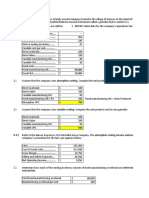

Chapter 7 Problems PDF

Chapter 7 Problems PDF

Download as pdf or txt

You might also like

- DocDocument13 pagesDocIbnu Bang BangNo ratings yet

- Chapter 4 Questions SolutionsDocument2 pagesChapter 4 Questions Solutionscamd1290100% (2)

- 2010-09-27 104244 AdvancedDocument11 pages2010-09-27 104244 Advancedhetalcar100% (1)

- Chapter 12 Factory Over Head Planned Actual and Applied Variance AnalysisDocument29 pagesChapter 12 Factory Over Head Planned Actual and Applied Variance AnalysisAthar ComsatsNo ratings yet

- IProtect Produces Covers For All Makes and Models of IPadsDocument2 pagesIProtect Produces Covers For All Makes and Models of IPadsElliot Richard0% (1)

- Answer Key Chap 1 3Document18 pagesAnswer Key Chap 1 3Huy Hoàng PhanNo ratings yet

- Discussion - Example Problem of Keep or Drop DecisionsDocument2 pagesDiscussion - Example Problem of Keep or Drop DecisionsGiselle Martinez0% (1)

- Chapter 3 AnswersDocument47 pagesChapter 3 AnswersPattranite100% (1)

- MA1MDocument14 pagesMA1MAbdullah NafeesNo ratings yet

- Horngren Cost 7ce ISM Ch14Document36 pagesHorngren Cost 7ce ISM Ch14Alan WenNo ratings yet

- TS2022 User Guide enDocument87 pagesTS2022 User Guide enRodrigo Ferreira de LimaNo ratings yet

- Assignment On CH 3 and 4 Cost 2Document4 pagesAssignment On CH 3 and 4 Cost 2sadiya AbrahimNo ratings yet

- Exercise 8-26 Cost Classification: RequirementDocument153 pagesExercise 8-26 Cost Classification: RequirementIkram100% (1)

- SM Horngren Cost Accounting 14e Ch17Document48 pagesSM Horngren Cost Accounting 14e Ch17Shrouk__Anas100% (2)

- CH 11+16th+globalDocument37 pagesCH 11+16th+globalAmina SultangaliyevaNo ratings yet

- BAB 16 v2Document10 pagesBAB 16 v2rahmat lubisNo ratings yet

- ACCT 3125 Chapter 5 SolutionsDocument7 pagesACCT 3125 Chapter 5 SolutionskayNo ratings yet

- Standard Costs and The Balanced ScorecardDocument32 pagesStandard Costs and The Balanced ScorecardfaheemNo ratings yet

- Differential Analysis Lecture Notes 1Document18 pagesDifferential Analysis Lecture Notes 1Yesaya SetiawanNo ratings yet

- Cost Accounting ch05Document57 pagesCost Accounting ch05samas7480100% (2)

- XLSXDocument28 pagesXLSXnaura syahdaNo ratings yet

- Lucky Carrot : Show Transcribed Image TextDocument2 pagesLucky Carrot : Show Transcribed Image TextAchmad RizalNo ratings yet

- P2 41 2 42 SolutionsDocument3 pagesP2 41 2 42 SolutionsMarjorie PalmaNo ratings yet

- Chapter 17Document8 pagesChapter 17rahmiamelianazarNo ratings yet

- Chapter 4-Exercises-Managerial AccountingDocument3 pagesChapter 4-Exercises-Managerial AccountingSheila Mae LiraNo ratings yet

- CH 2 Solutions Solution S For Chapter 2Document20 pagesCH 2 Solutions Solution S For Chapter 2Getachew MuluNo ratings yet

- 18-40 Spoilage in Job Costing: 1. What Is The Normal Spoilage Rate?Document4 pages18-40 Spoilage in Job Costing: 1. What Is The Normal Spoilage Rate?Von Andrei Medina100% (1)

- 4-28. Job Costing Actual, Normal, and Variation From Normal CostingDocument2 pages4-28. Job Costing Actual, Normal, and Variation From Normal CostingFadilah Kamilah100% (1)

- 1 Intermediate Accounting IFRS 3rd Edition-554-569Document16 pages1 Intermediate Accounting IFRS 3rd Edition-554-569Khofifah SalmahNo ratings yet

