Project Report On HSBC 2

Project Report On HSBC 2

Download as docx, pdf, or txt

You might also like

- Fco Used Rails - Amrani Trading - Bayonne Trading LLC PDFDocument2 pagesFco Used Rails - Amrani Trading - Bayonne Trading LLC PDFAmir KhanNo ratings yet

- Exam 2 Thanh toán quốc tế E 25 11Document2 pagesExam 2 Thanh toán quốc tế E 25 11MaiChi PhamNo ratings yet

- Syllabus For Banking and Insurance: Sem 1 1. Environment and Management of Financial ServicesDocument44 pagesSyllabus For Banking and Insurance: Sem 1 1. Environment and Management of Financial ServicesVinod TiwariNo ratings yet

- Methodology For Rating General Trading and Investment CompaniesDocument23 pagesMethodology For Rating General Trading and Investment CompaniesAhmad So MadNo ratings yet

- Cdcs PresentationDocument64 pagesCdcs PresentationAlok Pathak75% (4)

- Final Project of Reliance InfraDocument57 pagesFinal Project of Reliance InfraChaitali SarmalkarNo ratings yet

- Credit Management System of IFIC Bank LTDDocument73 pagesCredit Management System of IFIC Bank LTDHasib SimantoNo ratings yet

- Raymond WC MGMTDocument66 pagesRaymond WC MGMTshwetakhamarNo ratings yet

- Project Report For Pgdba FinanceDocument74 pagesProject Report For Pgdba FinanceAmit DwivediNo ratings yet

- Ba7022 Merchant Banking and Financial ServicesDocument214 pagesBa7022 Merchant Banking and Financial ServicesRitesh RamanNo ratings yet

- Maybank Annual Report 2010Document447 pagesMaybank Annual Report 2010rizza_jamahariNo ratings yet

- Volume 1, Issue 2, July 2014: ISSN: 2349-5677Document16 pagesVolume 1, Issue 2, July 2014: ISSN: 2349-5677IjbemrJournalNo ratings yet

- Finacial InstitutionDocument62 pagesFinacial InstitutionjdsamarocksNo ratings yet

- Accounts Receivable Management Practices and Growth of SMEDocument165 pagesAccounts Receivable Management Practices and Growth of SMELuke Robert HemmingsNo ratings yet

- Factoring Project ReportDocument15 pagesFactoring Project ReportSiddharth Desai100% (3)

- Summer Internship ProjectDocument25 pagesSummer Internship ProjectMegha PatelNo ratings yet

- Universal BankingDocument21 pagesUniversal Bankingnkhoja03No ratings yet

- Financial ServicesDocument24 pagesFinancial ServicesPrashant GamanagattiNo ratings yet

- Working CapitalDocument56 pagesWorking CapitalharmitkNo ratings yet

- MBA 3 Sem FInance SyllabusDocument8 pagesMBA 3 Sem FInance SyllabusGGUULLSSHHAANNNo ratings yet

- Management of Financial Services AssignmentDocument12 pagesManagement of Financial Services AssignmentDivya ShettyNo ratings yet

- Chapter - III Financial System and Non-Banking Financial Companies - The Structure and Status ProfileDocument55 pagesChapter - III Financial System and Non-Banking Financial Companies - The Structure and Status Profilechirag10pnNo ratings yet

- Jindal ReportDocument50 pagesJindal ReporthunnykukNo ratings yet

- A On Change in Corporate Identity and Its Impact On Stakeholders (A Case of Axis Bank)Document80 pagesA On Change in Corporate Identity and Its Impact On Stakeholders (A Case of Axis Bank)vaibhavbandhu100% (2)

- Summer Training in Intex TechnologyDocument37 pagesSummer Training in Intex TechnologyMj PayalNo ratings yet

- KCC BankDocument78 pagesKCC BankMukeshKumarNo ratings yet

- Project On Mutual FundDocument67 pagesProject On Mutual Fundpankaj100% (1)

- Word Final Project ReportDocument93 pagesWord Final Project Reportrubal0468No ratings yet

- Factoring MBADocument9 pagesFactoring MBADilip SinghNo ratings yet

- Navdeep Project FinanceDocument81 pagesNavdeep Project Financedushyants65No ratings yet

- Credit Risk Management HDFC Project Report Mba FinanceDocument102 pagesCredit Risk Management HDFC Project Report Mba FinanceNishant Kuradia0% (1)

- "Retail Banking": A Project ReportDocument72 pages"Retail Banking": A Project ReportneanaoNo ratings yet

