European sovereign debt crisis

Download as PPTX, PDF11 likes12,369 views

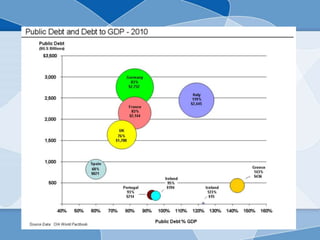

The European sovereign debt crisis began in late 2009 as fears grew over rising private and government debt levels in Europe. Greece, Ireland, and Portugal were hit hardest initially, accounting for 6% of Eurozone GDP combined. By 2012, concerns had spread to Spain as well. The crisis impacted EU politics and led to leadership changes in affected countries. Key causes included rising household and government debts, trade imbalances, structural issues in sharing a currency without a common fiscal policy, monetary policy inflexibility within the Eurozone, and loss of investor confidence. Long term solutions proposed integrating fiscal policies more through options like a European fiscal union or common Eurobonds.

More Related Content

What's hot (20)

Viewers also liked (17)

Similar to European sovereign debt crisis (20)

Recently uploaded (20)

European sovereign debt crisis

- 2. INTRODUCTION • From late 2009, fears of a sovereign debt crisis developed among investors as a result of the rising private and government debt levels around the world together with a wave of downgrading of government debt in some European states. • Three countries significantly affected, Greece, Ireland and Portugal, collectively accounted for 6% of the eurozone's gross domestic product (GDP).

- 3. •In June 2012, also Spain became a matter of concern, when rising interest rates began to affect its ability to access capital markets, leading to a bailout of its banks and other measures. •The crisis has had a major impact on EU politics, leading to power shifts in several European countries, most notably in Greece, Ireland, Italy, Portugal, Spain, and France.

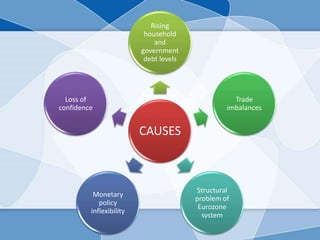

- 5. CAUSES Rising household and government debt levels Trade imbalances Structural problem of Eurozone system Monetary policy inflexibility Loss of confidence

- 6. Rising household and government debt levels • A number of economists have dismissed the popular belief that the debt crisis was caused by excessive social welfare spending. • According to their analysis, increased debt levels were mostly due to the large bailout packages provided to the financial sector during the late-2000s financial crisis.

- 7. • The average fiscal deficit in the euro area in 2007 was only 0.6% before it grew to 7% during the financial crisis. • The International Monetary Fund (IMF) reported in April 2012 that in advanced economies,the ratio of household debt to income rose by an average of 39 percentage points, to 138 percent in Denmark, Iceland, Ireland, the Netherlands.

- 8. • In the same period, the average government debt rose from 66% to 84% of GDP. • By the end of 2011, real house prices had fallen from their peak by about 41% in Ireland, 29% in Iceland, 23% in Spain and the United States, and 21% in Denmark.

- 10. TRADE IMBALANCES • A trade deficit can also be affected by changes in relative labor costs, which made southern nations less competitive and increased trade imbalances. • Since 2001, Italy's unit labor costs rose 32% relative to Germany's. • Greek unit labor costs rose much faster than Germany's during the last decade.

- 12. STRUCTURAL PROBLEM OF EUROZONE SYSTEM • There is a structural contradiction within the euro system, namely that there is a monetary union without a fiscal union (e.g., common taxation, pension, and treasury functions). • In the Eurozone system, the countries are required to follow a similar fiscal path, but they do not have common treasury to enforce it.

- 13. • That is, countries with the same monetary system have freedom in fiscal policies in taxation and expenditure. • Eurozone, having 17 nations as its members, require unanimous agreement for a decision making process.

- 14. • This would lead to failure in complete prevention of contagion of other areas, as it would be hard for the Euro zone to respond quickly to the problem. • That is, countries with the same monetary system have freedom in fiscal policies in taxation and expenditure

- 15. MONETARY POLICY INFLEXIBILITY • Eurozone establishes a single monetary policy, individual member states can no longer act independently, preventing them from printing money in order to pay creditors and ease their risk of default. • By "printing money", a country's currency is devalued relative to its (eurozone) trading partners, making its exports cheaper,increased GDP and higher tax revenues in nominal terms.

- 16. LOSS OF CONFIDENCE • The loss of confidence is marked by rising sovereign CDS (credit-default swaps) prices, indicating market expectations about countries creditworthiness. • Since countries that use the euro as their currency have fewer monetary policy choices certain solutions require multi-national cooperation.

- 18. IRELAND • The Irish sovereign debt crisis was not based on government over-spending, but from the state guaranteeing the six main Irish-based banks who had financed a property bubble. • Irish banks had lost an estimated 100 billion euros, much of it related to defaulted loans to property developers and homeowners made in the midst of the property bubble, which burst around 2007.

- 19. • Unemployment rose from 4% in 2006 to 14% by 2010, while the national budget went from a surplus in 2007 to a deficit of 32% GDP in 2010, the highest in the history of the eurozone, despite austerity measures.

- 21. PORTUGAL • Portugal requested a €78 billion IMF-EU bailout package in a bid to stabilise its public finances. • These measures were put in place as a direct result of decades-long governmental overspending and an over bureaucratised civil service. • On 16 May 2011, the eurozone leaders officially approved a €78 billion bailout package for Portugal, which became the third eurozone country, after Ireland and Greece, to receive emergency funds.

- 22. • The average interest rate on the bailout loan is expected to be 5.1 percent. As part of the deal, the country agreed to cut its budget deficit from 9.8 percent of GDP in 2010 to 5.9 percent in 2011, 4.5 percent in 2012.

- 23. Proposed long-term solution European fiscal union Eurobonds European Monetary Fund Drastic debt write-off financed by wealth tax Debt defaults and national exits from the Eurozone

- 24. EUROPEAN FISCAL UNION • Increased European integration giving a central body increased control over the budgets of member states. • Control, including requirements that taxes be raised or budgets cut, would be exercised only when fiscal imbalances developed.

- 25. EUROBONDS • A growing number of investors and economists say Eurobonds would be the best way of solving a debt crisis though their introduction matched by tight financial and budgetary coordination may well require changes in EU treaties. • On 21 November 2011, the European Commission suggested that Eurobonds issued jointly by the 17 euro nations would be an effective way to tackle the financial crisis.

- 26. EUROPEAN MONETARY FUND • On 20 october 2011, the austrian institute of economic research published an article that suggests transforming the efsf into a european monetary fund (emf), which could provide governments with fixed interest rate eurobonds at a rate slightly below medium-term economic growth • These bonds would not be tradable but could be held by investors with the EMF and liquidated at any time.

- 27. DRASTIC DEBT WRITE-OFF FINANCED BY WEALTH TAX • To reach sustainable levels the eurozone must reduce its overall debt level by €6.1 trillion. • According to BCG this could be financed by a one-time wealth tax of between 11 and 30 percent for most countries, apart from the crisis countries (particularly Ireland) where a write-off would have to be substantially higher.

- 29. DEBT DEFAULTS AND NATIONAL EXITS FROM THE EUROZONE • In mid May 2012 the financial crisis in Greece and the impossibility of forming a new government after elections led to strong speculation that Greece would have to leave the Eurozone shortly. • This phenomenon had already become known as "Grexit" and started to govern international market behaviour.