9. Basel II Presentation

Download as PPTX, PDF1 like797 views

Basel II has three pillars and aims to better align capital requirements with risks. Pillar 1 updates minimum capital requirements to use more risk-sensitive approaches for credit, market, and operational risk. Pillar 2 requires banks and supervisors to review risk management and capital adequacy. Pillar 3 promotes market discipline through disclosure. Vietnam is implementing Basel II in phases, with the goal of fully adopting the three pillar framework by 2018 to strengthen its banking system.

1 of 14

Downloaded 14 times

Recommended

Overview of basel 2 by s k mishra cbi

Overview of basel 2 by s k mishra cbiV R Iyer This document provides an overview of Basel II. It discusses what risks are and how they are inherent in banking. It notes that Basel II aims to improve on Basel I by taking a more risk-sensitive approach to determining capital requirements. It addresses key aspects of Basel II such as calculating capital needs based on aggregated risk, incentivizing higher quality assets with lower risk weights, and addressing operational risk which Basel I did not cover. The document provides background on the Basel Committee and why Basel I was introduced following bank failures to promote international banking regulation standards.

Basel 2

Basel 2vinaya.hs Basel II aims to establish a more risk-sensitive approach to capital adequacy by addressing three main areas or pillars: minimum capital requirements, supervisory review, and market discipline. It requires banks to hold capital reserves proportional to their credit, market, and operational risk. The framework allows two approaches for calculating credit risk - a standardized approach and internal ratings-based approaches. Pillar 2 covers supervisory review to ensure banks have adequate capital for all risks and encourage better risk management. Pillar 3 focuses on market discipline through public disclosures.

Us fsap stress testing wrap up 03 03-15 - redacted version

Us fsap stress testing wrap up 03 03-15 - redacted versionBenjamin Huston Presentation co-delivered with US FSAP stress testing technical to conclude the 2015 US FSAP stress testing exercise.

Operational Risk & Basel Ii

Operational Risk & Basel Iijhsiddiqi2003 The document discusses operational risk and Basel II regulations. It defines operational risk as losses from internal failures or external events. It outlines the three pillars of Basel II which establish minimum capital requirements, supervisory review, and market discipline. It describes the different approaches for calculating operational risk capital charges, including the Basic Indicator Approach, Standardized Approach, and Advanced Measurement Approach.

Financial Risk Management Framwork & Basel Ii Icmap

Financial Risk Management Framwork & Basel Ii Icmapjhsiddiqi2003 Javed H Siddiqi discusses risk management and the Basel Accords. The document covers:

1) An overview of risk management, including definitions of risk, the risk management process, and assessing risk tolerance.

2) A summary of the Basel I accord, including how it calculated regulatory capital requirements for credit and market risk.

3) An overview of the Basel II accord, which introduced approaches for calculating capital for operational risk and made capital requirements more risk sensitive.

Risk management in e banking

Risk management in e bankingAmer Mushtaq This document discusses risk management in e-banking. It defines e-banking and describes the main risks, including operational risk from failures and fraud, credit risk from counterparties, reputational risk from negative publicity, and legal risk from legal issues. It provides details on how to manage these risks, such as establishing proper processes, oversight, controls, and incident response plans to limit liability and ensure continuity of e-banking services.

Operational risk (by ms.sweta vijuraj)

Operational risk (by ms.sweta vijuraj)Saras Singh This document discusses operational risk management. It begins by defining risk management and the types of risks, including operational risk. It then discusses why operational risk management is important, highlighting some significant operational risk events. It describes tools for identifying and monitoring operational risk, such as loss data collection, risk and control self-assessments, and key risk indicators. It also discusses approaches for measuring operational risk capital requirements under Basel II and III, including the basic indicator approach, standardized approach, and advanced measurement approach. Finally, it notes some challenges in measuring operational risk and ways to mitigate and control operational risk exposures.

Risk based supervision in private and public sector banks in India,

Risk based supervision in private and public sector banks in India,Pravas Ranjan Mahapatra This document discusses risk management in the banking sector. It identifies four main types of risks that banks face: operational risk, credit risk, market risk, and regulatory risk. For each risk, it provides examples of the specific risks involved. It also discusses how risk management in banks has evolved from a focus on risk reduction to treating risk as an inherent part of the business that must be monitored. Regulatory responses aimed at improving risk management in the financial industry are also summarized.

Operational Risk Management under BASEL era

Operational Risk Management under BASEL eraTreat Risk Operational risk have always ignored by Banks as they thought Credit and market risks can cause catastrophe. But history of misfortunes taught us different lessons. Controls and internal audit have long been construed as guard till BASEL II dictates forced banks to look with insight. Understand the dimension of ORM in this presentation.

Credit risk management presentation

Credit risk management presentationharsh raj This presentation provides complete study ofcredit risk management,how it was performed in yester years ,how it is taken care nowadays and what is the road ahead in future

Operational risk ppt

Operational risk pptNehaKamboj10 OPERATIONAL RISK, CLASSIFICATION OF OPERATIONAL RISK, OPERATIONAL RISK MANAGEMENT(ORM), principles & policies, ROLE OF OPERATIONAL RISK MANAGEMENT

Risk Management in Banking Sectors.

Risk Management in Banking Sectors.Rupesh neupane Risk Management in Banking Sectors:

This side is helps to analyse the risk management in banking sectors.

SD Basel process automation seminar presentation

SD Basel process automation seminar presentationsarojkdas The document discusses key considerations for financial institutions in establishing a sustainable process for automating Basel III capital adequacy requirements. It emphasizes the need for a golden source of data, unified data management, and computational flexibility to implement complex models and regulatory changes. A reference information architecture is proposed with shared ownership of data and active collaboration between risk, finance, regulatory, and IT functions. Effective data governance and change management processes are necessary to ensure ongoing validity, consistency and completeness of data.

Operational Risk Management Oct 4

Operational Risk Management Oct 4av vedpuriswar This document discusses operational risk management in banks. It covers typical bank organizational structures including front, middle, and back offices. It describes key operational risk types like fraud, system failures, and processing errors. It also discusses operational risk management strategies such as risk mapping, indicators, qualitative assessments, and statistical approaches to quantify unexpected losses from operational risks.

