Transfer Pricing

Transfer Pricing

Download as ppt, pdf, or txt

You might also like

- Bohemia IndustriesDocument13 pagesBohemia Industriesaman100% (1)

- ADIT TP 2022-12 QuestionsDocument6 pagesADIT TP 2022-12 QuestionsSalih MansoorNo ratings yet

- ADIT TP 2021-06 QuestionsDocument6 pagesADIT TP 2021-06 QuestionsSalih MansoorNo ratings yet

- Sabya BhaiDocument6 pagesSabya BhaiamanNo ratings yet

- Договор отельDocument2 pagesДоговор отельСергей КаменёкNo ratings yet

- Taxation Trends in The European Union-KPDU22001ENN - 2022Document340 pagesTaxation Trends in The European Union-KPDU22001ENN - 2022Raul Stefan Costea100% (1)

- Transfer Pricing EssayDocument8 pagesTransfer Pricing EssayFernando Montoro SánchezNo ratings yet

- MTN Annual Financial Results Booklet 2014Document40 pagesMTN Annual Financial Results Booklet 2014The New VisionNo ratings yet

- Coordinated Issue Paper - Sec. 482 CSA Buy-In AdjustmentsDocument18 pagesCoordinated Issue Paper - Sec. 482 CSA Buy-In AdjustmentsSgt2No ratings yet

- Income Tax Provision ChecklistDocument20 pagesIncome Tax Provision Checklistakschess pNo ratings yet

- Eli Lilly Ranbaxy Joint Venture Case StudyDocument21 pagesEli Lilly Ranbaxy Joint Venture Case StudyAnil Jadli100% (2)

- GTZ Low Cost Housing Technical Manual Volume-IDocument0 pagesGTZ Low Cost Housing Technical Manual Volume-ISolomon BanteywaluNo ratings yet

- IFM 08 Transfer PriceDocument27 pagesIFM 08 Transfer PriceTanu GuptaNo ratings yet

- SMA Group 5 - Transfer PricingDocument16 pagesSMA Group 5 - Transfer PricingShreya PatelNo ratings yet

- Transfer PricingDocument25 pagesTransfer PricingAmanVashistNo ratings yet

- Transfer Pricing in Divisionalized CompaniesDocument33 pagesTransfer Pricing in Divisionalized CompaniesCarl Agape Davis100% (2)

- CA FINAL Transfer PricingDocument11 pagesCA FINAL Transfer Pricingjkrapps100% (1)

- Pricing Decisions AND Strategies: by B.W.MainaDocument64 pagesPricing Decisions AND Strategies: by B.W.MainanobleconsultantsNo ratings yet

- ICAI Guidance NoteDocument208 pagesICAI Guidance NotePadmanabha Narayan100% (1)

- Methods of Transfer Pricing (4 Methods) : (1) Market-Based PricesDocument11 pagesMethods of Transfer Pricing (4 Methods) : (1) Market-Based PricesnirakhanNo ratings yet

- Transfer Pricing MethodsDocument41 pagesTransfer Pricing MethodsExcel100% (1)

- Sir Tariq Tunio PRC - Itb - Merged NewDocument2,182 pagesSir Tariq Tunio PRC - Itb - Merged NewHanan AliNo ratings yet

- International Business Functional StrategiesDocument2 pagesInternational Business Functional StrategiesSachu Shaolin0% (1)

- Transfer Pricing and Advance Pricing Agreements: Aztec Software and Technology Service Ltd. vs. ACITDocument8 pagesTransfer Pricing and Advance Pricing Agreements: Aztec Software and Technology Service Ltd. vs. ACITA BNo ratings yet

- Ie Centralised Procurement Strategies Transfer PricingDocument4 pagesIe Centralised Procurement Strategies Transfer PricingHarryNo ratings yet

- Impact of Transfer Pricing On Tax PlanningDocument5 pagesImpact of Transfer Pricing On Tax PlanningDaisy AnitaNo ratings yet

- Lecture 23 - 45 CombinedDocument271 pagesLecture 23 - 45 CombinedMuhammad Kamran KhanNo ratings yet

