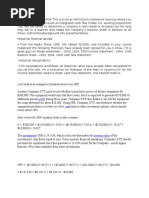

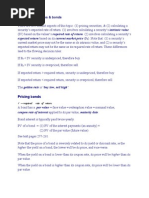

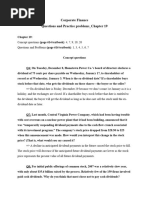

BA4811 Corporate Finance Fall 2020-2021 Exam 2

BA4811 Corporate Finance Fall 2020-2021 Exam 2

Download as docx, pdf, or txt

You might also like

- Voyages Soleil The Hedging Decision - AnswersDocument3 pagesVoyages Soleil The Hedging Decision - AnswersEdNo ratings yet

- FIN 300 - Cheat SheetDocument2 pagesFIN 300 - Cheat SheetStephanie NaamaniNo ratings yet

- Typical Cash Flows at The Start: Cost of Machines (200.000, Posses, So On Balance SheetDocument7 pagesTypical Cash Flows at The Start: Cost of Machines (200.000, Posses, So On Balance SheetSylvan EversNo ratings yet

- Wek 5 HomeworkDocument5 pagesWek 5 HomeworkJobarteh FofanaNo ratings yet

- Cash Flow EstimationDocument9 pagesCash Flow EstimationCassandra ChewNo ratings yet

- History of Linear ProgrammingDocument3 pagesHistory of Linear ProgrammingEdNo ratings yet

- Financial Statement Analysis ExerciseDocument5 pagesFinancial Statement Analysis ExerciseMelanie SamsonaNo ratings yet

- Exam 3 - Questions AnswersDocument10 pagesExam 3 - Questions Answersonetwothree3524No ratings yet

- Finance Problem SetDocument9 pagesFinance Problem Setisgigles157No ratings yet

- Principles of Finance Work BookDocument53 pagesPrinciples of Finance Work BookNicole MartinezNo ratings yet

- Interest Bond CalculatorDocument6 pagesInterest Bond CalculatorfdfsfsdfjhgjghNo ratings yet

- Ôn Tập Cuối Kỳ TCDN Kì I 2023 2024Document10 pagesÔn Tập Cuối Kỳ TCDN Kì I 2023 2024doithuhuongNo ratings yet

- SFMSOLUTIONS Master Minds PDFDocument10 pagesSFMSOLUTIONS Master Minds PDFHari KrishnaNo ratings yet

- Selected QuestionsDocument5 pagesSelected QuestionsMazhar AliNo ratings yet

- Test 3 Corprate FinanceDocument10 pagesTest 3 Corprate FinancekeelyNo ratings yet

- BA4811 Corporate Finance Fall 2020-2021 Exam 1Document4 pagesBA4811 Corporate Finance Fall 2020-2021 Exam 1EdNo ratings yet

- Cost of CapitalDocument23 pagesCost of CapitalAsad AliNo ratings yet

- Summary - Cost of CapitalDocument13 pagesSummary - Cost of Capitaldhn4591100% (1)

- Corporate FinanceDocument10 pagesCorporate FinancesurimuskansuriNo ratings yet

- Stock and Its Valuation: The Application of The Present Value ConceptDocument37 pagesStock and Its Valuation: The Application of The Present Value Concepter_aritraNo ratings yet

- Leasing Vs BuyingDocument5 pagesLeasing Vs BuyingOviyan IlancheranNo ratings yet

- Solutions To Quiz 1Document4 pagesSolutions To Quiz 1Chakri MunagalaNo ratings yet

- HW12Document7 pagesHW12nma.work173No ratings yet

- CF Final 2020 Preparation Answers: B. Payback PeriodDocument5 pagesCF Final 2020 Preparation Answers: B. Payback PeriodXatia Sirginava100% (1)

- FIN211 Financial Management Lecture NotesDocument8 pagesFIN211 Financial Management Lecture NotesNiket R. ShahNo ratings yet

- EF343.FSM (AL-I) Solution CMA January-2023 Exam.Document4 pagesEF343.FSM (AL-I) Solution CMA January-2023 Exam.GT Moringa LimitedNo ratings yet

- Time Value of Money FormulasDocument8 pagesTime Value of Money FormulasrovosoloNo ratings yet

- 1) Important Terms: Earning MoneyDocument9 pages1) Important Terms: Earning MoneyMaria DeeTee NguyenNo ratings yet

- TTM 10 Time Value of Money - LanjutanDocument58 pagesTTM 10 Time Value of Money - LanjutanDede KurniatiNo ratings yet

- Real Estate Investment CalculationsDocument12 pagesReal Estate Investment CalculationsJorge Nunes100% (1)

