Module 2 PDF

Module 2 PDF

Download as pdf or txt

You might also like

- Fundamentals of International FinanceDocument11 pagesFundamentals of International FinanceChirag KotianNo ratings yet

- Eskom 2019 Integrated Report PDFDocument95 pagesEskom 2019 Integrated Report PDFNatalie WaThaboNo ratings yet

- Chapter 17 HWDocument40 pagesChapter 17 HWEejay MagatNo ratings yet

- Practice Question For Depreciation & ProvisionDocument2 pagesPractice Question For Depreciation & ProvisionAli QasimNo ratings yet

- Unit 4 GLOBAL BUSINESS BBA NOTESDocument36 pagesUnit 4 GLOBAL BUSINESS BBA NOTESHome PCNo ratings yet

- Multinational Financial ManagementDocument32 pagesMultinational Financial ManagementAshok RanaNo ratings yet

- Chapter 4 The Interntional Flow of Funds and Exchange RatesDocument14 pagesChapter 4 The Interntional Flow of Funds and Exchange RatesRAY NICOLE MALINGI100% (1)

- Bop NotesDocument5 pagesBop NotesPari 2ANo ratings yet

- Foreign ExchangeDocument3 pagesForeign Exchangeatharva1760No ratings yet

- Mortgage Markets and Derivatives Foreign Exchange MarketsDocument29 pagesMortgage Markets and Derivatives Foreign Exchange Marketscreacion impresionesNo ratings yet

- Global Financial System: International InstitutionsDocument21 pagesGlobal Financial System: International Institutionsapi-265248190% (1)

- Q1) Factors Affecting Exchange Rates: Interest and Inflation RatesDocument7 pagesQ1) Factors Affecting Exchange Rates: Interest and Inflation RatesMandar SangleNo ratings yet

- Foreign Exchange RateDocument29 pagesForeign Exchange RateakshaynnaikNo ratings yet

- ForeignDocument70 pagesForeignadsfdgfhgjhkNo ratings yet

- 1) Introduction: Currency ConvertibilityDocument34 pages1) Introduction: Currency ConvertibilityZeenat AnsariNo ratings yet

- 01 Global Financial System: 1.1 International InstitutionsDocument25 pages01 Global Financial System: 1.1 International Institutionsapi-26524819No ratings yet

- Global Financial System: International InstitutionsDocument15 pagesGlobal Financial System: International Institutionsapi-26524819No ratings yet

- Part C CDocument22 pagesPart C Camir chandiNo ratings yet

- Exchangeratedetermination 231203051223 b5530f63Document26 pagesExchangeratedetermination 231203051223 b5530f63opmontchallangeNo ratings yet

- Meaning of ForexDocument4 pagesMeaning of Forexdeepanshu90509No ratings yet

- Unit - 4: Exchange Rate and Its Economic Effects: Learning OutcomesDocument20 pagesUnit - 4: Exchange Rate and Its Economic Effects: Learning Outcomesganeshnavi2008No ratings yet

- International Monetary and Financial Systems - Chapter-4 MbsDocument62 pagesInternational Monetary and Financial Systems - Chapter-4 MbsArjun Mishra100% (1)

- TCQT EssayDocument11 pagesTCQT EssayThư TrầnNo ratings yet

- Determinants of Exchange RateDocument2 pagesDeterminants of Exchange RateSajid Ali BhuttaNo ratings yet

- Macro - Short NoteDocument8 pagesMacro - Short Noteabirhamalehubel92No ratings yet

- Open Economy Macroeconomics Class 12 Notes CBSE Macro Economics Chapter 6 PDFDocument5 pagesOpen Economy Macroeconomics Class 12 Notes CBSE Macro Economics Chapter 6 PDFganeshNo ratings yet

- How International Currency Excharge Rate WorksDocument6 pagesHow International Currency Excharge Rate Worksggi2022.1928No ratings yet

- Case C8Document6 pagesCase C8Việt Tuấn TrịnhNo ratings yet

- The Meaning of Foreign ExchangeDocument5 pagesThe Meaning of Foreign ExchangeRohini ManiNo ratings yet

- Final Assignment Forex MarketDocument6 pagesFinal Assignment Forex MarketUrvish Tushar DalalNo ratings yet

- Chapter 4Document24 pagesChapter 4Manjunath BVNo ratings yet

- Cbse Class 12 Macro Economics Notes Chapter 6Document7 pagesCbse Class 12 Macro Economics Notes Chapter 6Abhishek Singh ManhasNo ratings yet

- Inflation. Interest Rates. Balance of Payments. Government Intervention. Other FactorsDocument2 pagesInflation. Interest Rates. Balance of Payments. Government Intervention. Other FactorsEmmanuelle RojasNo ratings yet

