Merger & acquisition presentation

•Download as PPTX, PDF•

10 likes•16,344 views

The document provides information about mergers and acquisitions (M&A) in Nepal, including causes, examples of M&As, challenges, and the legal/regulatory framework. Some of the key M&As in Nepal include the merger of Eastern Electricity with Nepal Electricity Authority, Standard Chartered acquiring Grindlays Bank, and Teliasonera acquiring Spice Nepal. Regulatory requirements from Nepal Rastra Bank have encouraged consolidation in the banking sector. Challenges in M&A transitions include managing brands, leadership, employees, and integrating systems. Laws like the Company Act and Bank and Financial Institutions Act govern M&As in Nepal.

Report

Share

Merger & acquisition presentation

- 1. Mergers & Acquisitions • Group: • Chandha Parajuli Neupane(14521) • Poojal Dahal Neupane(14522) • Dinesh Shrestha(14528) • Jipin Nakarmi(14520) • Krishna Hari Pandey(14523) • Sanjish Wagle(14537) • Suresh Kawan(14513) • Ujjwal Maghaiya(14516) • Madhu Sudan Dahal(14505) • Narayan Desar(14508) • Nakendra Dhami(14509)

- 2. The combining of two or more companies, generally by offering the stockholders of one company securities in the acquiring company in exchange for the surrender of their stock. Merger

- 3. Acquisition •When one company takes over another and clearly established itself as the new owner, the purchase is called an acquisition. •Acquisition is generally considered negative in nature

- 4. M&A Process

- 5. Trends of Merger and Acquisition in International Market

- 6. Motives for Mergers &acquisitions Economies of large scale business large-scale business organization enjoys both internal and external economies. Elimination of competition It eliminates severe, intense and wasteful expenditure by different competing organizations. Desire to enjoy monopoly power M&A leads to monopolistic control in the market. Adoption of modern technology corporate organization requires large resources Lack of technical and managerial talent Industrialization, scarcity of entrepreneurial, managerial and technical talent Economies of large scale business Elimination of competition Desire to enjoy monopoly power Adoption of modern technology Lack of technical and managerial talent

- 7. Benefits of Mergers and Acquisitions • Greater Value Generation. Mergers and acquisitions generally succeed in generating cost efficiency through the implementation of economies of scale. It is expected that the shareholder value of a firm after mergers or acquisitions. • Gaining Cost Efficiency. When two companies come together by merger or acquisition, the joint company benefits in terms of cost efficiency. As the two firms form a new and bigger company, the production is done on a much larger scale. • Increase in market share - An increase in market share is one of the plausible benefits of mergers and acquisitions. • Gain higher competitiveness - The new firm is usually more cost-efficient and competitive as compared to its financially weak parent organization.

- 8. Problems of Merger and Acquisitions • Integration difficulties • Large or extraordinary debt • Managers overly focused on acquisitions • Overly Diversified

- 9. Impact of Mergers and Acquisitions • Employees: Mergers and acquisitions impact the employees or the workers the most. It is a well known fact that whenever there is a merger or an acquisition, there are bound to be lay offs. • Impact of mergers and acquisitions on top level management Impact of mergers and acquisitions on top level management may actually involve a "clash of the egos". There might be variations in the cultures of the two organizations. • Shareholders of the acquired firm: The shareholders of the acquired company benefit the most. The reason being, it is seen in majority of the cases that the acquiring company usually pays a little excess than it what should. Unless a man lives in a house he has recently bought, he will not be able to know its drawbacks. • Shareholders of the acquiring firm: hey are most affected. If we measure the benefits enjoyed by the shareholders of the acquired company in degrees, the degree to which they were benefited, by the same degree, these shareholders are harmed

- 10. Strategies of Merger and Acquisition • Then there is an important need to assess the market by deciding the growth factors through future market opportunities, recent trends, and customer's feedback. • The integration process should be taken in line with consent of the management from both the companies venturing into the merger. • Restructuring plans and future parameters should be decided with exchange of information and knowledge from both ends.

