Regulatory Restructuring

•Download as PPT, PDF•

0 likes•280 views

Analysis and explanation of Obama administration regulatory restructuring plan for banks and financial institutions

Report

Share

Regulatory Restructuring

- 1. The Banking Crisis and Regulatory Restructuring July 24, 2009

- 2. Financial Crisis It can fairly be said that the chain of catastrophic bets made over the past decade by a few hundred bankers may well turn out to be the greatest nonviolent crime against humanity in history. They’ve brought the world’s economy to its knees, lost tens of millions of people their jobs and their homes, and trashed the retirement plans of a generation, and they could drive an estimated 200 million people worldwide into dire poverty…Bankers are now thought of as Paris Hilton in pinstripes—showy, thoughtless souvenirs of an age and a culture we wish to forget. – Graydon Carter, Editor, Vanity Fair , June 2009

- 3. Financial Crisis Minimum value of governmental bailouts of the global financial industry since 2007, per capita, worldwide: $1,250 Amount this represents as a percentage of the median annual income worldwide: 39

- 4. Financial Crisis Estimated total amount that world financial institutions will write off by 2010, according to the IMF: $4,100,000,000,000 Portion of these bad loans and securities that originated in the U.S.: 2/3 Percentage of rich Americans who say they have “lost faith in the integrity of financial service institutions: 64

- 5. Home Business News Markets Personal Finance Retirement Technology Luxury Small Business Fortune Video My Portfolio CNN.com Column Archive SPECIAL REPORT Road to Rescue Where the banks are failing Bank failures - many caused by foreclosures - keep mounting. Where it helps: Stimulus and jobs Where the money is going: Stimulus and state deficits US Indexes Fortune 500 Movers July 14, 2009 4:03 PM ET Jul 14 3:56pm ET † Sponsored by s ymbol lookup © 2009 Cable News Network. A Time Warner Company. All Rights Reserved. Terms under which this service is provided to you. Privacy Policy Home Portfolio Calculators Contact Us Newsletters Podcasts RSS Mobile Widgets Site Map User Preferences Advertise with Us Magazine Customer Service Download Fortune Lists Reprints Career Opportunities Special Sections Conferences Business Leader Council Live Quotes automatically refresh, but individual equities are delayed 15 minutes for Nasdaq, and 20 minutes for other exchanges. Market indexes are shown in real time, except for the DJIA, which is delayed by two minutes. All times are ET. * : Time reflects local markets trading time. † - Intraday data delayed 15 minutes for Nasdaq, and 20 minutes for other exchanges. Disclaimer Home Business News Markets Personal Finance Retirement Technology Luxury Small Business Fortune Video My Portfolio CNN.com Column Archive SPECIAL REPORT Road to Rescue Where the banks are failing Bank failures - many caused by foreclosures - keep mounting. Where it helps: Stimulus and jobs Where the money is going: Stimulus and state deficits US Indexes Fortune 500 Movers July 14, 2009 4:03 PM ET Jul 14 3:56pm ET † Sponsored by s ymbol lookup © 2009 Cable News Network. A Time Warner Company. All Rights Reserved. Terms under which this service is provided to you. Privacy Policy Home Portfolio Calculators Contact Us Newsletters Podcasts RSS Mobile Widgets Site Map User Preferences Advertise with Us Magazine Customer Service Download Fortune Lists Reprints Career Opportunities Special Sections Conferences Business Leader Council Live Quotes automatically refresh, but individual equities are delayed 15 minutes for Nasdaq, and 20 minutes for other exchanges. Market indexes are shown in real time, except for the DJIA, which is delayed by two minutes. All times are ET. * : Time reflects local markets trading time. † - Intraday data delayed 15 minutes for Nasdaq, and 20 minutes for other exchanges. Disclaimer Subscribe to Fortune Make CNNMoney my Homepage Add to Favorites -0.002 1 euro = $1.396 U.S.Dollar Yield: 3.48% 97 2/32 10-year Bond 4.78 / 0.53% 905.84 S&P 500 6.52 / 0.36% 1,799.73 Nasdaq 27.81 / 0.33% 8,359.49 Dow Jones Change Last Markets 13.79% 0.66 Blockbuster Inc -14.37% 12.10 Health Net Inc 17.78% 1.59 CIT Group Inc 37.40% 1.15 General Motors Corp % Change Price Company Copyright © 2009 BigCharts.com Inc. All rights reserved. Please see our Terms of Use . MarketWatch, the MarketWatch logo, and BigCharts are registered trademarks of MarketWatch, Inc. Intraday data provided by Interactive Data Real-Time Services and subject to the Terms of Use . Intraday data is at least 20-minutes delayed. All times are ET. Historical, current end-of-day data, and splits data provided by Interactive Data Pricing and Reference Data . Fundamental data provided by Morningstar, Inc. . SEC Filings data provided by Edgar Online Inc. . Earnings data provided by FactSet CallStreet, LLC. Privacy Policy Subscribe to Fortune Make CNNMoney my Homepage Add to Favorites -0.002 1 euro = $1.396 U.S.Dollar Yield: 3.48% 97 2/32 10-year Bond 4.78 / 0.53% 905.84 S&P 500 6.52 / 0.36% 1,799.73 Nasdaq 27.81 / 0.33% 8,359.49 Dow Jones Change Last Markets 13.79% 0.66 Blockbuster Inc -14.37% 12.10 Health Net Inc 17.78% 1.59 CIT Group Inc 37.40% 1.15 General Motors Corp % Change Price Company Copyright © 2009 BigCharts.com Inc. All rights reserved. Please see our Terms of Use . MarketWatch, the MarketWatch logo, and BigCharts are registered trademarks of MarketWatch, Inc. Intraday data provided by Interactive Data Real-Time Services and subject to the Terms of Use . Intraday data is at least 20-minutes delayed. All times are ET. Historical, current end-of-day data, and splits data provided by Interactive Data Pricing and Reference Data . Fundamental data provided by Morningstar, Inc. . SEC Filings data provided by Edgar Online Inc. . Earnings data provided by FactSet CallStreet, LLC. Privacy Policy

