Money and credit

•Download as PPTX, PDF•

113 likes•84,990 views

It is an attempt to make the learning of the chapter contents easier to the students by giving some extended information.

Report

Share

Money and credit

- 1. Money And Credit Class – X, Economics Chapter- Money and Credit 8/3/2019 1Pankaj Saikia-2015

- 2. You've probably never thought very much about money. It is just there. When you want or need something, you simply collect some money and pay for it. That wasn't always the way things were done, Would you not like to to know about how money has come. 8/3/2019 Pankaj Saikia-2015 2

- 3. Why should we study about money • All of us wants a good income in our future which is measured in terms of money. • Money is the means through which we measure how much we earn, we spent, we lend, we borrow, we save, we donate……………… • To earn economic wealth managing money is no way less important than earning. • Studying about money and credit enable us to make wise economic decision like allocation, investment, savings, expanditure, etc. 8/3/2019 3Pankaj Saikia-2015

- 4. Major learning Objectives 1. DIFFERENT PHASES OF EVALUATION OF MONEY. 2. DEFINITION, FEATURES, FUNCTIONS AND SIGNIFICANCE OF MONEY. 3. VARIOUS MODERN FORM OF MONEY. 4. BANK AND ITS BASIC FUNCTIONS. 5. CREDIT, TERMS OF CREDIT AND THEIR ROLE. 6. SOURCES OF CREDIT, CRITICAL ANALYSIS. 7. ROLE OF CO-OPERATIVE AND SHGS IN CAPITAL FORMATION. 8/3/2019 4Pankaj Saikia-2015

- 5. HOW DID MONEY EVOLVED. • In the premitive age need of people were very limited and people by themselves collected everything like food to eat and skin of animals and plants to wear, etc. • There was no need of exchange and money. 8/3/2019 5Pankaj Saikia-2015

- 6. Emergence of exchange • With the growth of civilisation needs of people started increasing. • People who were expert in producing some goods started taking it as a profession. • THEY STARTED COLLECTING OTHER GOODS THAT THEY NEED FROM OTHER PRODUCER IN EXCHANGE OF THE GOODS PRODUCED BY THEM. • EXAMPLE – A PERSON MAKING STONE TOOLS GIVES THE TOOLS TO THE HUNTER AND GETS MEAT AGAINST THE TOOLS. • WICH LEAD TO DEVELOPMENT OF BARTER 8/3/2019 6Pankaj Saikia-2015

- 7. Barter System The system of direct exchange in which comodities are exchanged for some other comodity without using any medium of exchange. 8/3/2019 Pankaj Saikia-2015 7

- 8. Main Features of Barter. 1. IT IS THE OLDEST EXCHANGE SYSTEM. 2. GOODS OR SERVICES ARE EXCHANGED / SWAP FOR OTHER GOODS OR SERVICES DIRECTLY. 3. THERE WAS NO COMMON MEASURE OV VALUE. 4. NO MONEY OR OTHER MEDIUM OF EXCHANGE WAS USED. 5. DOUBLE CO-INCIDENCE OF WANTS IS AN ESSENCE OF BARTER SYSTEM. 8/3/2019 8Pankaj Saikia-2015

- 9. Advantages of Barter. • It is the direct exchange system and therefore needs could be satisfied immediately. • No medium of exchange is required. • Low transaction time is required which helps the people to avoid the risk of change in value over time. 8/3/2019 9Pankaj Saikia-2015

- 10. Limitations of Barter. • Need of double co incidence of wants. • Lack of standard measure of Value. • Problem of divisibility. • Problem in storing value. • Problem of transferring value. • Deferred payment was not possible. 8/3/2019 10Pankaj Saikia-2015

