Ecotrix CA

Ecotrix CA

Download as pdf or txt

You might also like

- 7.Hum-A Study of Economics Implications of Foreign Direct Investment in IndiaDocument10 pages7.Hum-A Study of Economics Implications of Foreign Direct Investment in IndiaImpact JournalsNo ratings yet

- ECON3110 Group Project - FDIDocument22 pagesECON3110 Group Project - FDIMohamed Ahmed aliNo ratings yet

- Stats Research PaperDocument14 pagesStats Research PaperRoshni SinghNo ratings yet

- Empirical AnalysisDocument10 pagesEmpirical Analysisrobin boseNo ratings yet

- Abstract:: The Impact of Exchange Rate Fluctuations On Foreign Direct Investment in NigeriaDocument7 pagesAbstract:: The Impact of Exchange Rate Fluctuations On Foreign Direct Investment in NigeriaAshrafulNo ratings yet

- Journal of International Trade Law and Policy: Emerald Article: Determinants of Foreign Direct Investment in IndiaDocument20 pagesJournal of International Trade Law and Policy: Emerald Article: Determinants of Foreign Direct Investment in IndiaRahmii Khairatul HisannNo ratings yet

- Relationship of Foreign Direct Investment (FDI) Inflows and Exchange Rate in The Context of India: A Two Way Analysis Approach Piyali Roy Chowdhury, A AnuradhaDocument10 pagesRelationship of Foreign Direct Investment (FDI) Inflows and Exchange Rate in The Context of India: A Two Way Analysis Approach Piyali Roy Chowdhury, A AnuradhaRamya PichiNo ratings yet

- A Study On The Impact of Fdi Inflows On Exports and Growth of An Economy: Evidence From The Context of Indian EconomyDocument8 pagesA Study On The Impact of Fdi Inflows On Exports and Growth of An Economy: Evidence From The Context of Indian Economygs randhawaNo ratings yet

- Research Report: Trade Openness vs. Growth in PakistanDocument9 pagesResearch Report: Trade Openness vs. Growth in PakistanSheraz NasirNo ratings yet

- The Effect of Inward Foreign Direct Investment On Economic Growth - The Case of Chinese Provinces.Document22 pagesThe Effect of Inward Foreign Direct Investment On Economic Growth - The Case of Chinese Provinces.Alisson NBNo ratings yet

- Bop ArtDocument4 pagesBop ArtJumli BomjenNo ratings yet

- 1 s2.0 S2212567115006474 MainDocument10 pages1 s2.0 S2212567115006474 Mainruqaiyya sabeballyNo ratings yet

- R. PapersDocument3 pagesR. PapersMuhammad Mughera RehmanNo ratings yet

- Chapter 3-Trade LiberalizationDocument10 pagesChapter 3-Trade LiberalizationnatashakeikoNo ratings yet

- Fdi in India: Determinants And: ITS Comparison With ChinaDocument5 pagesFdi in India: Determinants And: ITS Comparison With ChinaManoj Kumar SinghNo ratings yet

- Impact of Fdi Inflow On Service Sector in India: An Empirical AnalysisDocument5 pagesImpact of Fdi Inflow On Service Sector in India: An Empirical AnalysisMitali PitkarNo ratings yet

- Research ProposalDocument5 pagesResearch ProposalMansi MateNo ratings yet

- Asgmnt Ecnomtrc Half SiapDocument6 pagesAsgmnt Ecnomtrc Half SiapkirupaliniNo ratings yet

- ssrn-4012853Document41 pagesssrn-4012853quynhhuong03forworkNo ratings yet

- Haris BoiDocument24 pagesHaris BoiMuhammad HarisNo ratings yet

- the-impact-of-foreign-direct-investment-on-economic-growth_-empirical-evidence-from-algeria-(1990-2021)Document13 pagesthe-impact-of-foreign-direct-investment-on-economic-growth_-empirical-evidence-from-algeria-(1990-2021)ferieladim4No ratings yet

- Presentation For M. Phil. ProposalDocument22 pagesPresentation For M. Phil. ProposalRituraj BhatNo ratings yet

- The Impact of Exports and Imports On Exchange Rates in India Revised Manisha Maam PaperDocument10 pagesThe Impact of Exports and Imports On Exchange Rates in India Revised Manisha Maam PaperManvi AgrawalNo ratings yet

- Exchange Rate and Economic Growth in IndiaDocument10 pagesExchange Rate and Economic Growth in Indiajanhavibirhade05No ratings yet

- GDP Growth Determinants (CW Econometrics)Document9 pagesGDP Growth Determinants (CW Econometrics)Murodullo BazarovNo ratings yet

- Impact of Fdi On Economic Growth in Pakistan ThesisDocument8 pagesImpact of Fdi On Economic Growth in Pakistan ThesisWriteMyPaperReviewsOverlandPark100% (2)

