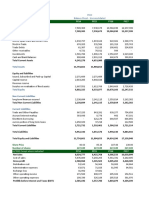

EREGL DCF Model

EREGL DCF Model

Download as xlsx, pdf, or txt

You might also like

- Eun 9e International Financial Management PPT CH01 AccessibleDocument29 pagesEun 9e International Financial Management PPT CH01 AccessibleDao Dang Khoa FUG CTNo ratings yet

- Insurance Law NotesDocument14 pagesInsurance Law NotesAnnet MutabarukaNo ratings yet

- Alk SidoDocument2 pagesAlk SidoRebertha HerwinNo ratings yet

- 02 06 BeginDocument6 pages02 06 BeginnehaNo ratings yet

- 02 04 EndDocument6 pages02 04 EndnehaNo ratings yet

- FIN 440 Group Task 1Document104 pagesFIN 440 Group Task 1দিপ্ত বসুNo ratings yet

- Ratio AnalysisDocument35 pagesRatio AnalysisMd. Sakib HossainNo ratings yet

- Fin 254 Group Project ExcelDocument12 pagesFin 254 Group Project Excelapi-422062723No ratings yet

- Answer To The Question No 1 (I) ACI Group of Company Balance Sheet (Vertical Analysis) For The Years Ended June 30, 2019Document4 pagesAnswer To The Question No 1 (I) ACI Group of Company Balance Sheet (Vertical Analysis) For The Years Ended June 30, 2019Estiyak JahanNo ratings yet

- Activity Week 3Document6 pagesActivity Week 3haseeb ShaikhNo ratings yet

- Finacial Position FINAL GLOBE TELECOMDocument4 pagesFinacial Position FINAL GLOBE TELECOMLenard TaberdoNo ratings yet

- Income Statement FINALDocument2 pagesIncome Statement FINALLenard TaberdoNo ratings yet

- Al Fajar WorkingDocument3 pagesAl Fajar WorkingsureniimbNo ratings yet

- PIOC Data For Corporate ValuationDocument6 pagesPIOC Data For Corporate ValuationMuhammad Ali SamarNo ratings yet

- Calculations of OGDCL by Safdar, Safi Ullah, Muhamad AminDocument39 pagesCalculations of OGDCL by Safdar, Safi Ullah, Muhamad AminSaeed Ahmed (Father Name:Jamal Ud Din)No ratings yet

- 2653384-Maruti_Suzuki_Financial_Model_-ProjectionsDocument21 pages2653384-Maruti_Suzuki_Financial_Model_-ProjectionsCall of duty mobileNo ratings yet

- Ghandhara NissanDocument7 pagesGhandhara NissanShamsuddin SoomroNo ratings yet

- 2,017 2,016 Total Revenue Cost of Sales Gross Profit ExpensesDocument4 pages2,017 2,016 Total Revenue Cost of Sales Gross Profit ExpensesHayotNo ratings yet

- Financial Statements Analysis: Arsalan FarooqueDocument31 pagesFinancial Statements Analysis: Arsalan FarooqueMuhib NoharioNo ratings yet

- M.Shahnam Ul Hassan ProjectDocument13 pagesM.Shahnam Ul Hassan ProjectM.ShahnamNo ratings yet

- Balance Sheet of WiproDocument3 pagesBalance Sheet of WiproRinni JainNo ratings yet

- Indus Dyeing & Manufacturing Co. LTD: Horizontal Analysis of Financial StatementsDocument12 pagesIndus Dyeing & Manufacturing Co. LTD: Horizontal Analysis of Financial StatementsSaad NaeemNo ratings yet

- Financial Statement AnalysisDocument5 pagesFinancial Statement AnalysisMohammad Abid MiahNo ratings yet

- Indus Dyeing & Manufacturing Co. LTD: Horizontal Analysis of Financial StatementsDocument12 pagesIndus Dyeing & Manufacturing Co. LTD: Horizontal Analysis of Financial StatementsSaad NaeemNo ratings yet

- Attock Refinery FM Assignment#3Document13 pagesAttock Refinery FM Assignment#3Vishal MalhiNo ratings yet

- MCB Financial AnalysisDocument30 pagesMCB Financial AnalysisMuhammad Nasir Khan100% (4)

- Final Banking ProjectDocument18 pagesFinal Banking Projectabdullah ashrafNo ratings yet

- Horizental Analysis On Income StatementDocument21 pagesHorizental Analysis On Income StatementMuhib NoharioNo ratings yet