- 11. Top M&A DEALS In global Market

- 12. 1. Tata Steel-Corus: $12.2 billion • January 30, 2007 • Largest Indian take-over • After the deal TATA’S became the 5th largest STEEL co. • 100 % stake in CORUS paying Rs 428/- per share

- 13. 2. Vodafone-Hutchison Essar: $11.1 billion • TELECOM sector • 11th February 2007 • 2nd largest takeover deal • 67 % stake holding in hutch Image: The then CEO of Vodafone Arun Sarin visits Hutchison Telecommunications head office in Mumbai.

- 14. 3. Tata Motors-Jaguar Land Rover: $2.3 billion • March 2008 (just a year after acquiring Corus) • Automobile sector • Acquisition deal • Gave tuff competition to M&M after signing the deal with ford

- 15. 4. ONGC-Imperial Energy:$2.8billion • January 2009 • Acquisition deal • Imperial energy is a biggest chinese co. • ONGC paid 880 per share to the shareholders of imperial energy • ONGC wanted to tap the siberian marketImage: Imperial Oil CEO Bruce March.

- 16. 5. RIL-RPL merger: $1.68 billion • March 2009 • Merger deal • amalgamation of its subsidiary Reliance Petroleum with the parent company Reliance industries ltd. • Rs 8,500 crore • RIL-RPL merger swap ratio was at 16:1 Image: Reliance Industries' chairman Mukesh Ambani.

- 17. MERGER BETWEEN AIR INDIA AND INDIAN AIRLINES • The government of India on 1 march 2007 approved the merger of Air India and Indian airlines. • Consequent to the above a new company called National Aviation Company of India limited was incorporated under the companies act 1956 on 30 march 2007 with its registered office at New Delhi.

- 19. • Cross border M&A rose significantly in East Asian Countries (Indonesia, Korea, Malaysia and Thailand) during the East Asian crisis period. • Cross border merger can encourage longer-term reforms like operational restructuring and reallocation of assets in firms along with improving efficiency, competitiveness and corporate governance (UNCTAD) • The need of M&A has significantly increased along with the rise of globalization.

- 20. Cross-Border Mergers and Acquisitions (Purchases), 1991–2009 (billion US$) Source UNCTAD 2010 1991–96 1997–99 2000–05 2006 2007 2008 2009 World 76.6 406.0 409.2 625.3 1022.7 706.5 249.7 Developed Economies 65.3 376.1 347.3 497.3 841.7 568.0 160.8 Developing Economies 7.8 12.6 37.7 114.9 144.8 105.8 74.0 Asia 4.7 9.3 27.6 70.8 94.5 94.4 67.3 East Asia 2.4 7.1 12.9 21.2 0.7 39.9 35.9 Southeast Asia 2.1 2.6 9.6 7.5 25.9 18.9 4.3 South Asia INDIA 0.1 0.0 1.1 6.7 29.1 13.5 0.3

- 21. Top 10 acquisitions made by Indian companies worldwide: Acquirer Target Company Country targeted Deal value ($ ml) Industry Tata Steel Corus Group plc UK 12,000 Steel Hindalco Novelis Canada 5,982 Steel Videocon Daewoo Electronics Corp. Korea 729 Electronics Dr. Reddy’s Labs Betapharm Germany 597 Pharmaceutical Suzlon Energy Hansen Group Belgium 565 Energy HPCL Kenya Petroleum Refinery Ltd. Kenya 500 Oil and Gas Ranbaxy Labs Terapia SA Romania 324 Pharmaceutical Tata Steel Natsteel Singapore 293 Steel Videocon Thomson SA France 290 Electronics VSNL Teleglobe Canada 239 Telecom

- 22. The Future of Mergers and Acquisition • Although a number of factors influence M&A, the market is the primary force that drives them. • The late 1990s saw an unprecedented influx in mergers. In 1999, companies filed about three times the number received in 1995 and the total dollar value $11 trillion of mergers was ten times the amount since 1992. http://legal- dictionary.thefreedictionary.com/Mergers+and+Acquisitions • Mergers rise during a booming economy and decrease as the companies forced to downsize during recession.