Operational Risk Management

Operational Risk Managementarsqureshi The document discusses operational risk and provides guidance on defining, identifying, measuring, monitoring, controlling, and mitigating operational risk according to the Basel Committee on Banking Supervision. It addresses issues with operational risk loss data and outlines principles for developing an appropriate operational risk management environment, process, and framework. The document also examines challenges with using internal and external loss data for quantifying operational risk capital requirements.

OFSAA-ALM

OFSAA-ALMsailajasatish The document discusses asset liability management (ALM) in banking. It covers several key topics in 3 paragraphs:

1) ALM refers to managing a bank's balance sheet to allow for different interest rate and liquidity scenarios. This involves assessing risks from changes in interest rates, exchange rates, and liquidity. ALM aims to quantify these risks and provide strategies to make credit, interest, and liquidity risks acceptable.

2) Common ALM techniques include gap analysis, duration analysis, scenario analysis, simulation, and value-at-risk to measure risks. Interest rate risk is a major focus, and tools like gap and duration analysis examine how changes in rates impact profits and asset values.

3)

Risk management basel ii

Risk management basel iiUjjwal 'Shanu' The weekly VAR(10%) is $27,951

VAR(10%)20-days(monthly) = 12,500 √20= 50,000

Credit risk management

Credit risk managementazmatmengal Risk is the potential for undesirable outcomes from actions or activities. While safe harbors avoid risk, that is not what ships are designed for. There are many types of risks organizations face, including business, capital, credit, market, liquidity, environmental, operational, control, management, compliance, and organizational risks. Risk management involves identifying risks, assessing their probability and potential impact, establishing risk tolerances, and implementing controls and governance. Key principles of risk management include top management involvement, tailored approaches based on organizational nature, documented risk analysis, segregation of duties, accountability, internal auditing, integration across the organization, and established risk tolerance limits. Effective risk management requires clear roles, interdepartmental relationships, flexibility, and control

Operational risk management (orm)

Operational risk management (orm)Bushra Angbeen This document discusses operational risk and provides details on its definition, measurement, and management. It defines operational risk as losses resulting from inadequate or failed internal processes, people, and systems or from external events. It describes the Basic Indicator Approach, Standardized Approach, and Advanced Measurement Approach for calculating operational risk capital charges under Basel II. It also outlines the data elements, risk categories, and tools used to measure and manage operational risk.

RBI guidelines for risk managment

RBI guidelines for risk managmentKavitha Ravi The Reserve Bank of India (RBI) recognizes the importance of risk management in the banking sector. In 1999, RBI issued guidelines for banks regarding asset liability management and managing credit, market, and operational risks. The major risks banks face are liquidity risk, interest rate risk, market risk, credit or default risk, and operational risk. RBI evaluates banks' financial soundness using the CAMELS framework, which assesses capital adequacy, asset quality, management, earnings, liquidity, and sensitivity to market risk. RBI's guidelines require banks to establish comprehensive risk rating systems, develop value at risk methodologies, and integrate asset liability management and credit policy activities to better manage risks.

Operational Risk Management Under Basel II & Basel III

Operational Risk Management Under Basel II & Basel IIIEneni Oduwole This presentation discusses operational risk under Basel II and III. It provides an overview of the evolution of Basel guidelines and the focus of the Basel II framework on providing capital standards for banks to mitigate financial and operational risks. It defines operational risk and discusses the approaches to estimating capital - basic indicator, standardized, and advanced measurement. The presentation notes some pitfalls of Basel II and the focus of Basel III on increased capital requirements and liquidity standards. It addresses ongoing challenges in operational risk management and potential improvements.

Economic Capital Model and System implementation

Economic Capital Model and System implementationsarojkdas This document discusses frameworks and solutions for risk and capital management. It addresses establishing an enterprise risk management framework, optimizing capital allocation by linking risk to capital, and maximizing risk-adjusted returns. It emphasizes the importance of building these frameworks on a strong data and analytics foundation with continuous measurement and optimization. It also discusses identifying and quantifying total risk, allocating economic capital, and scenario analysis as part of an internal capital adequacy assessment process.

Operational Risk Management in China

Operational Risk Management in ChinaKapronasia Although Chinese banks have in the past not focused tremendously on risk management, recent events and comments from regulators indicate that risk management will be more of a focus for banks. In the first of our series of webinars on risk management in China, we look at operational risk management in Chinese banks to understand more about what it is, how things are different in China and what will happen in the near future.

This webinar will give you an in-depth look at the opportunities and challenges for banks as well as the potential implications for vendors and vendor solution offerings.

Operational Risk Loss Forecasting Model

for Stress Testing

Operational Risk Loss Forecasting Model

for Stress TestingCRISIL Limited Presentation on ‘Operational Risk Loss Forecasting Model for Stress Testing – A Three-Stage Approach’ made by Dr. James Lu, Director, Risk & Analytics, CRISIL Global Research & Analytics (GR&A) at The 17th Annual OpRisk North America 2015, New York

Chapter 3 - Risk Management - 2nd Semester - M.Com - Bangalore University

Chapter 3 - Risk Management - 2nd Semester - M.Com - Bangalore UniversitySwaminath Sam MODULE 3:

Credit Risks Credit Risk Management models - Introduction, Motivation, Funtionality of good credit. Risk Management models- Review of Markowitz’s Portfolio selection theory –Credit Risk Pricing Model – Capital and Rgulation. Risk management of Credit Derivatives.

Measuring operational risk

Measuring operational riskUjjwal 'Shanu' Operational risk can arise from inadequate or failed internal processes, people and systems or from external events. It can be measured using a top-down approach such as the Basic Indicator Approach which calculates capital as 15% of average gross income, or the Standardized Approach which divides activities into business lines each with a factor. A bottom-up approach uses internal loss data but has challenges around position equivalence, completeness, and context dependence. Key risk indicators can also be used to signal potential operational losses.

operations risk management power point presentation.

operations risk management power point presentation.Miyelani Shibambo Operational risk can result in losses from internal failures or external events. It is classified based on frequency and impact of events. Management typically focuses on low frequency/high impact events and high frequency/low impact events. The Basel Accords define three approaches to operational risk capital requirements: Basic Indicator, Standardized, and Advanced Measurement. The Standardized Approach divides business activities into eight lines and assigns a beta multiplier to each line's gross income. The Advanced Measurement Approach uses banks' internal models to calculate regulatory capital.

