12-ACCA-FA2-Chp 12

12-ACCA-FA2-Chp 12

Download as pdf or txt

You might also like

- MA2 Mock 1-Qs - 2023-24Document11 pagesMA2 Mock 1-Qs - 2023-24daniel.maina2005No ratings yet

- Noida Golf Course Rules and Regulations BookDocument21 pagesNoida Golf Course Rules and Regulations BookAanchal Mishra100% (1)

- 02 MA2 LRP QuestionsDocument36 pages02 MA2 LRP QuestionsKopanang Leokana67% (3)

- Ma1 Management Information: Compiled By: Shahab ShafiDocument2 pagesMa1 Management Information: Compiled By: Shahab ShafishahabNo ratings yet

- MA2 SummaryDocument20 pagesMA2 SummarypringuserNo ratings yet

- F2 Mock Questions 201603Document12 pagesF2 Mock Questions 201603Renato WilsonNo ratings yet

- A Brief Overview On Data Mining Survey PDFDocument8 pagesA Brief Overview On Data Mining Survey PDFNed ThaiNo ratings yet

- The Impact of E-Service Quality and E-Loyalty On Online Shopping: Moderating Effect of E-Satisfaction and E-TrustDocument12 pagesThe Impact of E-Service Quality and E-Loyalty On Online Shopping: Moderating Effect of E-Satisfaction and E-TrustHARIYANTONo ratings yet

- 07-ACCA-FA2-Chp 07Document28 pages07-ACCA-FA2-Chp 07SMS PrintingNo ratings yet

- T2 Mock Exam (Dec'08 Exam)Document12 pagesT2 Mock Exam (Dec'08 Exam)vasanthipuruNo ratings yet

- FA2 S20-A21 Examiner's ReportDocument6 pagesFA2 S20-A21 Examiner's ReportAreeb AhmadNo ratings yet

- 13-ACCA-FA2-Chp 13Document22 pages13-ACCA-FA2-Chp 13SMS PrintingNo ratings yet

- AAA Study Support Guide: Plan Prepare PassDocument29 pagesAAA Study Support Guide: Plan Prepare Passltatoms100% (1)

- Maintaining Financial Records (FA2) December 2011Document11 pagesMaintaining Financial Records (FA2) December 2011xxxfarahxxx100% (1)

- F3 AW Interactive Study GuideDocument24 pagesF3 AW Interactive Study Guidebigab31327No ratings yet

- Ma1 t2 Study Text 2015 11 PDFDocument289 pagesMa1 t2 Study Text 2015 11 PDFFarrukh Khan100% (1)

- Ma1 Examreport d12Document4 pagesMa1 Examreport d12Josh BissoonNo ratings yet

- Absorption & Marginal (Q)Document8 pagesAbsorption & Marginal (Q)Sunain JahejoNo ratings yet

- FM Study Notes AugustDocument226 pagesFM Study Notes Augustsahil thakurNo ratings yet

- MA1-Study Guide (Student Copy) - Updated For July 2021Document333 pagesMA1-Study Guide (Student Copy) - Updated For July 2021Tịnh Nhạc100% (1)

- MA 1 Mock Exam QuestionDocument4 pagesMA 1 Mock Exam QuestionAbdul Gaffar100% (1)

- Ma1 - Formula SheetDocument6 pagesMa1 - Formula SheetRGN 11E 6 ANANYA GARGNo ratings yet

- 08-ACCA-FA2-Chp 08Document28 pages08-ACCA-FA2-Chp 08SMS PrintingNo ratings yet

- PM Study Notes MayDocument234 pagesPM Study Notes May77 Raj Bhanushali100% (1)

- CAT T2 - Mock 1Document10 pagesCAT T2 - Mock 1joo33jooNo ratings yet

- t4 2008 Dec QDocument8 pagest4 2008 Dec QShimera RamoutarNo ratings yet

- Ma1 Formula Sheet Lecture Notes All ChaptersDocument7 pagesMa1 Formula Sheet Lecture Notes All ChaptersJ&A Partners JANNo ratings yet

- Chapter - 02 - MADocument23 pagesChapter - 02 - MAMaithri Vidana KariyakaranageNo ratings yet

- Process CostingDocument1 pageProcess Costingyashwant ashokNo ratings yet

- Ma2chapter PDFDocument42 pagesMa2chapter PDFLinh LeNo ratings yet

- MA2Document32 pagesMA2eklavyaa_gaurav100% (1)