- Kohinoor Chemical Company LTD.: Horizontal AnalysisDocument19 pagesKohinoor Chemical Company LTD.: Horizontal AnalysisShehreen ArnaNo ratings yet

- Restaurant BusinessDocument14 pagesRestaurant BusinessSAKIBNo ratings yet

- Key Operating and Financial Data 2017 For Website Final 20.3.2018Document2 pagesKey Operating and Financial Data 2017 For Website Final 20.3.2018MubeenNo ratings yet

- Dersnot 1372 1684245035Document6 pagesDersnot 1372 1684245035Murat SiyahkayaNo ratings yet

- Explanation 2015 2014: Akij Food and Beverage Statement of Financial Position (June31,2015)Document5 pagesExplanation 2015 2014: Akij Food and Beverage Statement of Financial Position (June31,2015)jisansalehin1No ratings yet

- M Saeed 20-26 ProjectDocument30 pagesM Saeed 20-26 ProjectMohammed Saeed 20-26No ratings yet

- Atlas Honda (2019 22)Document6 pagesAtlas Honda (2019 22)husnainbutt2025No ratings yet

- Financial Management Slides 3.3Document7 pagesFinancial Management Slides 3.3honathapyarNo ratings yet

- Income Statement For Astra Agro Lestari TBK (AALI) From Morningstar PDFDocument1 pageIncome Statement For Astra Agro Lestari TBK (AALI) From Morningstar PDFGvz HndraNo ratings yet

- Sir Sarwar AFSDocument41 pagesSir Sarwar AFSawaischeemaNo ratings yet

- Ratio Analysis TanyaDocument10 pagesRatio Analysis Tanyatanya chauhanNo ratings yet

- DU Pont AnalysisDocument9 pagesDU Pont Analysisshani2010No ratings yet

- Financial Analysis SofiDocument31 pagesFinancial Analysis SofiKayo AbebeNo ratings yet

- Non-Mark-up/Interest Income: Profit Before Taxation 22,198,843 23,249,286Document8 pagesNon-Mark-up/Interest Income: Profit Before Taxation 22,198,843 23,249,286shahzad khalidNo ratings yet

- Gildan Model BearDocument57 pagesGildan Model BearNaman PriyadarshiNo ratings yet

- Apple V SamsungDocument4 pagesApple V SamsungCarla Mae MartinezNo ratings yet

- FINM 7044 Group Assignment 终Document4 pagesFINM 7044 Group Assignment 终jimmmmNo ratings yet

- Beximco Pharmaceuticals LimitedDocument4 pagesBeximco Pharmaceuticals Limitedsamia0akter-228864No ratings yet

- Askari Bank Limited Financial Statement AnalysisDocument16 pagesAskari Bank Limited Financial Statement AnalysisAleeza FatimaNo ratings yet

- JSW Steel SummaryDocument2 pagesJSW Steel Summaryprasad271299No ratings yet

- CMA CIA 3 YateeDocument38 pagesCMA CIA 3 YateeYATEE TRIVEDI 21111660No ratings yet

- Financial Statement Analysis Zoom Session 3Document7 pagesFinancial Statement Analysis Zoom Session 3MANSOOR AHMEDNo ratings yet

- Consolicated PL AccountDocument1 pageConsolicated PL AccountDarshan KumarNo ratings yet

- VineetAg FADocument10 pagesVineetAg FAVineet AgarwalNo ratings yet

- FSA AssignmentDocument4 pagesFSA AssignmentDharmil OzaNo ratings yet

- Ali Asghar Report ..Document7 pagesAli Asghar Report ..Ali AzgarNo ratings yet

- Fiscal Year Ending December 31 2020 2019 2018 2017 2016Document22 pagesFiscal Year Ending December 31 2020 2019 2018 2017 2016Wasif HossainNo ratings yet

- FS SNS Q2 2023 (Inhouse) Hasan Queries AspireDocument64 pagesFS SNS Q2 2023 (Inhouse) Hasan Queries AspireHasan Akmal AlatasNo ratings yet

- FIN440 Phase 2 ExcelDocument27 pagesFIN440 Phase 2 ExcelRiddo BadhonNo ratings yet

- Persistent KPIT - Merger ModelDocument86 pagesPersistent KPIT - Merger ModelAnurag JainNo ratings yet

- SPL - 3rd QTR BL-PNL-DEC 2018-2019 (Full)Document17 pagesSPL - 3rd QTR BL-PNL-DEC 2018-2019 (Full)MedulNo ratings yet