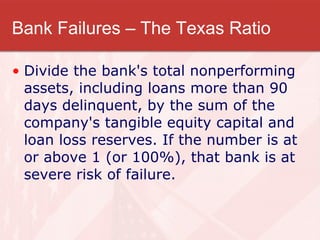

- 6. Bank Failures – The Texas Ratio Divide the bank's total nonperforming assets, including loans more than 90 days delinquent, by the sum of the company's tangible equity capital and loan loss reserves. If the number is at or above 1 (or 100%), that bank is at severe risk of failure.

- 7. Financial Crisis Inquiry Commission Will investigate 20+ specific areas related to the financial crisis fraud and abuse state and federal regulatory enforcement tax treatment of financial products credit rating agencies lending practices Securitization unregulated financial products corporate governance executive compensation. The commission will also examine the causes that made major financial institutions fail or likely to fail had they not received exceptional government assistance.

- 9. Too Big To Fail Federal Reserve Becomes the systemic risk regulator for large and interconnected financial firms Large, interconnected firms as well as their parents and subsidiaries would be subject to heightened capital, liquidity, and risk management standards. The Federal Reserve would also gain the power to supervise systemically important payment, clearing, and settlement systems.

- 10. Too Big To Fail Systemic Risk Council Facilitates coordination of policy and resolution of disputes, and identify emerging risks in firms and market activities. Chaired by the Secretary of the Treasury and made up of the heads of the principal financial regulators. Would have the power to gather information from any financial firm in order to identify emerging systemic risks. Gives the Dept. of Treasury resolution authority over non-bank financial institutions that pose systemic risk.