- Test t4 Labor CostingDocument2 pagesTest t4 Labor CostingSyed Muzaffar Ali ShahNo ratings yet

- lABOUR COST - Docx - 1662565663377Document4 pageslABOUR COST - Docx - 1662565663377Hammad KhanNo ratings yet

- FA2 Revision Questions 2Document9 pagesFA2 Revision Questions 2miss ainaNo ratings yet

- Acca f3 NotesDocument71 pagesAcca f3 Notesbisma aslamNo ratings yet

- Examiner's Report F2/FMA: For CBE and Paper Exams Covering January To June 2016Document5 pagesExaminer's Report F2/FMA: For CBE and Paper Exams Covering January To June 2016Minh NguyễnNo ratings yet

- ACCA FA1 Practice Question 1Document5 pagesACCA FA1 Practice Question 1arslan.ahmed8179No ratings yet

- Ma1 BPP ST 2017Document289 pagesMa1 BPP ST 2017Asad ZahidNo ratings yet

- IGCSE Economics NotesDocument83 pagesIGCSE Economics NoteshiramchurnNo ratings yet

- Ma1 Mock Exam 1 AnswersDocument18 pagesMa1 Mock Exam 1 Answers138.Mehreen “79” FaisalNo ratings yet

- A Level Economics Paper 3 QPDocument36 pagesA Level Economics Paper 3 QPYusuf SaleemNo ratings yet

- MA1 Exam Report June 2012Document3 pagesMA1 Exam Report June 2012S.L.L.CNo ratings yet

- Fa2 Mock 3 Questins-1Document19 pagesFa2 Mock 3 Questins-1sameerjameel678No ratings yet

- MA2 Mock 1-As - 2023-24Document8 pagesMA2 Mock 1-As - 2023-24daniel.maina2005No ratings yet

- Labour-PQDocument5 pagesLabour-PQRohaib MumtazNo ratings yet

- Ma1 Me1Document14 pagesMa1 Me1miss ainaNo ratings yet

- FIA - MA2 - Final Mock Exam - Qs - 2023Document18 pagesFIA - MA2 - Final Mock Exam - Qs - 2023cnarin100% (2)

- F2 and FMA Full Specimen Exam Answers PDFDocument4 pagesF2 and FMA Full Specimen Exam Answers PDFSNEHA MARIYAM VARGHESE SIM 16-18No ratings yet

- O Level EconomicsDocument35 pagesO Level EconomicsHafiz DanialNo ratings yet

- Vocabulary Sheet Weekdays 2 With ActivitiesDocument2 pagesVocabulary Sheet Weekdays 2 With ActivitiesGislaine RodriguesNo ratings yet

- MA1 First Test UpdatedDocument14 pagesMA1 First Test UpdatedHammad Khan100% (1)

- MA2 Managing Cost - Finance Notes Complete FileDocument129 pagesMA2 Managing Cost - Finance Notes Complete FileUzairNo ratings yet

- Fa2 SyllabusDocument19 pagesFa2 Syllabusazizrehman15951No ratings yet

- Oveheads Practice QuestionsDocument674 pagesOveheads Practice Questionsyashwant ashokNo ratings yet

- Principles and CharacteristicsDocument12 pagesPrinciples and CharacteristicsFloyd DaltonNo ratings yet

- Fia - Exercises (C1-C4)Document46 pagesFia - Exercises (C1-C4)NHI NGUYEN PHUONG THAONo ratings yet

- 2023-24 - MA2 - AQB-OT-Set 1-AnswersDocument8 pages2023-24 - MA2 - AQB-OT-Set 1-Answersdaniel.maina2005No ratings yet

- A3 Incomplete Records and Single EntryDocument11 pagesA3 Incomplete Records and Single EntrydiggywilldoitNo ratings yet

- Chapter 5 Incomplete RecordDocument20 pagesChapter 5 Incomplete RecordNUR ADLIN ZAFIRAH BINTI NORAZLI KTNNo ratings yet

- CH 2 - Incomplete Records & Non Profit OrganisationDocument56 pagesCH 2 - Incomplete Records & Non Profit OrganisationFaris IzzatNo ratings yet

- ACCCOB1 - Quiz #1 - Tuesday - Set A - Answer KeyDocument4 pagesACCCOB1 - Quiz #1 - Tuesday - Set A - Answer KeyrabekogoNo ratings yet

