Apre 4 t03

•

0 likes•189 views

The document summarizes the 2003 financial results of Eletropaulo and Tietê. Eletropaulo's market grew 1% in 2003. It invested R$1,654 million between 1998-2003, with R$217 million invested in 2003 to maintain and expand its grid. Key performance indicators like outage duration and frequency improved after privatization and met regulatory standards in 2003. Eletropaulo had high short-term debt, so in September 2003 it proposed readjusting over R$2.3 billion of private debt to recover its investment grade, align cash flows with debt payments, and reduce exchange rate risk. The proposal aimed to significantly deleverage over 3-5

Report

Share

Apre 4 t03

- 1. Eletropaulo and Tietê 2003 Financial Results February 6, 2004 1

- 2. Agenda

- 3. Agenda – MARKET – FINANCIAL AND OPERATIONAL PERFORMANCE – DEBT PROFILE – CONCESSION – FINANCIAL PERFORMANCE – CONCLUSION

- 4. !!"# $ % & ' ( ) ) & * * ) * +, & $ ) , & # # - #, & , & . *) & , & ( # & &+ $ ) + ( /$ & $ *

- 5. *0 )&+ Eletropaulo Tietê & $ 12234 5 67*) & $ 8 & * ( 12224 D ,$ &+ , & *9) + $ ) :14;;;, &# 7 8 *9) + * & 7"3= & &* & , <!= * $ 8 D# & &* & , & * , )& <!= & * , )& & > &) !!! & 5 *9) + ?@= & 4 D * $ EF 7 8 *9) + $ + $ ) :141<@ & <= * $ D ) + , & , ( & , ,$ 4# & 1!!= + *9) & ) ) , + ( &+ & 5 $ % + )& ) & ( 4, & +) & !!14 &+ ) ++ ( *) & & * & .* & % & &* 1223 , )& :"!!, & , ) & & 1< $ & , + + ( # *9) & *9) & D $ ) 4 &+ & 5 $ + : 2@!, & &+ # &+ ) , )& & ) ) !!14 & ) 7 8( # 4 :1A ( & 1,2 BI $)( * 4 *9) + 2A<;= D , )& & & &% , & :;1 & $ , ( 34 !!" , &+), , &A ) + & &/* &% ( + ( & ) &+ &+ & 7B C# 8 & +( # & # *) ) & , ) & & ) ) !!< &+ +& )* ) & + ( +& & * ,( 4 !!" & , & # & +( # & &+

- 6. & $ * , & % !& & & & $ & &&&# ! " $ # " ! # '# ( ) (# ) " * # ) +'# ) %# ' ) * * ( &) - G ), - :<1!, & @/ * $ + , -11 & - .* & % & H 2= &% ( &

- 7. ,$ * & Eletropaulo and Tietê , & )&* & &+ 0 + + $) +& * ,$ & I +& * & , & * & * ,$ & I , & , & ( & %& + %+ , * + &% % + & +J , & $ * ) &+ ( +& $ $ ) $ ) # ( & + * % - Reference Value -R$million * 3rd tranche of the rationing loan 240 Prepayment of the CVA 497 , - Gross values before adjustments K) & , & & &* # $ )

- 9. Agenda INTRODUCTION – MARKET – FINANCIAL AND OPERATIONAL PERFORMANCE – DEBT PROFILE – CONCESSION – FINANCIAL PERFORMANCE – CONCLUSION

- 10. $ ) &% * + 0 & KL (!% (!+ (! +!/ +!. +!% +!+ +! 3 2 2 2 2 0 0 4 4 4 2 0 $ 1 " & && + + " + + + ( Eletropaulo market grew 1% in 2003

- 11. Profile of the Consumer Market - Eletropaulo + +5 4 6783 + (5 4 6783 " *# " " *# . ( *# " ( ' +*# 9 +.' *# +/ # * : 5 44 $ 3 ( *# "' +/' *# + +9 + (9 '/ *# / # * ( *# &" % *# % 9 +&% *# +&& *# : 5 44 $ 3 +(' *# +". *#