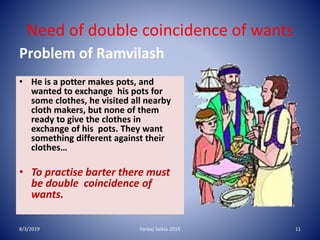

- 11. Need of double coincidence of wants Problem of Ramvilash • He is a potter makes pots, and wanted to exchange his pots for some clothes, he visited all nearby cloth makers, but none of them ready to give the clothes in exchange of his pots. They want something different against their clothes… • To practise barter there must be double coincidence of wants. 8/3/2019 11Pankaj Saikia-2015

- 12. Commodity Money • The most primitive type of money is commodity money. Some useful commodity that is in general demand is used as an exchange medium and may serve both as a means of payment and a measure of value. 8/3/2019 Pankaj Saikia-2015

- 13. Examples of Commodity Money • Various commodities have historically served as money – Cattle, tobacco, sugar, grains, nails, shells, hides, metals, etc. • But the transaction is still essentially a barter trade of one good or service for another good. 8/3/2019 Pankaj Saikia-2015 13

- 14. Limitations with comodity money. • Need of double co incidence of wants. • Lack of standard measure of Value. • Problem in storing value. • Problem of transferring value. • Deferred payment is not possible. 8/3/2019 14Pankaj Saikia-2015

- 15. Cattle Money • To overcome the problem of transfere of value with commodity money people started using cattles as money. Domestic animals having common utility were used as medium of exchange. These animals were known as cattle money. 8/3/2019 Pankaj Saikia-2015

- 16. Cattle money.. 8/3/2019 16Pankaj Saikia-2015

- 17. Limitations with cattle money. • Need of double co incidence of wants. • Lack of standard measure of Value. • Problem in storing value. • Problem of transferring value. • Deferred payment is not possible. • Problem of divisibility. 8/3/2019 17Pankaj Saikia-2015

- 18. Metallic Money. • Some precious metals like gold, silver, etc., having common utility were started using as medium of exchange. Which were known as Metallic money. • These were easy to store and not get damaged. • Conveniently carry from one place to another • Dividable in smaller parts. 8/3/2019 18Pankaj Saikia-2015

- 19. Way to modern coins---- Started adding symbols to express value. It gives a standrd measure of value. 8/3/2019 19Pankaj Saikia-2015

- 20. Way to modern coins---- Standardized with weight, size and colour. 8/3/2019 20Pankaj Saikia-2015

- 21. Way to modern coins---- Old precious metal were replaced with less costly metals- 8/3/2019 21Pankaj Saikia-2015

- 22. MONEY • Anything which is used as a medium of exchange, store of value, measure of value and standard of differed payments. 8/3/2019 22Pankaj Saikia-2015

- 23. Money can be anything • Has purchasing power. • Used as medium of exchange. • Used to measure value of any goods or services. • Used to transfere value from one person to another or one place to another. • Used to store value for future use. • Used as a standard of deferred payment. 8/3/2019 23Pankaj Saikia-2015

- 24. FUNCTIONS OF MONEY • 1. Medium of Exchange. 8/3/2019 Pankaj Saikia-2015 24

- 25. FUNCTIONS OF MONEY 2. Store of Value. 8/3/2019 25Pankaj Saikia-2015

- 26. FUNCTIONS OF MONEY 3. Measure of Value. 8/3/2019 26Pankaj Saikia-2015

- 27. FUNCTIONS OF MONEY 4. Transfere of Value. 8/3/2019 27Pankaj Saikia-2015

- 28. FUNCTIONS OF MONEY 5. Standard of deferred payment. 8/3/2019 28Pankaj Saikia-2015

- 29. Money in India • The coins and paper currency of paise and rupee are generally accepted as medium of exchange or money in India. • Paper currency note and mattellic coins for denomination of Rs.2 and above are issued by Reserve Bank of India in permission of Finance Ministry of the central government. At present it Issues coins and notes of Rs. 2, 5, 10, 20, 50, 100, 200, 500 and 2000. • Rs 1 and its subsidiaries are issued by the Ministry of Finance. It issues coins of Rs 1 and 50 Paise. 8/3/2019 29Pankaj Saikia-2015

