Download as pdf or txt

You might also like

- HBS Finance Basics Course NotesDocument16 pagesHBS Finance Basics Course NotesAlice JeanNo ratings yet

- Ratio Analysis Missing FiguresDocument1 pageRatio Analysis Missing FiguresFahad Batavia0% (1)

- 3-9 FINANCIAL STATEMENTS The Davidson CorporationDocument3 pages3-9 FINANCIAL STATEMENTS The Davidson Corporationlai vivianNo ratings yet

- All Q&ADocument27 pagesAll Q&AFor LearningNo ratings yet

- F5 AbcDocument20 pagesF5 AbcMazni HanisahNo ratings yet

- Answers/loan Amortization Schedule Personal Finance Problem Joan Messineo Borrowed 20 000 9 Annual q51926905Document7 pagesAnswers/loan Amortization Schedule Personal Finance Problem Joan Messineo Borrowed 20 000 9 Annual q51926905HasanAbdullahNo ratings yet

- Table That Follows For Hoffmeister Industries Using The Following Financial DataDocument3 pagesTable That Follows For Hoffmeister Industries Using The Following Financial DataHamza ZainNo ratings yet

- Discussion - Example Problem of Keep or Drop DecisionsDocument2 pagesDiscussion - Example Problem of Keep or Drop DecisionsGiselle Martinez0% (1)

- AFACHPT3Document18 pagesAFACHPT3LATOYA PHILIP100% (1)

- Chapter 3: Working With Financial StatementsDocument10 pagesChapter 3: Working With Financial StatementsNafeun AlamNo ratings yet

- Chapter 7 Materials Controlling and CostingDocument43 pagesChapter 7 Materials Controlling and CostingNabiha Awan100% (1)

- Assignment 5-2020Document2 pagesAssignment 5-2020Muhammad Hamza0% (4)

- Valuation of Long Term SecuritiesDocument12 pagesValuation of Long Term SecuritiesRasab Ahmed0% (1)

- Illustration1: For The Production of 10000 Units of A Product, The Following Are The Budgeted ExpensesDocument4 pagesIllustration1: For The Production of 10000 Units of A Product, The Following Are The Budgeted ExpensesGabriel BelmonteNo ratings yet

- Meghna Bank Retail Banking - Updated - Nov16Document47 pagesMeghna Bank Retail Banking - Updated - Nov16Md SayeedNo ratings yet

- 18Document4 pages18Aditya Wisnu P100% (1)

- Chapter 4 (The Valuation of Long-Term Securities)Document21 pagesChapter 4 (The Valuation of Long-Term Securities)Wilson Dhruba KuluntunuNo ratings yet

- Capital Budgeting QuestionsDocument3 pagesCapital Budgeting QuestionsTAYYABA AMJAD L1F16MBAM0221100% (1)

- Chapter 4Document96 pagesChapter 4lentra anandaNo ratings yet

- Zaire Electronics Can Make Either of PDFDocument6 pagesZaire Electronics Can Make Either of PDFHafiz Reza100% (1)

- Exercise Stock ValuationDocument2 pagesExercise Stock ValuationUmair ShekhaniNo ratings yet

- Question 1: Score 0/1: Your Response Correct ResponseDocument50 pagesQuestion 1: Score 0/1: Your Response Correct ResponseAtarinta Dyah PitalokaNo ratings yet

- Leverage and Capital Structure: Multiple Choice QuestionsDocument30 pagesLeverage and Capital Structure: Multiple Choice QuestionsRod100% (1)

- Mississippi River Shipyards Is Considering The Replacement of An - Appendix 11B-3 Replacement Project AnalysisDocument1 pageMississippi River Shipyards Is Considering The Replacement of An - Appendix 11B-3 Replacement Project AnalysisRajib DahalNo ratings yet

- ACC00152 Business Finance Topic 6 Tutorial AnswersDocument2 pagesACC00152 Business Finance Topic 6 Tutorial AnswersPaul TianNo ratings yet

- Adv CH Onefor 3rd YearDocument32 pagesAdv CH Onefor 3rd Yearalemayehu100% (2)

- Cost Accounting by Usry Chapter 6 Exercise 1Document4 pagesCost Accounting by Usry Chapter 6 Exercise 1Saadia Saeed100% (2)

- Assignment On CH 3 and 4 Cost 2Document4 pagesAssignment On CH 3 and 4 Cost 2sadiya AbrahimNo ratings yet

- Chapter 12Document42 pagesChapter 12Ivo_Nicht100% (4)

- Chapter One TDocument39 pagesChapter One TtemedebereNo ratings yet

- Capital Budgeting Exercise1Document14 pagesCapital Budgeting Exercise1Bigbi Kumar50% (2)

- Common Size AnalysisDocument25 pagesCommon Size AnalysisYoura DeAi0% (1)

- Assignment 2Document3 pagesAssignment 2AnasAhmed0% (1)

