0% found this document useful (0 votes)

4 viewsAssignment II Spring 2025 Solution

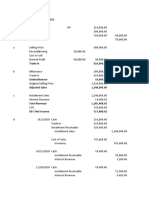

The document discusses capital budgeting, explaining its purpose in evaluating potential investments and the distinction between independent and mutually exclusive projects. It outlines project evaluation rules using NPV and IRR, the implications of callable and convertible bonds, and the significance of bond ratings. Additionally, it addresses cannibalization effects on cash flows and provides various financial problems related to bond pricing, project evaluation, and investment decisions.

Uploaded by

blake1warnerCopyright

© © All Rights Reserved

Available Formats

Download as DOC, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

4 viewsAssignment II Spring 2025 Solution

The document discusses capital budgeting, explaining its purpose in evaluating potential investments and the distinction between independent and mutually exclusive projects. It outlines project evaluation rules using NPV and IRR, the implications of callable and convertible bonds, and the significance of bond ratings. Additionally, it addresses cannibalization effects on cash flows and provides various financial problems related to bond pricing, project evaluation, and investment decisions.

Uploaded by

blake1warnerCopyright

© © All Rights Reserved

Available Formats

Download as DOC, PDF, TXT or read online on Scribd

/ 8