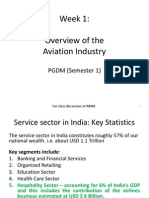

Aviation Industry

Aviation Industry

Download as pptx, pdf, or txt

You might also like

- Navblue Specification and LegendDocument166 pagesNavblue Specification and LegendDhega Noor Aji100% (5)

- Case Study:: Singapore Airlines - The India DecisionDocument27 pagesCase Study:: Singapore Airlines - The India DecisionCon Fluence100% (2)

- Corporate Strategy PDFDocument27 pagesCorporate Strategy PDFaryan singhNo ratings yet

- KF Airline PESTEL AnalysisDocument16 pagesKF Airline PESTEL Analysisbrij_jeshNo ratings yet

- Aviation Industry and Its ChallengesDocument19 pagesAviation Industry and Its ChallengesDinesh Pal100% (1)

- Introduction of Aviation SectorDocument15 pagesIntroduction of Aviation Sectorpoojapatil90No ratings yet

- Portfolio Analysis Airline Industry - Group 4 - Section C - SM2 Project PDFDocument27 pagesPortfolio Analysis Airline Industry - Group 4 - Section C - SM2 Project PDFroguembaNo ratings yet

- STP Strategy Analysis: SegmentationDocument8 pagesSTP Strategy Analysis: SegmentationAnkit KumarNo ratings yet

- Faa Airframe Handbook PDFDocument2 pagesFaa Airframe Handbook PDFPaige100% (2)

- Airline IndustryDocument57 pagesAirline IndustryAchal_jainNo ratings yet

- Kingfisher Airlines .T He King of Good Times: by Shruti Bhatia, IILM Lodhi RoadDocument16 pagesKingfisher Airlines .T He King of Good Times: by Shruti Bhatia, IILM Lodhi RoadSurbhi MehtaNo ratings yet

- Presentation MarketingDocument31 pagesPresentation MarketingBaskerbasNo ratings yet

- Kingfisher AirlineDocument15 pagesKingfisher AirlinegajenderiipmNo ratings yet

- Kingfisher Airlines .The King of Good TimesDocument15 pagesKingfisher Airlines .The King of Good TimesArvind SharmaNo ratings yet

- Aviation IndustryDocument32 pagesAviation IndustryMayank JoshiNo ratings yet

- Aviation IdustryDocument40 pagesAviation IdustryGourav BhattacharjeeNo ratings yet

- Indian Aviation IndustryDocument30 pagesIndian Aviation IndustryHumair ShaheenNo ratings yet

- Aviation Presentation 2003Document15 pagesAviation Presentation 2003tpanchal2009No ratings yet

- Aviation in India (Rev PPT 2)Document30 pagesAviation in India (Rev PPT 2)Akshay ThaparNo ratings yet

- Airline IndustryDocument21 pagesAirline IndustryAmeya VengurlekarNo ratings yet

- Challenges of Indian Aviation Industry in Chaotic Phase: Rajesh U. KantheDocument3 pagesChallenges of Indian Aviation Industry in Chaotic Phase: Rajesh U. KanthePratham MittalNo ratings yet

- Aviation Industry in IndiaDocument20 pagesAviation Industry in IndiaNikhil KasatNo ratings yet

- Indian Airline Industry AnalysisDocument15 pagesIndian Airline Industry Analysisekta_1011No ratings yet

- Jet Airways - Strategy MGMTDocument93 pagesJet Airways - Strategy MGMTShubha Brota Raha100% (2)

- Impact of B.E On Airline Industry: Presented By, Devu V Ii Sem Mba ICM-IMK, PoojapuraDocument14 pagesImpact of B.E On Airline Industry: Presented By, Devu V Ii Sem Mba ICM-IMK, PoojapuraSiva PrakashNo ratings yet

- Etop-1st Assignment of Azhar Susheel Rohan RohitDocument30 pagesEtop-1st Assignment of Azhar Susheel Rohan Rohitazharmohd0% (1)

- The Airline IndustryDocument61 pagesThe Airline IndustryManash VermaNo ratings yet

- Aviataion Industry: Ajay Pal Kunal Singh Manali Vende Snehal Katvi Supriya Singh Vivek SinghDocument19 pagesAviataion Industry: Ajay Pal Kunal Singh Manali Vende Snehal Katvi Supriya Singh Vivek SinghSupriya SinghNo ratings yet

- Industry Analysis Project Aviation INDUSTRY: Submitted To: Director Dr. Dinesh D. HarsolekarDocument23 pagesIndustry Analysis Project Aviation INDUSTRY: Submitted To: Director Dr. Dinesh D. Harsolekarvinayak1scribdNo ratings yet

- Jet AirwaysDocument11 pagesJet AirwaysAnonymous tgYyno0w6No ratings yet

- Final JET Vs KinfisherDocument22 pagesFinal JET Vs Kinfisherkaushik100% (2)