- Eswatini 2020 Formulation External BudgetFramework NatGov COMESASADC EnglishDocument240 pagesEswatini 2020 Formulation External BudgetFramework NatGov COMESASADC EnglishPanda CoinNo ratings yet

- Khulna Power Company Limited: Balnace Sheet StatementDocument9 pagesKhulna Power Company Limited: Balnace Sheet StatementTahmid ShovonNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Simple InterestDocument9 pagesSimple Interestclear conceptsNo ratings yet

- Role of IT Mindfulness On Continuance Intention of Mobile Payment SystemDocument12 pagesRole of IT Mindfulness On Continuance Intention of Mobile Payment SystemPradeepNo ratings yet

- CFA Level 1 2021 Study Planner - by Mohit DamaniDocument19 pagesCFA Level 1 2021 Study Planner - by Mohit DamaniАндрей Б-нNo ratings yet

- 2023C3A278E767E2Document1 page2023C3A278E767E2Ashiq HussainNo ratings yet

- Sustainability Reportingand Financial Performanceof Malaysian Public Listed CompaniesDocument17 pagesSustainability Reportingand Financial Performanceof Malaysian Public Listed CompaniesAna FienaNo ratings yet

- Lecture 3Document20 pagesLecture 3Pubg KrNo ratings yet

- InvoiceDocument1 pageInvoiceOmkar JadhavNo ratings yet

- LTL PanelDocument5 pagesLTL PanelBansi LalNo ratings yet

- Chairing A Meeting British English TeacherDocument7 pagesChairing A Meeting British English TeacherJimena AbdoNo ratings yet

- Mid Term Supply Chain Inventory ManagementDocument6 pagesMid Term Supply Chain Inventory ManagementOilandGas IndependentProjectNo ratings yet

- Requirements of Buyer For BidaDocument1 pageRequirements of Buyer For BidaKeith CasinabeNo ratings yet

- Unit CostingDocument3 pagesUnit CostingAnkit YadavNo ratings yet

- 2 Annuities1Document19 pages2 Annuities1Fredrick BarasaNo ratings yet

- Human Resources Department of Kumari Bank Litimed: BY Durga Dumre EXAM ROLL NO. 939/15 T.U. Reg No. 7-2-0032-0008-2015Document45 pagesHuman Resources Department of Kumari Bank Litimed: BY Durga Dumre EXAM ROLL NO. 939/15 T.U. Reg No. 7-2-0032-0008-2015Sujan BajracharyaNo ratings yet

- Partnership Formation Answer KeyDocument8 pagesPartnership Formation Answer KeyNichole Joy XielSera TanNo ratings yet

- Fdocuments - in PNB Training ReportdocxDocument87 pagesFdocuments - in PNB Training ReportdocxAviral Pratap Singh KhareNo ratings yet

- Ee Unit - !Document13 pagesEe Unit - !Senthil Kumar GanesanNo ratings yet

- President Donald J. Trump's Accomplishment List Archive. - MAGAPILL PDFDocument33 pagesPresident Donald J. Trump's Accomplishment List Archive. - MAGAPILL PDFpeter100% (1)

- Assig 2Document4 pagesAssig 2Sýëd FűrrűķhNo ratings yet

- ASM2 Hoang Nam 5076Document39 pagesASM2 Hoang Nam 5076quangpmgbh210461No ratings yet

- Sample Goals ListDocument29 pagesSample Goals ListSurajit MitraNo ratings yet

- FA AnswersDocument12 pagesFA AnswersErica XaoNo ratings yet

- Counterparty Valuation Adjustments by BloombergDocument13 pagesCounterparty Valuation Adjustments by BloombergMo MokNo ratings yet

- SCM ComplexityDocument39 pagesSCM ComplexityhandryanNo ratings yet

- B2+ Test Series (28) : Name: - Score: - /100Document4 pagesB2+ Test Series (28) : Name: - Score: - /100Ngân Nguyễn Bùi HoaNo ratings yet

- Mundell Fleming ModelDocument22 pagesMundell Fleming ModelNishant YadavNo ratings yet

- Brenda Rianita Hapsari - 12030119130222 - Tugas Opsi Dan FutureDocument4 pagesBrenda Rianita Hapsari - 12030119130222 - Tugas Opsi Dan FutureBrenda HapsariNo ratings yet

- Ujjwal JainDocument2 pagesUjjwal Jainhjgjh uihkikuhjNo ratings yet