- CF - Questions and Practice Problems - Chapter 18Document5 pagesCF - Questions and Practice Problems - Chapter 18Mai PhạmNo ratings yet

- Present ValueDocument38 pagesPresent Valuemarjannaseri77100% (1)

- Expected Return Based On Its Current Market Price (P: Valuation of Shares & BondsDocument8 pagesExpected Return Based On Its Current Market Price (P: Valuation of Shares & Bondsv_viswaprakash3814No ratings yet

- Materi 210312Document71 pagesMateri 210312Novita HalimNo ratings yet

- Banking, Inflation and Exchange Rates Notes and QuestionsDocument22 pagesBanking, Inflation and Exchange Rates Notes and QuestionsKelvinNo ratings yet

- AnnuitiesDocument13 pagesAnnuitiesjabbimuhammed50No ratings yet

- 2019 Exam - Moed A - Computer Science - (Solution)Document11 pages2019 Exam - Moed A - Computer Science - (Solution)adoNo ratings yet

- FM ch-3 PP ... EDITEDDocument21 pagesFM ch-3 PP ... EDITEDswalih mohammedNo ratings yet

- Solution:: Operating Profit RatioDocument8 pagesSolution:: Operating Profit RatioMuhammad DaniSh ManZoorNo ratings yet

- ANNUITY NADocument10 pagesANNUITY NAbnigerian9No ratings yet

- 1.1 What Is Their Profit Margin? Profit MarginDocument16 pages1.1 What Is Their Profit Margin? Profit MarginVenay SahadeoNo ratings yet

- Corporate FinanceDocument16 pagesCorporate FinanceSale EdupartnerNo ratings yet

- Financial Management-Lecture 7Document26 pagesFinancial Management-Lecture 7TinoManhangaNo ratings yet

- Chapter 1: Answers To Questions and Problems: Managerial Economics and Business Strategy, 4eDocument5 pagesChapter 1: Answers To Questions and Problems: Managerial Economics and Business Strategy, 4eadityaintouchNo ratings yet

- Corporate FinanceDocument5 pagesCorporate FinanceanusuyagaudNo ratings yet

- Chapter 006Document60 pagesChapter 006aisha belucciNo ratings yet

- Finc600 Chapter 2 PPTDocument41 pagesFinc600 Chapter 2 PPTmnh2006No ratings yet

- Earnings Per ShareDocument30 pagesEarnings Per ShareTanka P Chettri100% (1)

- Lec8.Cost of CapitalDocument52 pagesLec8.Cost of Capitalvivek patelNo ratings yet

- Bond Solution ProblemsDocument7 pagesBond Solution ProblemsNojoke1No ratings yet

- Finance OverviewDocument19 pagesFinance OverviewyomoNo ratings yet

- CBA Exercise Sheet - English Revised Oct 2016Document15 pagesCBA Exercise Sheet - English Revised Oct 2016pravin mundeNo ratings yet

- Lecture3Document11 pagesLecture3vnhinguyen1812No ratings yet

- Acc. Valuations and use of Free Cash flowDocument10 pagesAcc. Valuations and use of Free Cash flowhapfyNo ratings yet

- CF - Questions and Practice Problems - Chapter 19Document7 pagesCF - Questions and Practice Problems - Chapter 19Mai PhạmNo ratings yet

- Assignment1 SolutionDocument9 pagesAssignment1 SolutionAlexa Mouawad100% (1)

- 644 - Corporate Finance SolutionDocument7 pages644 - Corporate Finance Solutionrayan.wydouwNo ratings yet

- COCDocument48 pagesCOCDeepak KumarNo ratings yet

- Markup: Prepared By: Ruwen BugayDocument26 pagesMarkup: Prepared By: Ruwen BugayFaye Nathalie MontesNo ratings yet

- 6 7 TVMDocument31 pages6 7 TVMaannisa pdNo ratings yet

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- Information Systems in Global Business TodayDocument9 pagesInformation Systems in Global Business TodayEdNo ratings yet

- Maximal Flow Problem: ConstraintsDocument4 pagesMaximal Flow Problem: ConstraintsEdNo ratings yet

- Solution For Mini Exam 4Document3 pagesSolution For Mini Exam 4EdNo ratings yet

- BA4811 Corporate Finance Fall 2020-2021 Exam 1Document4 pagesBA4811 Corporate Finance Fall 2020-2021 Exam 1EdNo ratings yet

- Shortest Path Problem: ConstraintsDocument4 pagesShortest Path Problem: ConstraintsEdNo ratings yet

- Case StudyDocument5 pagesCase StudyEdNo ratings yet

- Odaiko ElectronicsDocument3 pagesOdaiko ElectronicsEdNo ratings yet

- The Theory of Financial IntermediationDocument3 pagesThe Theory of Financial IntermediationEdNo ratings yet