- Airline IndustryDocument37 pagesAirline IndustrySudhakar TummalaNo ratings yet

- Aviation InsuranceDocument25 pagesAviation InsuranceratidwivediNo ratings yet

- Reforms in Aviation SectorDocument36 pagesReforms in Aviation SectorpassionpecNo ratings yet

- Singapore Airlines-Case Discussion: Kharthik Narayanan, Somyadeep Mandal, Monica, Sheryn Samson, Parul, LakshmipriyaDocument9 pagesSingapore Airlines-Case Discussion: Kharthik Narayanan, Somyadeep Mandal, Monica, Sheryn Samson, Parul, LakshmipriyaKharthik NarayananNo ratings yet

- Arline Industry: Appicaion of Business Analytics and Intelligence in Airline IndustryDocument51 pagesArline Industry: Appicaion of Business Analytics and Intelligence in Airline IndustryNeel LakdawalaNo ratings yet

- Indian Airline IndustryDocument37 pagesIndian Airline IndustryNazish Sohail100% (1)

- CSEB3101 Strategic Management: Lecturer: DR Tey Lian Seng Case PresentationDocument62 pagesCSEB3101 Strategic Management: Lecturer: DR Tey Lian Seng Case PresentationwendryNo ratings yet

- Managerial Economics - Mudita & PallaviDocument15 pagesManagerial Economics - Mudita & PallaviMuditaNimje100% (1)

- Airline Industry: Mayank RanjanDocument35 pagesAirline Industry: Mayank RanjanMayank RanjanNo ratings yet

- Indian Aviation IndustryDocument30 pagesIndian Aviation IndustryRaj MalhotraNo ratings yet

- Service Marketing MixDocument5 pagesService Marketing MixDeepak SantNo ratings yet

- Aviation Industry IndiaDocument16 pagesAviation Industry IndiaPandey NeetaNo ratings yet

- Industry Analysis Project (Indigo)Document30 pagesIndustry Analysis Project (Indigo)amar82% (11)

- Type The Document SubtitleDocument17 pagesType The Document Subtitlebansal_gctiNo ratings yet

- Final Analysis On Aviation Sector in IndiaDocument29 pagesFinal Analysis On Aviation Sector in IndiaKinchit PandyaNo ratings yet

- Airline Industry: Service Sector ManagementDocument37 pagesAirline Industry: Service Sector ManagementMahesh AnbalaganNo ratings yet

- Industry Analysis Report ... Aviation IndustryDocument36 pagesIndustry Analysis Report ... Aviation Industrybalaji bysani100% (1)

- Indian Airports - Global Landing GroundDocument44 pagesIndian Airports - Global Landing Groundhh.deepakNo ratings yet

- Aviataion Industry: Presented By: Ajay Pal Kunal Singh (MMS) Manali Vende Snehal Katvi Supriya Singh Vivek SinghDocument51 pagesAviataion Industry: Presented By: Ajay Pal Kunal Singh (MMS) Manali Vende Snehal Katvi Supriya Singh Vivek SinghSupriya SinghNo ratings yet

- Lecturer: DR Tey Lian Seng Case Presentation:: CSEB3101 Strategic ManagementDocument62 pagesLecturer: DR Tey Lian Seng Case Presentation:: CSEB3101 Strategic ManagementwendryNo ratings yet

- Air Charters: The Path Ahead: Amrita Krishnan Himanshu Arora Jatin Bhatia Kaveri Ghosh Pallavi Radhika KapoorDocument31 pagesAir Charters: The Path Ahead: Amrita Krishnan Himanshu Arora Jatin Bhatia Kaveri Ghosh Pallavi Radhika KapoorHimanshu AroraNo ratings yet

- Air Deccan Implementing The Low-Cost Model in India: AbstractDocument22 pagesAir Deccan Implementing The Low-Cost Model in India: AbstractTanmoy GhosalNo ratings yet

- 1st PresentationDocument24 pages1st PresentationMadhu KumariNo ratings yet

- Air Blue ProjectDocument50 pagesAir Blue Projectsyed usman wazir92% (13)

- Indian Aviation Sector: Presented By: Lijo Sarangi Diksha MeenalDocument17 pagesIndian Aviation Sector: Presented By: Lijo Sarangi Diksha MeenalSarangi UthamanNo ratings yet

- Higher Than The Blue SkiesDocument1 pageHigher Than The Blue SkiesPushkar HatéNo ratings yet

- Cruising to Profits, Volume 1: Transformational Strategies for Sustained Airline ProfitabilityFrom EverandCruising to Profits, Volume 1: Transformational Strategies for Sustained Airline ProfitabilityNo ratings yet

- Indian Labour LawsDocument4 pagesIndian Labour LawsiamgodrajeshNo ratings yet

- Human Resource Information SystemDocument45 pagesHuman Resource Information Systemvigneshsw100% (2)

