Litigation Finance Mechanics

Litigation Finance Mechanics

Download as pdf or txt

You might also like

- Phillip Saunders On Control PremiumDocument7 pagesPhillip Saunders On Control Premiumbharath289No ratings yet

- Guide To Brazilian Local MarketsDocument40 pagesGuide To Brazilian Local MarketsRedhairrecords SlabsNo ratings yet

- NUS BBA Various SpecialisationDocument12 pagesNUS BBA Various SpecialisationjameslukitoNo ratings yet

- CREFC CMBS 2 - 0 Best Practices Principles-Based Loan Underwriting GuidelinesDocument33 pagesCREFC CMBS 2 - 0 Best Practices Principles-Based Loan Underwriting Guidelinesmerlin7474No ratings yet

- Jazz Pharmaceuticals Investment Banking Pitch BookDocument20 pagesJazz Pharmaceuticals Investment Banking Pitch BookAlexandreLegaNo ratings yet

- b10 eDocument22 pagesb10 ejrgannonNo ratings yet

- Defeasance and Your Deal PDFDocument8 pagesDefeasance and Your Deal PDFcleveland123100% (2)

- MBS Abs ModellingDocument9 pagesMBS Abs Modellinglmelo2No ratings yet

- Apollo Global Management LLC Feb Investor Presentation Update VFinalDocument40 pagesApollo Global Management LLC Feb Investor Presentation Update VFinalPepe Jara GinsbergNo ratings yet

- IFRS 13 FV and IVS - Slide PackDocument26 pagesIFRS 13 FV and IVS - Slide PackjalalNo ratings yet

- 4 - 6-Credit Risk Management PDFDocument39 pages4 - 6-Credit Risk Management PDFPallavi PuriNo ratings yet

- Advanced MergersDocument18 pagesAdvanced Mergersveda20No ratings yet

- Corporate Governance and Value Creation - Private Equity StyleDocument9 pagesCorporate Governance and Value Creation - Private Equity StylemokitiNo ratings yet

- Private Placement Offering Checklist1Document3 pagesPrivate Placement Offering Checklist1J.P. FernandesNo ratings yet

- AircraftABS 7sept05Document0 pagesAircraftABS 7sept05jamesbrentsmithNo ratings yet

- Pru HQ CMBS Value of Structure 7 10Document12 pagesPru HQ CMBS Value of Structure 7 10guliguruNo ratings yet

- IDSS MplusDocument4 pagesIDSS MplusKen ChewNo ratings yet

- WbsDocument32 pagesWbsdeven_cNo ratings yet

- Portfolio and Risk Analytics Brochure4Document11 pagesPortfolio and Risk Analytics Brochure4Jorge ContrerasNo ratings yet

- Purchase Price Allocation Study 2019 2020Document63 pagesPurchase Price Allocation Study 2019 2020cheungNo ratings yet

- Ê, in Finance, Is AnDocument11 pagesÊ, in Finance, Is AnJome MathewNo ratings yet

- Pon Deal Making PDFDocument32 pagesPon Deal Making PDFTatiana HerreraNo ratings yet

- Private Equity Unchained: Strategy Insights for the Institutional InvestorFrom EverandPrivate Equity Unchained: Strategy Insights for the Institutional InvestorNo ratings yet

- Westpac - Two Sides of The US Student Debt Coin (July 2013)Document6 pagesWestpac - Two Sides of The US Student Debt Coin (July 2013)leithvanonselenNo ratings yet

- Mortgage Backed Securities PrimerDocument9 pagesMortgage Backed Securities Primerjohnsang50% (2)

- Mezzanine Debt StructuresDocument2 pagesMezzanine Debt StructuresJavierMuñozCanessaNo ratings yet

- Financial Due Diligence BookletDocument28 pagesFinancial Due Diligence BookletEl Hadji A Aziz NDIAYENo ratings yet

- Critical Financial Review: Understanding Corporate Financial InformationFrom EverandCritical Financial Review: Understanding Corporate Financial InformationNo ratings yet

- Securities Lending Times Issue 223Document44 pagesSecurities Lending Times Issue 223Securities Lending TimesNo ratings yet

- Investment PhilosophyDocument7 pagesInvestment PhilosophyElad BreitnerNo ratings yet

- Taylor & Francis, Ltd. Financial Analysts JournalDocument16 pagesTaylor & Francis, Ltd. Financial Analysts JournalJean Pierre BetancourthNo ratings yet

- PIMCO ETFs ISS - Smart PassiveDocument4 pagesPIMCO ETFs ISS - Smart Passivefreebanker777741No ratings yet

- Capital Structure Theory Current PerspectiveDocument13 pagesCapital Structure Theory Current PerspectiveAli GardeziNo ratings yet

- Overview of Athene PDFDocument22 pagesOverview of Athene PDFArchana SankarNo ratings yet