- Role, Meaning, Importance of Financial Institutions An Banks in The Emerging New Environment of Privatization and GlobalizationDocument87 pagesRole, Meaning, Importance of Financial Institutions An Banks in The Emerging New Environment of Privatization and GlobalizationSumit SharmaNo ratings yet

- HDFC Bank CAMELS AnalysisDocument15 pagesHDFC Bank CAMELS Analysisprasanthgeni22No ratings yet

- Spoorthi BennurDocument58 pagesSpoorthi BennurSarva ShivaNo ratings yet

- Liquidity Crisis in BDDocument5 pagesLiquidity Crisis in BDJakir_bnk100% (1)

- Finance Tee 2nd TermDocument24 pagesFinance Tee 2nd TermNikhil PereiraNo ratings yet

- Project ReportDocument75 pagesProject ReportPankaj ThakurNo ratings yet

- A Study BTL Seasonality Across Media and Banking and FMCG Sector in INDIADocument54 pagesA Study BTL Seasonality Across Media and Banking and FMCG Sector in INDIATejas KadakiaNo ratings yet

- Kalupur 14719Document78 pagesKalupur 14719Parmar HitendrakumarNo ratings yet

- Summer Training Report Trends and Practices of HDFC Bank:-Retail Abnking Conducted at HDFC BANK, Ambala CityDocument104 pagesSummer Training Report Trends and Practices of HDFC Bank:-Retail Abnking Conducted at HDFC BANK, Ambala Cityjs60564No ratings yet

- Lgeil YashDocument3 pagesLgeil YashYash RoxsNo ratings yet

- BlackbookDocument56 pagesBlackbookrashmishaikh68No ratings yet

- Analysis of Customer Satisfaction at HyundaiDocument53 pagesAnalysis of Customer Satisfaction at HyundaiUmar ThukarNo ratings yet

- Calicut University Bcom SyllabusDocument57 pagesCalicut University Bcom Syllabuslibison1No ratings yet

- Retail Banking: by Prof Santosh KumarDocument30 pagesRetail Banking: by Prof Santosh KumarSuraj KumarNo ratings yet

- Further Scope of The Study Regarding Investment BankingDocument3 pagesFurther Scope of The Study Regarding Investment BankingMehedi HassanNo ratings yet

- Assignment On FactoringDocument5 pagesAssignment On FactoringVISHNU. M. K MBA 2018No ratings yet

- A Study On Credit Appraisal System On SME of Union Bank of IndiaDocument56 pagesA Study On Credit Appraisal System On SME of Union Bank of IndiaSarva ShivaNo ratings yet

- A Project On Banking SectorDocument81 pagesA Project On Banking SectorAkbar SinghNo ratings yet

- Report On Loan Disbursement and Recovery Status of Krishi BankDocument66 pagesReport On Loan Disbursement and Recovery Status of Krishi BankAnendya Chakma100% (1)

- A Project Report On: Customer Preference & Attributes Towards Saving-AccountDocument68 pagesA Project Report On: Customer Preference & Attributes Towards Saving-AccountchinunanaNo ratings yet

- Working Capital Assessment of Eicher Motors LTDDocument8 pagesWorking Capital Assessment of Eicher Motors LTDAkhilesh Shukla GMPE 2018 BatchNo ratings yet

- Planning of HBLDocument18 pagesPlanning of HBLAsad Ullah0% (1)

- Project On HDFC BANKDocument70 pagesProject On HDFC BANKAshutosh MishraNo ratings yet

- Summer Training MBA1Document47 pagesSummer Training MBA1Dipen PatelNo ratings yet

- Syndicate-Bank Company ProfileDocument13 pagesSyndicate-Bank Company ProfileSanthosh SomaNo ratings yet

- Internship ReportDocument65 pagesInternship ReportPakassignmentNo ratings yet

- Islamia UniDocument37 pagesIslamia UniKamran RasoolNo ratings yet

- Summer Training MBADocument47 pagesSummer Training MBAHiteshwari JadejaNo ratings yet

- Abn Ambro Bank Final 19-09-2007Document85 pagesAbn Ambro Bank Final 19-09-2007Gaurav NathaniNo ratings yet

- Customer Relationship ManagementDocument18 pagesCustomer Relationship ManagementMayuri NaikNo ratings yet

- 0365 Mock TestDocument17 pages0365 Mock TestMayuri NaikNo ratings yet

- Chapter 5 - The Communication ProcessDocument23 pagesChapter 5 - The Communication ProcessMayuri NaikNo ratings yet

