Cost Management

Cost Management

Download as pdf or txt

You might also like

- IT Category Strategy TemplateDocument10 pagesIT Category Strategy Templatepratyush parmarNo ratings yet

- ISO19650 Cheat SheetDocument5 pagesISO19650 Cheat SheetRichard GarciaNo ratings yet

- Standard Two-Storey SCHL BLDG DUPADocument157 pagesStandard Two-Storey SCHL BLDG DUPAKaren Balisacan Segundo Ruiz100% (2)

- Presentation PS (Overview of SAP PS 1module)Document32 pagesPresentation PS (Overview of SAP PS 1module)Raman Satish75% (4)

- Lifting PlanDocument23 pagesLifting PlanAbdul GhaffarNo ratings yet

- D200-1995 - Project Checklist - 001Document24 pagesD200-1995 - Project Checklist - 001Maram SabaNo ratings yet

- CRM and ISU OverviewDocument92 pagesCRM and ISU OverviewAcharya Daksha100% (2)

- 4.QTY Presentation 4Document15 pages4.QTY Presentation 4asregidhaguNo ratings yet

- CCM Lecture 7Document111 pagesCCM Lecture 7Er Inamul HassanNo ratings yet

- WK 3Document28 pagesWK 3joehe2625No ratings yet

- Project Summary Template 01Document2 pagesProject Summary Template 01Agus WahiyudinNo ratings yet

- SAP - PS - Overview - Kopya - KopyaDocument32 pagesSAP - PS - Overview - Kopya - KopyaTurn RectNo ratings yet

- SAP PS OverviewDocument32 pagesSAP PS OverviewTurn RectNo ratings yet

- Welcome To Project System (PS)Document32 pagesWelcome To Project System (PS)Turn RectNo ratings yet

- 2010.04.21 AIA LA Presentation FINALDocument8 pages2010.04.21 AIA LA Presentation FINALaialosangelesNo ratings yet

- Engineering Project Implementation CycleDocument2 pagesEngineering Project Implementation CycleBinyam BekeleNo ratings yet

- Annexure A-Centralized Estimation Process Map - EICDocument1 pageAnnexure A-Centralized Estimation Process Map - EICKamal HassanNo ratings yet

- A C E T: Ctivity OST Stimates EmplateDocument7 pagesA C E T: Ctivity OST Stimates Emplateهيثم الحدادNo ratings yet

- JCRDocument11 pagesJCRabhiroopboseNo ratings yet

- TestSubject 001Document4 pagesTestSubject 001chareitheresealdeaNo ratings yet

- GeM Bidding 4188133Document5 pagesGeM Bidding 4188133Atharva PrasadNo ratings yet

- LU2 - Pre Contract StageDocument24 pagesLU2 - Pre Contract StageMervyn WongNo ratings yet

- 08-08-20 MPS PDFDocument4 pages08-08-20 MPS PDFSona NingNo ratings yet

- MMG - Evaluation Report_FINAL newDocument37 pagesMMG - Evaluation Report_FINAL newanirudh.kumar.2015No ratings yet

- PCM-1Document15 pagesPCM-1Hurmat AhmedNo ratings yet

- Navbuild Eu Erp CetusDocument3 pagesNavbuild Eu Erp CetusSyed ImranNo ratings yet

- Technical BOSDocument37 pagesTechnical BOSJohanna GómezNo ratings yet

- PS-Real EstateDocument32 pagesPS-Real Estatechetan salunkeNo ratings yet

- Non Conformance Report-FormatDocument1 pageNon Conformance Report-FormatRahul SinghNo ratings yet

- 09 Project Cost Estimation and BudgetingDocument48 pages09 Project Cost Estimation and BudgetingSaketNo ratings yet

- Retail Management: Private & Confidential For Use and Circulation Within Acorn Holdings LimitedDocument10 pagesRetail Management: Private & Confidential For Use and Circulation Within Acorn Holdings LimitedIndresh Singh SalujaNo ratings yet

- Appendix D Measuring The Front-End Definition LevelDocument1 pageAppendix D Measuring The Front-End Definition LevelGOWTHAMNo ratings yet

- Services To GASCO On Unified Drawing Format & Drawing AutomationDocument14 pagesServices To GASCO On Unified Drawing Format & Drawing Automationmadhu_karekar100% (1)

- Approved Use Matrix - GSADocument1 pageApproved Use Matrix - GSANagarjuna Reddy MNo ratings yet

- Roject Anagement LAN: E.S Pak Power Plant Program, Chakri, PakistanDocument1 pageRoject Anagement LAN: E.S Pak Power Plant Program, Chakri, PakistanAnusheh AsadNo ratings yet