Operation Risk Management in Banking Sector

Operation Risk Management in Banking SectorSanjay Kumbhar This presentation discusses operational risk management in the banking sector. It covers topics such as categories of operational risk, risk identification and analysis techniques, key risk indicators, and risk mitigation strategies. The presentation is delivered by five students and contains several sections that outline the flow of topics to be presented.

Ciencia de la información y bibliotecología

Ciencia de la información y bibliotecologíaLigia34 Este programa forma profesionales con amplio conocimiento en ciencia de la información para crear y dirigir bibliotecas de acuerdo con las necesidades de usuarios y la sociedad. Los estudiantes aprenden a sistematizar el conocimiento científico y cultural usando estándares internacionales para preservar y difundir la información como patrimonio humano. El profesional resultante es responsable de aplicar las leyes de archivos para proteger el patrimonio documental a niveles municipal, departamental y nacional.

ALL LANDSCAPE SUPPLIES FINAL 2015 PRICE LIST-ABSOLUTE LATEST

ALL LANDSCAPE SUPPLIES FINAL 2015 PRICE LIST-ABSOLUTE LATESTAll Landscape Supplies This document provides a price list for various landscape and garden materials from mulches and soils to stones, pavers, and turf. It lists over 45 products along with their prices per half cubic meter or cubic meter. In addition to materials, the business also offers landscaping services such as concreting, paving, turf installation and more. Delivery is available to surrounding Brisbane areas.

More Related Content

What's hot (20)

Operational Risk Management under BASEL era

Operational Risk Management under BASEL eraTreat Risk Operational risk have always ignored by Banks as they thought Credit and market risks can cause catastrophe. But history of misfortunes taught us different lessons. Controls and internal audit have long been construed as guard till BASEL II dictates forced banks to look with insight. Understand the dimension of ORM in this presentation.

Credit risk management presentation

Credit risk management presentationharsh raj This presentation provides complete study ofcredit risk management,how it was performed in yester years ,how it is taken care nowadays and what is the road ahead in future

Operational risk ppt

Operational risk pptNehaKamboj10 OPERATIONAL RISK, CLASSIFICATION OF OPERATIONAL RISK, OPERATIONAL RISK MANAGEMENT(ORM), principles & policies, ROLE OF OPERATIONAL RISK MANAGEMENT

Risk Management in Banking Sectors.

Risk Management in Banking Sectors.Rupesh neupane Risk Management in Banking Sectors:

This side is helps to analyse the risk management in banking sectors.

SD Basel process automation seminar presentation

SD Basel process automation seminar presentationsarojkdas The document discusses key considerations for financial institutions in establishing a sustainable process for automating Basel III capital adequacy requirements. It emphasizes the need for a golden source of data, unified data management, and computational flexibility to implement complex models and regulatory changes. A reference information architecture is proposed with shared ownership of data and active collaboration between risk, finance, regulatory, and IT functions. Effective data governance and change management processes are necessary to ensure ongoing validity, consistency and completeness of data.

Operational Risk Management Oct 4

Operational Risk Management Oct 4av vedpuriswar This document discusses operational risk management in banks. It covers typical bank organizational structures including front, middle, and back offices. It describes key operational risk types like fraud, system failures, and processing errors. It also discusses operational risk management strategies such as risk mapping, indicators, qualitative assessments, and statistical approaches to quantify unexpected losses from operational risks.

Operational Risk Management

Operational Risk Managementarsqureshi The document discusses operational risk and provides guidance on defining, identifying, measuring, monitoring, controlling, and mitigating operational risk according to the Basel Committee on Banking Supervision. It addresses issues with operational risk loss data and outlines principles for developing an appropriate operational risk management environment, process, and framework. The document also examines challenges with using internal and external loss data for quantifying operational risk capital requirements.

OFSAA-ALM

OFSAA-ALMsailajasatish The document discusses asset liability management (ALM) in banking. It covers several key topics in 3 paragraphs:

1) ALM refers to managing a bank's balance sheet to allow for different interest rate and liquidity scenarios. This involves assessing risks from changes in interest rates, exchange rates, and liquidity. ALM aims to quantify these risks and provide strategies to make credit, interest, and liquidity risks acceptable.

2) Common ALM techniques include gap analysis, duration analysis, scenario analysis, simulation, and value-at-risk to measure risks. Interest rate risk is a major focus, and tools like gap and duration analysis examine how changes in rates impact profits and asset values.

3)

Risk management basel ii

Risk management basel iiUjjwal 'Shanu' The weekly VAR(10%) is $27,951

VAR(10%)20-days(monthly) = 12,500 √20= 50,000

Credit risk management

Credit risk managementazmatmengal Risk is the potential for undesirable outcomes from actions or activities. While safe harbors avoid risk, that is not what ships are designed for. There are many types of risks organizations face, including business, capital, credit, market, liquidity, environmental, operational, control, management, compliance, and organizational risks. Risk management involves identifying risks, assessing their probability and potential impact, establishing risk tolerances, and implementing controls and governance. Key principles of risk management include top management involvement, tailored approaches based on organizational nature, documented risk analysis, segregation of duties, accountability, internal auditing, integration across the organization, and established risk tolerance limits. Effective risk management requires clear roles, interdepartmental relationships, flexibility, and control

Operational risk management (orm)

Operational risk management (orm)Bushra Angbeen This document discusses operational risk and provides details on its definition, measurement, and management. It defines operational risk as losses resulting from inadequate or failed internal processes, people, and systems or from external events. It describes the Basic Indicator Approach, Standardized Approach, and Advanced Measurement Approach for calculating operational risk capital charges under Basel II. It also outlines the data elements, risk categories, and tools used to measure and manage operational risk.

RBI guidelines for risk managment

RBI guidelines for risk managmentKavitha Ravi The Reserve Bank of India (RBI) recognizes the importance of risk management in the banking sector. In 1999, RBI issued guidelines for banks regarding asset liability management and managing credit, market, and operational risks. The major risks banks face are liquidity risk, interest rate risk, market risk, credit or default risk, and operational risk. RBI evaluates banks' financial soundness using the CAMELS framework, which assesses capital adequacy, asset quality, management, earnings, liquidity, and sensitivity to market risk. RBI's guidelines require banks to establish comprehensive risk rating systems, develop value at risk methodologies, and integrate asset liability management and credit policy activities to better manage risks.