- Carried Interest Waterfall With Catch UpDocument4 pagesCarried Interest Waterfall With Catch UpricgordonNo ratings yet

- The Locked Box MechanismDocument3 pagesThe Locked Box MechanismAnish NairNo ratings yet

- Mastering Illiquidity: Risk management for portfolios of limited partnership fundsFrom EverandMastering Illiquidity: Risk management for portfolios of limited partnership fundsNo ratings yet

- Mauboussin - Interdisciplinary Perspectives On Risk PDFDocument6 pagesMauboussin - Interdisciplinary Perspectives On Risk PDFRob72081No ratings yet

- Earn Out ValuationDocument6 pagesEarn Out Valuationpmk1978No ratings yet

- Sharpening The Arithmetic of Active Management - AQR 2016Document14 pagesSharpening The Arithmetic of Active Management - AQR 2016Guido 125 LavespaNo ratings yet

- Tax Issues in Purchase and Sale AgreementsDocument20 pagesTax Issues in Purchase and Sale AgreementsTaichi ChenNo ratings yet

- Credit Apprisal Method-FDocument16 pagesCredit Apprisal Method-FRishabh JainNo ratings yet

- AQR Corporate Arbitrage Overview and Benefits of A Dynamic Multistrategy ApproachDocument12 pagesAQR Corporate Arbitrage Overview and Benefits of A Dynamic Multistrategy ApproachJereynierNo ratings yet

- 2014 12 Mercer Risk Premia Investing From The Traditional To Alternatives PDFDocument20 pages2014 12 Mercer Risk Premia Investing From The Traditional To Alternatives PDFArnaud AmatoNo ratings yet

- Why Strategy Matters - Exploring The Link Between Strategy, Competitive Advantage and The Stock MarketDocument8 pagesWhy Strategy Matters - Exploring The Link Between Strategy, Competitive Advantage and The Stock Marketpjs15No ratings yet

- Modigliani & Miller ApproachDocument11 pagesModigliani & Miller ApproachsaidarsikaNo ratings yet

- Catastrophic Risk and The Capital Markets: Berkshire Hathaway and Warren Buffett's Success Volatility Pumping Cat ReinsuranceDocument15 pagesCatastrophic Risk and The Capital Markets: Berkshire Hathaway and Warren Buffett's Success Volatility Pumping Cat ReinsuranceAlex VartanNo ratings yet

- Structured Finance - A guide to the principles of asset securitizationDocument17 pagesStructured Finance - A guide to the principles of asset securitizationhesham zakiNo ratings yet

- Expected Returns On Stocks and BondsDocument21 pagesExpected Returns On Stocks and BondshussankaNo ratings yet

- Introduction To BancDocument16 pagesIntroduction To BancAkash BishtNo ratings yet

- Thesis: The Influence of Hedge Funds On Share PricesDocument63 pagesThesis: The Influence of Hedge Funds On Share Pricesbenkedav100% (7)

- (Booz Allen Hamilton) The M&a Collar Handbook - How To Manage Equity RiskDocument15 pages(Booz Allen Hamilton) The M&a Collar Handbook - How To Manage Equity RiskanuragNo ratings yet

- Modigliani Miller Prop 1 and 2 PDFDocument8 pagesModigliani Miller Prop 1 and 2 PDFChittisa CharoenpanichNo ratings yet

- Capital Structure, The Determinants and FeaturesDocument5 pagesCapital Structure, The Determinants and FeaturesRianto StgNo ratings yet

- Executive Profile - Sam ZellDocument4 pagesExecutive Profile - Sam ZellAmit RanaNo ratings yet

- Case #1: You're Cramming at The Last-Minute For Interviews or Case Study / Modeling TestsDocument8 pagesCase #1: You're Cramming at The Last-Minute For Interviews or Case Study / Modeling TestsAndreea PavelNo ratings yet

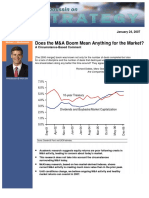

- Mauboussin - Does The M&a Boom Mean Anything For The MarketDocument6 pagesMauboussin - Does The M&a Boom Mean Anything For The MarketRob72081No ratings yet

- Merger Acquisition Chapter 10Document26 pagesMerger Acquisition Chapter 10rayhanrabbiNo ratings yet

- LBO TutorialDocument8 pagesLBO Tutorialissam chleuhNo ratings yet

- Bracegirdle Rife MicroscopesDocument15 pagesBracegirdle Rife MicroscopesToby SmallNo ratings yet

- Inbound 6794401006500051339Document15 pagesInbound 6794401006500051339Toby SmallNo ratings yet

- Inbound 5801658029110259543Document5 pagesInbound 5801658029110259543Toby SmallNo ratings yet

