Q3FY20

Q3FY20

Download as pdf or txt

You might also like

- Case Analysis BakeryDocument12 pagesCase Analysis BakeryUnice Jacob Villanueva100% (2)

- Unilever Training & DevelopmentDocument23 pagesUnilever Training & DevelopmentVivd Looks78% (9)

- Q3 & 9 MONTHS FYâ ™17 TRANSCRIPT ON EARNINGâ ™S CONFERENCE CALLDocument14 pagesQ3 & 9 MONTHS FYâ ™17 TRANSCRIPT ON EARNINGâ ™S CONFERENCE CALLShyam SunderNo ratings yet

- Motilal Oswal Financial Services: Concall Summary & Earnings ReleaseDocument11 pagesMotilal Oswal Financial Services: Concall Summary & Earnings Releasefoodieexpress913No ratings yet

- Q4FY23 Earnings Call TranscriptDocument17 pagesQ4FY23 Earnings Call TranscriptmunotarhamNo ratings yet

- Aarti IndustriesDocument33 pagesAarti IndustriesVijay CNo ratings yet

- "Alkem Laboratories Limited Q3 FY2020 Earnings Conference Call" February 07, 2020Document20 pages"Alkem Laboratories Limited Q3 FY2020 Earnings Conference Call" February 07, 2020GurjeevNo ratings yet

- Results Press Release For September 30, 2016 (Result)Document4 pagesResults Press Release For September 30, 2016 (Result)Shyam SunderNo ratings yet

- LTFH Q2 FY20 Earnings Call TranscriptDocument15 pagesLTFH Q2 FY20 Earnings Call Transcriptkishore13No ratings yet

- Transcript MM q3f24 Analyst Meet 14 Feb 2024 Final - 0Document22 pagesTranscript MM q3f24 Analyst Meet 14 Feb 2024 Final - 0surajagrawal1234No ratings yet

- Stock Update PTC India: IndexDocument6 pagesStock Update PTC India: IndexRam NarayananNo ratings yet

- Stock Advisory For Today - But Stock of Coal India LTD and Cipla LimitedDocument24 pagesStock Advisory For Today - But Stock of Coal India LTD and Cipla LimitedNarnolia Securities LimitedNo ratings yet

- Tata Chemicals Limited Q4 FY16 Earnings Conference CallDocument13 pagesTata Chemicals Limited Q4 FY16 Earnings Conference CallGary BurnNo ratings yet

- PhillipCap BalkrishnaIndus 15nov 2022Document18 pagesPhillipCap BalkrishnaIndus 15nov 2022Rajas RijuNo ratings yet

- Page Earning Call Feb 2020 PDFDocument18 pagesPage Earning Call Feb 2020 PDFRakesh JhunjhunwallaNo ratings yet

- Cosmo Films Q4FY20 - Conference - Call - TranscriptDocument14 pagesCosmo Films Q4FY20 - Conference - Call - TranscriptSam vermNo ratings yet

- Aarti Industries Concall Nov 2019Document17 pagesAarti Industries Concall Nov 2019Ved-And-TechsNo ratings yet

- RKL Q1 FY2021 Concall TranscriptDocument16 pagesRKL Q1 FY2021 Concall TranscriptUmangNo ratings yet

- PidiliteDocument45 pagesPidiliteVijay DosapatiNo ratings yet

- Aarti IndustriesDocument15 pagesAarti IndustriesHimanshu GoyalNo ratings yet

- M&M Concalls-188-354Document167 pagesM&M Concalls-188-354ursdaddyNo ratings yet

- Natco Pharma Conference CallDocument22 pagesNatco Pharma Conference CallVed-And-TechsNo ratings yet

- Kewal Kiran Clothing LTDDocument3 pagesKewal Kiran Clothing LTDdreaminvestment0819No ratings yet

- Transcript-M-and-M-Q2F25-Analyst-Meet-7th - Nov - 2024 FinalDocument19 pagesTranscript-M-and-M-Q2F25-Analyst-Meet-7th - Nov - 2024 Finalrania.nayeem2006No ratings yet

- Samuel Savepalli Sivanandam Section A FAR Individual Assignment-1Document7 pagesSamuel Savepalli Sivanandam Section A FAR Individual Assignment-1Samuel SarvepalliNo ratings yet

- FCCCP_DAFDSF_A23Q4234_DAFAFDASAFDocument29 pagesFCCCP_DAFDSF_A23Q4234_DAFAFDASAFsivakumar1914No ratings yet

- Conference Call TranscriptDocument14 pagesConference Call TranscriptBVMF_RINo ratings yet