- 23. Trends of MA in Nepal

- 24. Causes of M&A in Nepal • Lack of confidence in domestic institutions – compete with global players who could potentially begin their operations here owing to WTO arrangements. – Regulatory Requirement • compulsive of sorts as the NRB has asked the BFIs belonging to the same business house to integrate without any “ifs and buts’’ – those who fear the complete meltdown • to consolidate resources, introduce corporate best practices and reduce expenses • Issues of liquidity crisis, unstable investment climate • M&As establish an ideal solution • For improving productivity • economic conditions, capacity utilization • achieving cost effectiveness of enterprises

- 25. M&A in Nepal • The first formal Merger – Eastern Electricity Corporation with Nepal Electricity Authority – Land Reform Saving corporation and Cooperative Development Bank (now the ADB/N) • Merger of dish/home TV • Standard Chartered Bank acquired Grindlays Bank from the ANZ Group • Butwal Power Company acquired Khimti and Bhotekoshi Hydropower companies • Teliasonera acquired Spice Nepal to form Ncell

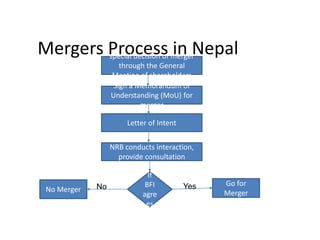

- 26. Mergers Process in Nepalspecial decision of merger through the General Meeting of shareholders Sign a Memorandum of Understanding (MoU) for merger Letter of Intent NRB conducts interaction, provide consultation If BFI agre es No Merger Go for Merger No Yes

- 27. NIC-ASIA, Successful Merger • Reason- Regulatory Pressure • BOA – facing problem in their lending portfolio and growth • NIC – facing problem in quality growth • Strategy of this merger – Gaining strength in size, capital, IT platform, trained human resources – Blending benefits of strong retail business of BoA and strong corporate business of NIC – Robust IT platform – HR integration through continuous counseling and orientation

- 28. Prabhu-Kist, Successful Acquistion • Prabhu Development Bank, a good and strong development bank in terms of its capital and market penetration acquired Kist Bank Limited, a “A” Class Commercial Bank in Nepal for the license of a “A” Class Bank • Prabhu Bank also acquired Nepal Development Bank, a liquidated bank because this bank was a foreign joint Venture • In a period of less than 3 years, a development bank turned out to be a “A” class commercial bank with a foreign JV, strong customer base, huge market penetration, strong financial backup and a good workforce venture

- 29. • Standard Chartered took Grindlays from ANZ group. • Teliasonera acquired Spice Nepal to form Ncell • Merger of dish/home TV

- 30. • The more recent merger in financial sector includes the merger between Laxmi Bank Ltd and HISEF Finance. • The merger between Narayani Finance Ltd and National Finance Ltd to form Narayani National Finance. • The merger between Nepal Bangladesh Bank and Nepal Sri Lanka Merchant Finance. • The initiation among Himchuli, Birgunj finance etc.

- 31. • Regarding bank mergers the move is from a regime of large number of small banks to small number of large banks.

- 32. Challenges in Transition • Brand Name • Composition in BOD and Shareholders • Structure of New Management Team • Employee Management • Ownership Division • Banking Software

- 33. Legal and Regulatory Approaches • Article 177 of the Company Act 2063 – provisioned for the amalgamation of company • Articles 68 and 69 of Bank and Financial Institutions Act 2063 Nepal Rastra bank enacted merger bylaw in 2011 – provisions for amalgamations among bank and financial institutions • The monetary and fiscal policies of 2067/68 also initiated and encouraged for mergers and acquisitions

- 34. Legal and Tax Perspective • The first one is the Companies Act 2063, Section 177, which highlights the impediments posed against the growth of M&As in Nepal • The BAFI Act 2063 – Chapter 10 restricts cross holdings of companies • The Insurance Act 2049 and the Silent Proposed Act • Competition, Promotion, and Market Protection Act, 2063 prevents a company from creating a monopoly in the market which an M&A could most likely produce • Securities Act 2063 and Labor Act 2048 are other Acts • Section 36 to 401, Section 47, and Section 57 of the Income Tax Act 2058 which outlines the applicability of taxes on the gains or losses derived as a result of the disposal of assets and liabilities.