- 30. Other names of Modern currency. • Symbolic or Token Money:- • As the currency notes and coins have no or very less intrinsic value but represents a higher value, therefore they are called Token money. 8/3/2019 30Pankaj Saikia-2015

- 31. Other names of Modern currency. • High Powered Money;- • Currency notes and coins are called high powered money because they represent higher value (high power) than their actual value. 8/3/2019 31Pankaj Saikia-2015

- 32. Other names of Modern currency. •Legal tender money:- •The Rupee notes and coins in India are called legal tender money because they poses a legal value and no one can legally refuse any payment made through these. 8/3/2019 32Pankaj Saikia-2015

- 33. BANK • Bank is a financial institution who deals with money and credit as its regular course of business. • It accepts deposits from the depositors and grant loans to the needy borrowers. 8/3/2019 33Pankaj Saikia-2015

- 34. FUNCTIONS OF BANK • Accepting deposit. • Granting Loans. • Providing safety to valuables of customers. • Transfering funds from one place to another for customer. • Accepting payment for customer. • Making payment on behalf of customer. Paying electricity bill/ Insurance primium etc.) 8/3/2019 34Pankaj Saikia-2015

- 35. MAIN FUNCTION Of BANK Depositors BANK Borrowers 8/3/2019 35Pankaj Saikia-2015

- 36. Major types of Deposits Demand Deposit • Withdrawable at any time on demand. • It Includes deposit in- a. Current Account, and b. Savings Account. Time or Term Deposit • Withdrawable after a certain period of time. • It Includes deposit in- a. Fixed deposit Account, and b. Recurring deposit Account. 8/3/2019 36Pankaj Saikia-2015

- 37. Four Major Types of Deposit Accounts • Current Deposit Account • No restriction in deposit. • No restriction in withdrowal. • No interest is paid by the bank on deposit. • Main purpose of opening such account is to provide safety to customers cash. • Rich businessman and organisation opens such accounts. 8/3/2019 37Pankaj Saikia-2015

- 38. Four Major Types of Deposit Accounts • Savings Deposit Account • No restriction in deposit. • Withdrowal is possible at any time subject to some restrictions. • Low rate (3-4%) of interest is paid by the bank on deposit. • Main purpose of opening such account is savings and meeting uncertain urgencies. • Small businessman and people with low or moderate income opens such accounts. 8/3/2019 38Pankaj Saikia-2015

- 39. Four Major Types of Deposit Accounts • Recurring Deposit Account • Fixed amount is deposited at a fixed interval for a fixed period. • Withdrowal is only on maturity. • Good rate of interest is paid by the bank on deposit. • Main purpose of opening such account is capital formation and savings. • People with regular income usually opens such accounts. 8/3/2019 39Pankaj Saikia-2015

- 40. Four Major Types of Deposit Accounts • Fixed Deposit Account • Fixed amount is deposited for a fixed period. • Withdrowal is only on maturity. • Highest rate of interest. • Main purpose of opening such account is to earn interest and save for certain future needs. • People having no other investment options and with some certain future needs deposits here. 8/3/2019 40Pankaj Saikia-2015

- 41. DEMAND DEPOSIT IS A MODERN FORM OF MONEY • Money in demand deposit can be withdrawn at any time through Cheque, ATM, etc. • It can be used to make payment or purchase at any time through Cheque, Debit card, Net Banking, etc.. • It has purchasing power----- • Anything having purchasing power is money— • Therefore demand deposit is money. 8/3/2019 41Pankaj Saikia-2015

- 42. Modern form of money • Money is anything that has Purchasing Power • Demand Deposit has Purchasing Power. (As it can be used to make payment or to purchase) therefore, Demand Deposit is Money. • ----------------------------------- • Money = Purchasing Power . • Demand Deposit = Purchasing Power = Money . 8/3/2019 42Pankaj Saikia-2015

