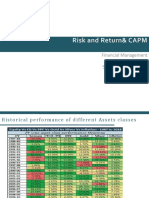

Trade-Off Between Risk & Return

Trade-Off Between Risk & Return

Download as ppt, pdf, or txt

You might also like

- Chapter 7 StudentDocument61 pagesChapter 7 StudentLinh HoangNo ratings yet

- EFM2e, CH 07, Slides-1Document51 pagesEFM2e, CH 07, Slides-1Maria DevinaNo ratings yet

- Unit 3: Risk, Return, and Capital Asset Pricing Model (CAPMDocument30 pagesUnit 3: Risk, Return, and Capital Asset Pricing Model (CAPMCyrine Miwa RodriguezNo ratings yet

- Chapter 4 Risk and ReturnDocument40 pagesChapter 4 Risk and ReturnmedrekNo ratings yet

- R P - P - + C: Chapter Seven Basics of Risk and ReturnDocument13 pagesR P - P - + C: Chapter Seven Basics of Risk and ReturntemedebereNo ratings yet

- ch05 - Risk and ReturnsDocument53 pagesch05 - Risk and Returnsdoulat valmaniNo ratings yet

- Chapter 08Document50 pagesChapter 08hunkar1974No ratings yet

- FM Lecture - 6 - ch08 - 201819S2Document48 pagesFM Lecture - 6 - ch08 - 201819S2ziqingyeNo ratings yet

- IIMC Corp Finance 2018-19Document54 pagesIIMC Corp Finance 2018-19Ambuj AgrawalNo ratings yet

- Risk and Rates of Return: Stand-Alone Risk Portfolio Risk Risk & Return: CAPMDocument49 pagesRisk and Rates of Return: Stand-Alone Risk Portfolio Risk Risk & Return: CAPMNazmus Sakib RahatNo ratings yet

- Slides Set1Document119 pagesSlides Set1Iqra JawedNo ratings yet

- CH 06 (Edited)Document57 pagesCH 06 (Edited)sam heisenbergNo ratings yet

- LN - p1 - t5 - MPT and The CapmDocument33 pagesLN - p1 - t5 - MPT and The CapmAGRIM CHAUDHURYNo ratings yet

- CH (8) - Risk Return - Part 1Document37 pagesCH (8) - Risk Return - Part 1amrrrefa3y74No ratings yet

- Ch 8Document42 pagesCh 8anbalaganc.sclasNo ratings yet

- Risk and Return - Lu-6Document54 pagesRisk and Return - Lu-6Mega capitalmarket100% (1)

- Risk & Rates of ReturnDocument30 pagesRisk & Rates of ReturnasifanisNo ratings yet

- Risk and Rates of Return: Stand-Alone Risk Portfolio Risk Risk & Return: CAPM / SMLDocument31 pagesRisk and Rates of Return: Stand-Alone Risk Portfolio Risk Risk & Return: CAPM / SMLArslan QayyumNo ratings yet

- Week 7 Week 8 - Intro To Portfolio TheoryDocument24 pagesWeek 7 Week 8 - Intro To Portfolio TheoryJoshua NemiNo ratings yet

- Lecture 4 Return and RiskDocument50 pagesLecture 4 Return and RiskMuhammad YahyaNo ratings yet

- CF Lecture 3 Risk and Return v1Document44 pagesCF Lecture 3 Risk and Return v1Tâm NhưNo ratings yet

- Ch03-5 Portifolio Theory - Risk Return AnalysisDocument113 pagesCh03-5 Portifolio Theory - Risk Return AnalysismupiwamasimbaNo ratings yet

- Finacial Amnagement, Chapter 03Document39 pagesFinacial Amnagement, Chapter 03Rabby hasanNo ratings yet

- Risk and Return - The Two Sides of An Investment Coin : Unit IIDocument31 pagesRisk and Return - The Two Sides of An Investment Coin : Unit IIjainneelamNo ratings yet

- Lecture 7-Risk & ReturnDocument58 pagesLecture 7-Risk & ReturnSour CandyNo ratings yet

- Combinepdf PDFDocument65 pagesCombinepdf PDFCam SpaNo ratings yet

- Chapter 1 FMDocument47 pagesChapter 1 FMabdellaNo ratings yet

- Lecture 7 Risk - Return Stand Alone - 05042023 115110amDocument30 pagesLecture 7 Risk - Return Stand Alone - 05042023 115110amMasoom AlamNo ratings yet