Operational Risk Management Under Basel II & Basel III

Operational Risk Management Under Basel II & Basel IIIEneni Oduwole This presentation discusses operational risk under Basel II and III. It provides an overview of the evolution of Basel guidelines and the focus of the Basel II framework on providing capital standards for banks to mitigate financial and operational risks. It defines operational risk and discusses the approaches to estimating capital - basic indicator, standardized, and advanced measurement. The presentation notes some pitfalls of Basel II and the focus of Basel III on increased capital requirements and liquidity standards. It addresses ongoing challenges in operational risk management and potential improvements.

Economic Capital Model and System implementation

Economic Capital Model and System implementationsarojkdas This document discusses frameworks and solutions for risk and capital management. It addresses establishing an enterprise risk management framework, optimizing capital allocation by linking risk to capital, and maximizing risk-adjusted returns. It emphasizes the importance of building these frameworks on a strong data and analytics foundation with continuous measurement and optimization. It also discusses identifying and quantifying total risk, allocating economic capital, and scenario analysis as part of an internal capital adequacy assessment process.

Operational Risk Management in China

Operational Risk Management in ChinaKapronasia Although Chinese banks have in the past not focused tremendously on risk management, recent events and comments from regulators indicate that risk management will be more of a focus for banks. In the first of our series of webinars on risk management in China, we look at operational risk management in Chinese banks to understand more about what it is, how things are different in China and what will happen in the near future.

This webinar will give you an in-depth look at the opportunities and challenges for banks as well as the potential implications for vendors and vendor solution offerings.

Operational Risk Loss Forecasting Model

for Stress Testing

Operational Risk Loss Forecasting Model

for Stress TestingCRISIL Limited Presentation on ‘Operational Risk Loss Forecasting Model for Stress Testing – A Three-Stage Approach’ made by Dr. James Lu, Director, Risk & Analytics, CRISIL Global Research & Analytics (GR&A) at The 17th Annual OpRisk North America 2015, New York

Chapter 3 - Risk Management - 2nd Semester - M.Com - Bangalore University

Chapter 3 - Risk Management - 2nd Semester - M.Com - Bangalore UniversitySwaminath Sam MODULE 3:

Credit Risks Credit Risk Management models - Introduction, Motivation, Funtionality of good credit. Risk Management models- Review of Markowitz’s Portfolio selection theory –Credit Risk Pricing Model – Capital and Rgulation. Risk management of Credit Derivatives.

Measuring operational risk

Measuring operational riskUjjwal 'Shanu' Operational risk can arise from inadequate or failed internal processes, people and systems or from external events. It can be measured using a top-down approach such as the Basic Indicator Approach which calculates capital as 15% of average gross income, or the Standardized Approach which divides activities into business lines each with a factor. A bottom-up approach uses internal loss data but has challenges around position equivalence, completeness, and context dependence. Key risk indicators can also be used to signal potential operational losses.

operations risk management power point presentation.

operations risk management power point presentation.Miyelani Shibambo Operational risk can result in losses from internal failures or external events. It is classified based on frequency and impact of events. Management typically focuses on low frequency/high impact events and high frequency/low impact events. The Basel Accords define three approaches to operational risk capital requirements: Basic Indicator, Standardized, and Advanced Measurement. The Standardized Approach divides business activities into eight lines and assigns a beta multiplier to each line's gross income. The Advanced Measurement Approach uses banks' internal models to calculate regulatory capital.

Operation Risk Management in Banking Sector

Operation Risk Management in Banking SectorSanjay Kumbhar This presentation discusses operational risk management in the banking sector. It covers topics such as categories of operational risk, risk identification and analysis techniques, key risk indicators, and risk mitigation strategies. The presentation is delivered by five students and contains several sections that outline the flow of topics to be presented.

Viewers also liked (15)

Ciencia de la información y bibliotecología

Ciencia de la información y bibliotecologíaLigia34 Este programa forma profesionales con amplio conocimiento en ciencia de la información para crear y dirigir bibliotecas de acuerdo con las necesidades de usuarios y la sociedad. Los estudiantes aprenden a sistematizar el conocimiento científico y cultural usando estándares internacionales para preservar y difundir la información como patrimonio humano. El profesional resultante es responsable de aplicar las leyes de archivos para proteger el patrimonio documental a niveles municipal, departamental y nacional.

ALL LANDSCAPE SUPPLIES FINAL 2015 PRICE LIST-ABSOLUTE LATEST

ALL LANDSCAPE SUPPLIES FINAL 2015 PRICE LIST-ABSOLUTE LATESTAll Landscape Supplies This document provides a price list for various landscape and garden materials from mulches and soils to stones, pavers, and turf. It lists over 45 products along with their prices per half cubic meter or cubic meter. In addition to materials, the business also offers landscaping services such as concreting, paving, turf installation and more. Delivery is available to surrounding Brisbane areas.

The Archived Canadian Patent Competitive Intelligence (June 21, 2011)

The Archived Canadian Patent Competitive Intelligence (June 21, 2011)Muchiu (Henry) Chang, PhD. Cantab In 2009, when worked for the Region of Peel government, Canada, we successfully used patent mapping to identify 20 US patent intensive companies as the potential employers for highly educated immigrants. Following this initiative, we have created and been maintaining a Canadian patent competitive intelligence (CI) database to track the latest patent competence of over 3000 Canadian entities on a weekly basis. This database provides intelligence for long-term strategic research planning and short-term tactics.

The archived Canadian US Patent Competitive Intelligence Database (2014/11/25)

The archived Canadian US Patent Competitive Intelligence Database (2014/11/25) Muchiu (Henry) Chang, PhD. Cantab This is a directory of Canadian US patents holders. It has the latest information about who has US patents in Canada, where the US patent holders are, what they patented in the US market and the trends of their US patents.

