0% found this document useful (0 votes)

81 viewsModule 4 - Financial Statement Analysis Lecture S23

The document provides an overview of accounting concepts including:

- The agenda covers basic accounting principles, financial statements, depreciation, and financial ratios.

- Accounting records and classifies financial transactions and events in monetary terms. Financial statements include the balance sheet, income statement, and statement of cash flows.

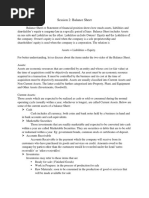

- The balance sheet lists assets, liabilities, and equity on a specific date. The basic accounting equation is Assets = Liabilities + Equity.

- The income statement reports revenues and expenses over a period of time.

Uploaded by

Prachi YadavCopyright

© © All Rights Reserved

Available Formats

Download as PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

81 viewsModule 4 - Financial Statement Analysis Lecture S23

The document provides an overview of accounting concepts including:

- The agenda covers basic accounting principles, financial statements, depreciation, and financial ratios.

- Accounting records and classifies financial transactions and events in monetary terms. Financial statements include the balance sheet, income statement, and statement of cash flows.

- The balance sheet lists assets, liabilities, and equity on a specific date. The basic accounting equation is Assets = Liabilities + Equity.

- The income statement reports revenues and expenses over a period of time.

Uploaded by

Prachi YadavCopyright

© © All Rights Reserved

Available Formats

Download as PDF, TXT or read online on Scribd

/ 25