- Quick Note: Sintex IndustriesDocument6 pagesQuick Note: Sintex Industriesred cornerNo ratings yet

- UPL CMD 2024 TranscriptionDocument30 pagesUPL CMD 2024 TranscriptionNishu GuptaNo ratings yet

- Page Industries LTDDocument3 pagesPage Industries LTDdreaminvestment0819No ratings yet

- PI Industries Limited Q4 & FY2019 Earnings Conference Call TranscriptDocument14 pagesPI Industries Limited Q4 & FY2019 Earnings Conference Call TranscriptTerminatorNo ratings yet

- Q 4 Fy 11 TranscriptDocument18 pagesQ 4 Fy 11 TranscriptequityanalystinvestorNo ratings yet

- Best Performing Stock Advice For Today - Neutral Rating On GAIL Stock With A Target Price of Rs.346Document22 pagesBest Performing Stock Advice For Today - Neutral Rating On GAIL Stock With A Target Price of Rs.346Narnolia Securities LimitedNo ratings yet

- Digitally Signed by Gangani Mayur Popatbhai Date: 2024.10.18 14:24:03 +05'30'Document17 pagesDigitally Signed by Gangani Mayur Popatbhai Date: 2024.10.18 14:24:03 +05'30'manish waghNo ratings yet

- Piramal Enterprises Limited Investor Presentation Nov 2016 20161108025005Document74 pagesPiramal Enterprises Limited Investor Presentation Nov 2016 20161108025005ratan203No ratings yet

- J. P Morgan - Pidilite IndustriesDocument36 pagesJ. P Morgan - Pidilite Industriesparry0843No ratings yet

- FY20 Q1 Earnings Call TranscriptDocument24 pagesFY20 Q1 Earnings Call Transcriptrishab agarwalNo ratings yet

- pb fintech concall qoqDocument22 pagespb fintech concall qoqgurdeepsaannaaNo ratings yet

- Transcript of Conference Call (Company Update)Document15 pagesTranscript of Conference Call (Company Update)Shyam SunderNo ratings yet

- Aarti Ind: SalesDocument10 pagesAarti Ind: Salespeaceful investNo ratings yet

- Kalpataru Power Transmission LTDDocument9 pagesKalpataru Power Transmission LTDakshatnia4No ratings yet

- NIIT Technologies Limited: Investors Conference Call For Quarterly Results Ended Jun 2006 July 19, 2006Document22 pagesNIIT Technologies Limited: Investors Conference Call For Quarterly Results Ended Jun 2006 July 19, 2006Jaya RamchandaniNo ratings yet

- Q1FY21Document18 pagesQ1FY21Err DatabaseNo ratings yet

- Sunil Kumar JainDocument16 pagesSunil Kumar Jainsahil.goelNo ratings yet

- Shahzabeen Irsa Latif Tayyab MazharDocument29 pagesShahzabeen Irsa Latif Tayyab MazharErsa LatifNo ratings yet

- Business Plan BP QBDocument10 pagesBusiness Plan BP QBFinto AlexanderNo ratings yet

- RKL Q4 FY2020 Concall TranscriptDocument18 pagesRKL Q4 FY2020 Concall TranscriptUmangNo ratings yet

- Mahindra & Mahindra Group: Consolidated Financial PositionDocument11 pagesMahindra & Mahindra Group: Consolidated Financial PositionSrutiNo ratings yet

- SGA GabrielIndiaLtd 09feb 2024Document16 pagesSGA GabrielIndiaLtd 09feb 2024ajkarwaNo ratings yet

- Eisai Co LTD (ESALF) Q3 2023 Earnings Call Transcript - Seeking AlphaDocument27 pagesEisai Co LTD (ESALF) Q3 2023 Earnings Call Transcript - Seeking Alphasaksham.gosainNo ratings yet

- BBMF2023 Tutorial Group 3 Power Root BerhadDocument35 pagesBBMF2023 Tutorial Group 3 Power Root BerhadKar EngNo ratings yet

- Pavan IapmDocument8 pagesPavan IapmPavan Kumar YNo ratings yet

- RPC Annual Report 2009-2010Document124 pagesRPC Annual Report 2009-2010Prabhath KatawalaNo ratings yet

- Transcript Regarding Investors' Conference Call (Company Update)Document25 pagesTranscript Regarding Investors' Conference Call (Company Update)Shyam SunderNo ratings yet

- FY23 Q2 Conference Call TranscriptDocument14 pagesFY23 Q2 Conference Call TranscriptIndraneel MahantiNo ratings yet