- The King of Good Times: Guneet Kaur Saluja Taijasa Bhatkar Sohini GhoshDocument32 pagesThe King of Good Times: Guneet Kaur Saluja Taijasa Bhatkar Sohini GhoshMayuri NaikNo ratings yet

- JAIIB-LRAB-Short Notes by Murugan PDFDocument93 pagesJAIIB-LRAB-Short Notes by Murugan PDFDishant Chandrayan33% (3)

- BUYER DLC VERBIAGEDocument3 pagesBUYER DLC VERBIAGEswwicoNo ratings yet

- KHAIMAT LLC LTD UK MOU EN590 25k TTO .Document7 pagesKHAIMAT LLC LTD UK MOU EN590 25k TTO .wallaceaatwoodNo ratings yet

- Trade Service and Import Training ManualDocument114 pagesTrade Service and Import Training Manualmekonnin tadesseNo ratings yet

- Credit Analysis Report - FinalDocument84 pagesCredit Analysis Report - FinalVinod NagappanNo ratings yet

- Letter of Credit Bank Specific !Document17 pagesLetter of Credit Bank Specific !JOEMEETSMONUNo ratings yet

- Report On Loan Disbursement and Recovery Status of Krishi BankDocument66 pagesReport On Loan Disbursement and Recovery Status of Krishi BankAnendya Chakma100% (1)

- Market Analysis of Iron OreDocument46 pagesMarket Analysis of Iron OrePranshuKashyap100% (1)

- Credit and Collection ReviewerDocument7 pagesCredit and Collection ReviewerAlbiz, Vanessa R.No ratings yet

- Cir VS MagsaysayDocument4 pagesCir VS MagsaysayMaria RumusudNo ratings yet

- Indian Institute of Banking & Finance: Rules & Syllabus 2016Document14 pagesIndian Institute of Banking & Finance: Rules & Syllabus 2016Anubhav RawatNo ratings yet

- Ia Manual PDFDocument66 pagesIa Manual PDFAbhiNo ratings yet

- 22nd Vis Moot Arbitrator's BriefDocument15 pages22nd Vis Moot Arbitrator's BriefJoaquin DenisNo ratings yet

- PKS Draft Contract FOB MV (30 10 2012) NewDocument18 pagesPKS Draft Contract FOB MV (30 10 2012) NewrobertNo ratings yet

- 2017 Mercantile Law Bar Exam CoverageDocument12 pages2017 Mercantile Law Bar Exam CoverageRodney AtibulaNo ratings yet

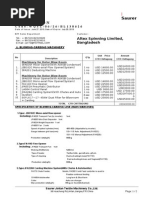

- Altex Spinning Mills LTD (16CARDS)Document2 pagesAltex Spinning Mills LTD (16CARDS)ardhendu1No ratings yet

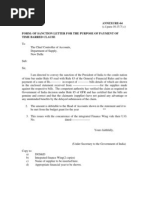

- Form: of Sanction Letter For The Purpose of Payment of Time Barred ClauseDocument25 pagesForm: of Sanction Letter For The Purpose of Payment of Time Barred ClauseSoma GhoshNo ratings yet

- Activities of Foreign Exchange InternshiDocument50 pagesActivities of Foreign Exchange InternshiJannatul FerdousNo ratings yet

- Export/Import Procedures: Md. Sarwar Hossain Deputy General Manager Bangladesh BankDocument12 pagesExport/Import Procedures: Md. Sarwar Hossain Deputy General Manager Bangladesh BankAlam (MDO)No ratings yet

- Issued Date - OfferDocument5 pagesIssued Date - Offerkong yun100% (3)

- Ga Draft ICPODocument2 pagesGa Draft ICPOFelix GaitaNo ratings yet

- Procurement of Projects: InfrastructureDocument34 pagesProcurement of Projects: InfrastructureIrie Mae GuzmanNo ratings yet

- UBL Final Project ReportDocument87 pagesUBL Final Project ReportPisces-isl IslNo ratings yet

- Application For Issuing An Irrevocable Documentary Credit: DateDocument4 pagesApplication For Issuing An Irrevocable Documentary Credit: DateZuka SoupNo ratings yet

- Application For Duty Free Import Authorisation (DFIADocument9 pagesApplication For Duty Free Import Authorisation (DFIAakashaggarwal88No ratings yet

- Draft DC Initials Signing BUYER CDF Rev 1Document14 pagesDraft DC Initials Signing BUYER CDF Rev 1R. KurniawanNo ratings yet