FIR 4770 Midterm Review Questions: Student

FIR 4770 Midterm Review Questions: Student

Download as docx, pdf, or txt

You might also like

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2024 Edition)From EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2024 Edition)Rating: 4.5 out of 5 stars4.5/5 (5)

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2024 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2024 Edition)Rating: 5 out of 5 stars5/5 (1)

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2024 Edition)From EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2024 Edition)No ratings yet

- EC3333 Midterm Fall 2014.questionsDocument7 pagesEC3333 Midterm Fall 2014.questionsChiew Jun SiewNo ratings yet

- QuizDocument6 pagesQuizchitu1992No ratings yet

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2019 Edition)From EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2019 Edition)Rating: 5 out of 5 stars5/5 (1)

- Miss Samantha D Erlston Doreen 56 B High RD Edenvale 1609: Transactions in RAND (ZAR) Accrued Bank ChargesDocument2 pagesMiss Samantha D Erlston Doreen 56 B High RD Edenvale 1609: Transactions in RAND (ZAR) Accrued Bank ChargesSamantha Erlston100% (2)

- Understanding Fixed-Income Risk and ReturnDocument19 pagesUnderstanding Fixed-Income Risk and ReturnHassan100% (1)

- R55 Understanding Fixed-Income Risk and Return Q BankDocument20 pagesR55 Understanding Fixed-Income Risk and Return Q BankAhmedNo ratings yet

- Loan StatementDocument3 pagesLoan StatementNityananda SahuNo ratings yet

- Midterm Practice (Solution)Document7 pagesMidterm Practice (Solution)kaetie.yuan04No ratings yet

- Quiz 15 (443C) : StudentDocument6 pagesQuiz 15 (443C) : StudentCeleste YuNo ratings yet

- 70 32301805Document54 pages70 32301805Mar Conesa OtónNo ratings yet

- Test Bank Chapter 15 Investment BodieDocument42 pagesTest Bank Chapter 15 Investment BodieTami DoanNo ratings yet

- CH 7Document45 pagesCH 7yawnzz89100% (3)

- FRM Test Portfolio ManagementDocument7 pagesFRM Test Portfolio Managementram ramNo ratings yet

- Financial Economics - Model 2 - Solutions - LastDocument6 pagesFinancial Economics - Model 2 - Solutions - Lastalicia.serrano01No ratings yet

- RRR MCQDocument18 pagesRRR MCQRezzan Joy MejiaNo ratings yet

- 4412 2024B SampleMTDocument5 pages4412 2024B SampleMTemirdurmaz200131No ratings yet

- Financial Economics - Model 1 - Solutions - LastDocument6 pagesFinancial Economics - Model 1 - Solutions - Lastalicia.serrano01No ratings yet

- QuestionsDocument72 pagesQuestionsmudassar saeedNo ratings yet

- 4412 2024B SampleMT KeyDocument5 pages4412 2024B SampleMT Keyemirdurmaz200131No ratings yet

- Investment Quiz Test QNST and AnswerDocument9 pagesInvestment Quiz Test QNST and AnswerPrimrose Chisunga100% (1)

- File 20220531 173746 Thị Trường Tài ChínhDocument11 pagesFile 20220531 173746 Thị Trường Tài ChínhNguyễn Trâm AnhNo ratings yet

- ExamDocument18 pagesExamLiza Roshchina100% (1)

- Choice Multiple Questions - Docx.u1conflictDocument4 pagesChoice Multiple Questions - Docx.u1conflictAbdulaziz S.mNo ratings yet

- Weekly Quiz 2Document30 pagesWeekly Quiz 2Emmmanuel ArthurNo ratings yet

- Fa 06 Ex 3Document7 pagesFa 06 Ex 3MuhammadIjazAslamNo ratings yet

- FIN. 4828 CH. 18: CreateDocument22 pagesFIN. 4828 CH. 18: CreateSwati VermaNo ratings yet

- UntitledDocument4 pagesUntitledMuhammad AbdullahNo ratings yet

- Chap007 Test Bank (1) SolutionDocument11 pagesChap007 Test Bank (1) SolutionMinji Michelle J100% (1)

- TB Chapter20Document25 pagesTB Chapter20Viola HuynhNo ratings yet

- Mockterm FINS2624 S1 2013Document12 pagesMockterm FINS2624 S1 2013sagarox7No ratings yet