- Balaji WafersDocument14 pagesBalaji WafersUdit PandyaNo ratings yet

- Digitally Signed by Dayeeta Shrinivas Gokhale Date: 2024.02.16 14:34:55 +05'30'Document18 pagesDigitally Signed by Dayeeta Shrinivas Gokhale Date: 2024.02.16 14:34:55 +05'30'rahulraotigerNo ratings yet

- Piramal Enterprises Limited, Q3 2020 Earnings Call, Feb 04, 2020Document16 pagesPiramal Enterprises Limited, Q3 2020 Earnings Call, Feb 04, 2020Savil GuptaNo ratings yet

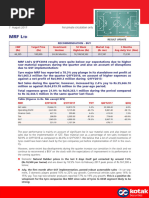

- Research Report for MRF ShareDocument4 pagesResearch Report for MRF ShareVanisha MaddheshiyaNo ratings yet

- Sunil Kumar JainDocument15 pagesSunil Kumar Jainsahil.goelNo ratings yet

- Tracxn CC Q2 FY 2022-2023Document17 pagesTracxn CC Q2 FY 2022-2023RAJESH NIRANIYANo ratings yet

- Project For SharekhanDocument52 pagesProject For SharekhanSahil Aggarwal100% (2)

- Business Plan Erica AnneDocument11 pagesBusiness Plan Erica Annedancolico9No ratings yet

- Business Plan PolicyDocument23 pagesBusiness Plan PolicynaNo ratings yet

- Lithium Cell and Battery Test Summary: New Rule and Long TransitionDocument2 pagesLithium Cell and Battery Test Summary: New Rule and Long TransitionEhab MohamedNo ratings yet

- F.A.I.R Summer Internship ProgrammeDocument3 pagesF.A.I.R Summer Internship ProgrammeRuchita PaulNo ratings yet

- Purchase Order: Supplier ConfirmDocument1 pagePurchase Order: Supplier ConfirmMochamad Daffa RaihanNo ratings yet

- Financial Analysis For Sapphire Fibres LimitedDocument6 pagesFinancial Analysis For Sapphire Fibres LimitedRashmeen NaeemNo ratings yet

- Linear Programming FormulationDocument27 pagesLinear Programming FormulationDrama ArtNo ratings yet

- Sales Kit & Media Promotions Townsquare CilandakDocument27 pagesSales Kit & Media Promotions Townsquare CilandaksigitentranceNo ratings yet

- L9Media and InformationDocument8 pagesL9Media and Informationxhiaklee91No ratings yet

- Annual Report 2023 FinalDocument246 pagesAnnual Report 2023 FinalHasin IsrakNo ratings yet

- Week One Worksheet Assignment-6Document3 pagesWeek One Worksheet Assignment-6Greg KaschuskiNo ratings yet

- Kasneb Exam Entry FormDocument2 pagesKasneb Exam Entry FormOkong'o Ogutu78% (9)

- Module 1 Practice QuestionsDocument7 pagesModule 1 Practice QuestionsEllah MaeNo ratings yet

- Ihrm Unit 1,2,3 NotesDocument109 pagesIhrm Unit 1,2,3 NotesHemantNo ratings yet

- The Law Society of Singapores Conditions of Sale 2020Document14 pagesThe Law Society of Singapores Conditions of Sale 2020Dave YangNo ratings yet

- Paessler.R2019 02 0232554 01Document2 pagesPaessler.R2019 02 0232554 01Ziad El SamadNo ratings yet

- Usman New CVDocument1 pageUsman New CVVivek LuckyNo ratings yet

- Architectural Consultancy Proposal - Full TimeDocument3 pagesArchitectural Consultancy Proposal - Full TimeAngel NuevoNo ratings yet

- OD331532051782845100Document1 pageOD331532051782845100vipin.sharma0517No ratings yet

- BUS 800 FinalDocument4 pagesBUS 800 Finaladnan.pervezNo ratings yet

- 08 MerchandiseManagementDocument18 pages08 MerchandiseManagementCrystal Maria DsouzaNo ratings yet

- Volkswagen Beetle.: Market SegmentationDocument5 pagesVolkswagen Beetle.: Market SegmentationOmar JuliusNo ratings yet

- Financial Analysis of Amalgamation Between TCS CMC A Project Report PDFDocument16 pagesFinancial Analysis of Amalgamation Between TCS CMC A Project Report PDFRajeshNo ratings yet

- A192 QuestionDocument11 pagesA192 QuestionZati ZnlNo ratings yet

- Hathway ReportDocument37 pagesHathway ReportSHIVANSH BANSALNo ratings yet

- FashionDocument2 pagesFashionAnsh SachdevaNo ratings yet

- Retail Environment 2Document27 pagesRetail Environment 2Retail Fashion MerchandisingNo ratings yet