- TAX Academy Updated 2020Document22 pagesTAX Academy Updated 2020Ok ayNo ratings yet

- Lectures On Financial Economics (PDFDrive)Document900 pagesLectures On Financial Economics (PDFDrive)Emalu BonifaceNo ratings yet

- Lesson 9 Problems of Transfer Pricing Practical ExerciseDocument6 pagesLesson 9 Problems of Transfer Pricing Practical ExerciseMadhu kumarNo ratings yet

- 4 Intra-Industry AnalysisDocument20 pages4 Intra-Industry AnalysisOscar YondaNo ratings yet

- Taxation 2015 UP Pre-WeekDocument216 pagesTaxation 2015 UP Pre-WeekIriz Beleno100% (3)

- Engineering Economics (Theory of Cost)Document12 pagesEngineering Economics (Theory of Cost)Usman QasimNo ratings yet

- Transfer Prices Functions, Types and Behavioral ImplicationsDocument12 pagesTransfer Prices Functions, Types and Behavioral ImplicationsSareema KoiralaNo ratings yet

- Working Capital Adjustments Under Transfer PricingDocument9 pagesWorking Capital Adjustments Under Transfer PricingTaxpert Professionals Private LimitedNo ratings yet

- Lecture 23 - Advanced Cost and Management AccountingDocument16 pagesLecture 23 - Advanced Cost and Management AccountingawaisjinnahNo ratings yet

- Counterparty Credit Exposure and CVA - An Intergrated Approch (UBS)Document34 pagesCounterparty Credit Exposure and CVA - An Intergrated Approch (UBS)Mo MokNo ratings yet

- Transfer Pricing-A Case Study of Vodafone: ArticleDocument5 pagesTransfer Pricing-A Case Study of Vodafone: ArticleRazafinandrasanaNo ratings yet

- Facts On Royalties: WWW - Energy.alberta - CaDocument2 pagesFacts On Royalties: WWW - Energy.alberta - CaWilson Pepe GonzalezNo ratings yet

- The OECD Guidelines Provide Techniques For Determining Transfer PricingDocument3 pagesThe OECD Guidelines Provide Techniques For Determining Transfer PricingInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Pricing by Strategy - Hock MCQDocument20 pagesPricing by Strategy - Hock MCQRajeena pkNo ratings yet

- Rs Fund Transfer PricingDocument12 pagesRs Fund Transfer PricingAman JainNo ratings yet

- 500 MctheoriesDocument81 pages500 Mctheorieserickson hernanNo ratings yet

- Pricing EconomicsDocument59 pagesPricing EconomicsJai JohnNo ratings yet

- Transfer PricingDocument53 pagesTransfer PricingkannnamreddyeswarNo ratings yet

- June 2017 Paper 3.03 (Question Paper)Document7 pagesJune 2017 Paper 3.03 (Question Paper)Timore Francis100% (1)

- December 2017 Paper 1 (Candidate Script)Document9 pagesDecember 2017 Paper 1 (Candidate Script)arunvaleraphotos2023No ratings yet

- Transfer PricingDocument15 pagesTransfer PricingJulie Marie Anne LUBINo ratings yet

- Doupnik ch11Document33 pagesDoupnik ch11Catalina Oriani0% (1)

- Deloitte Publication - Legal Entity SimplificationDocument4 pagesDeloitte Publication - Legal Entity SimplificationlacengearNo ratings yet

- 3 Income Taxation Final PDFDocument109 pages3 Income Taxation Final PDFwilliam0910900% (1)

- Pricing F. Livesey PDFDocument180 pagesPricing F. Livesey PDFshuktaaNo ratings yet

- International BusinessDocument270 pagesInternational BusinessKaran Menghani100% (1)

- Functional Areas of IBDocument27 pagesFunctional Areas of IBAbhinav KumarNo ratings yet

- Me - Funds Transfer Pricing InsightsDocument9 pagesMe - Funds Transfer Pricing Insightsskyping75No ratings yet

- Local File ChecklistDocument6 pagesLocal File ChecklistBorys UlanenkoNo ratings yet