- Hull: Options, Futures, and Other Derivatives, Tenth Edition Chapter 25: Credit Derivatives Multiple Choice Test BankDocument4 pagesHull: Options, Futures, and Other Derivatives, Tenth Edition Chapter 25: Credit Derivatives Multiple Choice Test BankKevin Molly KamrathNo ratings yet

- Prelim Exam - For PrintingDocument4 pagesPrelim Exam - For PrintingThat's FHEVulousNo ratings yet

- QuizDocument6 pagesQuizchitu1992No ratings yet

- 재무관리 기말고사 족보Document14 pages재무관리 기말고사 족보yanghyunjun72No ratings yet

- 8230 Sample Final 1Document8 pages8230 Sample Final 1lilbouyinNo ratings yet

- Bank 1,2,3,4-Portfolios IiDocument11 pagesBank 1,2,3,4-Portfolios IimileNo ratings yet

- Quiz 1Document8 pagesQuiz 1HUANG WENCHENNo ratings yet

- Valuation of Debt Contracts and Their Price Volatility Characteristics Questions See Answers BelowDocument7 pagesValuation of Debt Contracts and Their Price Volatility Characteristics Questions See Answers Belowevivanco1899No ratings yet

- ĐTTC Duy LinhDocument21 pagesĐTTC Duy LinhThảo LêNo ratings yet

- 7 November 2020 - Question - Book 5-UnlockedDocument6 pages7 November 2020 - Question - Book 5-UnlockedAditya NugrohoNo ratings yet

- Fin 3013 Chapter 10Document56 pagesFin 3013 Chapter 10spectrum_48No ratings yet

- Chap 14Document27 pagesChap 14Thu YếnNo ratings yet

- Investment and Portoflio MGT QuestionsDocument6 pagesInvestment and Portoflio MGT QuestionsnathnaelNo ratings yet

- Fixed IncomeDocument19 pagesFixed IncomeNgọc ThảoNo ratings yet

- TB Chapter07Document83 pagesTB Chapter07dan_joel069968No ratings yet

- 97fi MasterDocument12 pages97fi MasterHamid UllahNo ratings yet

- QLDMDTDocument35 pagesQLDMDThang25040107No ratings yet

- Fin333 Secondmt04w Sample QuestionsDocument10 pagesFin333 Secondmt04w Sample QuestionsSara NasNo ratings yet

- Possible Mid-Term QuestionsDocument10 pagesPossible Mid-Term QuestionsZobia JavaidNo ratings yet

- Hull: Options, Futures, and Other Derivatives, Tenth Edition Chapter 5: Determination of Forward and Futures Prices Multiple Choice Test BankDocument4 pagesHull: Options, Futures, and Other Derivatives, Tenth Edition Chapter 5: Determination of Forward and Futures Prices Multiple Choice Test BankKevin Molly KamrathNo ratings yet

- Test 092403Document10 pagesTest 092403Janice ChanNo ratings yet

- Section 04Document97 pagesSection 04HarshNo ratings yet

- TT ĐCTCDocument7 pagesTT ĐCTCthuyvanscNo ratings yet

- Chap 005Document90 pagesChap 005조서현50% (2)

- Fin 072 Midterm ExamDocument10 pagesFin 072 Midterm ExamGargaritanoNo ratings yet

- FPQP Practice Question Workbook: 1,000 Comprehensive Practice Questions (2024 Edition)From EverandFPQP Practice Question Workbook: 1,000 Comprehensive Practice Questions (2024 Edition)No ratings yet

- CFA 2012 - Exams L1 : How to Pass the CFA Exams After Studying for Two Weeks Without AnxietyFrom EverandCFA 2012 - Exams L1 : How to Pass the CFA Exams After Studying for Two Weeks Without AnxietyRating: 3 out of 5 stars3/5 (2)

- Summary of William J. Bernstein's The Intelligent Asset AllocatorFrom EverandSummary of William J. Bernstein's The Intelligent Asset AllocatorNo ratings yet

- Security Analysis & Portfolio Management: Mba 3 SemesterDocument6 pagesSecurity Analysis & Portfolio Management: Mba 3 SemesterDERAJUDDIN AHMRDNo ratings yet