In 2009, when I was working for the Region of Peel government, Canada, I successfully used patent mapping to identify 20 US patent intensive companies as the potential employers for highly educated immigrants. Following this initiative, I created a Canadian patent competitive intelligence (CI) database to track the latest patent competence of over 5000 Canadian entities, in all sector throughout Canada, on a weekly basis. My work with Region of Peel from 2010 to 2012 showed that this database can provide the "no-older-than-7-day" intelligence for long-term strategic research/planning and short-term tactics. This is also the first attempt in Canada to use patent landscape as a regional economic strength indicator and a baseline for policy harmonization and policy performance evaluation.

Control de intervalo

Control de intervalocamilo802 gfkcvnjlalicmmejfkhhjljhsvjdshvjfiuhfudoujcjwnqjodidfbckbv hdljhqjdqhfou

спільна заява укр мова

спільна заява укр моваMykhailo Bno-Airiian спільна заява Міністерства енергетики та вугільної промисловості України та Міністерства економіки, торгівлі та промисловості Японії щодо співробітництва в галузі енергетики

IMC_Campaign

IMC_CampaignTeresa Compton This document provides an integrated marketing communications plan for The Home Depot for 2016. It begins with an executive summary that outlines the key objectives of appealing to millennials and developing relationships with a new type of customer. It then provides background on The Home Depot, including its history, values, financials, products/services. It analyzes competitors like Lowe's and Ace Hardware. The plan also identifies the target audience, provides a SWOT analysis, and outlines marketing objectives and strategies. It proposes approaches for creative content, media planning, public relations, direct marketing, sales promotion, and evaluation. The goal is to use an integrated approach across traditional, digital and other channels to connect with customers.

Gamification en santé

Gamification en santéTELECOM-PARISTECH-SANTE Introduction à la quatrième réunion thématique du groupe Télécom Paristech Santé du 20 janvier 2016.

Présentation des activités du groupe et des intervenants.

Queen Elizabeth Keynote Presentation--ENGL 323

Queen Elizabeth Keynote Presentation--ENGL 323abalizet Queen Elizabeth I ruled England from 1558 to 1603 during a time of religious conflict between Catholics and Protestants. As a Protestant monarch, Elizabeth persecuted Catholics who pledged allegiance to the Pope rather than her. In 1588, the Spanish Armada attempted to invade England on behalf of Catholic Spain but was destroyed in a storm, seen as an act of God protecting Protestant England. As she aged without an heir, Elizabeth centralized power in the monarchy and defended England against threats, dressing as a soldier to inspire troops against the Spanish. Upon her death in 1603 without children, King James VI of Scotland took the throne, bringing peace but less faith in the monarchy as he squandered funds.

M-Edge IMCP v2

M-Edge IMCP v2Ann Andrist This document presents an integrated marketing communications plan for M-Edge. It identifies the target market as active lifestyle mobile professionals and aims to position M-Edge as the obvious choice for this group through the term "Working Warrior." The plan proposes using viral videos on social media and providing products to fitness instructors to generate awareness of M-Edge. It also outlines message strategies, media choices, and sales promotions including social media contests and giveaways to trainers to help increase brand awareness among the target market.

¿Qué hemisferio cerebral controla tu vida?

¿Qué hemisferio cerebral controla tu vida?UNACARTemasSelectosdeFisica El cerebro esta constituido por dos mitades o hemisferios: El Derecho y el Izquierdo.

Cada uno de los cuales esta especializado en funciones diferentes.

Slide deck

Slide deckI-Chieh Chen This document provides an overview of a proposed upscale resale boutique called Scavenger's Gems located in Taipei, Taiwan. The business aims to elevate the concept of resale fashion by providing an inspiring shopping experience with gently used apparel and accessories from moderate to high-end brands. The target market includes females aged 18-35 who are trend-conscious, image-focused, and seek value. The marketing strategy outlines goals, branding, and planned use of social media, websites, emails, and display ads to promote the boutique.

Protección de datos

Protección de datosAbel Revoredo Presentación introductoria al entorno legal vinculado a la protección de Datos Personales en el Perú.

The Archived Canadian Patent Competitive Intelligence (June 21, 2011)

The Archived Canadian Patent Competitive Intelligence (June 21, 2011)Muchiu (Henry) Chang, PhD. Cantab

The archived Canadian US Patent Competitive Intelligence Database (2014/11/25)

The archived Canadian US Patent Competitive Intelligence Database (2014/11/25) Muchiu (Henry) Chang, PhD. Cantab

Similar to 9. Basel II Presentation (20)

Risk management & basel ii

Risk management & basel ii Amir Razvi The document discusses various aspects of risk management and capital requirements under Basel II. It provides explanations of key concepts such as economic capital, regulatory capital, credit risk measurement approaches, operational risk approaches, and credit risk mitigation techniques. It also compares the standardized and internal ratings-based approaches for credit risk and provides examples of calculating risk-weighted assets and capital adequacy ratios.

Capital adequacy (final)

Capital adequacy (final)Harsh Chadha Here are the key points about reverse repo rate from the document:

- Reverse repo rate is the rate at which the central bank of a country (Reserve Bank of India in case of India) borrows money from commercial banks.

- It is a monetary policy instrument used by the central bank to control money supply. An increase in reverse repo rate will decrease money supply and vice versa.

- When reverse repo rate is increased, it provides more incentive for commercial banks to park their funds with the central bank, thus decreasing the money available in the market.

JAMES OKARIMIA - BASEL II PILLAR1 ANAYTICS - Covering Credit, Market,and Op...

JAMES OKARIMIA - BASEL II PILLAR1 ANAYTICS - Covering Credit, Market,and Op...JAMES OKARIMIA The document discusses Basel II analytics covering the three pillars of credit risk, market risk, and operational risk. For credit risk, it describes various risk components like probability of default, exposure at default, and loss given default. It also discusses the standardised and internal ratings-based approaches. For market risk, it briefly mentions various risk types. For operational risk, it outlines the basic indicator, standard, and advanced measurement approaches. It then provides an overview of Pillar 2 covering the internal capital adequacy assessment process and supervisory review. Finally, it discusses Pillar 3 requirements for market discipline and disclosure.

James Okarimia - Basel II Pillar1 Analytics : Covering Credit, Market,and Ope...