- Risk and Return: Past and PrologueDocument39 pagesRisk and Return: Past and ProloguerrNo ratings yet

- Chapter5 Risk and Rate of ReturnDocument53 pagesChapter5 Risk and Rate of Returnmyvth22404caNo ratings yet

- Risk and Rates of Return CH06 PDFDocument16 pagesRisk and Rates of Return CH06 PDFLily DaniaNo ratings yet

- 재무관리8Document32 pages재무관리8신동엽No ratings yet

- Risk and Rates of ReturnDocument25 pagesRisk and Rates of ReturnAobakwe Rose TshupeloNo ratings yet

- Finance Final Cheat SheetDocument4 pagesFinance Final Cheat Sheetpwkearns32No ratings yet

- Risk and Return Risk and ReturnDocument33 pagesRisk and Return Risk and ReturnIxhaq motiwalaNo ratings yet

- Introduction To Risk and Return: Principles of Corporate FinanceDocument30 pagesIntroduction To Risk and Return: Principles of Corporate FinancechooisinNo ratings yet

- Chapter 5: Risk and ReturnDocument31 pagesChapter 5: Risk and ReturnEyobedNo ratings yet

- Manchester Business School - Global Business and Accounting Workshop - Day2Document32 pagesManchester Business School - Global Business and Accounting Workshop - Day2K PNo ratings yet

- Lecture 7-Risk & ReturnDocument59 pagesLecture 7-Risk & Returnnhunhp04No ratings yet

- Abraham G. (Assistant Professor) : Advanced Financial Management MAF - 581Document47 pagesAbraham G. (Assistant Professor) : Advanced Financial Management MAF - 581Abraham Gebregiorgis BerheNo ratings yet

- Chapter 8 Risk and Return PresentationDocument29 pagesChapter 8 Risk and Return PresentationsarmadNo ratings yet

- Finance 2022 Fall1 LectureNotes Module06Document48 pagesFinance 2022 Fall1 LectureNotes Module06Jiayi ZhuNo ratings yet

- Risk and Return TheoryDocument45 pagesRisk and Return Theoryanshika rathoreNo ratings yet

- Risk & Return: Risk of A Portfolio-Uncertainty Main View Two AspectsDocument36 pagesRisk & Return: Risk of A Portfolio-Uncertainty Main View Two AspectsAminul Islam AmuNo ratings yet

- D1 Equity Price Risk Student VersionDocument30 pagesD1 Equity Price Risk Student VersionChu Phương ThảoNo ratings yet

- Risk & Return BBA 2313Document24 pagesRisk & Return BBA 2313seyam kaiserNo ratings yet

- Class Return & Risk-Part-1Document57 pagesClass Return & Risk-Part-1Sanjida KajolNo ratings yet

- TEME 6 Engl 2022Document50 pagesTEME 6 Engl 2022ihor.rudyk.mmeba.2022No ratings yet

- EFM - MSESPM - Lec 5 - Risk and Return - Chapt4 - 2020Document21 pagesEFM - MSESPM - Lec 5 - Risk and Return - Chapt4 - 2020RabinNo ratings yet

- IFA NAZUWA (69875) Tutorial 2Document6 pagesIFA NAZUWA (69875) Tutorial 2Ifa Nazuwa ZaidilNo ratings yet

- Corporate Finance-Lecture 4Document39 pagesCorporate Finance-Lecture 4nguyenngocdoquyen9bNo ratings yet

- The Return & Risk: Books: L J GitmanDocument23 pagesThe Return & Risk: Books: L J GitmanNilima Islam Mim 201-11-6426No ratings yet

- IPS Group3Document29 pagesIPS Group3KHOA LÊ VŨ CHÂUNo ratings yet

- Lecture 9 - Portfolio TheoryDocument13 pagesLecture 9 - Portfolio TheoryJason LuximonNo ratings yet

- Risk and Rate of Returns in Financial ManagementDocument50 pagesRisk and Rate of Returns in Financial ManagementReaderNo ratings yet

- Corporate Finance Formulas: A Simple IntroductionFrom EverandCorporate Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Advanced Portfolio Management: A Quant's Guide for Fundamental InvestorsFrom EverandAdvanced Portfolio Management: A Quant's Guide for Fundamental InvestorsNo ratings yet

- Aircraft Surface Treatment MarketDocument67 pagesAircraft Surface Treatment Marketkhushboo chandaniNo ratings yet