- 1.the Determinants of Foreign Direct InvesDocument13 pages1.the Determinants of Foreign Direct InvesAzan RasheedNo ratings yet

- Impact of Exchange Rate Movements On Ind PDFDocument14 pagesImpact of Exchange Rate Movements On Ind PDFNishatNo ratings yet

- Management Report PresentationDocument6 pagesManagement Report PresentationShiban shaikhNo ratings yet

- Analysis of India'S Current ACCOUNT (1991-2013) : Project ReportDocument61 pagesAnalysis of India'S Current ACCOUNT (1991-2013) : Project Reportjas_wadNo ratings yet

- 1.time Series Analysis of Inward Foreign Direct Investment Function in MalaysiaDocument7 pages1.time Series Analysis of Inward Foreign Direct Investment Function in MalaysiaAzan RasheedNo ratings yet

- Comparison of Emerging Economy Through Macro Economy IndicatorsDocument29 pagesComparison of Emerging Economy Through Macro Economy Indicatorssarangk87No ratings yet

- Determinants of Foreign Direct Investment inDocument20 pagesDeterminants of Foreign Direct Investment inMASHIURNo ratings yet

- MBA Thesis by Mohammad Hasan FINAL VERSIONDocument52 pagesMBA Thesis by Mohammad Hasan FINAL VERSIONPalash BharadwajNo ratings yet

- Intro-Lit Review DraftDocument9 pagesIntro-Lit Review Draftapi-3706508No ratings yet

- Economic Effects of Inward Foreign Direct Investment in Vietnamese Provinces.Document22 pagesEconomic Effects of Inward Foreign Direct Investment in Vietnamese Provinces.Alisson NBNo ratings yet

- FDI's Impact On Indian EconomyDocument3 pagesFDI's Impact On Indian Economypwd001No ratings yet

- 0 - THE Impact of FDI and ODA On Economic Growth of French SSADocument9 pages0 - THE Impact of FDI and ODA On Economic Growth of French SSAHeldio ArmandoNo ratings yet

- Journals InformationDocument6 pagesJournals InformationabdulsaqibNo ratings yet

- Scope of StudyDocument9 pagesScope of StudySukanya DeviNo ratings yet

- FDIand International TradeDocument6 pagesFDIand International Tradesaadaltamash920No ratings yet

- Synopsis FDIDocument7 pagesSynopsis FDIdroniteNo ratings yet

- FINALPublishedpaper IJREAMV04 I0642047Document7 pagesFINALPublishedpaper IJREAMV04 I0642047shubham thkNo ratings yet

- An, Yeh (2020) Growth Effect of Foreign Direct Investment and Financial Development - New Insightes - 18 Countries Vietnam - Emphirical StudyDocument19 pagesAn, Yeh (2020) Growth Effect of Foreign Direct Investment and Financial Development - New Insightes - 18 Countries Vietnam - Emphirical StudyNajaha GasimNo ratings yet

- Ifm - Term PaperDocument19 pagesIfm - Term PaperpriyankaNo ratings yet

- Onthe Role Remittanceand FDIin Economic Developmentof NepalDocument11 pagesOnthe Role Remittanceand FDIin Economic Developmentof Nepalsiddhivinayak qcNo ratings yet

- Relationship Between FDI and GDPDocument25 pagesRelationship Between FDI and GDPruchikadamani100% (3)

- Chapter 1 IntroductionDocument8 pagesChapter 1 IntroductionLenard PamisaNo ratings yet

- Hansen 2006Document21 pagesHansen 2006Gerson JangaNo ratings yet

- Ashoka DP 25 Determinants of Global Value Chain ParticipationDocument27 pagesAshoka DP 25 Determinants of Global Value Chain ParticipationBiswajit BanerjeeNo ratings yet

- Determinants of Trade in AsiaDocument13 pagesDeterminants of Trade in AsiaslapdashrantsNo ratings yet

- Impact of FDI On Economic Growth of SAARC NationDocument11 pagesImpact of FDI On Economic Growth of SAARC Nationaadolf2004No ratings yet

- Does FDI Have Differential Impacts On Exports? Evidence From Developing CountriesDocument16 pagesDoes FDI Have Differential Impacts On Exports? Evidence From Developing CountriesJimena BENITO CORDOVANo ratings yet

- Foreign Direct Investment and Gross Domestic Product: An Application On ECO Region (1995-2011)Document10 pagesForeign Direct Investment and Gross Domestic Product: An Application On ECO Region (1995-2011)Adnan KamalNo ratings yet

- Trade and DevDocument13 pagesTrade and Devzahid aliNo ratings yet

- Dissertation On Fdi in IndiaDocument4 pagesDissertation On Fdi in IndiaWriteMyPaperOneDayCanada100% (2)

