 0%, 10%, 20% and 30% due to cash flows changing signs at those points.

1. The payback period method ignores the time value of money and cash flows expected after the cutoff period. This can lead to Type I errors where projects with negative NPV are accepted.

2. Misestimating the discount rate can lead a firm to reject projects that actually have positive NPV.

3. The NPV profile shows the project's IRR is 0%, 10%, 20% and 30% due to cash flows changing signs at those points.

1. The payback period method ignores the time value of money and cash flows expected after the cutoff period. This can lead to Type I errors where projects with negative NPV are accepted.

2. Misestimating the discount rate can lead a firm to reject projects that actually have positive NPV.

3. The NPV profile shows the project's IRR is 0%, 10%, 20% and 30% due to cash flows changing signs at those points.

Download as DOCX, PDF, TXT or read online from Scribd

Download as docx, pdf, or txt

You are on page 1/ 3

Exercise 1 (Answers)

1(a) I. The method ignores the cash flows that are expected after the cut-off period II. It focuses on quick cash-generation rather than value-maximization III. The Psychological appeal to the underlying idea is strong that lead to the wide usage of the method 1(b) the method ignores the time value of money. Hence, a project with a short payback period may have negative NPV

1(c) Type I error is most likely to occur.

2. The value of NPV is the direct estimate of change in value of the firm that will result if a particular project is taken up. Misestimating the discount rate could have lead the firm to reject projects that had positive NPVs if the correct discount rate was used.

3(a) The stock’s prices would have exhibited high growth in the past. 3(b) The CEO’s judgement is partially correct (because taking up the new project will lower the firm’s average return) and partially incorrect (because 18% return is still higher than the firms’ investors expectation of 15%. Hence, taking up the project would increase the firm value)

4. NPV = 0 and IRR= 10%

5. Asset A Asset B ROA 46% 22.2% Payback Period 2.55 2.33 Discounted Payback 3.16 3.609

6. NPV of The Project = $ 9,972,742

Change in Firm Value that will result from taking up the Project = NPV Change in the Price of the share = Change in value of firm / Number of shares = 9972742/10000000= 0.9972742 Therefore, New price = $ 10.9973

7.

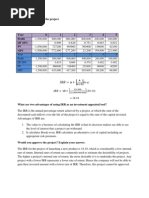

Incrementa DCF Renovate Replace l (Incremental) 0 -9,000,000 -1,000,000 -8,000,000 -8000000 1 3,500,000 600,000 2,900,000 2442310.931 2 3,000,000 500,000 2,500,000 1773151.809 3 3,000,000 400,000 2,600,000 1553038.472 4 2,800,000 300,000 2,500,000 1257626.935 5 2,500,000 200,000 2,300,000 974411.9761 NPV 1,128,309 433,779 694,530 IRR 20.485% 36.1% 18.745% 8. Discount Rate NPV 0 0 5 -1.35 10 0 15 0.563 20 0 25 -0.672 30 0 35 3.458 50 41.48 NOTE: THE PROFILE SHOULD BE SMOOTH CURVE NOT A COMIBNATION OF STRAIGHT LINES AS DISPLAYED IN THE GRAPH BELOW. THIS WAS DUE THE LIMITATIONS EXCEL HAD IMPOSED TO DRAW A CURVED MARKED LINE.

NPV Profile 4

0 0 5 10 15 20 25 30 35 -1

-2

PROJECT’S IRR has four values: 0%, 10%, 20% and 30% (recall: cash flows changing signs)

9. Mail- Order Year Processor 0 -4,500,000 1 2,000,000 2 2,000,000 3 2,000,000 IRR 15.85%

a) OLD LINE: IRR > Hurdle rate (10%), hence, the project would be accepted b) HIGH TECH: IRR<Hurdle rate (20%), hence, the project will be rejected c) A project’s feasibility may vary from one firm to another, depending on the risk class they operate in. Hence, it may not be the case that a project that is feasible for one firm is also feasible for another unless the two firms lie in similar risk classification.

Decisions should only be taken on the basis of NPV. However, justification for the decision is only required when the firm’s practice is to use IRR as the capital budgeting technique and there’s a conflict in the decision resulting from the use of NPV and IRR simultaneously.