Hyundai Strategy

•

30 likes•32,481 views

1) The document discusses Hyundai's entry and growth in the Indian hatchback market, facing initial challenges in convincing customers to accept a Korean brand. 2) It analyzes Hyundai's marketing strategies over the years to launch and position the Santro model, becoming the #2 carmaker in India through strong branding. 3) Market trends are discussed, showing growth in compact vehicles and declining micro segment, with opportunities for Hyundai in India's underpenetrated car market.

Report

Share

Hyundai Strategy

- 1. Strategy Formulation Sec A Group 5 Abhay Sharma 1A Aniruddh Srivastava 9A Devansh Doshi 16A Manasi Jain 23A Sachin Gupta 38A Vidooshi Joshi 55A

- 2. Agenda Segment Strategic Elements Forces Trend Analysis Future Projections Vision Strategy

- 3. Market share of different types of PV in India 60%17% 11% 12% Sales Hatchback Sedan SUV MPV Market Share by Brand of different Hatchbacks 49% 22% 12% 4% 3% 3% 3% 2% 2% Maruti Suzuki Hyundai Tata Motors Ltd Ford General Motors Honda Volkswagen Toyota Others Monthly sales for Indian hatchback manufacturers 2012- 13 Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Hatchback Segment • Hyundai entered in 1996 in India and has become 2nd largest car manufacturer and largest passenger car exporter for 7 years in a row • Market share of 14.4% in PV segment, 2nd to MSIL • Currently has Eon, Santro, i10, Grand i10, i20 in hatchback segment Segment

- 4. 1. Indians were unsure about Korean products especially automobiles. First task was to develop a positive association with Indian customers 2. Developing a corporate image for Hyundai. Since cars are high involvement product, customers will make a choice looking on the maker, service support, spares availability , quality etc. Hence the launch of Santro should also launch the corporate brand Hyundai. 3. The design of Santro. Santro was designed to be a tall boy car and initial product testing revealed that Indians did not liked the tall boy design. So the unenviable task for Hyundai was to make Indian consumers like Santro. 4. The grip of Maruti on the Indian car market. The B segment was dominated by Zen which has proved itself to be a reliable workhorse. Zen was the preferred and logical upgrade to 800 and the car was considered to be the most reliable and powerful in that segment. To convert the potential Zen users to Santro was really a nightmare for any marketer. Challenges for Hyundai to launch Santro in 1998 The first ad introduced the brand and the company with a subtle statement : We settle only for the best -> Followed by teaser ads which depicted Shah Rukh being convinced to believe that Hyundai is serious about India, the quality issue and the brand Santro. Finally came the launch ad which showed Shah Rukh who represented the Indian consumer saying " I am Convinced" . Repositioning – Santro variant Changed design and launched under the name Santro Xing. Appeal to first time car buyers not as an upgrade for 800. TG was 25-30 years. Positioned as Sunshine car and roped Priety Zinta as the brand ambassador. Positioning Family Car targeting maruti suzuki 800 users who wanted to upgrade. TG was 35-45 years middleclass Indians. Ugly Car – Tall boy design Performance, design aspect – turned biggest disadvantage into advantage Runaway success within 4 years of its launch displaced Zen as the second largest selling car in India Santro – the sunshine story Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Segment

- 5. India’s hatchback segment over the years Other compact cars like Matiz, Fiat Uno, Palio failed to gain traction in the market and were phased out. Maruti Suzuki 800, Alto, Tata Indica and Hyundai Santro practically owned the hatchback segment until the recent entry of the foreign players. Mini models dominated the market for most of the past decade but now the sales of the compact cars lead the hatchback segment and 12 brands are producing models Maruti took hold of the hatchback market in 1980s when it introduced the Maruti 800, a customised car aimed at India’s mass market which dislodged Hm’s Ambassador from pole position. For an auto sector where previous decade annual sales were 35,000-40,000 units Maruti was manufacturing and selling 100,000 cars a year. HMIL in 1998 became the first carmaker to seriously challenge Maruti’s dominance by launching Santro, which was a runaway success and became the segment’s no.1 seller within the year it was launched. Maruti introduced WagonR in response but the car did not enter the market for 2 years due to production cycle issues. Tata Motors announced India’s first totally homegrown passenger car, the Indica, in 1998. Its rugged look was an instant hit. Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Segment