- Freeenergy 2003Document19 pagesFreeenergy 2003Toby SmallNo ratings yet

- Deeper Insights Into The Illuminati Formula by Fritz Springmeier & Cisco WheelerDocument2 pagesDeeper Insights Into The Illuminati Formula by Fritz Springmeier & Cisco WheelerToby SmallNo ratings yet

- T Trik Texts: /RT!FL I, // /LU"Document113 pagesT Trik Texts: /RT!FL I, // /LU"Toby SmallNo ratings yet

- A Manual For A New ExistenceDocument34 pagesA Manual For A New ExistenceToby SmallNo ratings yet

- Bloomberg Law Steps in The Litigation Finance ProcessDocument4 pagesBloomberg Law Steps in The Litigation Finance ProcessToby SmallNo ratings yet

- YOGA AND DIGESTION and ELIMINATION1Document25 pagesYOGA AND DIGESTION and ELIMINATION1Toby SmallNo ratings yet

- Deeper Insights Into The Illuminati Formula-2Document8 pagesDeeper Insights Into The Illuminati Formula-2Toby SmallNo ratings yet

- CH 1 Mini ExercisesDocument15 pagesCH 1 Mini Exercisesshehabsherif320No ratings yet

- Inventory Management AssignmentDocument6 pagesInventory Management Assignmentt4jmvwdxb8No ratings yet

- Sample 3 SF - AssignmentDocument18 pagesSample 3 SF - AssignmentArchana SarmaNo ratings yet

- Acca Paper f1 McqsDocument4 pagesAcca Paper f1 McqsAbuzar umar AnsariNo ratings yet

- Fundamental Analysis (Lecture 15)Document43 pagesFundamental Analysis (Lecture 15)Israel AkinyemiNo ratings yet

- UntitledDocument2 pagesUntitledUmi AnggraeniNo ratings yet

- CRM Unit 1Document26 pagesCRM Unit 1sharmaprashant08920No ratings yet

- Slides 07Document44 pagesSlides 07Vinay Gowda D MNo ratings yet

- ATS Resume Template-1 - Business DevelopmentDocument2 pagesATS Resume Template-1 - Business DevelopmenthrNo ratings yet

- 1 Scope of International MarketingDocument35 pages1 Scope of International MarketingLORENA HERRERA CASTRO100% (1)

- SURVEY-QUESTIONNAIRE Roca CostcoDocument5 pagesSURVEY-QUESTIONNAIRE Roca CostcoNhânNo ratings yet

- SSRN Id2621488Document26 pagesSSRN Id2621488KARTIKEYA KOTHARINo ratings yet

- Research Paper - ROLE OF BANKING AND NBFC IN THE DEVELOPMENT OF THE MSME SECTOR IN ANDHRA PRADESHDocument10 pagesResearch Paper - ROLE OF BANKING AND NBFC IN THE DEVELOPMENT OF THE MSME SECTOR IN ANDHRA PRADESHsaiNo ratings yet

- Since 1986Document2 pagesSince 1986Piyush ChoudharyNo ratings yet

- Risk Analysis (Divya Jadi Booti)Document48 pagesRisk Analysis (Divya Jadi Booti)Michael AdhikariNo ratings yet

- Opti VerDocument1 pageOpti VerRonnie KurtzbardNo ratings yet

- MM Short MaterialDocument24 pagesMM Short MaterialThippana GomathiNo ratings yet

- Market Entry Study NotesDocument2 pagesMarket Entry Study NotesmimiNo ratings yet

- trent pdfDocument41 pagestrent pdf68ngbxtqs9No ratings yet

- Nano Basket Infra SectorDocument4 pagesNano Basket Infra Sectorvaishali007No ratings yet

- Bitcoin Price History 2009 — 2024Document20 pagesBitcoin Price History 2009 — 20241400142562No ratings yet

- AFN ProbDocument3 pagesAFN ProbAli The Banner MakerNo ratings yet

- 02 Partnership OperationDocument4 pages02 Partnership OperationRoland jamesNo ratings yet

- Admission of PartnerDocument7 pagesAdmission of Partneradarshrathore12341234No ratings yet

- 100 Crucial LBO Model Jargons You Need To KnowDocument16 pages100 Crucial LBO Model Jargons You Need To Knownaghulk1No ratings yet

- PLC & BCG Matrix of AsianpaintsDocument11 pagesPLC & BCG Matrix of AsianpaintsNeeraj PrajapatNo ratings yet

- #Entrep - Lesson 3 - Relevance of Entrepreneurship and Entrepreneurs in Economic Development and SocietyDocument16 pages#Entrep - Lesson 3 - Relevance of Entrepreneurship and Entrepreneurs in Economic Development and SocietyMarxene Hazel Joy MoranteNo ratings yet

- Installment Sales Sample ProblemsDocument1 pageInstallment Sales Sample Problemslemvin121003No ratings yet

- Dividend Models - Set 2Document5 pagesDividend Models - Set 2Tushant bandhuNo ratings yet