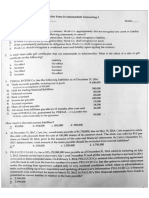

Acc 205-Intermediate Accounting I Part Ii Ppe Part 2: Long Quiz

Acc 205-Intermediate Accounting I Part Ii Ppe Part 2: Long Quiz

Download as pdf or txt

You might also like

- INTERMEDIATE ACCOUNTING 1 ReviewDocument57 pagesINTERMEDIATE ACCOUNTING 1 ReviewStefanie Fermin100% (1)

- What Is A Key Performance Indicator (KPI) - Explanation and Examples PDFDocument20 pagesWhat Is A Key Performance Indicator (KPI) - Explanation and Examples PDFJose ComorelNo ratings yet

- Batch Numbering System QA - 004Document5 pagesBatch Numbering System QA - 004Sagar Chavan100% (5)

- Gen 010 Q1 Sy2223Document5 pagesGen 010 Q1 Sy2223CLAIRE PAJONo ratings yet

- Intermediate Accounting 1 Final Grading ExaminationDocument18 pagesIntermediate Accounting 1 Final Grading ExaminationKrissa Mae LongosNo ratings yet

- Chapter 14 - Investments in AssociatesDocument7 pagesChapter 14 - Investments in AssociatesXiena100% (1)

- Government Grants: Use The Following Information For The Next Three QuestionsDocument2 pagesGovernment Grants: Use The Following Information For The Next Three QuestionsJEFFERSON CUTENo ratings yet

- Intermediate Accounting 1 Solution Manual: Chapter 15 - Property, Plant and Equipment To Chapter 17 - Depletion of Mineral ResourcesDocument20 pagesIntermediate Accounting 1 Solution Manual: Chapter 15 - Property, Plant and Equipment To Chapter 17 - Depletion of Mineral ResourcesMckenzieNo ratings yet

- Chapter 16 - Ppe Part 2Document10 pagesChapter 16 - Ppe Part 2Xiena50% (2)

- The Accomplishment of Joseph EstradaDocument3 pagesThe Accomplishment of Joseph Estradavalkyrior64% (14)

- GT Basic Practise SetDocument5 pagesGT Basic Practise SethemanthillipilliNo ratings yet

- This Study Resource Was: PPE Part 2Document8 pagesThis Study Resource Was: PPE Part 2Ms VampireNo ratings yet

- Quiz - Chapter 4 - Provisions, Cont. Liab. & Cont. Assets - 2021Document3 pagesQuiz - Chapter 4 - Provisions, Cont. Liab. & Cont. Assets - 2021Martin ManuelNo ratings yet

- 2nd Grading Exams Key AnswersDocument19 pages2nd Grading Exams Key AnswersUnknown WandererNo ratings yet

- Chapter 10 Impairment of Assets (Pas 36)Document11 pagesChapter 10 Impairment of Assets (Pas 36)Princess TaoinganNo ratings yet

- Property, Plant and Equipment (Part 2) : Problem 1: True or FalseDocument13 pagesProperty, Plant and Equipment (Part 2) : Problem 1: True or FalseJannelle SalacNo ratings yet

- Quiz - Chapter 11 - Investments - Additional Concepts - Ia 1 - 2020 EditionDocument2 pagesQuiz - Chapter 11 - Investments - Additional Concepts - Ia 1 - 2020 EditionJennifer RelosoNo ratings yet

- Quiz - Chapter 1 - Current Liabilities - 2021Document3 pagesQuiz - Chapter 1 - Current Liabilities - 2021Jennifer RelosoNo ratings yet

- PPE ReviewerDocument13 pagesPPE ReviewerMariel DichosoNo ratings yet

- Pas 40-41 & Pfrs 1 QuizDocument3 pagesPas 40-41 & Pfrs 1 QuizWendy Cagape0% (1)

- Receivables - Additional Concepts: Long QuizDocument9 pagesReceivables - Additional Concepts: Long Quizfinn mertens100% (1)

- Intermediate Accounting 2 Test BanksDocument14 pagesIntermediate Accounting 2 Test BankshwskbshgqxNo ratings yet

- Sol. Man. - Chapter 17 - Depletion of Mineral Resources - Ia Part 1BDocument3 pagesSol. Man. - Chapter 17 - Depletion of Mineral Resources - Ia Part 1BMahasia MANDIGANNo ratings yet