- Pages 55 Capital Market Operation FinalDocument38 pagesPages 55 Capital Market Operation FinalAakash SharmaNo ratings yet

- MBA666 - Decision - Trees Examples PDFDocument10 pagesMBA666 - Decision - Trees Examples PDFrajNo ratings yet

- Chap 2 - Management AccountingDocument13 pagesChap 2 - Management AccountingEmmanuel TeoNo ratings yet

- Chief Financial Officer in San Francisco Bay CA Kevin BerryDocument2 pagesChief Financial Officer in San Francisco Bay CA Kevin BerryKevinBerry1No ratings yet

- Month-To-Month Lease Agreement: FollowingDocument8 pagesMonth-To-Month Lease Agreement: FollowingyomexNo ratings yet

- Fixed Exchange Rates and Foreign Exchange Intervention (Lecture 8, Chapter 18)Document9 pagesFixed Exchange Rates and Foreign Exchange Intervention (Lecture 8, Chapter 18)nihadsamir2002No ratings yet

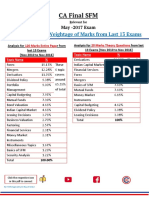

- CA Final SFM Chapter Wise Weightage Applicable For May 2017 NFUH6CATDocument1 pageCA Final SFM Chapter Wise Weightage Applicable For May 2017 NFUH6CATvignesh_vikiNo ratings yet

- FinanceDocument48 pagesFinanceMimi Adriatico JaranillaNo ratings yet

- Property Management Business ProposalDocument10 pagesProperty Management Business ProposalNicole LamNo ratings yet

- Simple InterestDocument58 pagesSimple InterestCleofeNo ratings yet

- Tutorial Letter 103/3/2016: Group Financial ReportingDocument52 pagesTutorial Letter 103/3/2016: Group Financial ReportingTINOTENDA MUCHEMWANo ratings yet

- Chapter 4 The Viability of A Business IdeaDocument28 pagesChapter 4 The Viability of A Business IdeaLawrence MosizaNo ratings yet

- Takeover FullDocument92 pagesTakeover Fullswatigupta8850% (2)

- ReportDocument12 pagesReportVishala GudageriNo ratings yet

- Portfolio Optimization in Electricity Markets: Min Liu, Felix F. WuDocument10 pagesPortfolio Optimization in Electricity Markets: Min Liu, Felix F. Wujorge jorgeNo ratings yet

- Robo Advisory 2Document8 pagesRobo Advisory 2Ankur Pandey0% (1)

- Comparative Analysis of Sbi Bank and Icici BankDocument74 pagesComparative Analysis of Sbi Bank and Icici BankRanju Chauhan80% (5)

- 58 - A - Shekhar - DPC Ii JournalDocument69 pages58 - A - Shekhar - DPC Ii JournalShekhar PanseNo ratings yet

- What Is Investment Definition?Document6 pagesWhat Is Investment Definition?Simohamed BennaniNo ratings yet

- Cersai GhigheDocument2 pagesCersai Ghighechandan bhatiNo ratings yet

- Information Sheet - BKKPG-8 - Preparing Financial StatementsDocument10 pagesInformation Sheet - BKKPG-8 - Preparing Financial StatementsEron Roi Centina-gacutanNo ratings yet

- PDF September Ict Notespdf - CompressDocument14 pagesPDF September Ict Notespdf - CompressSagar BhandariNo ratings yet

- W-8BEN: Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Document1 pageW-8BEN: Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Ajmain Abdullah Utshow100% (1)

- Business Development Plan ON: Adaa Ethnic Wears and DressesDocument34 pagesBusiness Development Plan ON: Adaa Ethnic Wears and DressesNishedh AdhikariNo ratings yet

- C. Worksheet 1 - Liquidation - B List of ContributoriesDocument7 pagesC. Worksheet 1 - Liquidation - B List of ContributoriesSnigdha RohillaNo ratings yet

- 10%DP12mos-BF W/ BANK CHARGES Amaia Land Corp. Amaia Scapes CabanatuanDocument1 page10%DP12mos-BF W/ BANK CHARGES Amaia Land Corp. Amaia Scapes CabanatuanMao WatanabeNo ratings yet

- Payments Standardss-InitiationDocument349 pagesPayments Standardss-InitiationpurushotamsaNo ratings yet