- 11. Regulatory Consolidation Consolidates the Office of the Comptroller of the Currency (“OCC”) and the Office of Thrift Supervision (“OTS”) into a single regulator, the National Bank Supervisor (“NBS”) Eliminates the federal thrift charter Removes obstacles to interstate branching by national and state banks.

- 12. New Consumer Protection Agency Would regulate all consumer financial products and services and the institutions that provide them. The CFPA would require that disclosure forms are clear and that consumers are offered simple and fair financial products. Currently, many consumer regulations are issued jointly by the Federal Reserve, NCUA, FDIC, OCC, OTS and state agencies.

- 13. Hedge Funds Require advisers to hedge funds and private pools of capital to register with the Securities and Exchange Commission (“SEC”) and impose recordkeeping, disclosure, and reporting requirements on the funds they advise.

- 14. Securities Keep the Commodity Futures Trading Commission (“CFTC”) and SEC as separate entities, but harmonize the regulation of futures and securities by creating uniform principles of regulation, and subject all over-the-counter (“OTC”) derivatives to comprehensive regulation.

- 15. Securitization Market Requires loan originators to retain a five percent interest in the risk of securitized credit exposures, imposing reporting requirements on issuers of asset-backed securities, and reducing regulator reliance on credit rating agencies. Strengthens regulation of credit rating agencies

- 16. Insurance Establish an Office of National Insurance (“ONI”) within the Treasury to gather information and coordinate policy in the insurance sector.

Editor's Notes

- Harper’s Index, copyright 2009, All Rights Reserved.

- Note- not necessarily the FDIC.

- Issue here is whether this is the first step towards eliminating the state bank charter.

- Would regulate products such as credit cards and mortgages. It would enforce measures such as Truth in Lending Act and the Real Estate Settlement and Procedures Act. The FPSC would function much like the Consumer Product Safety Commission, a watchdog agency created in 1972 to protect consumers from unsafe products. The idea behind the legislation [i ] is that when applying for a credit card or obtaining a loan, consumers should not have to understand the intricate details, just as they do not need to understand how a toaster works; the Commission would protect consumers from risky financial products by, among other matters, alleviating the need for them to understand the fine print in financial instruments and disclosures. In many ways, the bill reflects an attempt to create overarching standards of consumer fairness across the existing series of discrete laws that apply to different products and services. A key question will be how these new standards would be integrated into the existing regulatory framework applicable to the many industries to which it would apply. If enacted, the proposed legislation will dramatically affect the consumer finance industry. The FPSC would have authority to heavily regulate financial products and services, and violations of its rules could result in criminal liability.

- The proposal also calls for strengthening the regulation of credit rating agencies. Credit rating agencies would be required to have robust policies and procedures that manage and disclose conflicts of interest, differentiate between structured and other products, and otherwise promote the integrity of the ratings process. Regulators would also be required to reduce their reliance on credit ratings in regulations and supervisory practices. Such a change would impact net capital rules for broker-dealers, risk-based capital requirements for banks, eligibility requirements for securities that can be owned by money market mutual funds, and eligibility to register certain debt securities using a shelf registration statement. To the extent risk-based regulatory capital rules would continue to rely on credit ratings, those rules would account for the risk of structured credit products, including the concentrated systematic risk of senior tranches and re-securitizations and the risk of exposures held in highly leveraged off-balance sheet vehicles. These changes would be closely tied to the proposed increases in regulatory capital requirements on highly rated ABS.

- The proposal’s treatment of the insurance industry is paradoxical. It laments the weaknesses of regulating insurance at the state level and indicates a strong preference for federal regulation of insurance, but it fails to call for an end to state regulation in whole or in part. Instead, it proposes to create the ONI within Treasury, which would have the power to gather information, identify weaknesses, and coordinate policy throughout the insurance industry. The ONI would also have the power to negotiate international agreements and “speak with one voice” on behalf of the U.S. insurance industry.