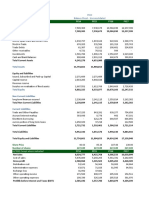

DU Pont Analysis

DU Pont Analysis

Download as pdf or txt

You might also like

- IMT CeresDocument5 pagesIMT Ceresrithvik roy100% (1)

- Petron Corp - Financial Analysis From 2014 - 2018Document4 pagesPetron Corp - Financial Analysis From 2014 - 2018Neil Nadua100% (1)

- Punjab Public Service Commission: PPSC-5Document1 pagePunjab Public Service Commission: PPSC-5shani2010No ratings yet

- Chapter 02 - Basic Financial StatementsDocument111 pagesChapter 02 - Basic Financial Statementsyujia Zhai100% (1)

- Sir Sarwar AFSDocument41 pagesSir Sarwar AFSawaischeemaNo ratings yet

- Financial Statements Analysis: Arsalan FarooqueDocument31 pagesFinancial Statements Analysis: Arsalan FarooqueMuhib NoharioNo ratings yet

- MnA Financial Statement Analysis Group 4Document37 pagesMnA Financial Statement Analysis Group 4bennettuniversity.studentNo ratings yet

- Final Report - Draft2Document32 pagesFinal Report - Draft2shyamagniNo ratings yet

- Unity Food QR Sep 2021 (Nov 02)Document31 pagesUnity Food QR Sep 2021 (Nov 02)Sohail MehmoodNo ratings yet

- UAS ALK Ganjil 2018-2019 SulasDocument10 pagesUAS ALK Ganjil 2018-2019 SulasZulkarnainNo ratings yet

- Finance For Non-Finance: Ratios AppleDocument12 pagesFinance For Non-Finance: Ratios AppleAvinash GanesanNo ratings yet

- Kamel Genuine Parts CompanyDocument4 pagesKamel Genuine Parts CompanyShamsher Ali KhanNo ratings yet

- Accounting Presentation (Beximco Pharma)Document18 pagesAccounting Presentation (Beximco Pharma)asifonikNo ratings yet

- 5 6120493211875018431Document62 pages5 6120493211875018431Hafsah Amod DisomangcopNo ratings yet

- Tesla FSAPDocument20 pagesTesla FSAPSihongYanNo ratings yet

- Afs ProjectDocument8 pagesAfs ProjectAnam AbrarNo ratings yet

- Group 11 - Mahindra and MahindraDocument10 pagesGroup 11 - Mahindra and Mahindrasovinahalli 1234No ratings yet

- Assets: Balance SheetDocument4 pagesAssets: Balance SheetAsadvirkNo ratings yet

- DGKC Financial With AFN Class Work Fall 2020 - SolutionDocument14 pagesDGKC Financial With AFN Class Work Fall 2020 - SolutionOsama HashmiNo ratings yet

- UAS ALK Ganjil 2018-2019Document11 pagesUAS ALK Ganjil 2018-2019ZulkarnainNo ratings yet

- Extract From The Warehouse Group Financial Statement With Analyses - AlbanyDocument11 pagesExtract From The Warehouse Group Financial Statement With Analyses - Albanyjoehe2625No ratings yet

- Analysis of BankDocument15 pagesAnalysis of BankSadiq SayaniNo ratings yet

- PIOC Data For Corporate ValuationDocument6 pagesPIOC Data For Corporate ValuationMuhammad Ali SamarNo ratings yet

- Ar Data Toyota & HondaDocument10 pagesAr Data Toyota & HondaRimsha MalikNo ratings yet

- A1.1 Maturity Matching-5Document16 pagesA1.1 Maturity Matching-5Mohammad KhataybehNo ratings yet

- Download Financial Statements to Spreadsheet(s) (1)Document192 pagesDownload Financial Statements to Spreadsheet(s) (1)Tiến Lương DânNo ratings yet

- Download Financial Statements to Spreadsheet(s)Document192 pagesDownload Financial Statements to Spreadsheet(s)Tiến Lương DânNo ratings yet

- 4 ChapterDocument28 pages4 ChapterFatima FarooqNo ratings yet

- Fintech Company:Paytm: 1.financial Statements and Records of CompanyDocument7 pagesFintech Company:Paytm: 1.financial Statements and Records of CompanyAnkita NighutNo ratings yet

- Fra Project FinalllDocument23 pagesFra Project Finalllshahtaj khanNo ratings yet

- Starbucks Corporation (SBUX) Income Statement: Análisis de Estados FinancierosDocument7 pagesStarbucks Corporation (SBUX) Income Statement: Análisis de Estados FinancierosjosolcebNo ratings yet

- Vodafone Class 5Document6 pagesVodafone Class 5akashkr619No ratings yet

- FINM 7044 Group Assignment 终Document4 pagesFINM 7044 Group Assignment 终jimmmmNo ratings yet

- Income Statement - PEPSICODocument11 pagesIncome Statement - PEPSICOAdriana MartinezNo ratings yet