- CHAPTER 15 PPE (PART 1) - Reviewer - For Distribution PDFDocument20 pagesCHAPTER 15 PPE (PART 1) - Reviewer - For Distribution PDFemman neriNo ratings yet

- Quiz - Chapter 7 - Inventories - Ia 1Document5 pagesQuiz - Chapter 7 - Inventories - Ia 1Mechaella Shella Ningal Apolinario100% (1)

- SOL MAN CHAPTER 15 PPE PART 1 IA PART 1B 2020ed1 DocxDocument21 pagesSOL MAN CHAPTER 15 PPE PART 1 IA PART 1B 2020ed1 DocxVkyla BataoelNo ratings yet

- Test Bank 2 - Ia 1Document20 pagesTest Bank 2 - Ia 1Xiena100% (1)

- Long Quiz 2 Lease Answer KeyDocument3 pagesLong Quiz 2 Lease Answer KeyMia FayeNo ratings yet

- Chapter 3 Bonds Payable Other ConceptsDocument7 pagesChapter 3 Bonds Payable Other ConceptschristianNo ratings yet

- Quiz Chapter-2 Notes-PayableDocument5 pagesQuiz Chapter-2 Notes-Payableangelinavalencia0307No ratings yet

- Answers - Chapter 1 - Current LiabilitiesDocument5 pagesAnswers - Chapter 1 - Current LiabilitiesLhica EsterasNo ratings yet

- Quiz Chapter 10 Investments in Debt Securities Ia 1 2020 EditionDocument7 pagesQuiz Chapter 10 Investments in Debt Securities Ia 1 2020 EditionChristine Jean MajestradoNo ratings yet

- Activity - PAS 41Document4 pagesActivity - PAS 41PapeleriaphNo ratings yet

- Leases (Part 2) : Problem 1: True or FalseDocument23 pagesLeases (Part 2) : Problem 1: True or FalseKim Hanbin100% (1)

- Adamson University Intermediate Accounting 1 Property, Plant, & Equipment Quiz - Answer KeyDocument4 pagesAdamson University Intermediate Accounting 1 Property, Plant, & Equipment Quiz - Answer KeyKhai Supleo PabelicoNo ratings yet

- Ia MCQ ComputationalDocument56 pagesIa MCQ ComputationalRomcel FlorendoNo ratings yet

- Chapter 16 Ppe (Part 2)Document27 pagesChapter 16 Ppe (Part 2)honeyjoy salapantanNo ratings yet

- This Study Resource Was: InvestmentsDocument5 pagesThis Study Resource Was: InvestmentsMs Vampire100% (1)

- Ia 1 Millan Test BankDocument193 pagesIa 1 Millan Test BankJon Paul DonatoNo ratings yet

- PPE Initial Meas Assignment With Answers FormattedDocument5 pagesPPE Initial Meas Assignment With Answers FormattedCJ IbaleNo ratings yet

- Intangibles QuizDocument4 pagesIntangibles QuizXytusNo ratings yet

- PAS 2 - Inventories - QuizDocument4 pagesPAS 2 - Inventories - QuizQueenie Mae San JuanNo ratings yet

- Reviewer For Mid Term ExamDocument12 pagesReviewer For Mid Term ExamJannelle SalacNo ratings yet

- Chapter 15Document10 pagesChapter 15Jess SiazonNo ratings yet

- Sol. Man. Chapter 5 Employee Benefits Part 1 2021Document9 pagesSol. Man. Chapter 5 Employee Benefits Part 1 2021Kim HanbinNo ratings yet

- Notes Receivable: Problem 1: True or FalseDocument21 pagesNotes Receivable: Problem 1: True or FalseAbegail Joy De GuzmanNo ratings yet

- Sol. Man. Chapter 9 Investments Ia Part 1a 2020 EditionDocument12 pagesSol. Man. Chapter 9 Investments Ia Part 1a 2020 EditionMizza Moreno CantilaNo ratings yet

- Sol. Man. - Chapter 14 - Investments in Assoc. - Ia Part 1BDocument15 pagesSol. Man. - Chapter 14 - Investments in Assoc. - Ia Part 1BChristian James RiveraNo ratings yet

- The Accounting Process: Name: Date: Professor: Section: Score: QuizDocument6 pagesThe Accounting Process: Name: Date: Professor: Section: Score: QuizAllyna Jane Enriquez100% (1)