- CH 08 SMDocument25 pagesCH 08 SMNafisah Mambuay100% (1)

- BAB 5 Cost Volume Profit RelationshipsDocument61 pagesBAB 5 Cost Volume Profit RelationshipsNurainin AnsarNo ratings yet

- Evan and Brett Are Students at Berkeley CollegeDocument3 pagesEvan and Brett Are Students at Berkeley CollegeElliot RichardNo ratings yet

- Cost Accounting and Cost Management 1 Accounting For Factory OverheadDocument19 pagesCost Accounting and Cost Management 1 Accounting For Factory OverheadJamaica David100% (1)

- Essence Company Blends and Sells Designer FragrancesDocument2 pagesEssence Company Blends and Sells Designer FragrancesElliot Richard100% (1)

- Chapter12 - AnswerDocument442 pagesChapter12 - AnswerKlowee E. Peñafiel100% (1)

- Managerial Accounting Chapter 8 & 9 SolutionsDocument8 pagesManagerial Accounting Chapter 8 & 9 SolutionsJotham NyanjeNo ratings yet

- Pricing SW1Document5 pagesPricing SW1DeniseNo ratings yet

- Review Problem: Activity-Based Costing: RequiredDocument11 pagesReview Problem: Activity-Based Costing: RequiredTunvir SyncNo ratings yet

- Programmazione e Controllo Esercizi Capi PDFDocument43 pagesProgrammazione e Controllo Esercizi Capi PDFHeap Ke XinNo ratings yet

- Dunn, Inc., Is A Privately Held Furniture Manufacturer. For August 2014, Dunn Had The Following Standards For One of Its ProductDocument1 pageDunn, Inc., Is A Privately Held Furniture Manufacturer. For August 2014, Dunn Had The Following Standards For One of Its ProductAishwarya RaoNo ratings yet

- MAKSI - UI - LatihanKuis - Okt 2019Document8 pagesMAKSI - UI - LatihanKuis - Okt 2019aziezoel100% (1)

- Vanderbeck Solman ch01-10Document288 pagesVanderbeck Solman ch01-10Jelly AceNo ratings yet

- ASM2 BAFI3184 s3818425 LyAnhTuan-2Document9 pagesASM2 BAFI3184 s3818425 LyAnhTuan-2tuan lyNo ratings yet

- E7-39 Comparing ABC and Plantwide Overhead Cost Assigments: Setup Hours Oven HoursDocument3 pagesE7-39 Comparing ABC and Plantwide Overhead Cost Assigments: Setup Hours Oven HoursDhiva Rianitha Manurung100% (1)

- Cost-Volume-Profit: Prepared by Meifida IlyasDocument64 pagesCost-Volume-Profit: Prepared by Meifida IlyasDixi AndriantoNo ratings yet

- Dokumen - Tips - Jawaban Soal Akmen Bab 8 PDFDocument44 pagesDokumen - Tips - Jawaban Soal Akmen Bab 8 PDFSiswo WartoyoNo ratings yet

- Chapter 12 SolutionsDocument29 pagesChapter 12 SolutionsAnik Kumar MallickNo ratings yet

- Flexible Budgets&Standard Cost SystemDocument27 pagesFlexible Budgets&Standard Cost SystemAsteway Mesfin100% (1)

- Yohanes Bosko Arya B - 041711333195 - AKM E23.11, P23.4Document3 pagesYohanes Bosko Arya B - 041711333195 - AKM E23.11, P23.4ulil alfarisyNo ratings yet

- Answer:: Per Unit Total For 20 BraceletsDocument2 pagesAnswer:: Per Unit Total For 20 BraceletsEevan SalazarNo ratings yet

- Chapter 5 Activity Based Costing and Activity Based ManagementDocument69 pagesChapter 5 Activity Based Costing and Activity Based Managementkhushboo100% (2)

- Chapter 3 - Part 2Document9 pagesChapter 3 - Part 2Aya MasoudNo ratings yet

- Chapter 3 Job Order CostingDocument31 pagesChapter 3 Job Order CostingzamanNo ratings yet

- 202-0101-001 - ARIF HOSEN - Management Accounting Assignment 1Document11 pages202-0101-001 - ARIF HOSEN - Management Accounting Assignment 1Sayhan Hosen Arif100% (1)