James Okarimia - Basel II Pillar1 Analytics : Covering Credit, Market,and Ope...JAMES OKARIMIA The document discusses Basel II analytics covering the three pillars of credit risk, market risk, and operational risk. For credit risk, it describes various risk components like probability of default, exposure at default, loss given default, expected loss, and different approaches for calculating capital requirements. For market risk, it mentions risks like market data analysis, sensitivity modeling, and stress testing. For operational risk, it discusses the basic indicator approach, standardized approach, and advanced measurement approach. It also covers the internal capital adequacy assessment process under Pillar 2 and market discipline requirements under Pillar 3.

James Okarimia - Basel II Pillar1 Analytics Covering Credit, Market, and Op...

James Okarimia - Basel II Pillar1 Analytics Covering Credit, Market, and Op...JAMES OKARIMIA The document discusses Basel II analytics covering the three pillars of the Basel Accords - Pillar 1 on minimum capital requirements, Pillar 2 on supervisory review, and Pillar 3 on market discipline. It covers credit, market and operational risk analytics used to calculate regulatory capital under Pillar 1, as well as internal capital adequacy assessment (ICAAP) under Pillar 2. Key areas discussed include credit risk modeling, market risk measurement, operational risk approaches, liquidity risk frameworks, and integrated risk and finance analytics covering risk-adjusted return on capital (RAROC) and regulatory capital calculations.

James Okarimia Basel II Pillar1 Analytics - Covering Credit, Market,and Ope...

James Okarimia Basel II Pillar1 Analytics - Covering Credit, Market,and Ope...JAMES OKARIMIA The document discusses Basel II analytics covering the three pillars of the Basel Accords - Pillar 1 on minimum capital requirements, Pillar 2 on supervisory review, and Pillar 3 on market discipline. It covers credit, market and operational risk analytics used to calculate regulatory capital under Pillar 1, as well as internal capital adequacy assessment (ICAAP) under Pillar 2. The analytics include models for probability of default, exposure at default, loss given default, value at risk, as well as stress testing, risk reporting and compliance.

JAMES OKARIMIA BASEL II - PILLAR 1 ANALYTICS - Covering Credit,Market,and ...

JAMES OKARIMIA BASEL II - PILLAR 1 ANALYTICS - Covering Credit,Market,and ...JAMES OKARIMIA The document discusses Basel II analytics covering the three pillars of the Basel Accords - Pillar 1 on minimum capital requirements, Pillar 2 on supervisory review, and Pillar 3 on market discipline. It covers credit, market and operational risk analytics used to calculate regulatory capital under Pillar 1, as well as internal capital adequacy assessment (ICAAP) under Pillar 2. The analytics include models for probability of default, exposure at default, loss given default, value at risk, as well as stress testing, risk reporting and compliance.

Basel II

Basel IIHarsh Chitroda Basel II is the second of the Basel Accords, which are recommendations on banking laws and regulations issued by the Basel Committee on Banking Supervision.

CH&Cie - Regulatory Offer

CH&Cie - Regulatory OfferThibault Le Pomellec Regulations and standards have evolved in response to issues revealed by the 2007 financial crisis. Basel 2 aimed to better capture credit, market, and operational risk, while Basel 2.5 focused on risks from extreme events and Basel 3 aimed to strengthen capital requirements and address systemic risk and liquidity risk. Accounting standards like IFRS 9 and IFRS 13 also evolved to converge with prudential rules regarding areas like impairment models and fair value measurement. The standards have broadened in scope to establish more comprehensive frameworks for risk management across different areas.

CH&Cie - Regulatory Offer

CH&Cie - Regulatory OfferThibault Le Pomellec This document discusses regulations and standards that govern the banking system. It provides context on factors that drive regulations, including the 2007-2008 financial crisis which revealed shortcomings in risk management. Major standards discussed include Basel II, Basel 2.5, Basel III, IFRS 9, and IFRS 13. Each standard addresses specific objectives like strengthening capital requirements, managing liquidity risk, and increasing transparency. The document also outlines the principles and objectives of the various standards, with a focus on Basel II, Basel 2.5, and how they aim to improve risk measurement and management.

Risk

Risksivakumar bhagavathi Risk management in banking involves four main steps: identifying risks, measuring them both qualitatively and quantitatively, managing the risks, and monitoring and reviewing risks on an ongoing basis. There are three main categories of risk for banks: credit risk, market risk, and operational risk. Basel II aimed to make capital requirements more risk-sensitive by directly linking capital to the risk levels of counterparties and businesses. It introduced three pillars: minimum capital requirements, supervisory review, and market discipline through disclosure.

caiib_rmmodd_nov08.ppt

caiib_rmmodd_nov08.pptPranith roy This document summarizes key aspects of risk management and capital adequacy from CAIIB modules, including:

- Basel I focused on credit risk and assigned risk weights and factors, while Basel II expanded this to include market and operational risk.

- Pillar 1 of Basel II covers minimum capital requirements calculated for credit, market, and operational risk. Pillar 2 involves supervisory review, and Pillar 3 covers disclosure requirements.

- Components of regulatory capital include Tier 1, Tier 2, and Tier 3 capital. Capital requirements are calculated based on risk-weighted assets.

- Guidelines in India selected the standardized approaches for credit and operational risk and the basic indicator approach for banks to initially adopt

1 basel ii overview - islamabad

1 basel ii overview - islamabadraoateeqbzu The document provides an overview of Basel II, including its background, main elements, and implementation process. It discusses:

- The three pillars of Basel II - minimum capital requirements, supervisory review, and market discipline.

- The different approaches for calculating capital requirements for credit, operational, and market risk. This includes standardized and internal ratings-based approaches.

- The importance of the supervisory review process in Pillar 2 for banks to assess their capital adequacy beyond regulatory minimums.

- The role of enhanced disclosure in Pillar 3 to improve market discipline.

It emphasizes that countries should consider their own banking system's readiness before implementing Basel II and that there is no single approach, with

RM_Basel_II_Javed_Hussain_Saddique.ppt

RM_Basel_II_Javed_Hussain_Saddique.pptssuser6c91f7 This document provides an overview of risk management and Basel II. It discusses key concepts such as types of capital, economic capital, regulatory capital, expected and unexpected loss. It also summarizes the three pillars of Basel II including minimum capital requirements, supervisory review process, and market discipline. Approaches for credit risk, operational risk and market risk management under Basel II are outlined. The document also covers topics like value at risk, credit risk mitigation, and best practices in credit risk management.