- Intl Eco LawDocument9 pagesIntl Eco LawPrassanna PrabagaranNo ratings yet

- Balance of PaymentDocument16 pagesBalance of PaymentHarjas KaurNo ratings yet

- Saman Jain C 228 WA No. - 1 ForexDocument8 pagesSaman Jain C 228 WA No. - 1 ForexSaman JainNo ratings yet

- Capital Account Convertibility (ECO)Document40 pagesCapital Account Convertibility (ECO)KhushbooNo ratings yet

- Chapter FiveDocument29 pagesChapter Fiveousni solomonNo ratings yet

- Exchange Rate Determinants AND Fixed & Flexible Exchange RatesDocument27 pagesExchange Rate Determinants AND Fixed & Flexible Exchange RatesArunav BarooahNo ratings yet

- Module IV and V NotesDocument21 pagesModule IV and V Notesamulyaranganath4No ratings yet

- IFM UNIT - 1 - CompressedDocument36 pagesIFM UNIT - 1 - CompressedChirurock TrividhiNo ratings yet

- Unit - Iii: Foreign Exchange Determination Systems &international InstitutionsDocument97 pagesUnit - Iii: Foreign Exchange Determination Systems &international InstitutionsShaziyaNo ratings yet

- Exchange Rate Movements: Changes in ExportsDocument11 pagesExchange Rate Movements: Changes in ExportsamitNo ratings yet

- Econ 323-Open MacroeconomyDocument14 pagesEcon 323-Open Macroeconomyezekielmuriithi34No ratings yet

- Exam Assigment of IFMDocument9 pagesExam Assigment of IFMPunita KumariNo ratings yet

- FEMA (Foreing Exchange Management Act)Document4 pagesFEMA (Foreing Exchange Management Act)mahbobullah rahmaniNo ratings yet

- Question Bank With Answers: Module-1Document52 pagesQuestion Bank With Answers: Module-1kkvNo ratings yet

- Antim Prahar Foreign Exchange and Risk Management 2024Document50 pagesAntim Prahar Foreign Exchange and Risk Management 2024Dishant TomarNo ratings yet

- Monetory Eco Assignment and PPTDocument8 pagesMonetory Eco Assignment and PPTobayed florianNo ratings yet

- International FinanceDocument6 pagesInternational FinanceKieu Anh PhamNo ratings yet

- The Impossible Trinity: Presented By: Group-8Document26 pagesThe Impossible Trinity: Presented By: Group-8khem_singhNo ratings yet

- The Determination of Exchange Rate: BY Annisa Ramadhani Bertha Muhammad Karina Fitri Zahira SalsabellaDocument25 pagesThe Determination of Exchange Rate: BY Annisa Ramadhani Bertha Muhammad Karina Fitri Zahira SalsabellaRatu ShaviraNo ratings yet

- Exchange Control RegulationDocument5 pagesExchange Control RegulationArjun lal KumawatNo ratings yet

- FIN 422 (Chapter 2)Document9 pagesFIN 422 (Chapter 2)Sumaiya AfrinNo ratings yet

- Factors Affecting Exchange RatesDocument9 pagesFactors Affecting Exchange RatesAnoopa NarayanNo ratings yet

- Unit 2 Foreign Exchange and Balance of Payments Foreign Exchange Market Meaning & Definition of Foreign ExchangeDocument26 pagesUnit 2 Foreign Exchange and Balance of Payments Foreign Exchange Market Meaning & Definition of Foreign ExchangeKaran C VNo ratings yet

- Currency Convertibili TY - Pros & Cons & 1997 ASIAN CrisisDocument22 pagesCurrency Convertibili TY - Pros & Cons & 1997 ASIAN Crisisrajan1204No ratings yet

- Chapter 9Document12 pagesChapter 9myrelle.oculNo ratings yet

- International Economic Integration and Institution WRDocument10 pagesInternational Economic Integration and Institution WRYvonne LlamadaNo ratings yet

- Foreign Exchange Marketg4Document37 pagesForeign Exchange Marketg4Shan CredoNo ratings yet

- International Trade of Goods and Services And: Key Factors That Affect Foreign Exchange Rates 1. Inflation RatesDocument5 pagesInternational Trade of Goods and Services And: Key Factors That Affect Foreign Exchange Rates 1. Inflation RatesUtkarsh GuptaNo ratings yet

- DownloadDocument4 pagesDownloadmanirajpoot45No ratings yet

- Module 5 PDFDocument17 pagesModule 5 PDFRAJASAHEB DUTTANo ratings yet

- Module 7 PDFDocument12 pagesModule 7 PDFRAJASAHEB DUTTANo ratings yet

- Module 4 PDFDocument19 pagesModule 4 PDFRAJASAHEB DUTTANo ratings yet

- Module 3 PDFDocument21 pagesModule 3 PDFRAJASAHEB DUTTANo ratings yet

- Module 1 PDFDocument11 pagesModule 1 PDFRAJASAHEB DUTTANo ratings yet

- Archisman Dutta (FPB1921 - 102) - FEM AssignmentDocument2 pagesArchisman Dutta (FPB1921 - 102) - FEM AssignmentRAJASAHEB DUTTANo ratings yet