- Chapter 21Document4 pagesChapter 21Rahila RafiqNo ratings yet

- Financial Markets Week 2 3Document9 pagesFinancial Markets Week 2 3Jericho DupayaNo ratings yet

- Multiple Choice Questions: Financial Statements and AnalysisDocument29 pagesMultiple Choice Questions: Financial Statements and AnalysisHarvey PeraltaNo ratings yet

- Paper - 5: Advanced Accounting Questions Answer The Following (Give Adequate Working Notes in Support of Your Answer)Document56 pagesPaper - 5: Advanced Accounting Questions Answer The Following (Give Adequate Working Notes in Support of Your Answer)Basant OjhaNo ratings yet

- Chapter 3 - Chapter 3: Financial Forecasting and PlanningDocument35 pagesChapter 3 - Chapter 3: Financial Forecasting and PlanningAhmad Ridhuwan AbdullahNo ratings yet

- Capital Rationing: Reporter: Celestial C. AndradaDocument13 pagesCapital Rationing: Reporter: Celestial C. AndradaCelestial Manikan Cangayda-AndradaNo ratings yet

- FM Unit 2 Lecture Notes - Financial Statement AnalysisDocument4 pagesFM Unit 2 Lecture Notes - Financial Statement AnalysisDebbie DebzNo ratings yet

- Self Study Solutions Chapter 3Document27 pagesSelf Study Solutions Chapter 3flowerkmNo ratings yet

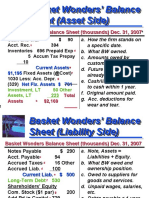

- Basket Wonders' Balance Sheet (Asset Side)Document32 pagesBasket Wonders' Balance Sheet (Asset Side)OSAMA0% (1)

- ANSWER: 4.375% or 4.38%: Stock Expected Return Standard Deviation BetaDocument2 pagesANSWER: 4.375% or 4.38%: Stock Expected Return Standard Deviation BetaMicon100% (2)

- Chap 008Document63 pagesChap 008Radu MirceaNo ratings yet

- Chapter 17 Standard Costing Setting Standards and Analyzing VariancesDocument23 pagesChapter 17 Standard Costing Setting Standards and Analyzing VariancesHashir AliNo ratings yet

- 03B) Chapter 3 Questions - BrighamDocument7 pages03B) Chapter 3 Questions - BrighamMohammad Ather100% (1)

- BFIN525 - Chapter 9 ProblemsDocument6 pagesBFIN525 - Chapter 9 Problemsmohamad yazbeckNo ratings yet

- EPS MCQs PDFDocument8 pagesEPS MCQs PDFMaria Jawed100% (1)

- CH # 8 (By Product)Document10 pagesCH # 8 (By Product)Rooh Ullah KhanNo ratings yet

- Financial Management - Stock Valuation Assignment 2 - Abdullah Bin Amir - Section ADocument3 pagesFinancial Management - Stock Valuation Assignment 2 - Abdullah Bin Amir - Section AAbdullah AmirNo ratings yet

- Assignement No 3Document2 pagesAssignement No 3Elina aliNo ratings yet

- Accounting Principles Chapter 4 SolutionDocument154 pagesAccounting Principles Chapter 4 SolutionMaldin JeremiaNo ratings yet

- Preffered Stock ValuationDocument1 pagePreffered Stock ValuationJeanne Sherlyn Tello100% (1)

- Chapter 13 SolutionsDocument5 pagesChapter 13 SolutionsStephen Ayala100% (1)

- Brief Exercises CHAPTER 7Document3 pagesBrief Exercises CHAPTER 7Trang LeNo ratings yet

- Week 3 Accounting HelpDocument4 pagesWeek 3 Accounting HelpGiuseppe Mccoy100% (1)

- Unit 7Document46 pagesUnit 7samuel kebede50% (2)

- Financial Statements and Ratio AnalysisDocument26 pagesFinancial Statements and Ratio Analysismary jean giananNo ratings yet

- Ratio AnalysisDocument11 pagesRatio AnalysisAna Marie EscoridoNo ratings yet

- Learning Activity 1 - Analysis of Financial StatementsDocument3 pagesLearning Activity 1 - Analysis of Financial StatementsAra Joyce PermalinoNo ratings yet

- MA A-3 Ratio AnalysisDocument3 pagesMA A-3 Ratio AnalysisShilpa AroraNo ratings yet

- Acctg1205 - Chapter 8Document48 pagesAcctg1205 - Chapter 8Elj Grace BaronNo ratings yet

- A Review On Dispute Resolution PracticeDocument2 pagesA Review On Dispute Resolution PracticeNikesh ShresthaNo ratings yet

- Design of Steel Section: Codes UsedDocument1 pageDesign of Steel Section: Codes UsedNikesh ShresthaNo ratings yet