- Acc107 Quiz 2-P1Document9 pagesAcc107 Quiz 2-P1itsayuhthingNo ratings yet

- Northern CPA Review Co. (NCPAR) : Practical Accounting Problems 1Document15 pagesNorthern CPA Review Co. (NCPAR) : Practical Accounting Problems 1Sherri BonquinNo ratings yet

- Quiz Pas 28 Investments in Assoc. JVDocument2 pagesQuiz Pas 28 Investments in Assoc. JVLlyana paula SuyuNo ratings yet

- Quiz Pas 26 Acctg Reptg by Retirement Benefit PlansDocument1 pageQuiz Pas 26 Acctg Reptg by Retirement Benefit PlansLlyana paula SuyuNo ratings yet

- Unit 4 Accounting For Investments: Topic 5 - Investment in PropertyDocument7 pagesUnit 4 Accounting For Investments: Topic 5 - Investment in PropertyRey HandumonNo ratings yet

- 11Document11 pages11Maria G. BernardinoNo ratings yet

- PAS 36 Impairment of AssetsDocument3 pagesPAS 36 Impairment of AssetsRia Gayle100% (1)

- Answer Q1 Job Order CostingDocument5 pagesAnswer Q1 Job Order CostingDiane Cris Duque100% (1)

- Notes Receivable: Long QuizDocument8 pagesNotes Receivable: Long Quizfinn mertensNo ratings yet

- Government Grants: Use The Following Information For The Next Three QuestionsDocument2 pagesGovernment Grants: Use The Following Information For The Next Three QuestionsXienaNo ratings yet

- PAS 41 AgricultureDocument4 pagesPAS 41 AgricultureCarlo B Cagampang100% (1)

- QUIZ - CHAPTER 16 - PPE PART 2 - 2020edDocument5 pagesQUIZ - CHAPTER 16 - PPE PART 2 - 2020edjanna napiliNo ratings yet

- (Drills - Ppe) Acc.107Document10 pages(Drills - Ppe) Acc.107Boys ShipperNo ratings yet

- Ppe Part 2 ProblemsDocument6 pagesPpe Part 2 Problemsemielyn lafortezaNo ratings yet

- ACT234 - Quiz 8 ANSWERDocument3 pagesACT234 - Quiz 8 ANSWERglenelou09No ratings yet

- Ppe Part 2 ProblemsDocument6 pagesPpe Part 2 Problemsemielyn lafortezaNo ratings yet

- Liab Part 1Document28 pagesLiab Part 1emielyn lafortezaNo ratings yet

- UntitledDocument30 pagesUntitledemielyn lafortezaNo ratings yet

- Prelim Handouts What Is Taxation?Document18 pagesPrelim Handouts What Is Taxation?emielyn lafortezaNo ratings yet

- UntitledDocument3 pagesUntitledemielyn lafortezaNo ratings yet

- Cpa Review School of The Philippines Manila Management Advisory Services Financial Statement AnalysisDocument13 pagesCpa Review School of The Philippines Manila Management Advisory Services Financial Statement Analysisemielyn lafortezaNo ratings yet

- Chapter 2: Taxes, Tax Laws, and Tax AdministrationDocument9 pagesChapter 2: Taxes, Tax Laws, and Tax Administrationemielyn lafortezaNo ratings yet

- The Monkey and The Turtle: Activity 1.1Document2 pagesThe Monkey and The Turtle: Activity 1.1emielyn lafortezaNo ratings yet

- Why Is Income Subject To Tax?Document6 pagesWhy Is Income Subject To Tax?emielyn lafortezaNo ratings yet

- UntitledDocument41 pagesUntitledemielyn lafortezaNo ratings yet

- UntitledDocument1 pageUntitledemielyn lafortezaNo ratings yet

- The Contemporary: WorldDocument82 pagesThe Contemporary: Worldemielyn lafortezaNo ratings yet

- UntitledDocument15 pagesUntitledemielyn lafortezaNo ratings yet

- Analysis of Movement and Rhythmic Skills in Physical Education StudentsDocument3 pagesAnalysis of Movement and Rhythmic Skills in Physical Education Studentsemielyn lafortezaNo ratings yet

- UntitledDocument127 pagesUntitledemielyn lafortezaNo ratings yet

- B. Cannot Be Stated As A PercentageDocument14 pagesB. Cannot Be Stated As A Percentageemielyn lafortezaNo ratings yet

