Dior Clothing Corporation's cash flow statement for 2009 and 2008 is to be prepared using the indirect method. The balance sheets as of March 31, 2009 and 2008 are provided, along with additional information regarding provision for tax, sale of fixed assets, dividends paid, and issuance of new debentures.

Dior Clothing Corporation's cash flow statement for 2009 and 2008 is to be prepared using the indirect method. The balance sheets as of March 31, 2009 and 2008 are provided, along with additional information regarding provision for tax, sale of fixed assets, dividends paid, and issuance of new debentures.

Dior Clothing Corporation's cash flow statement for 2009 and 2008 is to be prepared using the indirect method. The balance sheets as of March 31, 2009 and 2008 are provided, along with additional information regarding provision for tax, sale of fixed assets, dividends paid, and issuance of new debentures.

Dior Clothing Corporation's cash flow statement for 2009 and 2008 is to be prepared using the indirect method. The balance sheets as of March 31, 2009 and 2008 are provided, along with additional information regarding provision for tax, sale of fixed assets, dividends paid, and issuance of new debentures.

Download as DOCX, PDF, TXT or read online from Scribd

Download as docx, pdf, or txt

You are on page 1/ 2

FABM2

CASH FLOW STATEMENT QUIZ FABM2

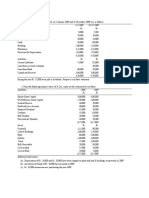

From the particulars given ahead prepare the cash flow statement as per AS-3 (Revised) using the CASH FLOW STATEMENT QUIZ indirect method: From the particulars given ahead prepare the cash flow statement as per AS-3 (Revised) using the Dior Clothing Corporation indirect method: Balance Sheets As At 31 March, ..... Dior Clothing Corporation Liabilities 2009 2008 Balance Sheets As At 31 March, ..... Equity Share Capital Php 80,000 Php 55,000 Liabilities 2009 2008 10% Preference Share Capital 20,000 25,000 Equity Share Capital Php 80,000 Php 55,000 General Reserve 7,600 4,000 10% Preference Share Capital 20,000 25,000 Profit & Loss Account 2,400 2,000 General Reserve 7,600 4,000 15% Debentures 14,000 12,000 Profit & Loss Account 2,400 2,000 Creditors 22,000 24,000 15% Debentures 14,000 12,000 Proposed Dividend 8,000 10,000 Creditors 22,000 24,000 Provision for Taxation 8,400 6,000 Proposed Dividend 8,000 10,000 1,62,400 1,38,000 Provision for Taxation 8,400 6,000 Assets 2009 2008 1,62,400 1,38,000 Fixed Assets 80,000 82,000 Assets 2009 2008 Less: Accumulated Depreciation 30,000 22,000 Fixed Assets 80,000 82,000 50,000 60,000 Less: Accumulated Depreciation 30,000 22,000 Stock 70,000 60,000 50,000 60,000 Debtors 34,400 15,000 Stock 70,000 60,000 Cash 7,000 2,400 Debtors 34,400 15,000 Prepaid Expenses 1,000 600 Cash 7,000 2,400 1,62,400 1,38,000 Prepaid Expenses 1,000 600 1,62,400 1,38,000 Additional Information: (a) Provision for tax made Rs. 9,400. Additional Information: (b) Fixed assets costing Rs. 20,000 (accumulated depreciation till the date of sale on them Rs. 6,000) (a) Provision for tax made Rs. 9,400. were sold for Rs. 10,000. (b) Fixed assets costing Rs. 20,000 (accumulated depreciation till the date of sale on them Rs. 6,000) (c) Interim dividend paid during the year Rs. 9,000. The proposed dividend of last year was declared were sold for Rs. 10,000. and paid during the year. Ignore corporate dividend tax. (c) Interim dividend paid during the year Rs. 9,000. The proposed dividend of last year was declared (d) New debentures were issued on 31 March 2009. and paid during the year. Ignore corporate dividend tax. (d) New debentures were issued on 31 March 2009.