- Morality: 1. General Introduction On Morale and Ethics Moral: DefinitionsDocument66 pagesMorality: 1. General Introduction On Morale and Ethics Moral: DefinitionsNikesh ShresthaNo ratings yet

- Professional Ethics Assignment 3Document12 pagesProfessional Ethics Assignment 3Nikesh ShresthaNo ratings yet

- SAP2000 TutorialDocument1 pageSAP2000 TutorialNikesh ShresthaNo ratings yet

- Fabm2 Q2 M4 - 4 CsefDocument20 pagesFabm2 Q2 M4 - 4 CsefZeus MalicdemNo ratings yet

- Federal Urdu University of Arts, Science and Technology, IslamabadDocument4 pagesFederal Urdu University of Arts, Science and Technology, IslamabadQasim Jahangir WaraichNo ratings yet

- Chapter 4Document31 pagesChapter 4Kristina Kitty100% (1)

- The Audit Quality Forum (2005) Thus Concluded Than A Simple Agency Model Involves That, " As A ResultDocument7 pagesThe Audit Quality Forum (2005) Thus Concluded Than A Simple Agency Model Involves That, " As A ResultRODRIGO JR. MADRAZONo ratings yet

- Negotiable Instruments - Case DigestDocument8 pagesNegotiable Instruments - Case DigestKeyba Dela CruzNo ratings yet

- International Financial MarketsDocument92 pagesInternational Financial MarketsSarvar Alam100% (2)

- Chase FeeDocument5 pagesChase FeePeter Ruliang YanNo ratings yet

- PPF VasuDocument2 pagesPPF VasuVasu AmmuluNo ratings yet

- COA CIRCULAR NO. 2024 006 March 14 2024Document21 pagesCOA CIRCULAR NO. 2024 006 March 14 2024Jen IgnacioNo ratings yet

- STARR Travel Insurance Application FormDocument1 pageSTARR Travel Insurance Application Formsheila coloradaNo ratings yet

- Work Sheet: SAMARA University College of Business and Economics Department of Accounting and FinanceDocument2 pagesWork Sheet: SAMARA University College of Business and Economics Department of Accounting and FinanceAsaye Tesfa100% (1)

- Akm IwelDocument7 pagesAkm IwelIwel NetriNo ratings yet

- Solutions To ExercisesDocument38 pagesSolutions To ExercisesAnh KietNo ratings yet

- Big Four Accounting Firms - WikipediaDocument4 pagesBig Four Accounting Firms - WikipediaNguyen Vu DoanNo ratings yet

- Manual Bank Reconciliation StatementDocument11 pagesManual Bank Reconciliation StatementAnandNo ratings yet

- Mobile Banking Codes PaybillDocument2 pagesMobile Banking Codes PaybillMauriceNo ratings yet

- Champions Cattle Case Study - Scrutinized During ReportDocument5 pagesChampions Cattle Case Study - Scrutinized During Reportdoy joyNo ratings yet

- Valuasi Ekonomi Penambangan Sumberdaya Belerang Kawah Ijen, Desa Tamansari, Kabupaten Banyuwangi, Provinsi Jawa Timur Latifatul KhoiriyahDocument10 pagesValuasi Ekonomi Penambangan Sumberdaya Belerang Kawah Ijen, Desa Tamansari, Kabupaten Banyuwangi, Provinsi Jawa Timur Latifatul Khoiriyahferdin sitinjakNo ratings yet

- Chapter 8 (Concept of Capital and C Maintainance) PDFDocument3 pagesChapter 8 (Concept of Capital and C Maintainance) PDFNadia ZahraNo ratings yet

- Project Report ON: A Study On Customer Satisfaction Towards Banking Services of State Bank of India in Kolkata Region"Document65 pagesProject Report ON: A Study On Customer Satisfaction Towards Banking Services of State Bank of India in Kolkata Region"Lucky MishraNo ratings yet

- Role of It in BankingDocument5 pagesRole of It in BankingSamaira SheikhNo ratings yet

- Due Diligence and ValuationDocument32 pagesDue Diligence and ValuationM. SiddiqueNo ratings yet

- Daftar Akun RenataDocument3 pagesDaftar Akun RenataFitriRahmanNo ratings yet

- Ebook Intermediate Accounting Reporting and Analysis PDF Full Chapter PDFDocument61 pagesEbook Intermediate Accounting Reporting and Analysis PDF Full Chapter PDFjulia.castro488100% (39)

- Premium ReceiptsDocument1 pagePremium ReceiptsRajNo ratings yet

- Deloitte Risk Management SurveyDocument40 pagesDeloitte Risk Management SurveyJohn Carney86% (7)

- PSRE-2400 Review EngagementDocument26 pagesPSRE-2400 Review EngagementMAG MAGNo ratings yet

- Placement Training Centre Bank Interview Questions and AnswersDocument20 pagesPlacement Training Centre Bank Interview Questions and AnswershariNo ratings yet