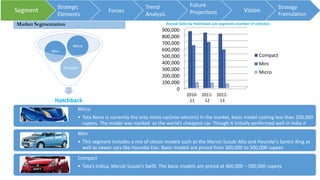

- 6. Market Segmentation Hatchback Compact Mini Micro 0 100,000 200,000 300,000 400,000 500,000 600,000 700,000 800,000 900,000 2010- 11 2011- 12 2012- 13 Compact Mini Micro Annual Sales by Hatchback sub-segments (number of vehicles) Micro • Tata Nano is currently the only micro car(non-electric) in the market, basic model costing less than 200,000 rupees. The model was marked as the world’s cheapest car. Though it initially performed well in India it has been struggling off late Mini • This segment includes a mix of classic models such as the Maruti Suzuki Alto and Hyundai’s Santro Xing as well as newer cars like Hyundai Eon. Basic models are priced from 300,000 to 500,000 rupees Compact • Tata’s Indica, Maruti Suzuki’s Swift. The basic models are priced at 400,000 – 500,000 rupees Forces Trend Analysis Future Projections Vision Strategy Fromulation Strategic Elements Segment

- 7. Sales vs Price positioning of key hatchback models Source: SIAM Customers want value for money not just a low priced car Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Segment

- 8. Specification Comparison Specification Maruti Suzuki Alto 800 Vxi Hyundai Eon Magna+ Cost INR 3.25 Lakh INR 3.5 Lakh Displacement (cc) 796 814 Mileage (ARAI) (kmpl) 22.74 21.4 Central Locking Yes Remote 12V Power Outlets - 1 Adjustable Head-rests X Front & Rear Seat Belt Warning X Present Door Ajar Warning X Present Steering Adjustment X Tilt Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic elements Segment

- 9. Specification Maruti Suzuki Wagon R Hyundai i10 Sportz Cost INR 4.34 Lakh INR 4.36 Lakh Displacement (cc) 1197 1197 Mileage (ARAI) (kmpl) 20.5 19.81 Anti-Lock Braking System X Present Central Locking Present Remote Airbags X 2 (Driver & Co-Driver) Rain-sensing Wipers X Present Fog Lamps Front Front & Rear USB Compatibility X Present Specification Comparison Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic elements Segment

- 10. • Only 13 cars per 1000 people • 60% of the PV market is Hatchback segment • Consumers are informed and they are value driven • Huge growth potential for HMIL CAR DENSITY •Emerging markets are slowing • Manufactured cars which suit Indian roads and Indian consumer tastes. • Disposable income level is at a constant increase -> the number of first time buyers is huge •Rapid urbanization – increase in Rural demand •100% FDI in the automotive sector • Govt. has granted concessions, such as reduced interest rates for export financing. Weighted tax deduction of up to 150% for in-house research and R & D activities •Several Indian firms have partnered with global players. While some have formed joint ventures with equity participation, other also has entered into technology tie-ups. Establishment of India as a manufacturing hub, for mini, compact cars, OEMs and for auto components. • Economies of scale achieved by existing players hard to surpass and difficult to discount. • Existing distribution channels : these channels lend an unparalleled advantage to established players, almost impossible to replicate • Existing service networks: these networks lend great strengths to established players, impossible to counter • Preference for small and compact cars. They are socially acceptable even amongst the well off. Preference for fuel efficient cars with low running costs • More and more emphasis is being laid on R & D activities carried out by companies in India • Minimum fuel efficiency norms for Passenger Vehicles - 14 % increase in mileage by 2016-17 - CAFC SOCIETAL FACTORS • Large and growing domestic auto market • Competition is huge in this segment – 12 brands are competing against each other in the hatchback segment • HMIL has market share of 48% of the total exports of PV from India TASK ENVIRONMENT EXTERNAL ENVIRONMENTAL FACTORS Trend Analysis Future Projections Vision Strategy Formulation Segment Forces Strategic elements

- 11. • Hyundai is known for its innovation • To give good quality used cars to Indian Customers. Vehicles are certified by Hyundai Engineers using 147 check points • Creating brand image among consumers through aggressive investment in advertisement and sponsorships • Hyundai products are not as cost effective since it doesn’t compromise on its quality • Human centric, eco-friendly technologies and services INNOVATION • Will have to increase its rural reach • High brand equity - Korean manufacture has become an Indian brand due to its long time presence in the Indian market • Perceived as value for money vehicle which does not compromise on its quality • India is a cricket crazy nation so tie ups with ICC the best possible marketing strategy BRAND POSITIONING • Management philosophy - . Realization of Possibilities, Unlimited sense of Responsibility , Respect for Mankind • Core Values – Customer, Challenge, Collaboration, People, Globality • Frequent change in management not good for the organization • Car sales dropped in July 2012 when the sales and marketing head resigned COMPANY CULTURE & VALUES INTERNAL ENVIRONMENTAL FACTORS Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic elements SegmentSegment