Risk mgt basel norms,caiib

Risk mgt basel norms,caiibrajendran nk The document discusses the minimum capital requirements under Pillar 1 of Basel II. It covers the definition of the three main risks - credit, market, and operational risk. It describes the different approaches to calculate capital charges for each risk, including the standardized and internal ratings-based approaches for credit risk. The document also provides details on the classification of capital, calculation of risk-weighted assets, and specific risk weights for various asset categories as prescribed in Basel II.

SII effects on asset management1.1

SII effects on asset management1.1Servaas Houben, AAG-FIA, CFA, FRM The document discusses the implications of Solvency II on asset management for insurance companies. It covers the following key points:

1) Under Solvency II, asset values will be marked-to-market, which increases the perceived riskiness of equity and other assets compared to a book value approach. This will impact return on capital calculations for different asset classes.

2) There is debate around what interest rate should serve as the risk-free rate for discounting insurance liabilities, with options including swap rates, government bonds, or AAA-rated corporate bonds. The choice will affect capital requirements and surplus.

3) Sovereign debt from different countries may receive different capital charges under Solvency

Basel accord

Basel accordPrannati Padhi This document discusses capital requirements for banks and the Basel accords. It provides context for why capital requirements are needed due to risks banks face from loans and investments. It summarizes the objectives and key aspects of Basel I, which was an initial international agreement on capital standards in 1988. It then discusses weaknesses in Basel I that led to its revision and the introduction of Basel II in 2004, which aimed to make capital requirements more risk-sensitive. The document outlines the three pillars of Basel II - minimum capital requirements, supervisory review, and market discipline. It also provides details on the approaches to calculating capital requirements for credit, market and operational risks under Basel II.

Alm in banks

Alm in banksParth Maheshwari Asset Liability Management (ALM) is concerned with strategic balance sheet management involving risks caused by changes in interest rates, exchange rates, and liquidity position. ALM aims to match assets and liabilities in terms of maturities and interest rate sensitivities to minimize interest rate risk and liquidity risk. It involves identifying, measuring, monitoring, and controlling risks like interest rate risk, liquidity risk, credit risk, and contingency risk through techniques like gap analysis and duration gap analysis. Effective ALM requires strong organizational framework, information systems, and regular monitoring and reporting to manage risks.

Commercial banking

Commercial bankingkshitizeanand The document discusses the implementation of Basel I and II capital adequacy norms by Indian banks. It provides background on the Basel Committee and an overview of the key aspects of Basel I, including the capital requirements and risk weighting of assets. It then summarizes the pillars of Basel II - minimum capital requirements, supervisory review, and market discipline - and highlights some of the pitfalls of both frameworks. The document concludes by noting the challenges faced by the Indian banking industry in implementing the new capital standards.

More from Elly Quan (Quan Thi Hanh Mai) (8)

comparing ST loans vs LT loans

comparing ST loans vs LT loansElly Quan (Quan Thi Hanh Mai) This document outlines different types of business loans including their purpose, duration, collateral, and special characteristics. Self-liquidating loans finance inventory purchases and last 60-90 days, using inventory and receivables as collateral. Working capital loans also finance inventory, last less than a year, and charge interest on actual amounts borrowed with compensating deposit balances required. Interim construction financing supports construction until completion when it switches to long-term loans. Security dealer financing supports stock purchasing and underwriting for a few days using government securities as collateral. Retailer and equipment financing supports durable goods installment contracts and dealer inventory financing for 90 days renewing for 30 days using inventory as collateral. Asset-based financing uses accounts receivable and inventory as

6C in banking management

6C in banking managementElly Quan (Quan Thi Hanh Mai) This document lists factors that a lender would consider when evaluating a loan application. It includes assessing the borrower's character, capacity to repay the loan, available collateral, current and projected economic conditions, whether the loan meets the lender's policies, the borrower's past payment history, ownership details, applicable laws and documents, the purpose of the loan, and financial details like cash flow, expenses, assets, and industry outlook. The extensive list covers both borrower specifics and external factors to conduct a comprehensive review.

BEHAVIOR FINANCE

BEHAVIOR FINANCEElly Quan (Quan Thi Hanh Mai) This document summarizes key concepts in behavioral finance, which models how psychological factors influence investor behavior. It discusses two categories of irrationalities: errors in information processing and behavioral biases. Specific errors discussed include forecast errors due to overreacting to recent data, overconfidence, conservatism in updating beliefs, and neglecting sample size. Biases discussed include reference dependence, regret avoidance, house money effect, and mental accounting.

bankruptcy testing analysis

bankruptcy testing analysisElly Quan (Quan Thi Hanh Mai) The document analyzes bankruptcy risk for three Vietnamese banks from 2008-2010 using four different methodologies: Moody's ratios, S&P ratios, Varizi's model, and Altman's Z-score. It begins with an introduction that provides background on financial risk management and describes the objectives and literature review. Chapter 2 explains the four methodologies to be used. Chapter 3 will provide qualitative and quantitative analysis of the banks using the various models and identify which model provides the most useful bankruptcy signals.

Slide final

Slide finalElly Quan (Quan Thi Hanh Mai) The document discusses Vietnam's stock market and interest rates. It provides information on:

1) Vietnam's declining interest rates from 2008-2011 and the effects on investments and the real estate/stock markets.

2) The VN-Index and HNX Index increasing from March-April 2012 following further interest rate cuts.

3) Analysis of specific company SAM's stock price increasing nearly 30% in April due to declining interest rates and expectations for real estate.

Ultimate VIX&CDS

Ultimate VIX&CDSElly Quan (Quan Thi Hanh Mai) The document discusses the VIX index and credit default swap (CDS) spreads. It provides definitions and background information on both. Regarding the VIX index, it notes that the VIX represents the implied volatility of S&P 500 index options and is often called the "fear index" because high values correspond to periods of uncertainty and falling stock prices. The document then charts the VIX index and S&P 500 from 2003-2011, showing that the VIX rises during financial crises as stock prices fall, such as during the 2008 global financial crisis when the VIX reached record highs above 80. It also discusses how CDS spreads relate to default probabilities.