- MPCLDocument4 pagesMPCLRizwan Sikandar 6149-FMS/BBA/F20No ratings yet

- Boston Chicken CaseDocument7 pagesBoston Chicken CaseDji YangNo ratings yet

- Group 68 FinanceDocument14 pagesGroup 68 FinanceAbdurehman Ullah khanNo ratings yet

- FMOD PROJECT Ouijhggfffe5Document97 pagesFMOD PROJECT Ouijhggfffe5Omer CrestianiNo ratings yet

- Comparative Income Statements and Balance Sheets For Merck ($ Millions) FollowDocument6 pagesComparative Income Statements and Balance Sheets For Merck ($ Millions) FollowIman naufalNo ratings yet

- DG Khan Cement Financial StatementsDocument8 pagesDG Khan Cement Financial StatementsAsad BumbiaNo ratings yet

- IndusDocument5 pagesIndusFateen HabibNo ratings yet

- EREGL DCF ModelDocument10 pagesEREGL DCF ModelKevser BozoğluNo ratings yet

- Thế Giới Di Động 2022Document16 pagesThế Giới Di Động 2022Phạm Thu HằngNo ratings yet

- Deferred Tax Asset Retirement Benefit Assets: TotalDocument2 pagesDeferred Tax Asset Retirement Benefit Assets: TotalSrb RNo ratings yet

- Financial Statement Analysis of Masan Company Masan GroupDocument24 pagesFinancial Statement Analysis of Masan Company Masan GroupTammy DaoNo ratings yet

- Bangladesh q3 Report 2020 Tcm244 556009 enDocument8 pagesBangladesh q3 Report 2020 Tcm244 556009 entdebnath_3No ratings yet

- Greetings Everyone: To My PresentationDocument15 pagesGreetings Everyone: To My PresentationZakaria ShuvoNo ratings yet

- Askari Bank Limited Financial Statement AnalysisDocument16 pagesAskari Bank Limited Financial Statement AnalysisAleeza FatimaNo ratings yet

- FIN 440 Group Task 1Document104 pagesFIN 440 Group Task 1দিপ্ত বসুNo ratings yet

- Institute of Management Development and Research (Imdr) : Pune Post Graduation Diploma in Management (PGDM)Document9 pagesInstitute of Management Development and Research (Imdr) : Pune Post Graduation Diploma in Management (PGDM)hitesh rathodNo ratings yet

- Act B - Horizontal AnalysisDocument5 pagesAct B - Horizontal AnalysisIsn't bitterness it's the truthNo ratings yet

- Interloop Limited Income Statement: Rupees in ThousandDocument13 pagesInterloop Limited Income Statement: Rupees in ThousandAsad AliNo ratings yet

- IMT CeresDocument5 pagesIMT CeresRithvik RoyNo ratings yet

- Rafhan Maize Products Company LTDDocument10 pagesRafhan Maize Products Company LTDALI SHER HaidriNo ratings yet

- Millat Tractors - Final (Sheraz)Document20 pagesMillat Tractors - Final (Sheraz)Adeel SajidNo ratings yet

- Acc Projects by Adnan SHKDocument23 pagesAcc Projects by Adnan SHKADNAN SHEIKHNo ratings yet

- Group 7:: Abhishek Goyal Dhanashree Baxy Ipshita Ghosh Puja Priya Shivam Pandey Vidhi KothariDocument26 pagesGroup 7:: Abhishek Goyal Dhanashree Baxy Ipshita Ghosh Puja Priya Shivam Pandey Vidhi KothariABHISHEK GOYALNo ratings yet

- FMOD PROJECT WeefervDocument13 pagesFMOD PROJECT WeefervOmer CrestianiNo ratings yet

- Ain 20201025074Document8 pagesAin 20201025074HAMMADHRNo ratings yet

- Consolicated PL AccountDocument1 pageConsolicated PL AccountDarshan KumarNo ratings yet

- (Pso) Pakistan State OilDocument4 pages(Pso) Pakistan State OilSalman AtherNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Week 08Document24 pagesWeek 08shani2010No ratings yet

- Procurement Plan(s)Document1 pageProcurement Plan(s)shani2010No ratings yet

- Week 10 11Document20 pagesWeek 10 11shani2010No ratings yet

- Week 14Document19 pagesWeek 14shani2010No ratings yet

- Statement: Annual BudgetDocument76 pagesStatement: Annual Budgetshani2010No ratings yet

- Week 12 13Document36 pagesWeek 12 13shani2010No ratings yet

- Week 15Document22 pagesWeek 15shani2010No ratings yet

- Syed TAHIR HUSSAIN MEHMOODI VS Agha Syed LIAQAT ALI, 2014 SCMR-SUPREME-COURT 637 (2014)Document4 pagesSyed TAHIR HUSSAIN MEHMOODI VS Agha Syed LIAQAT ALI, 2014 SCMR-SUPREME-COURT 637 (2014)shani2010No ratings yet

- Rana TANVEER KHAN VS NASEER-UD-DIN, 2015 SCMR-SUPREME-COURT 1401 (2014)Document4 pagesRana TANVEER KHAN VS NASEER-UD-DIN, 2015 SCMR-SUPREME-COURT 1401 (2014)shani2010No ratings yet