- 12. OPPORTUNITIES THREATS Car Density • Tremendous growth opportunity for Hyundai in hatchback segment Societal Factors • Disposable income level is at a constant increase -> the number of first time buyers is huge • 100% FDI in the automotive sector Government concessions Task Environment • Large and growing domestic auto market Innovation • Human centric, eco-friendly technologies and services • Govt. has granted concessions, such as reduced interest rates for export financing. Weighted tax deduction of up to 150% for in-house research and R & D activities Brand Positioning • Perceived as value for money vehicle which does not compromise on its quality • High brand equity - Korean manufacture has become an Indian brand due to its long time presence in the Indian market Societal Factors • Emerging markets are slowing • Poor service network of Hyundai - Existing service networks lend great strengths to established players, impossible to counter • Preference for fuel efficient cars with low running costs Task Environment • Competition is huge in this segment – 12 brands are competing against each other in the hatchback segment Brand Positioning • Will have to increase its rural reach Company Culture & Values • Frequent change in management not good for the organization Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic elements Segment

- 13. Per Capita GDP Borrowing Rate Automotive Industry on a growth phase Positive correlation with GDP growth PV density really low for India. Huge scope for hatchbacks. Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Segment

- 14. • Car sales in India fell for the first time in a decade - down 6.69 per cent in 2012-13 - as the automobile industry struggled to cope with demand slump due to a sluggish economy • The decline in passenger car sales last fiscal was also the steepest in the past 12 years when the segment declined by 7.73 per cent in 2000-01. • Interestingly, total passenger vehicle sales grew 2.15% to 2.69 million units, with people buying more sport utility vehicles (SUVs) in 2012-13 • Total sales of vehicles across categories registered a fall of 7.76 per cent to 14,86,522 units in March 2013, as against 16,11,525 units in the same month of 2012 Reasons: • High interest rates, which ranged around 11-15 per cent • High fuel prices, mainly that of petrol, also impacted car sales • Industrial output also fell in India by over 1% • Stalled infra projects and slow mining Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Segment Growth in household income vs car sales Indexed Growth of disposable income, inflation and car sales

- 15. Demand Drivers of Automobile Segment Availability of wider range of products Gradual shift to higher segment vehicles Increase in income levels and purchasing power Availability of low cost finance Decrease in vehicle changeover times Rapid urbanization and emergence of tier 2 cities/ non metros Replacement of aging four wheelers Growing Concept of second vehicle in Urban areas Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Segment

- 16. No longer seen as just basic means of affordable transport Hatchback is expected to drive the market with higher-end models competing directly with entry level sedans Mini and micro hatchbacks expected to penetrate secondary and tertiary markets; directly competing motorbike and scooter segment Expected auto industry revenue at end of FY2017: $127bn with CAGR forecast: 8%for 2013-20 The Passenger Vehicle market of India will even cross Japan by selling about 5 million Vehicles by 2017-18 The Indian auto exports will be up to $5.62 billion in the year ending March 2011 and the same will grow to $17.64 billion in 2015-16 1350000 1400000 1450000 1500000 1550000 1600000 1650000 2010-11 2011-12 2012-13 Annual Hatchback Sales Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Segment

- 17. Automotive Mission Plan 2016 Tax holiday for Automobile Industry for investment exceeding INR 500 crore One-stop clearance for FDI proposals in automotive sector Deduction of 30% of net (total) income for 10 years for new industrial undertaking State Government to be urged to offer Preferential allotment of land to automotive plants, Continuous uninterrupted power supply and promote Captive Generation Key Projects with Strategic Importance for India • NHDP Project: Largest Highway Development Project • NSEW Project: Connecting North, South & East, West lengths of India • Golden Quadrilateral: Connects 4 metros Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Segment

- 18. • PPP of India is projected to increase considerably, hence may lead to shift of customers from 2 wheelers to Cars 13.8 46.7 58.8 109.2 140.7 151.2 65.2 41 38 0 50 100 150 200 250 300 2000-01 2012-13 2015-16E Growth in Population categories with Higher incomes Low Income (<45k per month) Middle Income (Rs 45k-180k per month) High Income (> 180k per month) 70.3 76.7 89.5 100.9 113.3 127 0 20 40 60 80 100 120 140 2012 2013 2014 2015 2016 2017 Automobile Industry Growth Value (USD bn) Linear (Value (USD bn)) Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Segment

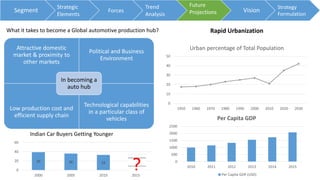

- 19. What it takes to become a Global automotive production hub? Attractive domestic market & proximity to other markets Political and Business Environment Low production cost and efficient supply chain Technological capabilities in a particular class of vehicles In becoming a auto hub Rapid Urbanization 0 10 20 30 40 50 1950 1960 1970 1980 1990 2000 2010 2020 2030 Urban percentage of Total Population 0 500 1000 1500 2000 2500 2010 2011 2012 2013 2014 2015 Per Capita GDP Per Capita GDP (USD) Indian Car Buyers Getting Younger 39 36 33 00 20 40 60 2000 2005 2010 2015 Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Segment