- 12. ,$ & & ), $ & & KL " # * ( ' +!' % (+!% " %' # */ 6/ & * # * # & " !'+' " !+/ " !+(' & " !% / & & ' !. !" % ." # *& ( ' !% ( (!+' 9 : 5 44 $ 3 + + + (

- 13. Agenda INTRODUCTION – MARKET – FINANCIAL AND OPERATIONAL PERFORMANCE – DEBT PROFILE – CONCESSION – FINANCIAL PERFORMANCE – CONCLUSION

- 14. ) M !!"7 :, &8 + + + ( : 3 " !( # * ) 9 " ) : B3 4 ) ) 40 %* + ( "# @ 3 )3 9< !' " ' / !( . ( !& !% " +( " *# "( : A ) ) ; 4 3 4 $ 9 : 7 = , !" ( /! +- , !. . ' - ( !. " /' *# : B ) B @ 33 5 1 C 25 ) :: @ 3 65 : /& " % !% "! & ' !' +%/ *# :4 A : 9 >@ 4 )$ :4 A 1: 5 >9 < : ," & ! !( % - +( ( !/ " "' *# : 3 )9 * , = )** @3 3 1 " !+# / )3 9 4 3 3 = 9 $9 : 9 : ? ,( *% - " &" ,( !/ ( % '- &% # *' $1 = 1 5 1 : 9 : ,> $1 $ - ,/ " ' - '! & / !+' . " && *# >@ 4 )$ < )3 9 3 , -8 3 ; 4 , -< )3

- 15. EBITDA Adjustments + + + ( : : 9 /& D % ,@ 3 3 )) ) 9 " D ! &/ * (With the effect of provisions and Debt Confession IIa) - ) 2) ) 2) 9 +" D & 2 9 " D 2 ) 3 2 ) 9 "/ D % 3 @ )E 9 /* D "' 25 ) :: 8 33 54 ) 2 6 9 " D +( 5 4 F 9 %* D .% 5 4 F : : ,8: $ 1 5 $1 1 ,8: $ 1 5 $1 5 1 < 9 : :$ $< - (" '-

- 16. Capex - 2003 9D ( ! . . / ( !& " + & +/ !. % . +/ ! % & " +" !( ' ' " !( . / ' "& &/ "& && + + " + + + ( Enlargement of the Distribution Grid 1998 2003 Growth % Transformers of the distribution grid 160.549 214947 54.398 33,9% Poles 1.003.554 1.091.742 88.188 8,8% Overhead circuits of the distribution grid (15kV) 1.269 1.459 190 15,0% Installed power in the distribution grid (MVA) 9.030 11274 2.244 24,9% Eletropaulo invested R$ 1,654 million between 1998 and 2003. During 2003 R$ 217million, were invested representing a 20.5% increase when compared to the previous year. Investments in 2003 were made for: Maintenance of the grid New Clients’ Connections Improvement in consumers’ services

- 17. Development of the Performance Indicators Pre-Privatization Trend 5,3 - Post-Privatization Trend " *. /. " *. /' " *. / " *+ '% "* /+" " *' .( " *+ .( " *% & " *% % Aneel Standard " *% "% " *& " /& *& /+" * 2003 DEC: "& &" "& &+ "& &( "& &% "& & "& &. "& &' "& &/ "& && + + " + + + ( 12,57 hours 1 5, 4 - Pre-Privatization Trend Post-Privatization Trend &* "* ' " */ / "* ' " *% ' " *. ' "* +" " *& " & + * &+ * Aneel Standard /. */ ' " * .& *" 2003 FEC: 8,95 times "& &" "& &+ "& &( "& &% "& & "& &. "& &' "& &/ "& && + + " + + + ( ,4 - Pre-Privatization Trend Post-Privatization Trend +" "' / "% "/ % "" . "/ "& Aneel Standard "& ( "% ( " "% " &% 2003 TMA: /' "& &" "& &+ "& &( "& &% "& & "& &. "& &' "& &/ "& && + + " + + + ( 130 min , - 4G 4H I 4 " 4 + !