- The Market For 'Lemons'': Quality Uncertainty and The Market MechanismDocument3 pagesThe Market For 'Lemons'': Quality Uncertainty and The Market MechanismEdNo ratings yet

- Process CostingDocument35 pagesProcess CostingAditya Chandrayan75% (4)

- Govacctg New PDFDocument190 pagesGovacctg New PDFJasmine Lim100% (1)

- The Income and Expenditure Account of Sweet Club For The Year 2021 Is AsDocument4 pagesThe Income and Expenditure Account of Sweet Club For The Year 2021 Is AsBAZINGANo ratings yet

- Comptes Consolidés 31 Décembre 2022 vENGDocument143 pagesComptes Consolidés 31 Décembre 2022 vENGUmar MasaudNo ratings yet

- Managerial Accounting: Topic 3 Manufacturing Costs - Hilton 12thDocument37 pagesManagerial Accounting: Topic 3 Manufacturing Costs - Hilton 12thنور عفيفه100% (1)

- Income Tax MCQDocument10 pagesIncome Tax MCQGlem Maquiling JosolNo ratings yet

- Chapter 5 Consolidated FS - Part 2Document13 pagesChapter 5 Consolidated FS - Part 2Geraldine Mae DamoslogNo ratings yet

- INTERCOMPANY TRANSACTIONsDocument3 pagesINTERCOMPANY TRANSACTIONsChelle CastuloNo ratings yet

- Cash FlowDocument60 pagesCash FlowMoo Jhan FaiNo ratings yet

- Presentation Made To Analysts/Investors Meeting (Company Update)Document28 pagesPresentation Made To Analysts/Investors Meeting (Company Update)Shyam Sunder100% (1)

- Journal Entries For Stockholders' EquityDocument2 pagesJournal Entries For Stockholders' EquityMary100% (11)

- 20 Air Canada vs. Commissioner of Internal RevenueDocument30 pages20 Air Canada vs. Commissioner of Internal Revenueshlm bNo ratings yet

- Asset-V1 MITx+15.516x+1T2024+type@asset+block@516x 2024 Week 4 Recitation HandoutsDocument18 pagesAsset-V1 MITx+15.516x+1T2024+type@asset+block@516x 2024 Week 4 Recitation HandoutsMarkus_MardenNo ratings yet

- Consolidated Financials Q4FY24Document10 pagesConsolidated Financials Q4FY24Akash KushwahaNo ratings yet

- Ar Mbi 2018 PDFDocument261 pagesAr Mbi 2018 PDFsherlijulianiNo ratings yet

- RD1219297071519Document1 pageRD1219297071519KIRANKUMARNo ratings yet

- CDD Acctg. For Bus - Co Preliminary ExaminationDocument25 pagesCDD Acctg. For Bus - Co Preliminary ExaminationMaryjoy Sarzadilla JuanataNo ratings yet

- I Tax Calculation 23-24Document5 pagesI Tax Calculation 23-24vikas2354_268878339No ratings yet

- Problem 1: 1 Reed CompanyDocument16 pagesProblem 1: 1 Reed CompanySarah Nelle PasaoNo ratings yet

- VOdafone CaseDocument1 pageVOdafone CaseAnoopKumarMangarajNo ratings yet

- Chap016 CondensedDocument8 pagesChap016 Condenseddodgeintrepid1996No ratings yet

- Analysis Beyond Consensus: The New Abc of ResearchDocument15 pagesAnalysis Beyond Consensus: The New Abc of ResearchRimjhim BhatiaNo ratings yet

- Unit 4 IAPM FM 01Document42 pagesUnit 4 IAPM FM 01areumkim261No ratings yet

- Capital BudgetingDocument14 pagesCapital BudgetingKakumbi Shukhovu ChitiNo ratings yet

- TFCO - Annual Report 2019 - LAMPDocument83 pagesTFCO - Annual Report 2019 - LAMProsida ibrahimNo ratings yet

- Reorganization and Troubled Debt Restructuring-MCDocument2 pagesReorganization and Troubled Debt Restructuring-MCRachelle AlmirañezNo ratings yet

- Chapter-4 Marginal CostingDocument11 pagesChapter-4 Marginal Costingbramara mutteNo ratings yet

- ExtAud 3 Quiz 4 Wo AnswersDocument5 pagesExtAud 3 Quiz 4 Wo AnswersJANET ILLESESNo ratings yet

- MGT401 Short Notes Lec 1 - 45Document33 pagesMGT401 Short Notes Lec 1 - 45HRrehmanNo ratings yet