0% found this document useful (0 votes)

148 viewsAfar Solution

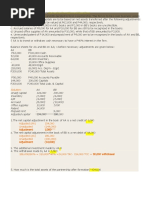

The document shows the profit allocation for partner A in a partnership. It details that A earned Rs. 30,000 in interest on capital, Rs. 160,000 in salary, and Rs. 150,000 bonus. A's equal share in remaining profit was Rs. 200,000, bringing their total profit share to Rs. 540,000. The partnership profit for the year was Rs. 1,050,000, of which Rs. 300,000 was used for interest and salary. The remaining Rs. 750,000 was subject to A's 20% bonus of Rs. 150,000.

Uploaded by

Tk KimCopyright

© © All Rights Reserved

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

148 viewsAfar Solution

The document shows the profit allocation for partner A in a partnership. It details that A earned Rs. 30,000 in interest on capital, Rs. 160,000 in salary, and Rs. 150,000 bonus. A's equal share in remaining profit was Rs. 200,000, bringing their total profit share to Rs. 540,000. The partnership profit for the year was Rs. 1,050,000, of which Rs. 300,000 was used for interest and salary. The remaining Rs. 750,000 was subject to A's 20% bonus of Rs. 150,000.

Uploaded by

Tk KimCopyright

© © All Rights Reserved

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

/ 2