- Consolidated Financial Statement Excercise 3-3Document2 pagesConsolidated Financial Statement Excercise 3-3Winnie TanNo ratings yet

- MGMT 027 Connect 04 HWDocument7 pagesMGMT 027 Connect 04 HWSidra Khan100% (1)

- Accounting Principles 10th Edition Weygandt Kimmel Chapter 3 PDFDocument139 pagesAccounting Principles 10th Edition Weygandt Kimmel Chapter 3 PDFbeenie manNo ratings yet

- Strategy, Balanced Scorecard, and Strategic Profitability Analysis 13-1 13-2Document40 pagesStrategy, Balanced Scorecard, and Strategic Profitability Analysis 13-1 13-2Ratiu SilviuNo ratings yet

- Chapter 7 Practice QuestionsDocument12 pagesChapter 7 Practice QuestionsZethu JoeNo ratings yet

- Chap 7 - Flexible Budget, Direct Cost Variance and Management Control - Students NoteDocument13 pagesChap 7 - Flexible Budget, Direct Cost Variance and Management Control - Students NoteZulIzzamreeZolkepliNo ratings yet

- Standard Costing and Variance AnalysisDocument14 pagesStandard Costing and Variance AnalysisSaad Khan YTNo ratings yet

- Correlationof Consistencyand Compressibility Propertiesof Soilsin Sulaimani CityDocument9 pagesCorrelationof Consistencyand Compressibility Propertiesof Soilsin Sulaimani CityArham SheikhNo ratings yet

- Permeability Coefficient of Low Permeable Soils AsDocument21 pagesPermeability Coefficient of Low Permeable Soils AsArham SheikhNo ratings yet

- Nawari 1991Document26 pagesNawari 1991Arham SheikhNo ratings yet

- 2023 24 February Entry Admission Guidelines For Intl Degree StudentsDocument8 pages2023 24 February Entry Admission Guidelines For Intl Degree StudentsArham SheikhNo ratings yet

- Impact of Worker's Remittance From M.E On Pakistan EconomyDocument30 pagesImpact of Worker's Remittance From M.E On Pakistan EconomyArham SheikhNo ratings yet

- Civl Engineer Interview QuestionsDocument139 pagesCivl Engineer Interview QuestionsArham SheikhNo ratings yet

- Design and Simulation of An Automatic Room Heater Control SystemDocument18 pagesDesign and Simulation of An Automatic Room Heater Control SystemArham SheikhNo ratings yet

- Pakistan Remittances Initiative and Remittance Flows To PakistanDocument27 pagesPakistan Remittances Initiative and Remittance Flows To PakistanArham SheikhNo ratings yet

- Remittances and Household WelfareDocument51 pagesRemittances and Household WelfareArham SheikhNo ratings yet

- Remittances For GrowthDocument18 pagesRemittances For GrowthArham SheikhNo ratings yet

- Conversion Gate01Document31 pagesConversion Gate01Arham SheikhNo ratings yet

- A Portable Electrocardiogram For Real Time Monitoring of CardiacDocument11 pagesA Portable Electrocardiogram For Real Time Monitoring of CardiacArham SheikhNo ratings yet

- Biosafety: Siji Skariah M.SC Botany ST - Thomas College KozhencherryDocument37 pagesBiosafety: Siji Skariah M.SC Botany ST - Thomas College KozhencherryArham SheikhNo ratings yet

- 93DSS JRP JJBIJETTIJETT V4I8P141Volume4Issue8 August2013Document6 pages93DSS JRP JJBIJETTIJETT V4I8P141Volume4Issue8 August2013Arham SheikhNo ratings yet

- Cardiovascular Diseases Traditional and Non-TraditDocument7 pagesCardiovascular Diseases Traditional and Non-TraditArham SheikhNo ratings yet

- Selected Solutions Chap 6 8Document49 pagesSelected Solutions Chap 6 8Arham SheikhNo ratings yet

- PMDG 737NXG Dark and Cold TutorialDocument23 pagesPMDG 737NXG Dark and Cold Tutorialluca26288% (17)

- 58MM Thermal Reciept Printer Operating Manual-20160805 PDFDocument13 pages58MM Thermal Reciept Printer Operating Manual-20160805 PDFteguhNo ratings yet

