Customer Centric Retail Innovation - Bucharest May 29, 2008

•Download as PPTX, PDF•

3 likes•1,560 views

This document discusses retail innovation from a strategic perspective, with a focus on customer-centric innovation. It argues that traditional formats of retail innovation are limited and that 97% of innovations fail. It advocates taking the customer's perspective in order to better understand their needs and emotions throughout their journey. The example is given of how Apple was able to break retail rules and achieve remarkable success and growth by focusing intently on customer experience, segmentation, and lifestyle marketing rather than just product sales.

Report

Share

Customer Centric Retail Innovation - Bucharest May 29, 2008

- 1. RETAIL INNOVATION: A STRATEGIC PERSPECTIVE FUTURELAB

- 3. 1. GET ON A PLANE TO LEARN AND NETWORK FUTURELAB

- 4. 2. IMPORT – SKILLS, IDEAS, FORMATS FUTURELAB

- 5. 3. SECURE AND TRAIN THE BEST PEOPLE

- 6. FUTURELAB COPY MODIFY CREATE DEGREE OF INNOVATION Introduce global Modify existing Develop new formats that already concepts to better concepts, targeting exist match local needs specific local segments and needs 4. INNOVATE LIKE ONLY ROMANIANS CAN

- 7. RETAIL INNOVATION, ACCORDING TO MANY POP Systems Online FUTURELAB

- 8. THEN, GO TO WORK BRANDS RETAILERS/INVESTORS Be the first to become friendly with your Be first to bring a (modified) format into the new customers market Help your existing distribution to Come with something « unique » which « make the jump » internationals can’t offer Pro-actively say goodbye to those who Get out of the way and sell as expensive as can‟t or won‟t innovate. possible. FUTURELAB

- 9. BUT WE WILL START WITH INNOVATION FROM A STRATEGIC PERSPECTIVE And to be more precise: « customer centric retail innovation » Source: IBM Business Consulting Services – The Retail Divide, 2004 FUTURELAB

- 10. Think Beyond the Store Broaden Your Innovation Horizon FUTURELAB

- 11. Why Customer Centric? • Traditional Innovation is Broken • Competition is Changing • There‟s not much to be done at retail anyway

- 12. Why Customer Centric? Quiz: Which % of innovations fail? 97% FUTURELAB

- 13. Why Customer Centric? WHO COMPETES WITH MARS? CONSUMER PERSPECTIVE FUTURELAB

- 14. WHY CUSTOMER-CENTRIC? FORMAT INNOVATION IS LIMITED FUTURELAB

- 15. WHY CUSTOMER-CENTRIC? FORMAT INNOVATION IS LIMITED FUTURELAB

- 16. WHY CUSTOMER-CENTRIC? FORMAT INNOVATION IS LIMITED FUTURELAB

- 17. WHY CUSTOMER-CENTRIC? FORMAT INNOVATION IS LIMITED FUTURELAB

- 18. WHY CUSTOMER-CENTRIC? FORMAT INNOVATION IS LIMITED FUTURELAB

- 19. WHY CUSTOMER-CENTRIC? FORMAT INNOVATION IS LIMITED FUTURELAB

- 20. Why Customer Centric? • Traditional Innovation is Broken • Competition is Changing • There‟s not much to be done at retail anyway FUTURELAB

- 21. FUTURELAB CUSTOMER CENTRIC RETAIL INNOVATION Customer Centric Retail Innovation WHAT ABOUT THE CUSTOMER?

- 22. REMARKABLE FUTURELAB

- 23. FUTURELAB Apple Retail 2001 Sorry Steve, Apple Stores Won‟t Work (Business Week) Apple Retail 2004: Watch video on Fastest retailer ever to reach the http://www.youtube.com/watch?v= $1 billion mark a year m-Y7vZMEPrU Apple Retail 2006 Fastest retailer ever to reach $1 billion/quarter mark Apple Retail 2007 Sales per sq.meter = $ 30,176 (as comparison: BestBuy = $10,643) HOW DID THEY DO IT?

