PWC - Pre Budget Briefing Mining June 2023

PWC - Pre Budget Briefing Mining June 2023

Download as pdf or txt

You might also like

- Apporva Chandra Comm Report (ACC)Document23 pagesApporva Chandra Comm Report (ACC)ThangarajNo ratings yet

- Asian Paints Financial ModelDocument15 pagesAsian Paints Financial ModelDeepak NechlaniNo ratings yet

- IpccDocument6 pagesIpccmichaeljudika578No ratings yet

- B. Model Ekonomi Teknis: Economic Model Annual SummaryDocument7 pagesB. Model Ekonomi Teknis: Economic Model Annual SummaryDheo AlviansyahNo ratings yet

- TOFE EN May 2023-140723Document10 pagesTOFE EN May 2023-140723boydilinh012No ratings yet

- UBL Annual Report 2018-96Document1 pageUBL Annual Report 2018-96IFRS LabNo ratings yet

- Hibiscuss May 2022Document13 pagesHibiscuss May 2022admn.bbmbuildersNo ratings yet

- HDF 2021-22 30-6-2022Document29 pagesHDF 2021-22 30-6-2022sami ul haqNo ratings yet

- Mining: Production and Sales (Preliminary) April 2023Document14 pagesMining: Production and Sales (Preliminary) April 2023anastasi mankese mokgobuNo ratings yet

- Hort Stats Fruit 22 23Document152 pagesHort Stats Fruit 22 23ladykarenna7No ratings yet

- Full Year Results Presentation 2022Document39 pagesFull Year Results Presentation 2022Kit WooNo ratings yet

- Mohnish Pabrai's Valuation Model (Modified) : FCF (Free Cash Flow)Document8 pagesMohnish Pabrai's Valuation Model (Modified) : FCF (Free Cash Flow)sohamNo ratings yet

- TASCODocument13 pagesTASCOsozodaaaNo ratings yet

- Cash - Cost - EBITDA 2017-2022 FVDocument7 pagesCash - Cost - EBITDA 2017-2022 FVJulian Brescia2No ratings yet

- Weekly Economic Update 37 - 2019Document4 pagesWeekly Economic Update 37 - 2019jyl12No ratings yet

- EC 052 Dt. 14.06.2022 Import of Veg. Oils Nov.21 May 22 - CompressedDocument7 pagesEC 052 Dt. 14.06.2022 Import of Veg. Oils Nov.21 May 22 - CompressedSAMYAK PANDEYNo ratings yet

- MEI 202311 eDocument22 pagesMEI 202311 eChathura WickramaNo ratings yet

- MM Forgings MM Forgings: Auto AutoDocument22 pagesMM Forgings MM Forgings: Auto Autorchawdhry123No ratings yet

- OZL Macquarie Australia ConferenceDocument13 pagesOZL Macquarie Australia ConferenceStephen C.No ratings yet

- Adro Mirae 02 Nov 2023 231102 150020Document9 pagesAdro Mirae 02 Nov 2023 231102 150020marcellusdarrenNo ratings yet

- Daily 01-05-2023Document1 pageDaily 01-05-2023Andi RiyantoNo ratings yet

- Fixed AssetsDocument11 pagesFixed AssetsIrish PitargueNo ratings yet

- Dec-2021 Monthly Delivery of Different Cement Plant-2021Document1 pageDec-2021 Monthly Delivery of Different Cement Plant-2021Alinoor TanvirNo ratings yet

- PT Merdeka Copper Gold TBK: Q3 2021 UpdateDocument37 pagesPT Merdeka Copper Gold TBK: Q3 2021 UpdateRichard nicoNo ratings yet

- Dashen Bank 2023 Report 4 Website 2 1Document63 pagesDashen Bank 2023 Report 4 Website 2 1yemaneatakNo ratings yet

- MENA Mining Report - Q1 2023Document60 pagesMENA Mining Report - Q1 2023saim siam100% (1)

- LNG Monthly March 2022 - 1Document35 pagesLNG Monthly March 2022 - 1Hello RomaNo ratings yet

- Q2 2017 Financial & Operating Results: Friday, July 28, 2017Document36 pagesQ2 2017 Financial & Operating Results: Friday, July 28, 2017kaiselkNo ratings yet

- KMG Valuation ReportDocument30 pagesKMG Valuation ReportAmanksvNo ratings yet

- Gold MinersDocument5 pagesGold Minerssaurabh.shrivastavNo ratings yet

- FIRST QUANTUM MINERALS - Production-Results-and-3-Year-Guidance-FINALDocument7 pagesFIRST QUANTUM MINERALS - Production-Results-and-3-Year-Guidance-FINALchinuasfaNo ratings yet

- SSAB - Presentation Q2 2023 - FDocument29 pagesSSAB - Presentation Q2 2023 - FHochbauer MáriaNo ratings yet

- Andritz Presentation GCC Conference 2023 DataDocument11 pagesAndritz Presentation GCC Conference 2023 DataAdam MooseNo ratings yet

- Schedule & S-Curve - Rev.01 - Submitted To JKR (Financial S Curve March 2021)Document1 pageSchedule & S-Curve - Rev.01 - Submitted To JKR (Financial S Curve March 2021)Tony JamesNo ratings yet

- P 2041 June 2022Document18 pagesP 2041 June 2022vuyanixanise1273No ratings yet

- Rajrappa PPT 16.04.2023Document40 pagesRajrappa PPT 16.04.2023jenniNo ratings yet

- Simulasi Fuel PurchaseDocument3 pagesSimulasi Fuel Purchasezulkarnain.epnNo ratings yet

