Inside Government 9 dec 2014

•

0 likes•537 views

HCA Executive Director of Programmes Fiona MacGregor's presentation at the Inside Government hosted Future Housing 2014 event.

Report

Share

Inside Government 9 dec 2014

- 1. Successful places with homes and jobs A NATIONAL AGENCY WORKING LOCALLY Funding an Increased Supply of High Quality, Affordable Homes Inside Government 9 December 2014 Fiona MacGregor, Director of Programmes - HCA

- 2. Contents Current Programme and delivery to date 2015-18 Programme – Ensuring a smooth transition –Initial bid round outcome and recap –Continuous Market Engagement •Meeting local priorities •Quality - Housing Technical Standards Review •Advanced Housing Manufacture – speeding up delivery Summary

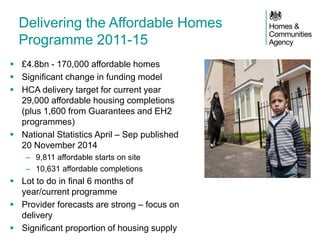

- 3. Delivering the Affordable Homes Programme 2011-15 £4.8bn - 170,000 affordable homes Significant change in funding model HCA delivery target for current year 29,000 affordable housing completions (plus 1,600 from Guarantees and EH2 programmes) National Statistics April – Sep published 20 November 2014 –9,811 affordable starts on site –10,631 affordable completions Lot to do in final 6 months of year/current programme Provider forecasts are strong – focus on delivery Significant proportion of housing supply

- 4. Affordable Housing Programme 2015 -18 £2.9bn investment for affordable housing over period 2015-18 (Spending Round – June 2013) Deliver 165,000 homes (range of sources) Funding outside London - £1.7bn FURTHER £1.9bn nationally – Autumn Statement – December 2014 Deliver 110,000 homes Total funding now £4.8bn – 275,000 affordable homes (range of sources) Average 55,000 homes per year – significant proportion of overall housing supply

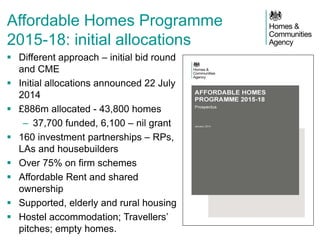

- 5. Affordable Homes Programme 2015-18: initial allocations Different approach – initial bid round and CME Initial allocations announced 22 July 2014 £886m allocated - 43,800 homes –37,700 funded, 6,100 – nil grant 160 investment partnerships – RPs, LAs and housebuilders Over 75% on firm schemes Affordable Rent and shared ownership Supported, elderly and rural housing Hostel accommodation; Travellers’ pitches; empty homes.

- 6. Smooth transition between programmes Guarantees and other programmes have acted as “bridge” between current programme and new AHP £200m Rent to Buy loan fund – prospectus published and bidding under CME Loan funding – low interest – increases from year 8 Affordable Rent – minimum of 7 years Loan repayable at end of 15 years Tenant first refusal to purchase

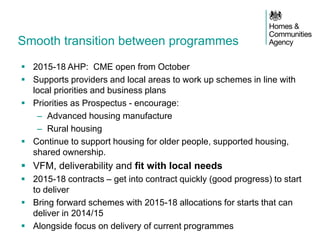

- 7. Smooth transition between programmes 2015-18 AHP: CME open from October Supports providers and local areas to work up schemes in line with local priorities and business plans Priorities as Prospectus - encourage: –Advanced housing manufacture –Rural housing Continue to support housing for older people, supported housing, shared ownership. VFM, deliverability and fit with local needs 2015-18 contracts – get into contract quickly (good progress) to start to deliver Bring forward schemes with 2015-18 allocations for starts that can deliver in 2014/15 Alongside focus on delivery of current programmes

- 8. Housing Standards Review: HCA Design and Quality standards 2007 Design and Quality standards remain for the 2011-15 AHP 2015-18 AHP no longer HCA specific standards as a condition of funding. Standards will be applied through the Building Regulations (for energy, security and waste) with optional requirements being introduced in the Building Regulations for the first time (accessibility and water efficiency). Responsibility for the application of optional standards in the Building Regulations will pass to Local Authorities (and compliance through Building Control) Responsibility for the Nationally Described Space Standard will pass to Local Authorities. HCA will consider space through IMS data returns.

- 9. Encouraging Advanced Housing Manufacture and speeding up delivery Advanced Housing Manufacture –Strong political interest –Cross tenure but AHP a place to demonstrate potential: especially for speed of delivery (at right price) –Skills shortages (and materials?) –Different scales –Different products Providers decide Share knowledge/experience (eg Accord) Smarter procurement – achieve scale through aggregation

- 10. Summary Affordable Housing included in National Infrastructure Plan in Autumn Statement announcements Extension of AHP – 5 year programme Acute interest in housing and increasing supply –Lyons Review –Budget –Manifestos and election –Spending Review Funding and delivery models –Grant funding and cross subsidy – what works where? –Devolution and alignment models Contribution of Affordable Housing to 200,000 (plus?) target Focus on now: –Continued delivery: Smooth transition between programmes; in contract –Continued bidding: 2015-18 AHP (CME); £200m Rent to Buy