- 24. DRIVERS FOR RECOMMENDATION IN ICT Source: Net Promoter ™ Economics: the Impact of WOM, Satmetrix, 2008 FUTURELAB

- 25. • Careful segmentation and focus on students, educators and creative professionals (even now consumer appeal broadens) • A retail experience differentiated by service before, during and after sales (Genius bar) • Scenario or lifestyle Marketing & Sales vs. Product « What do you want to do ? » • Style & design THE RESPONSE Source: Net Promoter ™ Economics: the Impact of WOM, Satmetrix, 2008 FUTURELAB

- 26. BREAKING ALL THE RULES • No commissions • Team bonuses • Focus on experience • Fashion & design people to run computer retail • Hire for personality, attitude and customer fit … train the rest Ron Johnson • High identification: Tshirts, iPod, discounts, … Target • 3 week immersion at start of job ONLY on customer relationship skills and understanding customer needs/lifestyle • All product training is online (except geniuses) • Training on store computers or borrowed MickeyDrexler laptop The Gap FUTURELAB

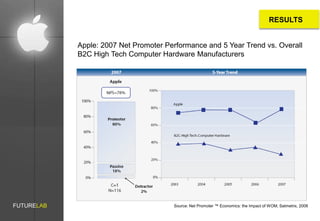

- 27. RESULTS Apple: 2007 Net Promoter Performance and 5 Year Trend vs. Overall B2C High Tech Computer Hardware Manufacturers FUTURELAB Source: Net Promoter ™ Economics: the Impact of WOM, Satmetrix, 2008

- 28. RESULTS Total Customer Value of an Apple advocate is almost twice that of the industry average FUTURELAB Source: Net Promoter ™ Economics: the Impact of WOM, Satmetrix, 2008

- 29. Revenue Growth % 2007 vs 2008 Source: Fortune Magazine, May 5,2008 24,3 13,8 8,4 6,5 6,2 5,5 0,8 HP Dell Apple Xerox Sun NCR Pitney Bowes RESULTS FUTURELAB

- 30. HOW ABOUT YOU? 5 To Customer Centric Retail Innovation steps FUTURELAB

- 31. Image by : Zombiefactory, CC-license 2.0 #1 TAKE THE CUSTOMER PERSPECTIVE FUTURELAB

- 32. HOTSPOT HOTSPOT Building Use & Awareness Purchase Repurchase Loyalty Advocacy Preference Service THE CUSTOMER JOURNEY – BRAND/RETAIL PERSPECTIVE FUTURELAB

- 33. Flipchart Time Which are the steps in the customer journey when booking a holiday? How could you innovate on them? THE CUSTOMER JOURNEY CUSTOMER PERSPECTIVE FUTURELAB

- 34. THE CUSTOMER JOURNEY CUSTOMER PERSPECTIVE 1. I dream of going on holiday 2. I research my holiday 3. I plan my holiday 4. I select my holiday 5. I purchase my holiday 6. I receive travel documents & tickets 7. I anticipate departure 8. I prepare my trip 9. I travel to my destination 10. I discover my destination 11. I experience my destination 12. I record my memories 13. I share my experience How Can You Innovate Now? 14. I travel back home 15. I share my memories LVMH - AOL Time Warner UBS - Richemont FUTURELAB

- 35. THE CUSTOMER JOURNEY CUSTOMER PERSPECTIVE How About You? TRAVEL CARS BANKING FOOD Photo Nils Bremer, cc. 2.0 FUTURELAB

- 36. FUTURELAB Photo: Joeannenah, cc: 2.0 #2 GET THE CUSTOMER HEARTBEAT

- 37. 1. I dream of going on holiday 2. I research my holiday WHAT DO YOUR CUSTOMERS 3. I plan my holiday REALLY CARE ABOUT? 4. I select my holiday 5. I purchase my holiday 6. I receive travel documents & tickets 7. I anticipate departure 8. I prepare my trip WHICH EMOTIONS ? 9. I travel to my destination 10. I discover my destination ARE ALL EMOTIONS EQUALLY STRONG? 11. I experience my destination 12. I record my memories 13. I share my experience 14. I travel back home 15. I share my memories FUTURELAB