- Incomplete Records - N4 22 PDFDocument57 pagesIncomplete Records - N4 22 PDFSay SopheakneathNo ratings yet

- Certificate Phil JarvisDocument1 pageCertificate Phil JarvisSMS PrintingNo ratings yet

- Hypermobilityvs InstabilityDocument18 pagesHypermobilityvs InstabilitySMS PrintingNo ratings yet

- CV For NaryDocument1 pageCV For NarySMS PrintingNo ratings yet

- 08-ACCA-FA2-Chp 08Document28 pages08-ACCA-FA2-Chp 08SMS PrintingNo ratings yet

- Mohammad Murtadha Ibrahim: ObjectivesDocument5 pagesMohammad Murtadha Ibrahim: ObjectivesNaveed AhmedNo ratings yet

- FB Pixels UpdateDocument36 pagesFB Pixels UpdateMichael JenkinsNo ratings yet

- ProspectusDocument191 pagesProspectusscrivenersimpactNo ratings yet

- Applied Areas Lec 5Document10 pagesApplied Areas Lec 5Abdul basitNo ratings yet

- Distributor Agreement: PreambleDocument3 pagesDistributor Agreement: PreambleEmmie TaboraNo ratings yet

- Rera AffidavitDocument3 pagesRera AffidavitAdv Simran Ved100% (1)

- Revised Guidelines Governing Registration of CooperativesDocument14 pagesRevised Guidelines Governing Registration of CooperativesNarciso Reyes Jr.No ratings yet

- Bag InvoiceDocument1 pageBag InvoiceNawaz RahmanNo ratings yet

- Tax2 - Estate Donors VAT ReviewerDocument3 pagesTax2 - Estate Donors VAT ReviewercardeguzmanNo ratings yet

- Microsoft Word - GPF Part FinalDocument3 pagesMicrosoft Word - GPF Part Finalacge nrptNo ratings yet

- SAP Road Map: S/4HANA Supply Chain For Transportation ManagementDocument15 pagesSAP Road Map: S/4HANA Supply Chain For Transportation ManagementJagadish JaganNo ratings yet

- Business Ethics and Corporate Governance PDFDocument7 pagesBusiness Ethics and Corporate Governance PDFSHIVANSHUNo ratings yet

- Group 6Document5 pagesGroup 6Siddhant AggarwalNo ratings yet

- BCR Rec21 Building Product SafetyDocument51 pagesBCR Rec21 Building Product SafetylucyNo ratings yet

- Session 16-18 CRM Roadmap Class PDFDocument17 pagesSession 16-18 CRM Roadmap Class PDFmanmeet kaurNo ratings yet

- A Camera That Protects Your BabyDocument13 pagesA Camera That Protects Your Babyramanpreet kaurNo ratings yet

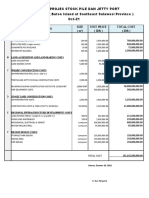

- RAB Jetty Dan Stock PileDocument1 pageRAB Jetty Dan Stock PilebimobimoprabowoNo ratings yet

- Case - Strategy GagaDocument5 pagesCase - Strategy GagaGautamNo ratings yet

- Midterm Exams Attempt ReviewDocument20 pagesMidterm Exams Attempt ReviewPrincess AleaNo ratings yet

- Telecommunications Dissertation TopicsDocument6 pagesTelecommunications Dissertation TopicsHowToWriteMyPaperNorthLasVegas100% (1)

- CMake ListsDocument2 pagesCMake Listsabcd abcdeNo ratings yet

- Executed Docs (00907407xBADA8)Document15 pagesExecuted Docs (00907407xBADA8)kuhnr8677No ratings yet

- Krishna TejaDocument6 pagesKrishna Tejasubhakaran saileshanNo ratings yet

- RHB Global Shariah Dynamic Income Fund - RM-H - FFSDocument2 pagesRHB Global Shariah Dynamic Income Fund - RM-H - FFSNadia Nusyuqin HarzuddinNo ratings yet

- MC MahonDocument3 pagesMC MahongardneradaraNo ratings yet

- Scout APM Announces Python Application Support For Error Monitoring ToolDocument3 pagesScout APM Announces Python Application Support For Error Monitoring ToolPR.comNo ratings yet

- Overruns or Underestimates?: Thucydides (C. 460 BC - C. 395 BC)Document46 pagesOverruns or Underestimates?: Thucydides (C. 460 BC - C. 395 BC)EstebanNo ratings yet