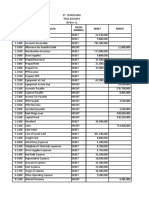

The Balance Sheet

The Balance Sheet

Download as docx, pdf, or txt

You might also like

- Universiti Teknologi Mara Final Assessment: Confidential 1 AC/JUL 2022/MAF503Document10 pagesUniversiti Teknologi Mara Final Assessment: Confidential 1 AC/JUL 2022/MAF503Alyn AdnanNo ratings yet

- Management of Banking OperationDocument206 pagesManagement of Banking OperationAtul BharshankarNo ratings yet

- Chapter 16 Credit AgreementsDocument56 pagesChapter 16 Credit AgreementsBekithemba MliloNo ratings yet

- Lead Schedule: Refer To The Attached Sample Bank Confirmation TemplateDocument4 pagesLead Schedule: Refer To The Attached Sample Bank Confirmation TemplateChristian Dela CruzNo ratings yet

- Lockbox Power PointDocument19 pagesLockbox Power Pointasrinu88881125100% (1)

- Ecommerce PresentationDocument9 pagesEcommerce PresentationSurabhi AgrawalNo ratings yet

- 5602 PDFDocument301 pages5602 PDFRabia JanNo ratings yet

- Mastercom User GuideDocument232 pagesMastercom User GuideMario Cortez EscárateNo ratings yet

- Franking User Manual V2.0Document159 pagesFranking User Manual V2.0Hyderabad Postal RegionNo ratings yet

- CDB1 Current AccountDocument9 pagesCDB1 Current Accountsvm kishoreNo ratings yet

- National Law Institute University, Bhopal: Basics of E-BankingDocument21 pagesNational Law Institute University, Bhopal: Basics of E-BankingDikshaNo ratings yet

- NIL - Discharge Cases Negotiable InstrumentsDocument8 pagesNIL - Discharge Cases Negotiable Instrumentsblackphoenix303No ratings yet

- Loan Management User GuideDocument22 pagesLoan Management User GuideNye LavalleNo ratings yet

- Retail BankingDocument56 pagesRetail BankingProf Dr Chowdari Prasad100% (20)

- Banking Awareness ImportantDocument30 pagesBanking Awareness ImportantThirrunavukkarasu R RNo ratings yet

- Deposit Card AgreementDocument7 pagesDeposit Card AgreementDavid ValdezNo ratings yet

- Adjustments of Final AccountsDocument11 pagesAdjustments of Final AccountsUmesh Gaikwad50% (10)

- Typesof ClearingDocument3 pagesTypesof Clearingteliumar100% (1)

- Prepare and Match ReciptsDocument15 pagesPrepare and Match Reciptstafese kuracheNo ratings yet

- Concurrent AuditDocument7 pagesConcurrent AuditCA Harsh Satish UdeshiNo ratings yet

- Deposit SlipDocument1 pageDeposit SlipHabibie GunawanNo ratings yet

- Guide To Accounting For Financial InstrumentsDocument12 pagesGuide To Accounting For Financial InstrumentsRobin Saha100% (1)

- AttachmentDocument31 pagesAttachmentHambaNo ratings yet

- Advanced Bank Reconciliation 2010 PDFDocument96 pagesAdvanced Bank Reconciliation 2010 PDFcallmeasthaNo ratings yet

- Ch08 ReceivablesDocument42 pagesCh08 ReceivablesGelyn CruzNo ratings yet

- A Cheque Is A DocumentDocument15 pagesA Cheque Is A Documentmi06bba030No ratings yet

- Mak Magic Gas SaverDocument1 pageMak Magic Gas SaverSarah EllisNo ratings yet

- Comercial BanksDocument21 pagesComercial BanksSanto AntonyNo ratings yet

- SEPA Creditors GuideDocument30 pagesSEPA Creditors GuideamraouaNo ratings yet

- CFPB Your Money Your Goals Choosing Paid ToolDocument6 pagesCFPB Your Money Your Goals Choosing Paid ToolJocelyn CyrNo ratings yet

- Statutory Bank Audits Practical Aspect Prepared by - Bhargav NathwaniDocument20 pagesStatutory Bank Audits Practical Aspect Prepared by - Bhargav NathwaniAkash SingrodiaNo ratings yet