- AssignmentDocument8 pagesAssignmentAnand sharmaNo ratings yet

- Effortless Excellence: With The World's Fastest Juicing AccessoryDocument2 pagesEffortless Excellence: With The World's Fastest Juicing AccessoryJahanzeb KhanNo ratings yet

- SIP Project ReportDocument6 pagesSIP Project ReportHoney MehrotraNo ratings yet

- Econ Asgment 2Document6 pagesEcon Asgment 2rahmani_4No ratings yet

- Reichard Maschinen, GMBHDocument4 pagesReichard Maschinen, GMBHSasisomWilaiwanNo ratings yet

- Cohesive NounsDocument2 pagesCohesive NounsMr DamphaNo ratings yet

- Homework AssignmentDocument11 pagesHomework AssignmentHenny DeWillisNo ratings yet

- Mains Checklist 545 by Aashish Arora PDFDocument24 pagesMains Checklist 545 by Aashish Arora PDFPratik SachanNo ratings yet

- Chap 001Document37 pagesChap 001falcore316No ratings yet

- Stone World Aug 2010Document104 pagesStone World Aug 2010Alex FilipovNo ratings yet

- 30th Hour PeakDocument18 pages30th Hour PeaksagarstNo ratings yet

- CE Board Problems in Engineering EconomyDocument6 pagesCE Board Problems in Engineering EconomyHomer Batalao75% (4)

- I Preferences and Choice 1Document17 pagesI Preferences and Choice 1shere0002923No ratings yet

- Common Source Amplifier: Experiment Date: 4 October 2011 Name: P.JAGADEESH (11MVD0015)Document11 pagesCommon Source Amplifier: Experiment Date: 4 October 2011 Name: P.JAGADEESH (11MVD0015)alokjadhavNo ratings yet

- Japanese Hippari (Jacket) Design & ConstructionDocument5 pagesJapanese Hippari (Jacket) Design & ConstructionHector Manuel Pereira CastilloNo ratings yet

- Da Study On Financial Statements of A Company in Terms of Liquidity, Solvency and ProfitabilityDocument28 pagesDa Study On Financial Statements of A Company in Terms of Liquidity, Solvency and ProfitabilityatikNo ratings yet

- Biopure FinalDocument22 pagesBiopure FinalNikhil JoyNo ratings yet

- The Role of Small Scale Industries in Nigeria EconomyDocument5 pagesThe Role of Small Scale Industries in Nigeria EconomyDamola AdigunNo ratings yet

- Case Analysis Note - Vanraj TractorsDocument4 pagesCase Analysis Note - Vanraj TractorsKeyur Sampat0% (1)

- Indian Airline Industry: As Service SectorDocument16 pagesIndian Airline Industry: As Service SectorRajesh MishraNo ratings yet

- Bmrcl-hmv-stn-r6-E-17 (r1 & A0) - Hulimavu Station-Dimensional Details of Track Level Superstructure Between Grids 1 and 10Document1 pageBmrcl-hmv-stn-r6-E-17 (r1 & A0) - Hulimavu Station-Dimensional Details of Track Level Superstructure Between Grids 1 and 10Anonymous GoJpm9WbNo ratings yet

- Chakravyuh Business Plan CompetitionDocument5 pagesChakravyuh Business Plan CompetitionNirmal SasidharanNo ratings yet

- Questionnaire For Bank (PNB)Document13 pagesQuestionnaire For Bank (PNB)Abhishek PathakNo ratings yet

- Good Night N All OutDocument1 pageGood Night N All Outraddy13No ratings yet

- Final QuestionsDocument2 pagesFinal QuestionsSyed Muhammad SalmanNo ratings yet

- Boarding & Alighting Time in Ducth Rail Stations - WiggenraadDocument26 pagesBoarding & Alighting Time in Ducth Rail Stations - WiggenraadAsif RehanNo ratings yet

- Negotiations 5 - Clinching The Deal - WorksheetDocument7 pagesNegotiations 5 - Clinching The Deal - WorksheetEley Szponar0% (1)

- Lembar Kerja Mengelola Buku Jurnal: Praktek Akuntansi Keuangan (Manual)Document24 pagesLembar Kerja Mengelola Buku Jurnal: Praktek Akuntansi Keuangan (Manual)Sri UtamiNo ratings yet

- Edie ScarfDocument2 pagesEdie Scarflola lee muchoNo ratings yet