2018 DRR Financing 4.2 Yusuke Taishi

- 1. 1 Weather Index-Based Insurance What have we learned so far? Yusuke Taishi UNDP Bangkok Regional Hub

- 2. 2 The promises of index-based insurance • No moral hazards • No adverse selection • Faster payouts • Lower transactions • More affordable insurance • Greater outreach • Improved protection for vulnerable farmers

- 3. 3 Experience from the Philippines • 2013-2016 • Outreach: 2,500 farmers • Products • Excess rainfall • Low and excess •Premiums • Php 694 (US$13)/ha for Excess rainfall • Php 1,390 (US$26)/ha for Low and excess • Amount of cover: Php 20,000 (US$370) • 178 out of 2,500 received payouts

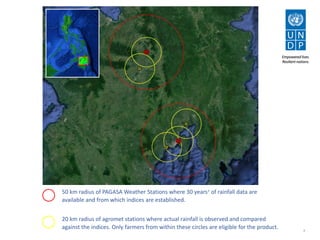

- 4. 4 50 km radius of PAGASA Weather Stations where 30 years+ of rainfall data are available and from which indices are established. 20 km radius of agromet stations where actual rainfall is observed and compared against the indices. Only farmers from within these circles are eligible for the product.

- 6. 6 Technical issues with indexing ➊ Originally… VEGETATIVE REPRODUCTIVE MATURITY

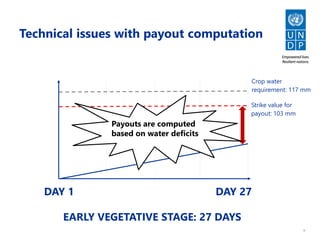

- 7. 7 Technical issues with indexing ➊ DAY 1 EARLY VEGETATIVE STAGE: 27 DAYS DAY 27 Strike value for payout: 103 mm Crop water requirement: 117 mm

- 8. 8 Technical issues with indexing ➊ During the project… Daily water requirements were calculated based on a physiological analysis of rice varieties

- 9. 9 Technical issues with payout computation DAY 1 EARLY VEGETATIVE STAGE: 27 DAYS DAY 27 Strike value for payout: 103 mm Crop water requirement: 117 mm Payouts are computed based on water deficits

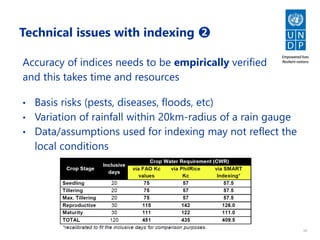

- 10. 10 Technical issues with indexing ➋ Accuracy of indices needs to be empirically verified and this takes time and resources • Basis risks (pests, diseases, floods, etc) • Variation of rainfall within 20km-radius of a rain gauge • Data/assumptions used for indexing may not reflect the local conditions

- 11. 11 Technical issues with indexing ➋ Verification of accuracy and continuous improvements of indices are important because… Farmers’ trust in insurance can erode quickly

- 12. 12 Lessons for scaling, sustainability and impact Political economy Food security Subsidy policy • “Right” level of subsidy tends to become more politically- driven than technically- or economically-driven • Crowding out effects of subsidy and discouragement of product design need to be recognized

- 13. 13 Lessons for scaling, sustainability and impact Weaknesses of weather index insurance Conventional insurance • Only one climate risk can be covered • Only weather risks that show high correlation with yields can be covered Perennial crops are harder to insure Use of technology • Covers multiple risks • More intuitive • Making conventional insurance more attractive for insurers • Remote sensing technology Cost-benefit of other interventions • Irrigation vs subsidized insurance

- 14. 14 Lessons for scaling, sustainability and impact Poverty reduction • Poverty reduction impact is generally not tracked • If insurance is bundled with other financial services, does insurance make farmers better borrowers? • Often, payouts cover only production inputs, not income from full harvests Bundling with financial services Amount of payouts

- 15. 15 New work in Burkina Faso • Starting in 2019 • Bundling with financial products • Resilient agricultural practices to address basis risks