- PCM Lesson 3Document21 pagesPCM Lesson 3Prasad ShettyNo ratings yet

- SAP Project SystemsDocument6 pagesSAP Project SystemskhanmdNo ratings yet

- Activity Based CostingDocument17 pagesActivity Based CostingPoonamNo ratings yet

- Cloud Business Case Development: Key AssumptionsDocument86 pagesCloud Business Case Development: Key Assumptionsadilwx30357No ratings yet

- 2-2 Location Layout IMBA StudentsDocument9 pages2-2 Location Layout IMBA StudentsLazaros KarapouNo ratings yet

- Building A Business Case For Shared Geospatial Data and ServicesDocument53 pagesBuilding A Business Case For Shared Geospatial Data and ServicesryanshaikhNo ratings yet

- TNB Application Process & Requirement For FiTDocument24 pagesTNB Application Process & Requirement For FiTrex100% (1)

- Bid Process MNGMTDocument2 pagesBid Process MNGMTK SNo ratings yet

- Managerial Accounting - TeshaleDocument123 pagesManagerial Accounting - Teshaleberhanu seyoumNo ratings yet

- Capturing Data Requirements: Expense BudgetDocument1 pageCapturing Data Requirements: Expense Budgetaasmita2007No ratings yet

- TEC202 Advanced Development BookletDocument2 pagesTEC202 Advanced Development BookletNiko Christian ArnaldoNo ratings yet

- Lecture 2 - CommunicationDocument28 pagesLecture 2 - CommunicationUMMI KALTHOM NABILAH ISMAILNo ratings yet

- Basis of EstimatesDocument39 pagesBasis of EstimatesFredie LabradorNo ratings yet

- 14A. SLB Planning PhaseDocument82 pages14A. SLB Planning PhaseDonald StraubNo ratings yet

- Sip ReportDocument1 pageSip Reportsreejan.chakrabortybm23No ratings yet

- Contract Management and Related Correspondence-1Document58 pagesContract Management and Related Correspondence-1Yogesh GuruNo ratings yet

- Lecture 2 - CommunicationDocument28 pagesLecture 2 - CommunicationGloria DanielNo ratings yet

- Webinar CubicostDocument42 pagesWebinar CubicostSupardi PardiNo ratings yet

- ATG - SAP Project System Overview 1Document18 pagesATG - SAP Project System Overview 1Adão da luzNo ratings yet

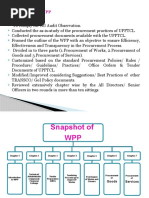

- Preparation of WPPDocument16 pagesPreparation of WPPae etdcNo ratings yet

- Tender Details240924040846Document3 pagesTender Details240924040846rajNo ratings yet

- Government EProcurement SystemDocument1 pageGovernment EProcurement SystemAnurag JainNo ratings yet

- Lecture 11 - Project Development & OIMSDocument12 pagesLecture 11 - Project Development & OIMSxjaf01No ratings yet

- Agile Procurement: Volume II: Designing and Implementing a Digital TransformationFrom EverandAgile Procurement: Volume II: Designing and Implementing a Digital TransformationNo ratings yet

- Service-Oriented Modeling: Service Analysis, Design, and ArchitectureFrom EverandService-Oriented Modeling: Service Analysis, Design, and ArchitectureNo ratings yet

- Plan 11Document1 pagePlan 11Abdul GhaffarNo ratings yet

- Civil - 1Document14 pagesCivil - 1Abdul GhaffarNo ratings yet

- Schedule Assessment Guide - Best Practices For Project Schedules Dic15Document240 pagesSchedule Assessment Guide - Best Practices For Project Schedules Dic15José Nolasco100% (1)

- Detailed Calculation PDFDocument2 pagesDetailed Calculation PDFAbdul GhaffarNo ratings yet

- Shuttering WorksDocument3 pagesShuttering WorksAbdul Ghaffar100% (1)

- Order 01Document1 pageOrder 01Abdul GhaffarNo ratings yet

- Leed PointsDocument1 pageLeed PointsAbdul GhaffarNo ratings yet

- Block WorkDocument4 pagesBlock WorkAbdul Ghaffar100% (1)

- Concrete WorkDocument3 pagesConcrete WorkAbdul Ghaffar100% (1)

- Circular 400Document2 pagesCircular 400Abdul GhaffarNo ratings yet

- 23 ZA DC F 107 Excavation Design Review ChecklistDocument1 page23 ZA DC F 107 Excavation Design Review ChecklistAbdul GhaffarNo ratings yet

- Back Filling WorksDocument3 pagesBack Filling WorksAbdul Ghaffar100% (1)

- Chapter 9 - Insulated Sandwich PanelsDocument11 pagesChapter 9 - Insulated Sandwich PanelsAbdul GhaffarNo ratings yet