- Assignment (Fem) (Batch19-21) Unique International Total Marks:20Document3 pagesAssignment (Fem) (Batch19-21) Unique International Total Marks:20RAJASAHEB DUTTANo ratings yet

- Problem Ch.14Document3 pagesProblem Ch.14kenny 322016048100% (1)

- Sample Company Profile-TCSDocument25 pagesSample Company Profile-TCSSALONI JaiswalNo ratings yet

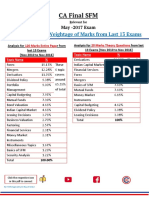

- CA Final SFM Chapter Wise Weightage Applicable For May 2017 NFUH6CATDocument1 pageCA Final SFM Chapter Wise Weightage Applicable For May 2017 NFUH6CATvignesh_vikiNo ratings yet

- 23.03.27 SW the-PutCall-ratio-As-A-contrarian-market-timing-Indicator (2022, Fabian Scheler, PCR As A Contrarian Indicator)Document4 pages23.03.27 SW the-PutCall-ratio-As-A-contrarian-market-timing-Indicator (2022, Fabian Scheler, PCR As A Contrarian Indicator)Rolf ScheiderNo ratings yet

- Spicejet: Credit Rating AnalysisDocument9 pagesSpicejet: Credit Rating Analysissatyakidutta007No ratings yet

- Laporan Kas Bank PT GalaksiDocument7 pagesLaporan Kas Bank PT GalaksiMoestofeUbunkTbiNo ratings yet

- Employer Branding in BFSI SectorDocument14 pagesEmployer Branding in BFSI SectorprabhjitsinghwaliaNo ratings yet

- Aror University ChallanDocument1 pageAror University ChallanmomeetechNo ratings yet

- Form No. 21 Deed of Conveyance in Favour of MortgageeDocument3 pagesForm No. 21 Deed of Conveyance in Favour of MortgageeSudeep SharmaNo ratings yet

- In Fs ICEMA NoexpDocument24 pagesIn Fs ICEMA NoexpG BabuNo ratings yet

- A Comparative Study On Financial Performance of Tata Steel LTD and JSW Steels LTDDocument8 pagesA Comparative Study On Financial Performance of Tata Steel LTD and JSW Steels LTDKathiravan SNo ratings yet

- 25 - Mithun - 10 - 2 - Individual AssignmentDocument4 pages25 - Mithun - 10 - 2 - Individual AssignmentMithun ChowdhuryNo ratings yet

- Dividend Policy Determinants: An Investigation of The Influences of Stakeholder TheoryDocument18 pagesDividend Policy Determinants: An Investigation of The Influences of Stakeholder Theorywedaje2003No ratings yet

- Chapter 7 Slides FIN 435Document18 pagesChapter 7 Slides FIN 435Wasim HassanNo ratings yet

- Top 61 Accounting Interview QuestionsDocument2 pagesTop 61 Accounting Interview Questionsparminder211985No ratings yet

- Stubben 2006Document48 pagesStubben 2006Widya PertiwiNo ratings yet

- Project FinanceDocument3 pagesProject FinancePallavi_Singh_3634No ratings yet

- IAS 23 - Borrowing CostDocument4 pagesIAS 23 - Borrowing CostMuhammad QamarNo ratings yet

- Han 2008Document15 pagesHan 2008Ana CamachoNo ratings yet

- Pre-Assessment Test For Auditing TheoryDocument13 pagesPre-Assessment Test For Auditing TheoryPrecious mae BarrientosNo ratings yet

- Business Research Report: The Minimization of Credit Card System Issues in HBL & Standard Chartered BankDocument41 pagesBusiness Research Report: The Minimization of Credit Card System Issues in HBL & Standard Chartered BankFawad IftikharNo ratings yet

- DBMS in LandbankDocument20 pagesDBMS in LandbankHoney AzeNo ratings yet

- Finact 3 Prelims 2019-2020Document5 pagesFinact 3 Prelims 2019-2020Kenneth Lim OlayaNo ratings yet

- CB VS CA - TOLENTINO (G.R. No. L-45710)Document2 pagesCB VS CA - TOLENTINO (G.R. No. L-45710)Thoughts and More ThoughtsNo ratings yet

- Dec 2022 BillDocument1 pageDec 2022 BillAnuj BansalNo ratings yet

- Filling of Resolution - MGT-14 - Series - 32Document9 pagesFilling of Resolution - MGT-14 - Series - 32Divesh GoyalNo ratings yet

- English Club Top 20 Business VocabularyDocument18 pagesEnglish Club Top 20 Business VocabularyemmyelitaNo ratings yet