Personal Loan Agreement

Personal Loan Agreement

Download as pdf or txt

You might also like

- Sudheer Loan Letter PDFDocument7 pagesSudheer Loan Letter PDFmr copy xeroxNo ratings yet

- Sanction 4Document4 pagesSanction 4ParinithNo ratings yet

- Sanctionletter 10045975 29-8-2023 113638Document3 pagesSanctionletter 10045975 29-8-2023 113638greenrootfinancialservicesNo ratings yet

- Most Important Terms and ConditionsDocument3 pagesMost Important Terms and ConditionsSaurav SamadhiyaNo ratings yet

- docSanctionLetterForm BL240205040100109Document7 pagesdocSanctionLetterForm BL240205040100109chawllarohitNo ratings yet

- Mr. Sathiyamoorthi Vijayan (Letter)Document3 pagesMr. Sathiyamoorthi Vijayan (Letter)riteshrathore2626No ratings yet

- Electric BillDocument2 pagesElectric BillJagannath PanigrahiNo ratings yet

- Sanction Letter Report CM'Document4 pagesSanction Letter Report CM'mukeshrs5614No ratings yet

- Sanction Letter Report CM'Document4 pagesSanction Letter Report CM'mukeshrs5614No ratings yet

- Sanction Letter Report Imrankhan Coimbatore BranchDocument4 pagesSanction Letter Report Imrankhan Coimbatore Branchranjanir1703No ratings yet

- Personal Loan Most Important Terms and Conditions 060623Document2 pagesPersonal Loan Most Important Terms and Conditions 060623saigurudevaliveNo ratings yet

- LAP Sanction Letter FixedDocument3 pagesLAP Sanction Letter Fixedpydimukkala SunilNo ratings yet

- Terms and ConditionDocument1 pageTerms and ConditionMuthu KumarNo ratings yet

- Loan Sanction Letter DC44F8TDocument10 pagesLoan Sanction Letter DC44F8Tspd882617No ratings yet

- Loan Sanction-Letter181240016761170869Document3 pagesLoan Sanction-Letter181240016761170869Sanjay MohapatraNo ratings yet

- Terms and Conditions Personal Loan 1684313861330Document2 pagesTerms and Conditions Personal Loan 1684313861330bleo02490No ratings yet

- RHB Product TC Personal FinancingDocument17 pagesRHB Product TC Personal FinancingDon LotNo ratings yet

- Terms and Conditions1724302044185Document9 pagesTerms and Conditions1724302044185sumitmkt2002No ratings yet

- Loan Sanction Letter E29049TDocument4 pagesLoan Sanction Letter E29049TketemineNo ratings yet

- UGRO SM Sanction LetterDocument4 pagesUGRO SM Sanction Letterjeeva27112003No ratings yet

- Sanction LetterDocument2 pagesSanction Letter313 65 Cheithanya Kumar MNo ratings yet

- LAP Sanction Letter Floating IndividualDocument3 pagesLAP Sanction Letter Floating Individualmishrashashwat199No ratings yet

- Terms and Conditions1709557590073Document6 pagesTerms and Conditions1709557590073nalanda612No ratings yet

- Charge Slip - 1723043986645Document3 pagesCharge Slip - 1723043986645nsjio6946No ratings yet

- CS421562169566 KFSDocument4 pagesCS421562169566 KFSShubhamNo ratings yet

- Key Facts Statement PDFDocument6 pagesKey Facts Statement PDFankulkumar54321ewqNo ratings yet

- keyFactStatement PDFDocument8 pageskeyFactStatement PDFINAM JUNG GUJJARNo ratings yet

- Most Important Terms and Conditions (Mitc) Loan Reference No.Document6 pagesMost Important Terms and Conditions (Mitc) Loan Reference No.prashant gargNo ratings yet

- Signed Loan AgreementDocument9 pagesSigned Loan AgreementDOC27 PavanNo ratings yet

- KB220820BICLQ - Sanction LetterDocument4 pagesKB220820BICLQ - Sanction LetterSiddhantNo ratings yet