- M&ADocument27 pagesM&ArinacharNo ratings yet

- Cost & Managerial Accounting Study MaterialDocument109 pagesCost & Managerial Accounting Study Materialdanielnebeyat7No ratings yet

- 4.presentation On TP MethodDocument47 pages4.presentation On TP MethodMasum BillahNo ratings yet

- International PricingDocument33 pagesInternational Pricingarvind_pathak_4No ratings yet

- TransferpricingDocument24 pagesTransferpricingollieNo ratings yet

- Transfer PricingDocument18 pagesTransfer PricingSunny SharmaNo ratings yet

- GM CH 6 Pricing DecisionsDocument48 pagesGM CH 6 Pricing DecisionsgeremewNo ratings yet

- Transfer PricingDocument41 pagesTransfer PricinggirishNo ratings yet

- Transfer Pricing RegulationsDocument25 pagesTransfer Pricing RegulationsRavi ShankerNo ratings yet

- Flexible Budgets, Variances, and Management Control: ManasweeDocument46 pagesFlexible Budgets, Variances, and Management Control: ManasweeamanNo ratings yet

- Clay Bottle DescriptionDocument1 pageClay Bottle DescriptionamanNo ratings yet

- Approved CAE GuidelineDocument50 pagesApproved CAE GuidelineamanNo ratings yet

- Indian Value System: Ethics. Aristotle in His N.E Part Company WithDocument16 pagesIndian Value System: Ethics. Aristotle in His N.E Part Company WithamanNo ratings yet

- HRM - Sustainability Management - 2016-2018 - PPT I - Introduction and Manpower PlanningDocument90 pagesHRM - Sustainability Management - 2016-2018 - PPT I - Introduction and Manpower Planningaman0% (1)

- Rice Mills of Jharkhand and Their Pollutions Problems by Er. S.K.singhDocument3 pagesRice Mills of Jharkhand and Their Pollutions Problems by Er. S.K.singhamanNo ratings yet

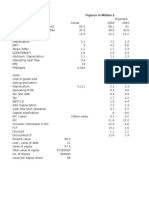

- Monmouth Inc Figures in Million $Document3 pagesMonmouth Inc Figures in Million $amanNo ratings yet

- MockExerciseDocument50 pagesMockExerciseamanNo ratings yet

- 1672 Market SignalsDocument8 pages1672 Market Signalsaman100% (1)

- Maruti SuzukiDocument12 pagesMaruti SuzukiamanNo ratings yet

- Interwar PeriodDocument2 pagesInterwar PeriodamanNo ratings yet

- X (No. of Cups) Y (No of Plates) 120 160 Profit $/unit 2 1.5Document9 pagesX (No. of Cups) Y (No of Plates) 120 160 Profit $/unit 2 1.5amanNo ratings yet

- Maruti SuzukiDocument12 pagesMaruti SuzukiamanNo ratings yet

- Ambuja Cement Annual Report 2015 Web Final - PDF 13Document170 pagesAmbuja Cement Annual Report 2015 Web Final - PDF 13amanNo ratings yet

- BA7108 Written CommunicationDocument5 pagesBA7108 Written CommunicationamanNo ratings yet

- Stability of The Equilibrium: Reference Material For International Finance Course For Ex-MBA-2016-17Document4 pagesStability of The Equilibrium: Reference Material For International Finance Course For Ex-MBA-2016-17amanNo ratings yet

- Case Analysis High Street 05.01.2017Document2 pagesCase Analysis High Street 05.01.2017amanNo ratings yet

- Zomato Brand ProfileDocument48 pagesZomato Brand ProfileamanNo ratings yet

- Q1. Why Does MR Butler Have To Borrow So Much Money To Support This Profitable Business?Document2 pagesQ1. Why Does MR Butler Have To Borrow So Much Money To Support This Profitable Business?amanNo ratings yet

- COMA Assignment Answer 1: Contribution Per KG (RS.) 13.33 8.33 8.89Document6 pagesCOMA Assignment Answer 1: Contribution Per KG (RS.) 13.33 8.33 8.89amanNo ratings yet