- Circular 364 - Material Quality ChecklistDocument9 pagesCircular 364 - Material Quality ChecklistAbdul GhaffarNo ratings yet

- Thesis On Ias 16Document4 pagesThesis On Ias 16BestCustomPaperWritingServiceCanada100% (2)

- A Dissertation: Submitted in Partial Fulfilment of The Requirements For The Degree ofDocument57 pagesA Dissertation: Submitted in Partial Fulfilment of The Requirements For The Degree ofBÐ BøYNo ratings yet

- Chapter 3 NREE PDFDocument77 pagesChapter 3 NREE PDFCabdilaahi CabdiNo ratings yet

- Tristar Home AppliancesDocument10 pagesTristar Home AppliancesAnurag KhaireNo ratings yet

- MI1 TestDocument9 pagesMI1 TestĐỗ Hoàng DungNo ratings yet

- EOT and Cost - FIDIC Red Book 1999Document5 pagesEOT and Cost - FIDIC Red Book 1999Gilbert Maruli Hutajulu100% (2)

- Man Acctg & Control - Topic 2Document25 pagesMan Acctg & Control - Topic 2Queenie Marie Obial AlasNo ratings yet

- Acc 206 Manufacturing Account 2021Document21 pagesAcc 206 Manufacturing Account 2021Boi NonoNo ratings yet

- MGT Term PaperDocument10 pagesMGT Term PaperMd JUNAYEDNo ratings yet

- Prices Revenue Manageme NT: Setting and ImplementingDocument36 pagesPrices Revenue Manageme NT: Setting and ImplementingAl ImranNo ratings yet

- Ipsas 11-Construction Contracts: Contracts, Published by The International Accounting Standards Board (IASB)Document28 pagesIpsas 11-Construction Contracts: Contracts, Published by The International Accounting Standards Board (IASB)riska putri utamiNo ratings yet

- Allen 8e PPT Ch06 FinalDocument37 pagesAllen 8e PPT Ch06 FinalNURHAZWANI ASMIDA BINTI ZAHARIN / UPMNo ratings yet

- Mock D QDocument15 pagesMock D QZeeshan Shaikh100% (1)

- Accounting Standard 8Document7 pagesAccounting Standard 8api-3828505100% (1)

- Cost Allocation: Joint Products and ByproductsDocument32 pagesCost Allocation: Joint Products and ByproductsTita NurvitaNo ratings yet

- U Sgov Principals On LaborDocument63 pagesU Sgov Principals On LaborBeverly Baker-HarrisNo ratings yet

- 3 Classifications of Costs PDFDocument3 pages3 Classifications of Costs PDFEi HmmmNo ratings yet

- Engineering-Economics-1610656365Document254 pagesEngineering-Economics-1610656365baternaangelmaeavilaNo ratings yet

- Business Activity Chapter 1 NotesDocument5 pagesBusiness Activity Chapter 1 Notestafadzwa mutandiroNo ratings yet

- mgt101 Paper11Document93 pagesmgt101 Paper11Ayesha MughalNo ratings yet

- 57136bos46280inter p3 QDocument8 pages57136bos46280inter p3 QSURYA PRAKASH SHARMANo ratings yet

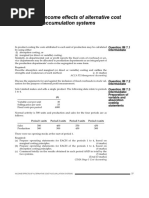

- Income Effects of Alternative Cost Accumulation Systems: Question IM 7.1 IntermediateDocument8 pagesIncome Effects of Alternative Cost Accumulation Systems: Question IM 7.1 IntermediateChansa KapambweNo ratings yet

- Mergers and Acquisitions: Reason and Results: Ali-Yrkkö, JyrkiDocument40 pagesMergers and Acquisitions: Reason and Results: Ali-Yrkkö, Jyrkidanphamm226No ratings yet

- Answers Managerial Accounting Prelim ExaminationDocument4 pagesAnswers Managerial Accounting Prelim ExaminationRegine ReyesNo ratings yet

- Pricewell Single Entity Financial StatementsDocument6 pagesPricewell Single Entity Financial StatementsBig SmutNo ratings yet

- Notes 2 Rate AnalysisDocument9 pagesNotes 2 Rate AnalysisMADHU SUDAN H.N C-ENo ratings yet

- Mid Term Assignment On: The Superior University LahoreDocument9 pagesMid Term Assignment On: The Superior University LahoreFaizan ChNo ratings yet

- Reconciliation of Cost and Financial AccountingDocument5 pagesReconciliation of Cost and Financial AccountingMighty RajuNo ratings yet

- CleanCloud Profit CalculatorDocument5 pagesCleanCloud Profit CalculatorMahmoud AliNo ratings yet