- 35. What is Wrong • For effective implementation of the policy there is a need of coordination among various regulatory authorities in Nepal. • Due to the liberal licensing policy adopted by NRB, there was a tremendous surge in the number of BFIs from 2004 to 2009. • It is believed that the joint efficiency of the two companies is much better than the single firms. It goes by the equation 2+2=5 which might not hold true. • Case of high payment more than the worth. Each merger is different and each valuation is different. Therefore, a good financial valuator’s presence is valuable during this process. Certain areas need to be covered and analyzed closely before coming into decision like share market, how the public image is, capital strength, market power and numbers of customers if possible.

- 36. • small market and small size firms – M&A has not strategic alternative for growth and diversification in non-financial enterprises

Editor's Notes

- Nepal’s financial market opened up for international investment on January 2010 capacity of local institution to compete with its foreign counterparts raising the capital requirement from Rs. 2 billion to Rs.5 billion the current issues of liquidity crisis and unstable investment climate pose significant challenges for companies to expand

- A’, ‘B’ and ‘C’ class financial institutions can merge into each other. ‘D’ class FI can merge with another ‘D’ class FI only. FIs that want to merge should form a separate merger committee and sign Memorandum of Understanding (MoU). The due process including MoU should be completed before applying to the Nepal Rastra Bank (NRB)for Letter of Intent (LoI). NRB should hold a meeting within 15 days of receiving LoI application. NRB decides whether to issue LoI or not after conducting discussions and detailed study of concerned institutions. Due Diligence Audit should complete within six months of receiving LoI from the central bank. The detailed factual report comprising assets and liabilities of concerned institutions should be submitted to the NRB. Copy of the decision regarding name, address and share ratio of concerned financial institutions should be submitted to NRB. Action plan of concerned financial institution including date of operation after merger process is completed should be submitted to NRB. Other documents as prescribed by the NRB should be submitted to NRB. NRB can ask for merger if the following situation prevails: In case representatives of a family, business group, firm or company are found assuming posts in the boards of directors of two or more BFIs and/or their financial conditions remain unhealthy. If the non-performing loans (NPL) exceeded 5 percent of the total loan portfolio for 3 consecutive years. Increase in systematic risk (i.e. in a situation when a BFI seems likely to fail to meet liabilities). If independent operation of a BFI is causing negative impact on the banking system. If a BFI faces prompt corrective action (PCA) for three times or more. If NRB finds that merger of systemically important BFIs will strengthen the entire banking system.

- 1. Brand Name The identity of the institution in the market is through the brand name. The image of an entity is joining with a brand image. So, the settlement in the brand name of the newly formed merged entity is essential. 2. Composition of board of directors (BoD) and shareholders The major decision makers in any entity are the board of directors and the shareholders. If the disputes arise among these people, the performance as well as the future of the entity will be directly hampered. So, the number as well as the persons that should represent at the BoD should be settled in cool mind. 3. Structure of the new management team The new merged entity comprises of the management team from two or more different entities. So, clear visions should be set-up for making the new management team which could handle the merged organization in coming days. 4. Employees Management As the organization is merged, at the same time the employees also come together. The major assets any organization is human resources. So, if the merged entity can not handle properly the grievances of the employees, the situation of disputes may arise. 5. Ownership Division The problem of division among the ownership might arise in the merged entity. The questions of shareholding as well as takeover of the share equity might create division among the shareholders. 6. Banking Software Various types of software are being used by the BFIs for the smooth operation. Huge cost and efforts had been gone in maintain the software in an organization. But if the two different entities are using two different types of banking software, the problem as well as cost may arise in the settlement of the books of accounts.