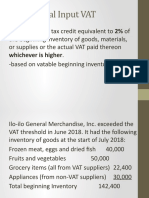

From Ngas To Gam

From Ngas To Gam

Download as pptx, pdf, or txt

You might also like

- Government Accounting SyllabusDocument12 pagesGovernment Accounting SyllabusJean Diane JoveloNo ratings yet

- OPM555 - Assignment 1 - NUR FATMA SYAZANA MOHD HILMI - 2018808652Document11 pagesOPM555 - Assignment 1 - NUR FATMA SYAZANA MOHD HILMI - 2018808652Nur Fatma Syazana Mohd HilmiNo ratings yet

- Government AccountingDocument131 pagesGovernment AccountingAngelo Andro Suan100% (1)

- Nature and Scope of The New Government Accounting SystemDocument16 pagesNature and Scope of The New Government Accounting SystemkmNo ratings yet

- Transitional Input VATDocument21 pagesTransitional Input VATJoanne TolentinoNo ratings yet

- Government AccountingDocument32 pagesGovernment AccountingLaika Mae D. CariñoNo ratings yet

- Accounting For Government DisbursementsDocument12 pagesAccounting For Government DisbursementsMerlina Cuare100% (1)

- CHAPTER 2 - Unified Accounts Code StructureDocument56 pagesCHAPTER 2 - Unified Accounts Code StructureRafael Victoria100% (1)

- Chapter 3 - The Government ProcessDocument48 pagesChapter 3 - The Government ProcessJoyce Candelaria100% (1)

- GovAcc HO No. 3 - The Government Accounting ProcessDocument9 pagesGovAcc HO No. 3 - The Government Accounting Processbobo kaNo ratings yet

- 2020 Dec. MIDTRM EXAM BSA 3A Accounting For Got. NPODocument6 pages2020 Dec. MIDTRM EXAM BSA 3A Accounting For Got. NPOVernn100% (1)

- Manual On Financial Manager of Barangays Module 3Document11 pagesManual On Financial Manager of Barangays Module 3vicsNo ratings yet

- GovAcctg. Modules 1 4 Part1Document58 pagesGovAcctg. Modules 1 4 Part1Sandra Doria100% (1)

- The Government Accounting ProcessDocument24 pagesThe Government Accounting Processyen claveNo ratings yet

- NGAS Illustrative Accounting EntriesDocument9 pagesNGAS Illustrative Accounting EntriesDaniel OngNo ratings yet

- PPSAS and The Revised Chart of AccountsDocument51 pagesPPSAS and The Revised Chart of Accountsmile100% (4)

- NOTESDocument2 pagesNOTESJñelle Faith Herrera SaludaresNo ratings yet

- Revenue and Other Receipts - ScriptDocument30 pagesRevenue and Other Receipts - ScriptChristine Leal-Estender100% (2)

- Obe Course Syllabus TrnstaxDocument4 pagesObe Course Syllabus TrnstaxKenneth Bryan Tegerero TegioNo ratings yet

- MidTerm-Govt.-accounting-RAMOS, ROSEMARIE CDocument12 pagesMidTerm-Govt.-accounting-RAMOS, ROSEMARIE Cagentnic100% (1)

- Philippine Public Sector Accounting Standard 1Document18 pagesPhilippine Public Sector Accounting Standard 1Anonymous bEDr3JhGNo ratings yet

- Module 1: Introduction To Government Accounting and The Philippine Budget ProcessDocument20 pagesModule 1: Introduction To Government Accounting and The Philippine Budget ProcessLaong laan100% (1)

- Chapter 13 - Multiple Choices Problem and Theries KeyDocument15 pagesChapter 13 - Multiple Choices Problem and Theries KeyKryscel ManansalaNo ratings yet

- Chapter 4 Revenues and Other ReceiptsDocument10 pagesChapter 4 Revenues and Other ReceiptsKyree VladeNo ratings yet

- Fair Value (Pfrs 13) :: PAS 41: AgricultureDocument2 pagesFair Value (Pfrs 13) :: PAS 41: AgricultureCzar RabayaNo ratings yet

- Accounting For Disbursements and Related TransactionsDocument12 pagesAccounting For Disbursements and Related TransactionsJustine GuilingNo ratings yet

- The PPSAS and The Revised Chart of Accounts: Tools To Enhance Accountability and Transparency in Financial ReportingDocument98 pagesThe PPSAS and The Revised Chart of Accounts: Tools To Enhance Accountability and Transparency in Financial ReportingJhopel Casagnap EmanNo ratings yet

- UACS NotesDocument5 pagesUACS NotesJamila Zarsuelo100% (2)