- KB220502AIMCU - Sanction Letter PDFDocument3 pagesKB220502AIMCU - Sanction Letter PDFRatnesh ShuklaNo ratings yet

- Bajaj Finance Limited: Loan Term SheetDocument12 pagesBajaj Finance Limited: Loan Term SheetazmimallickNo ratings yet

- DownloadDocument2 pagesDownloadpraneeth kuchimanchiNo ratings yet

- Sanction LetterDocument2 pagesSanction LetterSathyan Jr100% (1)

- MITCDocument8 pagesMITCajay huddaNo ratings yet

- Terms and Conditions Personal Loan 1694167502237Document9 pagesTerms and Conditions Personal Loan 1694167502237LAXMIDHAR BEHERANo ratings yet

- MITC 2024 UpdatedDocument26 pagesMITC 2024 UpdatedShree GaneshaNo ratings yet

- Terms and Condition Personal LoanDocument2 pagesTerms and Condition Personal Loanrupesh soniNo ratings yet

- NESL - E Contract AgreementDocument26 pagesNESL - E Contract AgreementMajhe GurujiNo ratings yet

- KB220315PRWTK - Sanction LetterDocument3 pagesKB220315PRWTK - Sanction LettersanjayjadusinghNo ratings yet

- Chandra Babu Sajja: Page 1 of 3Document3 pagesChandra Babu Sajja: Page 1 of 3Chandra Babu SajjaNo ratings yet

- Preview AgreementDocument11 pagesPreview Agreementasoukot84No ratings yet

- Loan Sanction Letter C33EFFTDocument10 pagesLoan Sanction Letter C33EFFTNAKSH CREATIONNo ratings yet

- keyFactStatement 1Document8 pageskeyFactStatement 1naga srinuNo ratings yet

- Terms and Conditions Personal Loan 1710164964727Document7 pagesTerms and Conditions Personal Loan 1710164964727THENDRAL 05No ratings yet

- Insta Overdraft Facility (Insta Od) Application Form: Application Id: CAOD0678881 IP Address: 14.139.245.68Document8 pagesInsta Overdraft Facility (Insta Od) Application Form: Application Id: CAOD0678881 IP Address: 14.139.245.68Prem KumarNo ratings yet

- DownloadDocument3 pagesDownloadwahidtab51No ratings yet

- Mitc To Be Signed by Customer OldDocument4 pagesMitc To Be Signed by Customer Oldstevenjones5001No ratings yet

- Personalloan PDFDocument2 pagesPersonalloan PDFparvathinarayanan1296No ratings yet

- Sanction Cum Loan Agreement 6656180Document44 pagesSanction Cum Loan Agreement 6656180suniltapukara1432No ratings yet

- Loan AgreementDocument7 pagesLoan Agreementsehrawatdushyant3No ratings yet

- Terms and ConditionsDocument14 pagesTerms and ConditionsPiyush ckNo ratings yet

- Unsecured Loan Agreement Editable Ver3 5 Aug23Document17 pagesUnsecured Loan Agreement Editable Ver3 5 Aug23svarun336No ratings yet

- Updated Key Fact SatementDocument4 pagesUpdated Key Fact SatementYashodhan RajwadeNo ratings yet

- Sanction Letter Tw -1Document3 pagesSanction Letter Tw -1rao.og777No ratings yet

- Repayment ScheduleDocument2 pagesRepayment ScheduleMaricris SerranoNo ratings yet

- SanctionDocument2 pagesSanctionBadal Singh Rajput0% (1)

- Sample Loan Agreement (Clix)Document8 pagesSample Loan Agreement (Clix)Digi CreditNo ratings yet

- Terms and Conditions Personal Loan 1701319332651Document7 pagesTerms and Conditions Personal Loan 1701319332651Parthiban DevendiranNo ratings yet

- Mathematics Form 3 - Chapter 3 Consumer MathematicsDocument10 pagesMathematics Form 3 - Chapter 3 Consumer MathematicsChan Soon won100% (1)