- Manron Ltd. - HRM PoliciesDocument6 pagesManron Ltd. - HRM PoliciesamanNo ratings yet

- How To Invest in Social CapitalDocument18 pagesHow To Invest in Social CapitalamanNo ratings yet

- Masquerade (Regional Eliminations)Document5 pagesMasquerade (Regional Eliminations)Ayvee BlanchNo ratings yet

- BudgetDocument15 pagesBudgetJoydip DasguptaNo ratings yet

- Advanced Derivatives Course Chapter 1Document6 pagesAdvanced Derivatives Course Chapter 1api-3841270No ratings yet

- Comparative Study of The Principles of Contract Formation India and Uk - HardDocument37 pagesComparative Study of The Principles of Contract Formation India and Uk - HardJyoti SharmaNo ratings yet

- KS Oil AnnualReport2014-2015 PDFDocument103 pagesKS Oil AnnualReport2014-2015 PDFAneesh VelluvalappilNo ratings yet

- Fishing in The Commons in The Text We Introduced TheDocument2 pagesFishing in The Commons in The Text We Introduced Thetrilocksp SinghNo ratings yet

- KelloggDocument23 pagesKelloggAnish JohnNo ratings yet

- Pi (E) Day Payday!: Marketing Lead: Sam DomingoDocument4 pagesPi (E) Day Payday!: Marketing Lead: Sam DomingoYuan TugnaoNo ratings yet

- RedmrcDocument1 pageRedmrcHitesh PanigrahiNo ratings yet

- The 6 Pillars of Successful BusinessesDocument81 pagesThe 6 Pillars of Successful BusinessesJoshelle B. BanciloNo ratings yet

- Econ 100.1 - ReviewerDocument34 pagesEcon 100.1 - ReviewerLianne Angelico Depante100% (1)

- 0521772524Document352 pages0521772524Samuel RyanNo ratings yet

- 1617 1stS FX CLim 1 1Document10 pages1617 1stS FX CLim 1 1ShitzeoNo ratings yet

- Internship Report (Mama Nourly SDN BHD)Document37 pagesInternship Report (Mama Nourly SDN BHD)RaziYangPemurah33% (3)

- FDWMS Research Report - TVS Electronics Ltd.Document3 pagesFDWMS Research Report - TVS Electronics Ltd.dakshbajajNo ratings yet

- CompetitorsDocument3 pagesCompetitorsTeam ProspeNo ratings yet

- Kimberly C. GleasonDocument44 pagesKimberly C. Gleasonfisayobabs11No ratings yet

- 094 CIMB-Principal Asia Pacific Dynamic Income Fund MYR FFSDocument2 pages094 CIMB-Principal Asia Pacific Dynamic Income Fund MYR FFSAbby IbnuNo ratings yet

- Oferta y DemandaDocument9 pagesOferta y DemandaRosario Rivera NegrónNo ratings yet

- Differences Between Indian Conditions of Contract AND Fidic Conditions of ContractDocument13 pagesDifferences Between Indian Conditions of Contract AND Fidic Conditions of ContractmanojkumarmurlidharaNo ratings yet

- Financing Paper May 09 - Final Draft W Table of Contents FINALDocument20 pagesFinancing Paper May 09 - Final Draft W Table of Contents FINALAnmol VanamaliNo ratings yet

- Export ManagementDocument34 pagesExport ManagementAkram Islam50% (2)

- Sports IndustryDocument69 pagesSports IndustryMohit AgarwalNo ratings yet

- DCF ExamplesDocument7 pagesDCF Examplesarti guptaNo ratings yet

- Minggu 5 Ch07 Stocks, Stock Valuation, and Stock Market EquilibriumDocument57 pagesMinggu 5 Ch07 Stocks, Stock Valuation, and Stock Market Equilibriumcinof012No ratings yet

- English Assignment - About EuroDocument11 pagesEnglish Assignment - About EuroFahmi Nur AlfiyanNo ratings yet

- Nit 3Document11 pagesNit 3santanu_banerjee_6No ratings yet