- 20. Future Projections: Segment wise Vehicle Production in India Change in Consumption Pattern Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Segment

- 21. Lifetime Partner in Automobiles and Beyond Car has become a life space that occupies a central role in people’s lives Hyundai seeks to become a lifetime partner in the everyday lives of customers To come one step closer to its customers and become their beloved brand. Hyundai is developing eco-friendly and human-oriented technologies for the future Taking the customer experience and satisfaction to another level Penetrate the service centers and Distributors network within tier-II and tier-III cities Aggressively pitching premium and micro hatchbacks Improving the experience of driving through tech heavy customizations Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Segment

- 22. Grand i10 (4.29L-6.41L) Grand i10 will slot into the segment above the existing i10, since Sub-compacts make up nearly 60 percent of the entire Indian car market, makes sense for Hyundai to offer Indian customers two sizes of i10 Specially Designed for Indian Market, with more boot space, Ground Clearance, rear air cond. Priced lower than chief competitor Swift, fuel-efficient, loaded with features (keyless start & go, cooled glove box) Disadvantage: More suited as a four seater, rather than 5 • Rear defogger, ABS & Airbags only on Asta (top variant). Should have been optional with the middle variant What can be done??? Automatic transmission should be included because of stop-and-go traffic of metros More focus on Mileage as Indian consumers are mileage driven Lesser price differentiation between i20 and grand i10, hence better positioning and differentiation are required 2nd in sales after Swift; more marketing efforts, service centers and distributors in rural areas is the need of the hour Hyundai service costs needs to bring down as customers now look for maintenance and after sales cost Forces: Economic Scenario: With improving economy, 5-6 lakh Premium hatchback will become the choice of 1st car purchase Favourable Customer Preference: buyer today looks to buy a car for the family and subsequently looks at the quality of the dealership for service Favorable Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Segment

- 23. i20 (4.73L-7.67L) Positives Negatives Strategy: What needs to be done? Automatic transmission Prices need to bring down to create better differentiation with compact sedans and low category sedans Overhaul engine and steering related problems as product recall might be imminent Since 2nd time buyers are most likely the user of Premium hatchback like i20, hence things like quality of the dealership for service, vehicle reliability and re-sale value should be enhanced. Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Segment

- 24. •The crude oil prices are high and are affecting the decision making Indian automobile customers •The most important factor Indians weigh now is the fuel economy of the vehicle •The biggest competitor for HMIL in India is MSIL and the positioning of its products is primarily based on mileage across segments. •Medium - Long term strategy for HMIL should be R&D and development of more fuel efficient engines, HEVs (Hybrid and electric cars) and gradually reposition some of their more fuel efficient models to take away the advantage from MSIL •Existing models of Hyundai in India are not far behind MSIL in terms of mileage •More fuel efficient vehicles would also attract more customers specially in Tier 2 and 3 cities Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Segment Global Crude Oil price

- 25. Entering into micro hatchback segment: Apart from Nano (unsuccessful), no other model exists (Short- term) Sales are continually dipping for Nano because of engine problems, wrong positioning (Cheapest). Hyundai can leverage its technology and introduce hatchback in this micro segment. Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Segment New launches: Launch in Hybrid (HEVs) car Segment Launch in Micro Hatchback Segment Toyota (Prius) and M&M have tried their luck in the segment of hybrid cars, with no success, as very high costs are involved in the production (High upfront cost, cost of energy storage despite on-going fuel savings) Develop in house R&D and develop Hybrid as annoying sky rocketing prices of fuel and can get Govts help (National Electric Mobility Mission Plan

- 26. •Working women specially in urban India have high disposable incomes and also enjoy decision making freedom •Seeing the success of Hero Pleasure and TVS Scooty Pep, Hyundai can enter with a new product especially designed for women •The positioning would be unique in India specially inclined towards women •Blue ocean strategy to enter this lucrative segment, but Hyundai must develop a car specially designed for women in India •Such experiments have been dome in the more mature economies of the west and Japan and have paid good dividends •The attraction is not only in the color of the cars but also safety feature and comfort the car provides to the driver •Competitors Honda, Nissan already have products in the category which they can launch in India when the market is ripe •Product Kia Spectra already in other markets(Kia is under Hyundai Motor Corporation) •Primary positioning is that it empowers women Forces Trend Analysis Future Projections Vision Strategy Formulation Strategic Elements Segment Women’s Car 19.7 22.3 25.7 27.5 0 50 1981 1991 2001 2011 Work Participation rate of Women