- Nodal - Officers - Central Bank of IndiaDocument8 pagesNodal - Officers - Central Bank of IndiaMassy ZafarNo ratings yet

- Wage and Tax Statement: OMB No. 1545-0008Document4 pagesWage and Tax Statement: OMB No. 1545-0008hmzxk28pcdNo ratings yet

- Money & FinanceDocument2 pagesMoney & FinanceZbigniew WałowskiNo ratings yet

- Stat 3Document9 pagesStat 3Madan RajNo ratings yet

- Account STMTDocument4 pagesAccount STMTsuranaveen814No ratings yet

- Velocity - RBF Introductory NoteDocument2 pagesVelocity - RBF Introductory Notekumarasathish0No ratings yet

- .PK Nmis Challan New VVFQNDU3ZkIDocument1 page.PK Nmis Challan New VVFQNDU3ZkIdarpankumar21No ratings yet

- YES BANK (Credit Card Nov-2024)Document2 pagesYES BANK (Credit Card Nov-2024)Anil AneNo ratings yet

- Testimony of ALAN JONES WELLS FARGODocument10 pagesTestimony of ALAN JONES WELLS FARGODinSFLANo ratings yet

- Account StatementDocument4 pagesAccount Statementdoomihashmi3No ratings yet

- Statement of DefficiencyDocument22 pagesStatement of DefficiencyJamaica DavidNo ratings yet

- Notice of Assessment - Year Ended 30 June 2020: !Msî15U (P4 Î#BabäDocument4 pagesNotice of Assessment - Year Ended 30 June 2020: !Msî15U (P4 Î#BabäClaudia AttardNo ratings yet

- Documents Checklist-BBDocument8 pagesDocuments Checklist-BBMd Rafat ArefinNo ratings yet

- 03 PROOF OF CASH Problem Solving Section 1 Solution 3Document2 pages03 PROOF OF CASH Problem Solving Section 1 Solution 3Erika Faith HalladorNo ratings yet

- Chile-Google Ads Usd Dif 3832.03Document1 pageChile-Google Ads Usd Dif 3832.03eduardo gomezNo ratings yet

- (Based On Presumed Data) File No.: 2-14349 Ddo: (000015) Accounts Officer Dte of TransportDocument2 pages(Based On Presumed Data) File No.: 2-14349 Ddo: (000015) Accounts Officer Dte of TransportD S PNo ratings yet

- Itns-281 TDS ChallanDocument1 pageItns-281 TDS Challanvirendra36999100% (2)

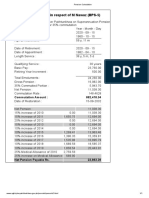

- Pension CalculationDocument1 pagePension Calculationulmilu15No ratings yet

- Partial Discharge - NoteDocument1 pagePartial Discharge - NotePrakruthi RanganathNo ratings yet

- 2023 06 20 10 25 36may 23 - 753008Document3 pages2023 06 20 10 25 36may 23 - 753008Biswamitra RathNo ratings yet

- CGC Food Corp.: Employee Id Employee Name Daily Rate Monthly SalaryDocument6 pagesCGC Food Corp.: Employee Id Employee Name Daily Rate Monthly Salaryacctg2012No ratings yet

- Bank StatementDocument3 pagesBank Statementbigman walthoNo ratings yet

- Premium Paid CertificateDocument1 pagePremium Paid CertificateSenthil balasubramanianNo ratings yet

- Genmath Lesson 8Document32 pagesGenmath Lesson 8Denmark SantosNo ratings yet

- Compound Interest (English)Document2 pagesCompound Interest (English)romigurjarNo ratings yet

- hotUSA Uncek 20Document27 pageshotUSA Uncek 20onaldnewday100% (1)

- Rbi IfscDocument183 pagesRbi IfscatulunofficialxNo ratings yet

- 2720 23032024120752Document2 pages2720 23032024120752rajmeenameenaji9797No ratings yet

- Đề-cương-ESP233Document30 pagesĐề-cương-ESP233AB CDNo ratings yet