- Human Resource Information SystemDocument45 pagesHuman Resource Information Systemvigneshsw100% (2)

- Comparing Cloud Computing and Grid ComputingDocument15 pagesComparing Cloud Computing and Grid ComputingRajesh RaghavanNo ratings yet

- Micro EconomicsDocument28 pagesMicro EconomicsThomas SilombaNo ratings yet

- Fundamentals of MarketingDocument85 pagesFundamentals of Marketingbatra_rahul88100% (5)

- Admission Information HandoutDocument6 pagesAdmission Information HandoutRajesh RaghavanNo ratings yet

- Flight Attendance Vocab. BookletDocument6 pagesFlight Attendance Vocab. Bookletإيهاب غازيNo ratings yet

- Aviation Aftermarket Defense Winter 2010-11Document76 pagesAviation Aftermarket Defense Winter 2010-11Jacob Jack Yosha100% (1)

- Fig Whiteboard If CuDocument1 pageFig Whiteboard If Cuhenry okilaNo ratings yet

- L.N - Am&cm - Unit - 1Document15 pagesL.N - Am&cm - Unit - 1Nambi RajanNo ratings yet

- Travel Reservation February 27 For MS WIDAD BERRADADocument2 pagesTravel Reservation February 27 For MS WIDAD BERRADAFarok fozyNo ratings yet

- Southwest SWOTDocument10 pagesSouthwest SWOTdrgovandeNo ratings yet

- Roundel 1951-10 Vol 3 No 10Document52 pagesRoundel 1951-10 Vol 3 No 10TateNo ratings yet

- Infographic A220 FamilyDocument1 pageInfographic A220 Familyromanduffort.lyaNo ratings yet

- Qantas Pilot Jokes and Funny Engineer Reports PDFDocument5 pagesQantas Pilot Jokes and Funny Engineer Reports PDFdnadie7No ratings yet

- Hawker 400XP-Beechjet 400A MTM Vol 1Document685 pagesHawker 400XP-Beechjet 400A MTM Vol 1AVIATION TRAINING CENTER SC75% (4)

- TTM Single Aisle Line & Base Ata 31Document512 pagesTTM Single Aisle Line & Base Ata 31林至伟No ratings yet

- SBKP - Rnav Gnss y Rwy 33 - Iac - 20141016 PDFDocument1 pageSBKP - Rnav Gnss y Rwy 33 - Iac - 20141016 PDFLuis Gustavo FavarettoNo ratings yet

- HondaJet SpecificationsDocument5 pagesHondaJet SpecificationsJohn Jennings100% (1)

- SQ32 (SIA32) Singapore Airlines Flight Tracking and History - FlightAwareDocument1 pageSQ32 (SIA32) Singapore Airlines Flight Tracking and History - FlightAwareSamppa MitraNo ratings yet

- A320 NE0 Fuel or Hydraulic or Oil Leakage LimitsDocument19 pagesA320 NE0 Fuel or Hydraulic or Oil Leakage LimitsArjuna SamaranayakeNo ratings yet

- Easa Pad 19-209 1Document4 pagesEasa Pad 19-209 1cf34No ratings yet

- A Seminar Report On Concorde.Document20 pagesA Seminar Report On Concorde.Ashok Kumar100% (1)

- Q 400 Avionics CAA ExamDocument3 pagesQ 400 Avionics CAA ExambernabasNo ratings yet

- WD18LHDocument1 pageWD18LHshahin jayaNo ratings yet

- Final Report OMNI WING AIRCRAFTDocument51 pagesFinal Report OMNI WING AIRCRAFTPrithvi AdhikaryNo ratings yet

- Flying Scale Models Issue 167 2013-10Document68 pagesFlying Scale Models Issue 167 2013-10PeterNo ratings yet

- Personnel Licensing: Cover Sheet To Amendment 169-BDocument38 pagesPersonnel Licensing: Cover Sheet To Amendment 169-BMohammad NorouzzadehNo ratings yet

- Casa ZburatoareDocument11 pagesCasa ZburatoareBrandy RomanNo ratings yet

- Final Year Project Report Latest VersionDocument60 pagesFinal Year Project Report Latest VersionJames Dunthorne75% (4)

- Chapter 1 - Raymer - Design PDFDocument2 pagesChapter 1 - Raymer - Design PDFCris M Rodríguez BNo ratings yet

- Air Asia India: Clash For The Indian Skies by X1Document11 pagesAir Asia India: Clash For The Indian Skies by X1Maithily SivabalanNo ratings yet

- DCS P-51D 1.1.2.1 Default Keyboard Bindings: Modifier Notation DebugDocument4 pagesDCS P-51D 1.1.2.1 Default Keyboard Bindings: Modifier Notation DebuglkjsdflkjNo ratings yet