- 18. Agenda INTRODUCTION – MARKET – FINANCIAL AND OPERATIONAL PERFORMANCE – DEBT PROFILE – CONCESSION – FINANCIAL PERFORMANCE – CONCLUSION

- 19. 2003 &+ ( +& 5 2C" " +J( J+ + 5 2 6 ( J" " +J+ ( ,9 !&2* ) D @3 3 9 +!'2 D ,9 !( * ) D 2 @3 39 +* 2 D 4 D- 4 D- (# & %# . 9D 9D D D %# .# " %+# B 3 ( # B3 &% @J 3 *# ' # @J 3 * B B , - 3 @ 3 2 )3 B3 3 ) 34 3A J+ +C( (( ! ( J+ (C +!/ & /+

- 20. Indebtedness – Short Term x Long Term ) ) C 42 6+ ( C 42 6+ ( +&# # 9 " 2 D ! 9 +!. D 2 9 "" .4 D *% @ ) 1 3 3 4 # '# " 9 +!. D 2 9 ( 2 D !/ 5 K > K 5 K > K The total amount recorded in the Short Term does not mirror the actual schedule of maturities, as it includes the reclassification of some debts that incurred in non-compliance of contractual obligations such as financial covenants, cross- defaults and payment defaults

- 21. Purposes and Strategies of the Proposal to Readjust the Debt On September 30, 2003 a proposal for the readjustment of the profile of the indebtedness of Eletropaulo was presented to the creditor banks, which aims at: – Recovering its investment grade position – Readjusting its cash generation to the schedule for the amortization of the debts – Mitigating the exchange risks, continuing with the strategy of of converting the debt to Reais and making possible its return to having access to the hedge market The proposal allows for a significant unleveraging in the next 3-5 years – No refinancing risk in the next 36 months – Significant improvement in the credit indicators reducing thus the risk insight

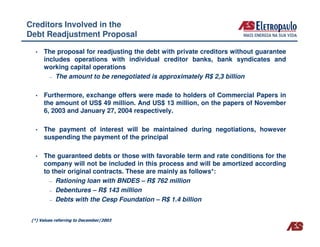

- 22. Creditors Involved in the Debt Readjustment Proposal The proposal for readjusting the debt with private creditors without guarantee includes operations with individual creditor banks, bank syndicates and working capital operations – The amount to be renegotiated is approximately R$ 2,3 billion Furthermore, exchange offers were made to holders of Commercial Papers in the amount of US$ 49 million. And US$ 13 million, on the papers of November 6, 2003 and January 27, 2004 respectively. The payment of interest will be maintained during negotiations, however suspending the payment of the principal The guaranteed debts or those with favorable term and rate conditions for the company will not be included in this process and will be amortized according to their original contracts. These are mainly as follows*: – Rationing loan with BNDES – R$ 762 million – Debentures – R$ 143 million – Debts with the Cesp Foundation – R$ 1.4 billion , -< ) 42 J+ (

- 23. The Proposal to Banks The proposal to creditor banks seeks to unify the debts to be restructured under one sole lot of documents – Isonomic treatment for creditor banks, with uniform rates, terms and covenants The Debt will be restructured in four tranches – The proportioning of the tranches was based on the projections of company’s liquidity – The tranches allow flexibility to creditors in regard to the desired exposure – At the most, 30% of each tranche will be denominated in US$ Schedule: – September 30, 2003: Proposal made to creditor banks – October 21, 2003: Indications of adhesion (non-binding) – December 22, 2003: Obtained 91% adhesion – February 16, 2004: Date anticipated for signing the contract

- 24. 24

- 25. Agenda INTRODUCTION – MARKET – FINANCIAL AND OPERATIONAL PERFORMANCE – DEBT PROFILE – CONCESSION – FINANCIAL PERFORMANCE – CONCLUSION

- 26. Concession Concession: 30 years. The concession contract provides the right to operate assets but does not grant the property of same Assets: 10 hydroelectric plants Location: Rivers Tietê, Grande, Pardo and Mogi Guaçu, located in the State of Sao Paulo 2,651 MW Installed Capacity: Operating Background: Plants started operations between 1958 and 1997 Capacity sold under Initial 100% of the productive capacity of Tietê (“assured Contracts (PPAs): energy”) 15% - 400MW – until 2008 according to a demand of the Increase in capacity: Privatization Notice

