Integrated Test Facility

- 2. DEFINITION An automated, on-going technique that enables the auditor to test an application’s logic and controls during its normal operation.

- 3. PURPOSE To audit an AIS in an operational setting

- 4. AUDITOR’S ROLE To examine results of transaction processing to find out how well the AIS does the tasks required of it.

- 5. 13 – 5 Transactions ITF transactions Computer application system Reports containing ITF information Reports without ITF data Data files ITF data INTEGRATED TEST FACILITY

- 6. ADVANTAGES

- 7. 1 2 3 4 ADVANTAGES Supports continuous monitoring of controls.

- 8. 1 2 3 4 ADVANTAGES Economically tested without disrupting the user’s operations and without the intervention of computer services personnel.

- 9. 1 2 3 4 ADVANTAGES Testing can be unscheduled and unknown to other staff.

- 10. 1 2 3 4 ADVANTAGES It provides prima facie evidence of correct program functions.

- 11. DISADVANTAGE The potential of corrupting data files with test data that may end up in the financial reporting process.

- 12. 1 2 3 4 5 INTEGRATED TEST FACILITY Common form of an ITF is as follows:

- 13. INTEGRATED TEST FACILITY 1 2 3 4 5 Common form of an ITF is as follows: A dummy ITF center is created for the auditors.

- 14. INTEGRATED TEST FACILITY 1 2 3 4 5 Common form of an ITF is as follows: Auditors create transactions for controls they want to test.

- 15. INTEGRATED TEST FACILITY 1 2 3 4 5 Common form of an ITF is as follows: Working papers are created to show expected results from manually processed information.

- 16. INTEGRATED TEST FACILITY 1 2 3 4 5 Common form of an ITF is as follows: Auditor transactions are run with actual transactions.

- 17. INTEGRATED TEST FACILITY 1 2 3 4 5 Common form of an ITF is as follows: Auditors compare ITF results to working papers.

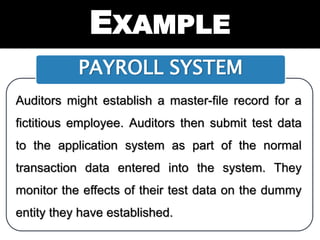

- 18. EXAMPLE PAYROLL SYSTEM Auditors might establish a master-file record for a fictitious employee. Auditors then submit test data to the application system as part of the normal transaction data entered into the system. They monitor the effects of their test data on the dummy entity they have established.

- 19. ACTIVITY 1.How does an ITF works? 2.Cite an advantage and a disadvantage of ITF

Editor's Notes

- © Copyright Showeet.com

- © Copyright Showeet.com

- © Copyright Showeet.com

- © Copyright Showeet.com

- © Copyright Showeet.com

- © Copyright Showeet.com

- © Copyright Showeet.com

- © Copyright Showeet.com

- © Copyright Showeet.com

- © Copyright Showeet.com

- © Copyright Showeet.com

- © Copyright Showeet.com

- © Copyright Showeet.com

- © Copyright Showeet.com

- © Copyright Showeet.com

- © Copyright Showeet.com

- © Copyright Showeet.com

- © Copyright Showeet.com