- GHULAM QADIR Alias QADIR BAKHSH VS Haji MUHAMMAD SULEMAN, 2002 CLC-LAHORE-HIGH-COURT-LAHORE 1111 (2001)Document4 pagesGHULAM QADIR Alias QADIR BAKHSH VS Haji MUHAMMAD SULEMAN, 2002 CLC-LAHORE-HIGH-COURT-LAHORE 1111 (2001)shani2010No ratings yet

- Abdul Aziz Khan VS Shah Jahan Begum, 1971 Pld-Supreme-Court 434 (1971)Document4 pagesAbdul Aziz Khan VS Shah Jahan Begum, 1971 Pld-Supreme-Court 434 (1971)shani2010No ratings yet

- LCS RulesDocument4 pagesLCS Rulesshani2010No ratings yet

- FPSC@FPSC - Gov.pk: Registered Post/ Email)Document8 pagesFPSC@FPSC - Gov.pk: Registered Post/ Email)shani2010No ratings yet

- HSBC Annual Report and Accounts 2020 (With Employee Share PlansDocument386 pagesHSBC Annual Report and Accounts 2020 (With Employee Share PlansSNo ratings yet

- Book Value Per Share PresentationDocument22 pagesBook Value Per Share PresentationharoonameerNo ratings yet

- Learning Plan IntrodocxDocument16 pagesLearning Plan IntrodocxSittie Ainna A. UnteNo ratings yet

- Issue of Share Only QuestionDocument6 pagesIssue of Share Only Questionmauryaaniket8668No ratings yet

- Chapter 1678Document41 pagesChapter 1678Govind Rathod0% (1)

- POE U S 116363 cheDocument76 pagesPOE U S 116363 cheMoges PillayNo ratings yet

- Thesis Budgeting and Performance PDFDocument189 pagesThesis Budgeting and Performance PDFHA CskNo ratings yet

- Mock Aqe 1Document15 pagesMock Aqe 1AshNor RandyNo ratings yet

- Quiz No 2 Fsa Oral Recits Quiz PDF FreeDocument13 pagesQuiz No 2 Fsa Oral Recits Quiz PDF FreeTshina Jill BranzuelaNo ratings yet

- 501-14-Kelvin Febriansyah Pratama-Latihan Ke-10aDocument4 pages501-14-Kelvin Febriansyah Pratama-Latihan Ke-10aKELVIN FEBRIANSYAH PRATAMANo ratings yet

- Accounting Ratio'sDocument26 pagesAccounting Ratio'sRajesh Jyothi100% (1)

- Construction Economics & Finance s16Document2 pagesConstruction Economics & Finance s16sgumble3007No ratings yet

- FR342.AL I Solution CMA May 2022 Examination 23 06 22Document6 pagesFR342.AL I Solution CMA May 2022 Examination 23 06 22Pavel DhakaNo ratings yet

- Ipsas 9 Revuenue Form Exchange TransactionsDocument14 pagesIpsas 9 Revuenue Form Exchange TransactionsNassib SongoroNo ratings yet

- RTP Dec 18 QNDocument21 pagesRTP Dec 18 QNbinu100% (1)

- Lou Simpson GEICO LettersDocument24 pagesLou Simpson GEICO LettersDaniel TanNo ratings yet

- Chapter 4Document65 pagesChapter 4임재영No ratings yet

- Akuntansi Menengah 2Document3 pagesAkuntansi Menengah 2CitraNo ratings yet

- Chapter 13 of Accounting CombiDocument27 pagesChapter 13 of Accounting CombiKheyzel YtacNo ratings yet

- Project Template Comparing Tootsie Roll & HersheyDocument16 pagesProject Template Comparing Tootsie Roll & HersheymcmoneysNo ratings yet

- A Report On: Analysis of Financial Statements OF Tata Consultancy Services & Maruti SuzukiDocument38 pagesA Report On: Analysis of Financial Statements OF Tata Consultancy Services & Maruti SuzukiSaurabhNo ratings yet

- Annual Report 2010 ZhulianDocument111 pagesAnnual Report 2010 ZhulianNurul Faezah Mat JalilNo ratings yet

- Advanced Financial Accounting and ReportingDocument15 pagesAdvanced Financial Accounting and ReportingAcain RolienNo ratings yet

- CH 4Document59 pagesCH 4ad_jebbNo ratings yet

- Multiple Choice QuestionsDocument12 pagesMultiple Choice QuestionsNguyen Thanh Thao (K16 HCM)No ratings yet

- Chapter 11 Audit of Insurance CompaniesDocument62 pagesChapter 11 Audit of Insurance CompaniesDiyanaBankovaNo ratings yet

- Acctg01 - Chapter 6Document5 pagesAcctg01 - Chapter 6Paul Ed Jeremy AlvinezNo ratings yet

- InvestmentsDocument13 pagesInvestmentsCorinne GohocNo ratings yet

- Sample PfrsDocument7 pagesSample PfrsClint AbenojaNo ratings yet