- Class 10 - Experiment 13-16Document8 pagesClass 10 - Experiment 13-16bengiajomin424No ratings yet

- BookChapter - Design and Performance Analysis of Controlled DC-DC ConverterDocument23 pagesBookChapter - Design and Performance Analysis of Controlled DC-DC ConvertersivakrishnaNo ratings yet

- (20190910) Policy of Ambulance Safety in Pre-Hospital Care Services in Ministry of Health Malaysia - LATEST EditDocument47 pages(20190910) Policy of Ambulance Safety in Pre-Hospital Care Services in Ministry of Health Malaysia - LATEST EditharilNo ratings yet

- Assessing The Information Needs of The CompanyDocument2 pagesAssessing The Information Needs of The CompanyAlexNo ratings yet

- SopDocument19 pagesSopAbdul RazzaqNo ratings yet

- Glow Plug System - Ingenium I4 2.0L Diesel Description and OperationDocument7 pagesGlow Plug System - Ingenium I4 2.0L Diesel Description and Operationatron88No ratings yet

- MRP, DP & BP - 031219055159 PDFDocument22 pagesMRP, DP & BP - 031219055159 PDFbidyut naskarNo ratings yet

- Four Types of Phrasal VerbsDocument5 pagesFour Types of Phrasal VerbsNicoletaNicoleta100% (1)

- COMP 122 COMP 121 DISCRETE MATHEMATICS May August 2019Document3 pagesCOMP 122 COMP 121 DISCRETE MATHEMATICS May August 2019victor kimutaiNo ratings yet

- Abstract Estimate Based On Current RatesDocument2 pagesAbstract Estimate Based On Current RatesSandeep KolappuramNo ratings yet

- Main Frame: Model Number: 863 Serial Number: 514411001 Thru 514439999, 514511001 Thru 514539999, 514611001 Thru 514639999Document3 pagesMain Frame: Model Number: 863 Serial Number: 514411001 Thru 514439999, 514511001 Thru 514539999, 514611001 Thru 514639999Romario LoiolaNo ratings yet

- Standard Practices ManualDocument98 pagesStandard Practices Manualgugu carterNo ratings yet

- K. Chitra, Et Al PDFDocument5 pagesK. Chitra, Et Al PDFNeena Bharti0% (1)

- Mad NotesDocument12 pagesMad NotesLisa FiverNo ratings yet

- CHM260 SWR Experiment 2Document6 pagesCHM260 SWR Experiment 2wnayNo ratings yet

- APTIS Writing Part 4Document11 pagesAPTIS Writing Part 4LaraNo ratings yet

- Honda Markaya Ozel Ariza KoduDocument2 pagesHonda Markaya Ozel Ariza KoduAlican AyginNo ratings yet

- Calculator Tricks + Number SystemDocument19 pagesCalculator Tricks + Number SystemRajeshwari ShuklaNo ratings yet

- Testing and Adjusting 12GDocument5 pagesTesting and Adjusting 12GJuan GonzalezNo ratings yet

- Promotion Strategies of McdonaldDocument34 pagesPromotion Strategies of McdonaldIndira Thayil100% (2)

- 4-Module 2 - Objectives of Shunt Connected FCATS Devices-04!08!2023Document20 pages4-Module 2 - Objectives of Shunt Connected FCATS Devices-04!08!2023saran killerNo ratings yet

- Distillation Column Design (Trial and Error)Document29 pagesDistillation Column Design (Trial and Error)AlexandraBarbeConawayNo ratings yet

- S 355 J2 + NDocument1 pageS 355 J2 + NValentin GalbenNo ratings yet

- Two-Way Slab Design Using The Coefficient MethodDocument7 pagesTwo-Way Slab Design Using The Coefficient MethodJason Edwards97% (66)

- NSK SelfDocument4 pagesNSK SelfChandru VelNo ratings yet

- Chem Mid Term and Answer KeyDocument10 pagesChem Mid Term and Answer KeyNatasha Kishore PandaranNo ratings yet

- Popular Mechanics USA 11 12 2024 Freemagazines TopDocument80 pagesPopular Mechanics USA 11 12 2024 Freemagazines TopcelestinethraexNo ratings yet