- 2010 Illustrative Fs Sme Final Clean New - UnlockedDocument74 pages2010 Illustrative Fs Sme Final Clean New - UnlockedKendall JennerNo ratings yet

- Bases Conversion and Development - RA 7227 PDFDocument17 pagesBases Conversion and Development - RA 7227 PDFRain Rivera RamasNo ratings yet

- TMAP - DOF-BLGF Policy UpdatesDocument35 pagesTMAP - DOF-BLGF Policy UpdatesPena Tn100% (2)

- Chapter 6 Accounting For Income Collections and Related TransactionsDocument3 pagesChapter 6 Accounting For Income Collections and Related TransactionsJapsNo ratings yet

- Ra 9298Document10 pagesRa 9298Abraham Mayo MakakuaNo ratings yet

- Chapter 5 Accounting For Disbursements and Related TransactionsDocument2 pagesChapter 5 Accounting For Disbursements and Related TransactionsJaps100% (1)

- NAME: Joven, Al Vincent M. Acc316/413: Assigned Quiz 1Document2 pagesNAME: Joven, Al Vincent M. Acc316/413: Assigned Quiz 1beeeeeeNo ratings yet

- Government Accounting Manual For National Government AgenciesDocument14 pagesGovernment Accounting Manual For National Government AgenciesKenneth CalzadoNo ratings yet

- GovAcc Quiz AcctgDocument19 pagesGovAcc Quiz AcctgChingNo ratings yet

- Pre-1. Introduction To Government AccountingDocument24 pagesPre-1. Introduction To Government AccountingPaupauNo ratings yet

- Preferential TaxationDocument8 pagesPreferential TaxationAngelica Nicole TamayoNo ratings yet

- IndividualDocument14 pagesIndividualKenneth Bryan Tegerero TegioNo ratings yet

- Government Accounting in The PhilippinesDocument2 pagesGovernment Accounting in The PhilippinesAndyGonzalesAlagar60% (10)

- Government Accounting ReviewDocument6 pagesGovernment Accounting ReviewErwinPaulM.SaritaNo ratings yet

- 01 Introduction and FormationDocument18 pages01 Introduction and Formationm_kobayashiNo ratings yet

- Chapter 2 - The Budget ProcessDocument16 pagesChapter 2 - The Budget Processmaria ronoraNo ratings yet

- The Government Accounting ProcessDocument4 pagesThe Government Accounting ProcessWawex DavisNo ratings yet

- 01 Accounting & Its EnvironmentDocument4 pages01 Accounting & Its EnvironmentRewsEn100% (1)

- Sustainability and Strategic AuditDocument51 pagesSustainability and Strategic AuditEizel Nasol100% (1)

- Government Accounting: Accounting For Non-Profit OrganizationsDocument88 pagesGovernment Accounting: Accounting For Non-Profit OrganizationsDe GuzmanNo ratings yet

- 6 - Notes On Government AccountingDocument6 pages6 - Notes On Government AccountingLabLab ChattoNo ratings yet

- Pfrs Update 2022Document21 pagesPfrs Update 2022Robert CastilloNo ratings yet

- Government AccountingDocument5 pagesGovernment AccountingPrincessa Lopez Masangkay100% (1)

- 2nd Quizzer 1st Sem SY 2020-2021 - AKDocument6 pages2nd Quizzer 1st Sem SY 2020-2021 - AKMitzi WamarNo ratings yet

- Chapter 5 Accounting For Revenue and Other ReceiptsDocument49 pagesChapter 5 Accounting For Revenue and Other ReceiptsKapoy-eeh Lazan100% (1)

- Chapter 03 The Government Accounting ProcessDocument20 pagesChapter 03 The Government Accounting ProcessRygiem Dela CruzNo ratings yet

- Gov Acc 2019 JC AbillonarDocument9 pagesGov Acc 2019 JC AbillonarGabriel PonceNo ratings yet

- Government AccountingDocument10 pagesGovernment AccountingRampotz Ü EchizenNo ratings yet

- Applied AuditingDocument2 pagesApplied Auditingctcasiple67% (3)

- Philippine Government Accounting StandardsDocument9 pagesPhilippine Government Accounting StandardsShien AgucayNo ratings yet

- Special Topics For Self StudyDocument19 pagesSpecial Topics For Self Studychiara uyNo ratings yet

- PART III of The Hand OutsDocument13 pagesPART III of The Hand OutsJudyeast AstillaNo ratings yet

- PART III of The Hand-OutsDocument13 pagesPART III of The Hand-OutsAce Hulsey TevesNo ratings yet