- Depository and Settlement SystemsDocument34 pagesDepository and Settlement Systemsarchana_anuragiNo ratings yet

- Funding Your COL AccountDocument17 pagesFunding Your COL AccountAnne ReyesNo ratings yet

- Dimensions of Cash Flow Management: Prof. N. C. KarDocument74 pagesDimensions of Cash Flow Management: Prof. N. C. KarAshok100% (1)

- UntitledDocument51 pagesUntitledNina KondićNo ratings yet

- BlackbookDocument55 pagesBlackbookYashasvi ShekhawatNo ratings yet

- General Closing Requirements - GuideDocument29 pagesGeneral Closing Requirements - GuideRicharnellia-RichieRichBattiest-Collins100% (1)

- A Look Inside UPS FedEx and USPS Declared Value Policies For The Parcel ShipperDocument18 pagesA Look Inside UPS FedEx and USPS Declared Value Policies For The Parcel Shipperattom8515100% (2)

- Authentication Process in USDocument2 pagesAuthentication Process in USXian VillarazaNo ratings yet

- Proposals For The Treasury, The Federal Reserve, The FDIC, andDocument6 pagesProposals For The Treasury, The Federal Reserve, The FDIC, andapi-25896854No ratings yet

- Client Manual Consumer Banking - CitibankDocument29 pagesClient Manual Consumer Banking - CitibankNGUYEN HUU THUNo ratings yet

- Automated Bitcoin TradingDocument5 pagesAutomated Bitcoin TradingErnst StavroNo ratings yet

- General Banking TermsDocument17 pagesGeneral Banking TermsVineeth JoseNo ratings yet

- Real AccountingDocument22 pagesReal Accountingakbar2jNo ratings yet

- Credit Card Setup in AR Document 1357967Document11 pagesCredit Card Setup in AR Document 1357967Madhuri UppalaNo ratings yet

- Adjusting EntriesDocument23 pagesAdjusting Entriestoobaahmedkhan100% (1)

- Verification of AdvancesDocument12 pagesVerification of AdvancesAvinash SinyalNo ratings yet

- Ocwen Q3Q4Document24 pagesOcwen Q3Q4Foreclosure FraudNo ratings yet

- Diamond AccountDocument2 pagesDiamond AccountJagadeesh YathirajulaNo ratings yet

- Merged Fa Cwa NotesDocument799 pagesMerged Fa Cwa NotesAkash VaidNo ratings yet

- Unit 10 AB Financial AccountingDocument5 pagesUnit 10 AB Financial AccountingAlamzeb KhanNo ratings yet

- Features of Credit CardDocument11 pagesFeatures of Credit CardBipin ThakorNo ratings yet

- Issue of FCCBs and Ordinary Shares Scheme 1993Document11 pagesIssue of FCCBs and Ordinary Shares Scheme 1993shashasyNo ratings yet

- Cash and ReceivablesDocument6 pagesCash and ReceivablesNylan AnyerNo ratings yet

- Goldman Sachs' Response To Senate Document ReleaseDocument89 pagesGoldman Sachs' Response To Senate Document ReleaseDealBook100% (1)

- Cheque Introduction: A Cheque Is A Document of Very Great Importance in TheDocument13 pagesCheque Introduction: A Cheque Is A Document of Very Great Importance in The777priyanka100% (1)

- Investment: Types of InvestmentsDocument20 pagesInvestment: Types of InvestmentsAtul YadavNo ratings yet

- Conservatives Versus Wildcats: A Sociology of Financial ConflictFrom EverandConservatives Versus Wildcats: A Sociology of Financial ConflictNo ratings yet

- Treasury Operations In Turkey and Contemporary Sovereign Treasury ManagementFrom EverandTreasury Operations In Turkey and Contemporary Sovereign Treasury ManagementNo ratings yet

- Chapter 1-SolutionsDocument14 pagesChapter 1-SolutionsPrince CalicaNo ratings yet

- 18.1 Goals of Long-Term Financial Planning: Chapter 18 Financial Modeling and Pro Forma AnalysisDocument34 pages18.1 Goals of Long-Term Financial Planning: Chapter 18 Financial Modeling and Pro Forma AnalysisKhalid AlomarNo ratings yet