- 38. FUTURELAB BUT DON’T JUMP TO CONCLUSIONS … THINK SCENARIOS

- 39. #3 FOCUS YOUR EFFORTS FUTURELAB

- 40. WHERE SHOULD YOU FOCUS? FUTURELAB

- 41. FUTURELAB WHICH IS THE EASIEST PATH TO WALK? Photo: StuSeeger, cc 2.0

- 42. AIRLINES BANKS COMPUTERS INNOVATORS SEEM TO DISAGREE PHARMA UTILITIES PROCESSED FOOD Source: The Doblin Group FUTURELAB

- 43. THIS ALSO APPLIES TO CUSTOMER CENTRIC INNOVATION 1. I dream of going on holiday 2. I research my holiday 3. I plan my holiday 4. I select my holiday 5. I purchase my holiday 6. I receive travel documents & tickets 7. I prepare my trip 8. I travel to my destination Observation 9. I discover my destination Most of the travel 10. I experience my destination industry focuses on 11. I record my memories those areas which have 12. I share my experience least or most negative 13. I travel back home emotional involvement 14. I share my memories FUTURELAB

- 44. DEBATE: ARE YOU A PENGUIN? FUTURELAB

- 45. CROSS YOUR INNOVATION LANDSCAPE WITH THE CUSTOMER ENGAGEMENT High Opportunities for Areas to keep up meaningful or stay ahead Customer Engagement differentiation Copy when Look at the niches proven only Low Low Innovation Intensity High FUTURELAB

- 46. #4 MAKE SURE YOUR PEOPLE ARE WITH YOU FUTURELAB

- 47. perception 80% of CEO‟s believe of believe their brand provides a superior customer experience 8 % of their customers agree (Bain & Company) FUTURELAB

- 48. Watch video on: http://www.youtube.com/watch?v=xa aAYVUWP0I We show that we value our customers by serving them well, putting their needs and interests at the center of everything we do. (from the AOL mission statement) FUTURELAB

- 50. FUTURELAB ONLY 5% OF THE WORKFORCE UNDERSTANDS THE STRATEGY (when innovating this gets even worse). Source: Norton, D. Aligning your Strategy to the Customer Value Proposition, 13/9/2005

- 51. WHILE THEY NEED TO DELIVER THE RETAIL (INNOVATION) PROMISE. FUTURELAB

- 52. 76% of consumers don‟t believe that companies tell the truth in advertisements Yankelowich,2006 FUTURELAB

- 53. FUTURELAB BUT PEOPLE TYPICALLY DON‟T HAVE “EMOTION MANAGEMENT” IN THEIR JOB DESCRIPTION

- 54. WHEN YOU INNOVATE, TRANSLATE INTO 6 DIRECTIONS Remarkable Practice: Gemalto

- 55. FUTURELAB Remarkable Practice: Gemalto

- 56. #5 START SWIMMING YOU FUTURELAB

- 57. 5 To Customer 1. Take the Customer Perspective Centric Retail 2. Get the Customer Heartbeat Innovation 3. Focus Your Efforts 4. Make Sure your People Are With You steps 5. Start Swimming FUTURELAB

- 58. AND DON’T FORGET TO STEAL WITH PRIDE

- 59. AND THEN WE WERE GOING TO HAVE A WORD ABOUT POP Systems Online FUTURELAB

- 60. THOUGHTS ON DIGITALLY AUGMENTED RETAIL FUTURELAB

- 61. Internet Mobile In-store Digitally Augmented Retail THREE PRACTICAL OPPORTUNITIES FUTURELAB

- 62. “Out of 35 European premium brand dealers 2007 Retail Study for Customer Focused Excellence (N = 300 large online retailers) only 1 responded to an email enquiry from their • 61% do not offer any information on the product page regarding own website … after 2 in-stock availability weeks” • 38% of sites have difficult to read fonts • Only 58% correctly answer an e-mail question within 24 hours • Only 33% offer customer reviews. • 24% do not allow customers to enlarge the product image Source: FutureNow, 2007 INTERNET IF YOU PLAY, GET THE BASICS RIGHT FUTURELAB