- ARDLDocument13 pagesARDLSayed Farrukh AhmedNo ratings yet

- AssignmentDocument19 pagesAssignmentPratiksha TiwariNo ratings yet

- That SoundsDocument8 pagesThat Soundsblairnasasira22No ratings yet

- ADB International Investment Agreement Tool Kit: A Comparative AnalysisFrom EverandADB International Investment Agreement Tool Kit: A Comparative AnalysisNo ratings yet

- Transit Chart ReportDocument6 pagesTransit Chart ReportAnita KadaverguNo ratings yet

- An Analysis of Figurative Language in A Thousand Years Song Lyrics by Cristina PerriDocument7 pagesAn Analysis of Figurative Language in A Thousand Years Song Lyrics by Cristina PerriHizkia Sebastian DannariNo ratings yet

- Intershala Autocad Training ReportDocument49 pagesIntershala Autocad Training Reportvishalssawant66No ratings yet

- Effective Communication in The Digital AgeDocument20 pagesEffective Communication in The Digital Agefictionlight30100% (1)

- Get The Science of Animal Agriculture 5th Edition Ray V Herren PDF ebook with Full Chapters NowDocument47 pagesGet The Science of Animal Agriculture 5th Edition Ray V Herren PDF ebook with Full Chapters Nowmoaidawht100% (3)

- 1814-Article Text-8044-1-10-20240122Document9 pages1814-Article Text-8044-1-10-20240122syafitriNo ratings yet

- First 2024-2025 ExamDocument13 pagesFirst 2024-2025 ExamRamil VergaraNo ratings yet

- ECN 2215 - Last - Topic - New - Macroeconomics PDFDocument26 pagesECN 2215 - Last - Topic - New - Macroeconomics PDFKalenga AlexNo ratings yet

- Abb Acs800-U11 ManualDocument114 pagesAbb Acs800-U11 ManualHenriViscarra100% (1)

- Scoring Integrative PaperDocument3 pagesScoring Integrative PaperCoco ManuelNo ratings yet

- Measures of Central Tendency (Mean, Median, Mode)Document6 pagesMeasures of Central Tendency (Mean, Median, Mode)RhoseNo ratings yet

- E-Banking in MoroccoDocument14 pagesE-Banking in MoroccopseNo ratings yet

- Prof ED 4 Creating Inclusive Culture Producing Inclusive PoliciesDocument27 pagesProf ED 4 Creating Inclusive Culture Producing Inclusive PoliciesMarvin CayagNo ratings yet

- Fans For Metro Tunnel DesignDocument34 pagesFans For Metro Tunnel Designkailasamvv100% (1)

- The Prehistory of The Tehuacan Valley VoDocument294 pagesThe Prehistory of The Tehuacan Valley VopepeNo ratings yet

- Tutorial Letter 101/0/2024: Geography of People - Resource Interaction in The Global SouthDocument15 pagesTutorial Letter 101/0/2024: Geography of People - Resource Interaction in The Global SouthLandiwe LangaNo ratings yet

- SIPDocument13 pagesSIPJanella Estrada100% (1)

- Class 4 - Weibull Distribution Function and Its ApplicationDocument57 pagesClass 4 - Weibull Distribution Function and Its ApplicationRizky LuthfieNo ratings yet

- Philip Crosby TQMDocument29 pagesPhilip Crosby TQMphdmaker100% (1)

- MGT 2070 - Chapter 3 - Practice QuestionsDocument81 pagesMGT 2070 - Chapter 3 - Practice QuestionsAasif MOCKADDAMNo ratings yet

- Ac Electrical Circuit LabDocument71 pagesAc Electrical Circuit LabtahiaNo ratings yet

- I See Sam Set 1 Book 1Document22 pagesI See Sam Set 1 Book 1NicoleNo ratings yet

- Body Language Gestures and SymbolsDocument2 pagesBody Language Gestures and SymbolsMsddak OmarNo ratings yet

- Depth PerceptionDocument7 pagesDepth PerceptionRaazia HaseebNo ratings yet

- Major ProjectDocument19 pagesMajor ProjectMohini BhartiNo ratings yet

- Contact Lens 2 Study GuideDocument5 pagesContact Lens 2 Study GuideGenre PesselNo ratings yet

- Annual Report JP-VERMADocument2 pagesAnnual Report JP-VERMAJay Prakash Narayan VermaNo ratings yet

- Report WritingDocument4 pagesReport Writingaadityanjha7No ratings yet

- Unicorn1 - Unicorns - Soonicorns in IndiaDocument4 pagesUnicorn1 - Unicorns - Soonicorns in IndiaSushmithaNo ratings yet

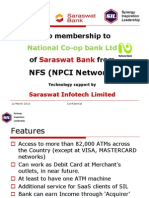

- NFS Sub Member BankDocument15 pagesNFS Sub Member BankAbhijit SamantNo ratings yet