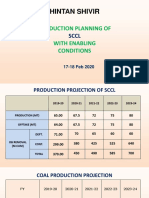

- Chintan Shivir: Production Planning of With Enabling ConditionsDocument25 pagesChintan Shivir: Production Planning of With Enabling ConditionsKudlappa DesaiNo ratings yet

- SDR FY 23 Data Pack FinalDocument31 pagesSDR FY 23 Data Pack FinalNistha ChakrabortyNo ratings yet

- Annexure 7 - Audited Financial Results For The Year Ended March 31 2011Document3 pagesAnnexure 7 - Audited Financial Results For The Year Ended March 31 2011PGurusNo ratings yet

- តារាងប្រតិបត្តិការហិរញ្ញវត្ថុ និង សេដ្ឋកិច្ចសម្រាប់ ខែវិច្ឆិកា ឆ្នាំ ២០២៣ ENGDocument10 pagesតារាងប្រតិបត្តិការហិរញ្ញវត្ថុ និង សេដ្ឋកិច្ចសម្រាប់ ខែវិច្ឆិកា ឆ្នាំ ២០២៣ ENGNurakSityaNo ratings yet

- EOT Calculation Sheet Revised As Per SirDocument10 pagesEOT Calculation Sheet Revised As Per Sirabhishek negi0% (1)

- O&G Analysis Mar 2017Document9 pagesO&G Analysis Mar 2017Anonymous C8mcpc8uNo ratings yet

- Draft Fourth Quarter SAUDI Donor Report 2022Document14 pagesDraft Fourth Quarter SAUDI Donor Report 2022Tadese Mulisa0% (1)

- AR_2023-24Document80 pagesAR_2023-24Prashant SwamiNo ratings yet

- Target MineDocument4 pagesTarget MineOwm Close CorporationNo ratings yet

- BOG Notice No 53 FMD T Bills 23rd July 2021 Auctresults 1756Document1 pageBOG Notice No 53 FMD T Bills 23rd July 2021 Auctresults 1756Fuaad DodooNo ratings yet

- LPPF Laporan InformasiDocument13 pagesLPPF Laporan InformasiDaniel PradityaNo ratings yet

- Gradual Increase in Rice Production Area and Reduction of Post-Harvest LossesDocument4 pagesGradual Increase in Rice Production Area and Reduction of Post-Harvest LossesDodong MelencionNo ratings yet

- Positive: PETRONAS Activity Outlook (PAO) 2021-23Document11 pagesPositive: PETRONAS Activity Outlook (PAO) 2021-23umyatika92No ratings yet

- BUDGET CALL Proforma For BE I-IVDocument10 pagesBUDGET CALL Proforma For BE I-IVShaheer HashmiNo ratings yet

- I-Claim Expense August 2020 W3Document39 pagesI-Claim Expense August 2020 W3HAN SUKARMANNo ratings yet

- CZ-III, IV&v DBM & BC Expenditure Details 17.02.2023Document4 pagesCZ-III, IV&v DBM & BC Expenditure Details 17.02.2023Abhishek BhandariNo ratings yet

- Corporate Presentation: PT Bukit Asam TBKDocument21 pagesCorporate Presentation: PT Bukit Asam TBKyusria setia85No ratings yet

- RFP-01353 - Price Update 2Document69 pagesRFP-01353 - Price Update 2the next miamiNo ratings yet

- December 2022 Market Operations HighlightsDocument9 pagesDecember 2022 Market Operations HighlightssychezmuNo ratings yet

- KMG Valuation Report_MidtermDocument32 pagesKMG Valuation Report_MidtermDariga BaiseitNo ratings yet

- Norwegian q4 2022 ReportDocument23 pagesNorwegian q4 2022 ReportJohnNo ratings yet

- The Increasing Importance of Migrant Remittances from the Russian Federation to Central AsiaFrom EverandThe Increasing Importance of Migrant Remittances from the Russian Federation to Central AsiaNo ratings yet

- Asia Small and Medium-Sized Enterprise Monitor 2022: Volume I: Country and Regional ReviewsFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2022: Volume I: Country and Regional ReviewsNo ratings yet

- Tribologist - Barrick Gold Corporation - DASMDocument4 pagesTribologist - Barrick Gold Corporation - DASMdamson allyNo ratings yet

- Barrick Gold Case PDFDocument18 pagesBarrick Gold Case PDFShahpar AltafNo ratings yet

- Advert - Industrial Practical TrainingDocument2 pagesAdvert - Industrial Practical TrainingAmosi Amosi100% (1)

- Myb3 2017 18 TanzaniaDocument4 pagesMyb3 2017 18 TanzaniaPuneet Nagwan100% (1)

- Joseph Bulugu CV PDFDocument4 pagesJoseph Bulugu CV PDFJoseph buluguNo ratings yet

- University of Dar Es Salaam: Bulyanhulu - BARRICKDocument72 pagesUniversity of Dar Es Salaam: Bulyanhulu - BARRICKfelycian sylivesterNo ratings yet

- 2017 Acacia Annual Report AccountsDocument180 pages2017 Acacia Annual Report AccountsDeus SindaNo ratings yet

- Prosperity in A Crisis Economy-The Nyamongo Gold Boom Tanzania 1973s-1993Document19 pagesProsperity in A Crisis Economy-The Nyamongo Gold Boom Tanzania 1973s-1993Zakaria NgerejaNo ratings yet

- Barrick Gold Corporation - CaseDocument14 pagesBarrick Gold Corporation - Casekane eveNo ratings yet

- ACACIA-Results For The 3 Months Ended 31 March 2019 - FINAL (1) - 1Document22 pagesACACIA-Results For The 3 Months Ended 31 March 2019 - FINAL (1) - 1Baraka LetaraNo ratings yet