9. Basel II Presentation

- 1. TABLE OF CONTENT 3 pillarsinbaselii motivesfor baselII ApplicationinVIetnam

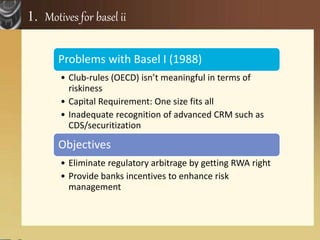

- 2. 1. Motives for basel ii Problems with Basel I (1988) • Club-rules (OECD) isn’t meaningful in terms of riskiness • Capital Requirement: One size fits all • Inadequate recognition of advanced CRM such as CDS/securitization Objectives • Eliminate regulatory arbitrage by getting RWA right • Provide banks incentives to enhance risk management

- 3. 1. Motives for basel II Text Text Text Text Text Liquidity Risk Reputation Risk Credit Risk Market Risk Operational Risk

- 4. 2. Three pillars in basel II

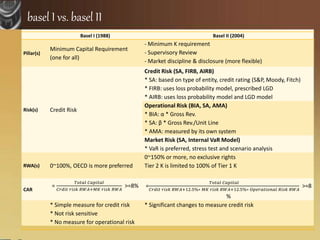

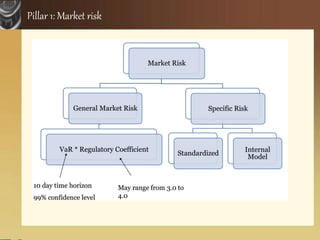

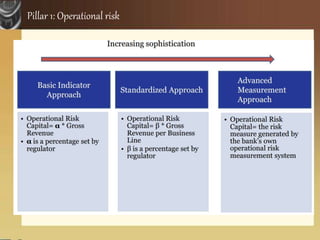

- 5. Basel I (1988) Basel II (2004) Pillar(s) Minimum Capital Requirement (one for all) - Minimum K requirement - Supervisory Review - Market discipline & disclosure (more flexible) Risk(s) Credit Risk Credit Risk (SA, FIRB, AIRB) * SA: based on type of entity, credit rating (S&P, Moody, Fitch) * FIRB: uses loss probability model, prescribed LGD * AIRB: uses loss probability model and LGD model Operational Risk (BIA, SA, AMA) * BIA: α * Gross Rev. * SA: β * Gross Rev./Unit Line * AMA: measured by its own system Market Risk (SA, Internal VaR Model) * VaR is preferred, stress test and scenario analysis RWA(s) 0~100%, OECD is more preferred 0~150% or more, no exclusive rights Tier 2 K is limited to 100% of Tier 1 K CAR = 𝑇𝑜𝑡𝑎𝑙 𝐶𝑎𝑝𝑖𝑡𝑎𝑙 𝐶𝑟𝑑𝑖𝑡 𝑟𝑖𝑠𝑘 𝑅𝑊𝐴+𝑀𝐾 𝑟𝑖𝑠𝑘 𝑅𝑊𝐴 >=8% = 𝑇𝑜𝑡𝑎𝑙 𝐶𝑎𝑝𝑖𝑡𝑎𝑙 𝐶𝑟𝑑𝑖𝑡 𝑟𝑖𝑠𝑘 𝑅𝑊𝐴+12.5%∗ 𝑀𝐾 𝑟𝑖𝑠𝑘 𝑅𝑊𝐴+12.5%∗ 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑜𝑛𝑎𝑙 𝑅𝑖𝑠𝑘 𝑅𝑊𝐴 >=8 % * Simple measure for credit risk * Not risk sensitive * No measure for operational risk * Significant changes to measure credit risk basel I vs. basel II

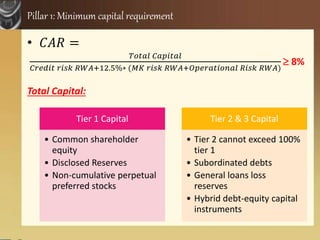

- 6. Pillar 1: Minimum capital requirement • 𝐶𝐴𝑅 = 𝑇𝑜𝑡𝑎𝑙 𝐶𝑎𝑝𝑖𝑡𝑎𝑙 𝐶𝑟𝑒𝑑𝑖𝑡 𝑟𝑖𝑠𝑘 𝑅𝑊𝐴+12.5%∗ (𝑀𝐾 𝑟𝑖𝑠𝑘 𝑅𝑊𝐴+𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑜𝑛𝑎𝑙 𝑅𝑖𝑠𝑘 𝑅𝑊𝐴) 8% Total Capital: Tier 1 Capital • Common shareholder equity • Disclosed Reserves • Non-cumulative perpetual preferred stocks Tier 2 & 3 Capital • Tier 2 cannot exceed 100% tier 1 • Subordinated debts • General loans loss reserves • Hybrid debt-equity capital instruments

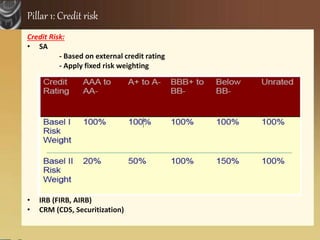

- 7. Pillar 1: Credit risk Credit Risk: • SA - Based on external credit rating - Apply fixed risk weighting • IRB (FIRB, AIRB) • CRM (CDS, Securitization)

- 8. Pillar 1: Market risk

- 9. Pillar 1: Operational risk

- 10. IN VIETNAM Regulatory Framework BASEL II Implementation

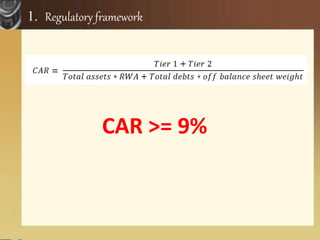

- 11. 1. Regulatory framework 2005 2014 Decree 457/2005 CAR: 8% (except for foreign bank branches) Circular 13/2010: CAR: 9% (all) Updated Circular 36/2014

- 12. 1. Regulatory framework CAR >= 9%

- 13. 2. BASEL II Implementation Credit Risk Awareness Lending activities: 90% Bad debt ratio is pretty high Phase 1: 2013 -2015 Phase 2: 2016 - 2018