- 27. Initial and Bilateral Contracts The tariffs of the initial contracts are adjusted annually following the calculation formulae as pre-established in the Concession Contract Tariff Adjustment Rate = VPA + VPB x IGPM Revenue 1200 The bilateral contracts (new Eletropaulo contract) are adjusted on the basis of 1000 the IGPM 800 600 MW 9 J 83 400 200 @ 3 D : 5 0 + + + + / + " + "+ + " "# # 9 4 9 4

- 28. Portfolio Of contracts " # &# /# '# .# MW # %# (# + # "# # + ( + % + + . " 51 > L

- 29. Energy Summary 2003 7 7 B 5 83 (( % % !% . 51 > " ( !+" !' " . % . +% " / +! / " >4 " !& ( +. 65: +!' . & % !. M < 4 3 ' +!( !( ( L $ > :>> "! % " !( % !& & ' " & !( ( +!" % ' "! " . / !& (' / %! +!( / " :2 ./ & !& & +" !% " % 4 E "! +!& & " 9 / !/ % ' ' 3 " / % !( !% + 6 +!' &!% 7 N . ' !% /

- 30. Agenda INTRODUCTION – MARKET – FINANCIAL AND OPERATIONAL PERFORMANCE – DEBT PROFILE – CONCESSION – FINANCIAL PERFORMANCE – CONCLUSION

- 31. Statement od Income (Loss) 2003 + + " + + + ( : 4 )+ # ) 2 @ 9< +* . * / + '* " ' // '* ( *# .. ) ) 3 2 @ ) 2 ! $ 9 : 7 = ," /( " *- ,( (' *- ," " - (* ," %" / *- % *# 1 4 + " + +A 3 B 3 1 4 + + + (A : ( %+ /* (" (* % &" (* &* %' ( *# % :7 64 2 B 1: 5 >9 < : ,++'. *- ,++(' *- ,( && ' *- ,+ "' *- 6( *# (' :4 A , = - : 9 ) : 5$ ,>$ - B 4 &* (' % . +* ,(/ *- +% * . 1$9 = , )3 :7 6 - : 5$ ,>$ - (* (* ( ,+*- " * & %

- 32. Agreement with the MAE Creditors December/03 – closing of the deal with the MAE creditors Agreement for the payment of debts related to the purchase and sale of electric energy operations recorded in the Energy Wholesale Market – MAE, for the period between September 2000 and December 2002 (Period of Energy Rationing) Payment of debts in 49 installments Cash payment for debts lower than R$500 thousand. Debts amounted to R$120 million

- 33. Eletrobrás Value: R$ 1,488 bilion Correction and Interest:IGPM + 10% a year Maturity: 2013 Amortization: Monthly of interest and principal (168 monthly installments) calcullated on the basis “Price Table” Guarantee : receivables Debt originally assumed by CESP 1 @ ) 4 , O: - 400 350 300 R$ milhões 250 200 150 100 50 - 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

- 34. Agenda INTRODUCTION – MARKET – FINANCIAL AND OPERATIONAL PERFORMANCE – DEBT PROFILE – CONCESSION – FINANCIAL PERFORMANCE – CONCLUSION

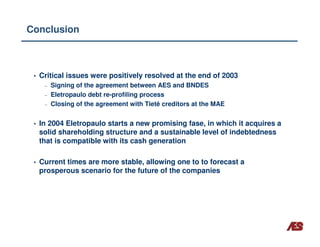

- 35. Conclusion Critical issues were positively resolved at the end of 2003 – Signing of the agreement between AES and BNDES – Eletropaulo debt re-profiling process – Closing of the agreement with Tietê creditors at the MAE In 2004 Eletropaulo starts a new promising fase, in which it acquires a solid shareholding structure and a sustainable level of indebtedness that is compatible with its cash generation Current times are more stable, allowing one to to forecast a prosperous scenario for the future of the companies

- 36. Eletropaulo and Tietê Results 2003 February 6, 2004