- Tax Collection Systems: Withholding Taxes Collected Under This SystemDocument9 pagesTax Collection Systems: Withholding Taxes Collected Under This Systememielyn lafortezaNo ratings yet

- Hyd Ref 7Document2 pagesHyd Ref 7emielyn lafortezaNo ratings yet

- Self-Assessment Questions (Saq) / Activity 2Document5 pagesSelf-Assessment Questions (Saq) / Activity 2emielyn lafortezaNo ratings yet

- UntitledDocument4 pagesUntitledemielyn lafortezaNo ratings yet

- UntitledDocument5 pagesUntitledemielyn lafortezaNo ratings yet

- Heat Exchanger For LectureDocument51 pagesHeat Exchanger For Lectureemielyn lafortezaNo ratings yet

- St. Thomas College MouDocument4 pagesSt. Thomas College MouParas PanwarNo ratings yet

- Capestone ProjectDocument93 pagesCapestone ProjectNikhil MahadikNo ratings yet

- FULLTEXT01Document95 pagesFULLTEXT01prabhuNo ratings yet

- Key Issues With Implementing LOPADocument5 pagesKey Issues With Implementing LOPADiego Vargas D100% (1)

- Tugas 3 ISBDDocument5 pagesTugas 3 ISBDlutfii dyahNo ratings yet

- Efek Moderasi Kontrol Diri Pada Hubungan Sifat Materialisme Terhadap Pembelian Impulsif OnlineDocument22 pagesEfek Moderasi Kontrol Diri Pada Hubungan Sifat Materialisme Terhadap Pembelian Impulsif OnlineDinda Aulia PutriNo ratings yet

- Rating - Underwriting NoticeDocument3 pagesRating - Underwriting NoticelesliedariqusNo ratings yet

- SHINE CONTRACT-DilshaniDocument5 pagesSHINE CONTRACT-Dilshanimariyamshadha2No ratings yet

- Afar Reviewer 1Document6 pagesAfar Reviewer 1StrwbrryNo ratings yet

- Abony Healthcare Po 1372Document2 pagesAbony Healthcare Po 1372pawan BansalNo ratings yet

- Lecture 2.business in India.Document13 pagesLecture 2.business in India.vj1234567No ratings yet

- Chapters About Coirfed AlappuzhaDocument79 pagesChapters About Coirfed AlappuzhaStephen Mani0% (1)

- Unit-1 PMOB NotesDocument16 pagesUnit-1 PMOB NotesKeerthana ENo ratings yet

- Prestige Institute of Management and Research (Department of Law)Document10 pagesPrestige Institute of Management and Research (Department of Law)Naman DWIVEDINo ratings yet

- Chapter 3Document46 pagesChapter 3James David Torres MateoNo ratings yet

- Printmedia 100813115605 Phpapp02Document24 pagesPrintmedia 100813115605 Phpapp02Sudesh BanareNo ratings yet

- Transport Policy: Begoña Guirao, Antonio García-Pastor, María Eugenia López-LambasDocument10 pagesTransport Policy: Begoña Guirao, Antonio García-Pastor, María Eugenia López-LambasHermis aaron alcantara rojasNo ratings yet

- Corporate Governance Imp QuestionsDocument11 pagesCorporate Governance Imp Questionskomalc2026No ratings yet

- Evaluation of WhittakerDocument4 pagesEvaluation of WhittakerAmar narayanNo ratings yet

- Cash Management and Working Capital ProblemsDocument2 pagesCash Management and Working Capital ProblemsRachel RiveraNo ratings yet

- Solved On August 19 2019 Portland Corporation Repurchases 1 400 Shares ofDocument1 pageSolved On August 19 2019 Portland Corporation Repurchases 1 400 Shares ofAnbu jaromiaNo ratings yet

- Compensation StructureDocument7 pagesCompensation StructureRajni Kant SinghNo ratings yet

- Accounting (Share Capital)Document11 pagesAccounting (Share Capital)PowerPoint GoNo ratings yet

- Unit 5: Getting Started On An HXM Solution StrategyDocument10 pagesUnit 5: Getting Started On An HXM Solution StrategyDipak NandeshwarNo ratings yet

- Company Law .PDF ShareDocument42 pagesCompany Law .PDF ShareMd Razu AhmedNo ratings yet

- Offer Letter 22879 13 02 2024 12 14 12Document4 pagesOffer Letter 22879 13 02 2024 12 14 12dk6993140No ratings yet