Financial planning

•Download as PPTX, PDF•

2 likes•519 views

Personal Financial Planning - Emergency Fund, Health Insurance, Life Insurance, Goals Planning - Child Education, Child Marriage, Retirement Planning

Financial planning

- 1. Financial Planning Emergency Fund Health Insurance Life Insurance Goals Planning Retirement Planning

- 2. Emergency Fund Emergencies like Job Loss, Medical emergency 3-6 times of monthly expenses Instruments Liquid Funds Fixed Deposit Saving Account

- 3. Protection Protecting Your Resources Protect your income Life insurance, Disability insurance Protect your wealth Property and casualty Protect you Health insurance

- 4. Health Insurance Family Floater Dependant Parents Sum Assured 3-5 lakhs Important Points to consider Lifelong Renewal Loading on claim No Co-payment No Submits No Room Rent Capping

- 5. Health Insurance … Other Insurance Accidental Insurance Critical illness Travel Insurance

- 6. Life Insurance Go for Term Insurance 10 – 20 times of annual earning Consider Monthly Expenses + Liabilities - Financial Assets - Existing Cover SA 1 Cr – Premium 10-12 K

- 7. Life Insurance • Premium Payment - Single Premium or Yearly Premium • Take Cover Up to 60 Years Age

- 8. Goals Identify financial goals ◦ Present Value ◦ Time to achive Categories – Short Term , Long Term

- 9. Goals Typical Personal Goals like ◦ Child Education ◦ Child Marriage ◦ Retirement ◦ Home Loan Repayment ◦ Buy new house – down payment ◦ Buy new car – down payment

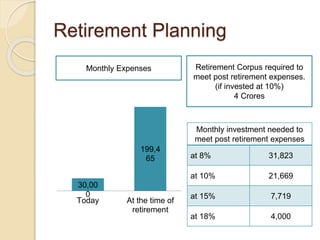

- 10. Retirement Planning Monthly Expenses 30,00 0 199,4 65 Today At the time of retirement Retirement Corpus required to meet post retirement expenses. (if invested at 10%) 4 Crores Monthly investment needed to meet post retirement expenses at 8% 31,823 at 10% 21,669 at 15% 7,719 at 18% 4,000

- 11. Child’s Education Educational Degree 1,000, 000 2,759, 032 Present When your child actually goes for degree Monthly investment needed to achieve this goal at 8% 7,920 at 10% 6,602 at 15% 4,076 at 18% 3,002

- 12. Start Early Starting early helps you spend time in the market and gain from Power of Compounding Mahesh Suresh Age 21 years Age 21 years Rs 5000 each year for next 14 years and then he lets that money sit until he is 55 Wait until he is 35 and then invest Rs 5000 a year until he is 55 earn 8.7% per year earn 8.7% per year

- 13. Start Early Mahesh Suresh Monthly ₹ 5,000 ₹ 5,000 Rate of Return 8.7% 8.7% Investment Up to (Years) 14 20 Investment Amount ₹ 8,40,000 ₹ 12,00,000 Investment Value at end of regular investment ₹ 16,43,276 ₹ 32,38,269 Years after regular investment 20 0 Maturity Amount ₹ 93,03,721 ₹ 32,38,269 Difference of ₹ 60,65,452 Suresh would have to increase his contribution to Rs 14,365 (additional 9,365) to 'catch up' to Mahesh

- 14. Tax Benefits Comparison Under 80C Instrument under 80c Lock in Period Returns Taxation Aspect ELSS 3 years Market-Linked Dividend & Capital Gain tax free PPF 15 years 8.7% Interest tax free Tax Saving FD 5 years 8.5% Interest taxable NSC 5/10 years 8.50% Interest taxable ULIP 5 years Market-Linked Maturity/claims tax free EPF Till Termination of employment 8.75% Interest tax free

- 15. ELSS SIP Return Fund Name No of Installme nts Investme nt Amount(I NR) XIRR (%) SIP Mode One Time Mode Axis Long Term Equity Growth 36 180000 45.29 336837.4 447530.6 Reliance Tax Saver (ELSS) Fund Growth 36 180000 45.34 337045.4 409432.5 ICICI Prudential Tax Plan Growth 36 180000 33.43 289365.8 361228 IDFC Tax Advantage (ELSS) Fund - Regular Plan - Growth36 180000 38 307112 387732.5 Birla Sun Life Tax Plan Growth 36 180000 38.17 307777.4 381660.3 Franklin India Taxshield Fund Growth 36 180000 35.81 298529 361118 Axis Long Term Equity Growth 60 300000 31.51 649779.8 861306.1 Reliance Tax Saver (ELSS) Fund Growth 60 300000 29.98 626692.8 776992.7 ICICI Prudential Tax Plan Growth 60 300000 23.1 531778.9 640979.4 IDFC Tax Advantage (ELSS) Fund - Regular Plan - Growth60 300000 25.56 564164.8 673008 Birla Sun Life Tax Plan Growth 60 300000 25.23 559729.2 645440.5 Franklin India Taxshield Fund Growth 60 300000 24.72 552929 686054.1 Investment Value (INR)

Editor's Notes

- Who will have the most?

- Who will have the most?

- Equity-oriented funds with a lock-in of three years. Qualifies for deduction upto Rs 1.5 lakh under Section 80C of the Income Tax Act