- Authority and ResponsibilityDocument19 pagesAuthority and ResponsibilityAparna100% (1)

- BCC Final Report Quant-Group 12Document17 pagesBCC Final Report Quant-Group 12Rana AbdullahNo ratings yet

- Profile On Acetylene PlantDocument21 pagesProfile On Acetylene Plantاحمد الدلالNo ratings yet

- Inside The Black Box - Revealing The Alternative Beta in Hedge Fund Returns - (J.P. Morgan Asset Management)Document10 pagesInside The Black Box - Revealing The Alternative Beta in Hedge Fund Returns - (J.P. Morgan Asset Management)QuantDev-MNo ratings yet

- C & B Module 1 - Introduction To CompensationDocument15 pagesC & B Module 1 - Introduction To CompensationRuturaj patilNo ratings yet

- Do ETFs Increase Volatilityinternetappendix SSRNDocument145 pagesDo ETFs Increase Volatilityinternetappendix SSRNMy ChangNo ratings yet

- Entrepreneurship in The PhilippinesDocument7 pagesEntrepreneurship in The Philippinesjoanne rivera100% (1)

- 9.jurnal Inter Cost Volume Profit AnalysisDocument10 pages9.jurnal Inter Cost Volume Profit AnalysisNi Made Ayu Nirmalasari Putri ErawanNo ratings yet

- Module - 13 Foreign Exchange Quotations: Cross, Rates, TT Buy/Sell Rates, TC Buy/SellratesDocument12 pagesModule - 13 Foreign Exchange Quotations: Cross, Rates, TT Buy/Sell Rates, TC Buy/SellratesGulshan KumarNo ratings yet

- FINAL Citizens Bank Annual Report 2022-23 FinalDocument206 pagesFINAL Citizens Bank Annual Report 2022-23 FinalNitesh SwarnakarNo ratings yet

- Principles of Marketing Module 3 Quarter 3Document10 pagesPrinciples of Marketing Module 3 Quarter 3Ezrella ValeriaNo ratings yet

- Orasi Ilmiah Engkos Achmad Kuncoro English 24 September 2022 FA NEW 3Document42 pagesOrasi Ilmiah Engkos Achmad Kuncoro English 24 September 2022 FA NEW 3Frog AndskyNo ratings yet

- Employee Retention Project ReportDocument5 pagesEmployee Retention Project Reportpintupal2008No ratings yet

- Invoice OD304363906183876000Document1 pageInvoice OD304363906183876000Lorrenzo Public SchoolNo ratings yet

- Vijay Solvex LTDDocument5 pagesVijay Solvex LTDManish SinghNo ratings yet

- Income Tax Ordinance 1984 - Amended Upto July 2022Document382 pagesIncome Tax Ordinance 1984 - Amended Upto July 2022Sumit GNo ratings yet

- 5 ProcessesDocument56 pages5 Processeshayder nuredinNo ratings yet

- TAX.3404 Withholding TaxesDocument13 pagesTAX.3404 Withholding TaxesJUARE MaxineNo ratings yet

- HRM Short NotesDocument5 pagesHRM Short NotesTitus ClementNo ratings yet

- Health Economics SupplyDocument7 pagesHealth Economics SupplyPao C EspiNo ratings yet

- KFC I - Full Text-09-02-2016Document538 pagesKFC I - Full Text-09-02-2016RajeshNo ratings yet

- Revival and Restructuring of Sick CompaniesDocument10 pagesRevival and Restructuring of Sick Companiessudhir.kochhar3530No ratings yet

- Combine PDFDocument21 pagesCombine PDFW-304-Bautista,PreciousNo ratings yet

- Calculative Questions - Chapter 10 Measuring A Nations IncomeDocument13 pagesCalculative Questions - Chapter 10 Measuring A Nations IncomePhuong Vy PhamNo ratings yet

- EFETBooklet Towards ASingle European Energy Market Jan 13 Reduced SizeDocument20 pagesEFETBooklet Towards ASingle European Energy Market Jan 13 Reduced SizeSlaven IvanovicNo ratings yet

- Chapter Five: Environmental Analysis and Strategic UncertaintyDocument15 pagesChapter Five: Environmental Analysis and Strategic UncertaintySoniya ZahidNo ratings yet

- Entrepreneurship Development: Presented by Prof.B.ManchandaDocument31 pagesEntrepreneurship Development: Presented by Prof.B.ManchandaAkshat AgarwalNo ratings yet

- The Effect of Changes in Foreign Exchange RateDocument8 pagesThe Effect of Changes in Foreign Exchange RateRafael Capunpon VallejosNo ratings yet