- 63. Hi Joel, Sorry if we weirded you or your friend out by US Online Review Users Identifying Review as following you on twitter. @JetBlue isn‟t a bot, it‟s merely me and my team keeping our ears to the Having Significant Influence on their Purchase ground and listening to our customers talk in open forums so we can improve our service to them. It‟s Category % not marketing, it‟s trying to engage on a level other than mass broadcast, something I personally Restaurant 79% believe more companies should try to do. Hotels 87% Because corporate involvement in social media is a Travel 84% new and evolving discipline, I also take a specific interest on conversations revolving around our role Automotive 78% here. I‟d have DMd you and Lisa directly if you allowed DMs, so please also forgive me for following Home 73% the link on your twitter page here to send you this note. Medical 76% You and Lisa are no longer being „followed‟ as you seem to indicate. Legal 79% Again, my apologies Source: Comscore Inc., the Kelsey Group, Oct. 2007 Morgan Johnston Corporate Communications JetBlue Airways INTERNET LISTEN AND REACT FUTURELAB

- 64. FUTURELAB KEEP IT SIMPLE ON THE MOBILE FRONT On-Demand SMS push Location Based Push ! RELEVANCE PERMISSION INFORMATIONAL (PART OF EXPERIENCE) PROMOTIONAL

- 65. IN-STORE INSPIRATION Watch video on http://www.youtube.com/watch?v=gQBFaVfBi9w&feature=related# FUTURELAB

- 66. WATCH THE CONTENT Queen‟s Arcade (Cardiff) McDonalds Amsterdam Veritas Antwerp INSTORE LESSONS IN NARROWCASTING FUTURELAB

- 67. ROMANIA IS ON THE VERGE OF SOMETHING BIG Turnover of Retail Trade in Romania 2001-2007, 2010 (€ billions) COPY MODIFY CREATE DEGREE OF INNOVATION FUTURELAB

- 68. THOSE WHO INNOVATE WIN FUTURELAB

- 69. FUTURELAB GO !!

- 70. FUTURELAB For more information contact Alain Thys via info@futurelab.net Or read up on the Futurelab blog at: http://blog.futurelab.net

Editor's Notes

- http://en.wikipedia.org/wiki/Sukiennice

- http://en.wikipedia.org/wiki/Supermarket

- When you look at the various aspects that drive recommendation in ICT markets, you find the product, yet also key experience variables like Reputation (trust), meeting needs (personalisation), ease of doing business, …Apple has addressed each of these elements with a number of unique elementsCareful segmentation allows them to better match the needs of opinion leaders The retail experience with highly knowledgeable staff who literally « lives » the brand has shifted focus from « the sale of a PC and after-sales » to a « hangout for sales, and after sales support + community building)Scenario and lifestyle marketing & sales has further allowed them to package and tailor their offer around computer usage rather than function (e.g. music, video, …)They have stuck to their own styling, which has enhanced the prodcut experience (you cannot live without a good product)

- When you look at the various aspects that drive recommendation in ICT markets, you find the product, yet also key experience variables like Reputation (trust), meeting needs (personalisation), ease of doing business, …Apple has addressed each of these elements with a number of unique elementsCareful segmentation allows them to better match the needs of opinion leaders The retail experience with highly knowledgeable staff who literally « lives » the brand has shifted focus from « the sale of a PC and after-sales » to a « hangout for sales, and after sales support + community building)Scenario and lifestyle marketing & sales has further allowed them to package and tailor their offer around computer usage rather than function (e.g. music, video, …)They have stuck to their own styling, which has enhanced the prodcut experience (you cannot live without a good product)

- Source: http://www.ifoapplestore.com/the_stores.html

- As a result, the number of Apple Advocates trends well above that of the B2C technology companies

- As a result, in spite of already being the third largest computer and office equipment company in the Fortune 500, Apple still captures growth rates will in excess of any of its competitors.

- So as consultants always like to do graphs I would summarize this in a framework which takes a bit broader perspective yet in broad terms says the same things.

- Mass value: Aldi, ikeaSolver: vodafone storeOpportunitist: apple store, zara, virgin megastore, Lifestyle: Nespresso, Lexus,