Raising Long Term Funda

•Download as PPT, PDF•

0 likes•615 views

This document discusses sources of long term funds for businesses through equity and debt financing. Equity sources include funds contributed by promoters, private equity investments, and public offerings like IPOs, FPOs, rights issues, and QIPs. Private companies rely mainly on promoter equity while public companies can also raise funds through public markets. Debt includes loans from financial institutions or issuing debentures. Debentures are rated based on their safety and risk of default. Higher ratings from AAA to BBB signify more safety while lower ratings from BB to D mean higher risk. Overall the document provides an overview of different long term financing methods for businesses.

Report

Share

Raising Long Term Funda

- 1. Raising Long Term FundsRaising Long Term Funds

- 2. Balance Sheet: Sources of Long Term Fund 1. A : Paid up Equity : (Common and Preference) 1. B: Reserve and Surplus 2. A: Secured Debt (L.T.) 2. B. Un-Secured Debt (L.T.) : e.g. Debentures 09/19/13

- 3. LOOKING FOR LONG TERM FINANCING • What Amount do I need? • How do I raise the Fund? Is it through Equity Or Debt? • What Information Do I Need To Provide The Lender/Investor? • If I finance it through Debt, what are the Repayment Terms? Do I have to Pay Interest? If so, will it vary over Time Or Fixed? • How long will it take to acquire the Funds? What will be the Floatation Cost? 09/19/13

- 4. FINANCING METHODS • LONG TERM FINANCING: Equity and Debt • Framework for Business Organisations raising various funds 09/19/13

- 5. Sources of Equity • Promoter Contributing the entire Capital • Private Placement (PE or VC Funding) • Going to Public by an IPO FPO Rights QIP 09/19/13

- 6. Private Limited Companies • They Cannot go to Public to Raise Equity • Share Transfer and Issue is restricted and subject to permission from RoC • Promoter Contributing the entire Capital (Most Common) • Private Placement (PE or VC Funding) 09/19/13

- 7. PRIVATE EQUITY FUNDS • A fund that invests in companies and/or entire business units with the intention of obtaining a controlling interest (usually by becoming a majority shareholder, sometimes by becoming the largest plurality shareholder) so as to be in the position of restructuring the target company's reserve capital, management, and organizational infrastructure. 09/19/13

- 8. Public Limited Companies • They can go to Public to raise Equity via Primary Market Segment of Capital Market • It can be new Public Ltd. Co Formation or conversion from Pvt. Ltd • Promoter Contributing substantial part of the equity capital and hence, in most cases, have controlling stake • Private Placement (PE or VC Funding) • Going to Public by an IPO FPO Rights QIP 09/19/13

- 9. Initial Public Offer (IPO) • Promoter initiating the formation of Public Ltd. Co • The Team of Banker, Investment Banker, R&T Agent • Role of SEBI • Authorised Share Capital, Face Value of one share, Authorised No of shares, Intended Share holding pattern • Book Building Issue: Offer Price determination • Issue of Prospectus • Application: Lot size and Application Money • Under, Par and Over-subscription • Allocation for Over and Par Subscription • 5 possibilities of Under-subscribed issue 09/19/13

- 10. Under-subscribed issue 5 possibilities of Under-subscribed issue 1. Issue is cancelled and IPO is re-launched after Cooling Period 2. More time is sought from SEBI and cut off date extended 3. Promoter picks up the rest of the unsubscribed share 4. Underwriters pick up the rest or Underwriter-promoter combined picks up the rest 5. Only shares which are subscribed are issued, thus raising less than the required fund through Equity 09/19/13

- 11. FPO, Rights, QIP • Follow-up Public Offer: Same steps as an IPO • Cooling period needed after an IPO • Offer Price is determined based on the market Response • Rights Issue is restricted to the existing shareholder only • Qualified Institutional Placement (QIP) is used when Market response for FPO or Rights is uncertain 09/19/13

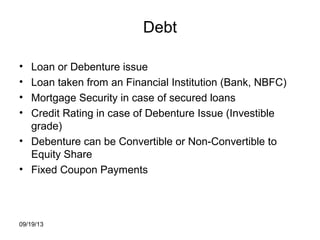

- 12. Debt • Loan or Debenture issue • Loan taken from an Financial Institution (Bank, NBFC) • Mortgage Security in case of secured loans • Credit Rating in case of Debenture Issue (Investible grade) • Debenture can be Convertible or Non-Convertible to Equity Share • Fixed Coupon Payments 09/19/13

- 13. RATING SYMBOLS

- 14. High Investment Grades AAA - (Triple A) Highest Safety • Debentures rated ‘AAA’ are judged to offer highest safety of timely payment of interest and principal.

- 15. • AA - (Double A) High Safety • Debentures rated ‘AA’ are judged to offer high safety of timely payment of interest and principal. They differ in safety from ‘AAA’ issues only marginally.

- 16. Investment Grades • A - Adequate Safety • Bonds rated ‘A’ are judged to offer adequate safety of timely payment of interest and principal. However, changes in circumstances can adversely affect such issues more than those in the higher rated categories.

- 17. BBB (Triple B) Moderate Safety • Debentures rated ‘BBB’ are judged to offer moderate safety of timely payment of interest and principal for the present; however, changing circumstances are more likely to lead to a weakened capacity to pay interest and repay principal than for debentures in higher rated categories.

- 18. Speculative Grades BB (Double B) Inadequate Safety • Debentures rated ‘BB’ are judged to carry inadequate safety and principal, the uncertainties that the issuer faces could lead to inadequate capacity to make timely interest and principal payments.

- 19. B - High Risk • Debentures rated ‘B’ are judged to have greater susceptibility to default; while currently interest and principal payments are met, adverse economic conditions would lead to lack of ability or willingness to pay, interest or principal.

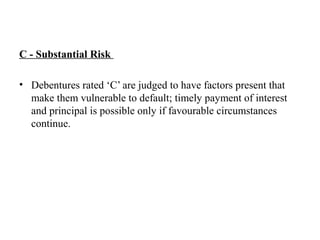

- 20. C - Substantial Risk • Debentures rated ‘C’ are judged to have factors present that make them vulnerable to default; timely payment of interest and principal is possible only if favourable circumstances continue.

- 21. D - Default • Debentures rated ‘D’ are in default and in arrears of interest or principal payments or are expected to default on maturity. Such debentures are extremely speculative and return from these debentures may be realized only on liquidation. • Rating agencies may apply ‘+’ (plus) or ‘-’ (minus) signs for ratings from AA to C to reflect comparative standing within the categories.

- 22. Thank You