- True - False QuestionsDocument3 pagesTrue - False QuestionsNguyen Thanh Thao (K16 HCM)No ratings yet

- "Kotak Mahindra Bank Q2FY21 Earnings Conference Call": October 26, 2020Document24 pages"Kotak Mahindra Bank Q2FY21 Earnings Conference Call": October 26, 2020divya mNo ratings yet

- UNIT I Business CombinationDocument22 pagesUNIT I Business CombinationDaisy TañoteNo ratings yet

- Financial Statement ExampleDocument12 pagesFinancial Statement ExampleRhem Capisan100% (1)

- FA 4 Chapter 4 - Q2Document5 pagesFA 4 Chapter 4 - Q2Vasant SriudomNo ratings yet

- A Project Report On Financial Performance Based On Ratios at HDFC BankDocument75 pagesA Project Report On Financial Performance Based On Ratios at HDFC Banksudam merya100% (1)

- Law of Insolvency and BankruptcyDocument2 pagesLaw of Insolvency and BankruptcyArpit GoyalNo ratings yet

- SAP B1 9.0 FA ProcessesDocument40 pagesSAP B1 9.0 FA Processescreatorsiva100% (1)

- Chapter Ten: Management of Translation ExposureDocument17 pagesChapter Ten: Management of Translation ExposureHu Jia QuenNo ratings yet

- Altum Credo - New CAM Format For NBFC Clean VersionDocument19 pagesAltum Credo - New CAM Format For NBFC Clean VersionSwarna SinghNo ratings yet

- Kean Dry Cleaners Is Owned and Operated by Wally Lowman ADocument1 pageKean Dry Cleaners Is Owned and Operated by Wally Lowman AM Bilal SaleemNo ratings yet

- Module 12 Piecemeal AcquisitionsDocument15 pagesModule 12 Piecemeal AcquisitionsSodiq Okikiola HammedNo ratings yet

- Chapter 4 Quiz Questions & AnswersDocument15 pagesChapter 4 Quiz Questions & AnswersPatrick Forney100% (1)

- r7 Mba Financial Accounting and Analysis Set1Document3 pagesr7 Mba Financial Accounting and Analysis Set1Sunil RaparthiNo ratings yet

- Kode Nama Akun Debet Kredit Saldo NormalDocument31 pagesKode Nama Akun Debet Kredit Saldo NormalSamsul PangestuNo ratings yet

- HW On Cash BDocument6 pagesHW On Cash BAngelo123No ratings yet

- TOA QuizletDocument13 pagesTOA QuizletJehugem BayawaNo ratings yet

- IAS 1 - Presentation of Financial StatementsDocument17 pagesIAS 1 - Presentation of Financial StatementsMạnh hưng LêNo ratings yet

- Business Analysis Strategy - Barrio FiestaDocument19 pagesBusiness Analysis Strategy - Barrio FiestasicorangelicaNo ratings yet

- Fundamentals of Accounting Questions With AnswersDocument13 pagesFundamentals of Accounting Questions With Answersdhabekarsharvari07No ratings yet

- Preparation For Consolidations in SAP ECC To Meet Your EPM Integration NeedsDocument25 pagesPreparation For Consolidations in SAP ECC To Meet Your EPM Integration NeedsarunvisNo ratings yet

- Second Grading ExaminationDocument17 pagesSecond Grading ExaminationAmie Jane MirandaNo ratings yet

- Accounting For Special Transactions Final Grading ExaminationDocument9 pagesAccounting For Special Transactions Final Grading Examinationjessica amorosoNo ratings yet

- Problem SolvingDocument23 pagesProblem SolvingFery AnnNo ratings yet

- Sunil Cibil ReportDocument177 pagesSunil Cibil Reportblinkfinance7No ratings yet

- Distressed Debt An Avenue To Profit in Corporate Bankruptcy Article 1Document2 pagesDistressed Debt An Avenue To Profit in Corporate Bankruptcy Article 1corporateboy36596No ratings yet

- Pre-Feasibility Study: (Calf Fattening)Document18 pagesPre-Feasibility Study: (Calf Fattening)Oroj KhanNo ratings yet