- 43. CHEQUE • It is a written document with which a depositor orders his banker to pay a certain amount to himself or to the bearer or to a certain person. 8/3/2019 43Pankaj Saikia-2015

- 44. FEATURES OF CHEQUE • Cheque is a written document in prescribed form provided by bank. • It is written by a depositor to his banker. • It caries an order to pay a certain sum of money from the deposit. • It is a modern form of money as it can be used to make payment. 8/3/2019 44Pankaj Saikia-2015

- 45. Essential components of a cheque • Signature of depositor. • Name of payee (Self/ Bearer/any third party) • Amount must be specific and written in both words and numbers. • Date of drawing or making. • Account number of the depositor. 8/3/2019 45Pankaj Saikia-2015

- 46. Different Modern Form of money • Card Money / Plastic Money- Debit card, Credit card, Smart Card, Health card, etc. • Digital Cash- Net Banking, Mobile Banking, etc. • Bank money- Cheque, Demand Draft, Bankers cheque, etc. • Credit. 8/3/2019 46Pankaj Saikia-2015

- 47. Credit • Credit is an arrangement in which ones financial need is satisfied with the money or resource of another with a promise to repay in future. 8/3/2019 47Pankaj Saikia-2015

- 48. Credit – A promese to pay in future • Cash/goods/sarvices B 8/3/2019 48Pankaj Saikia-2015

- 49. Role of Credit in Development • Credit makes proper use of excess money of the depositors by channelising it to a profitable investment. In this way it maximise the use of countries worth. • Enables the borrower to invest more than their resources available with them. • Maximizes the use of resources by providing working capital. • Helps the lenders to earn interest from their savings. 8/3/2019 49Pankaj Saikia-2015

- 50. Terms of Credit • Different conditions in which the borrower and the lender agreed before granting or taking a loan. •It includes- • Rate of Interest. • Mode of repayment. • Collateral. • Documentation required etc. 8/3/2019 50Pankaj Saikia-2015

- 51. Sources of Credit • The individual or organisation who grants loan. • Banks. • NBFIs. • Cooparatives. • Family members. • Friends. • Traders. • Money Lenders. 8/3/2019 51Pankaj Saikia-2015

- 52. Sources of Credit Formal Sources • Controlled by RBI. • Reasonable and justified rate of interest. • Granted for productive purpose only. • More documentation required. • Legal proceedings followed to recover loan amount if the borrower fail to repay. Informal sources • Not controlled by anyone. • Mostly high and unjust rate of interest. • Granted for any purpose. • No or less documentation required. • Lender can take any measure to recover loan if the borrower fail to repay. 8/3/2019 52Pankaj Saikia-2015

- 53. Formal Sources of credit • Advantages-- • Low rate of Interest. • Adopt judicious policy to recovery of loan. • Grants loans only for productive purpose and chances of falling in debt trap is less. • Helps the borrowers for effective utilisation of loan amount and promote development. • Interest rate is fixed considering the prevailing market and economic condition and therefore the risk of borrowers are less. 8/3/2019 53Pankaj Saikia-2015

- 54. Formal sources of credit • Limitations-- • Grants only secured loan. So, the people without proper colletoral can not borrow. • Long process and high documentation. • Less autonomy in utilisation of fund. • Difficult to get loan to meet small financial needs. • It grants loans only for Projects that are productive in their eyes. • Located at far from the borrowers particularly in rural areas. 8/3/2019 54Pankaj Saikia-2015

- 55. Informal sources of credit • Advantages-- • Very easy process and Instant Credit. • Less or No Documentation. • Full or high level of autonomy in utilisation of fund. • Free to fix the loan amount and time and mode of repayment. • Loans are granted to meet all kind of financial needs. 8/3/2019 55Pankaj Saikia-2015

- 56. Informal sources of credit • Limitations-- • High rate of interest. • Though conditions for repayment. • Undue and unnecessary interferance in utilisation of fund. • Unjust and unethical means of recovery of loan if the borrower fails to repay. • Mostly grants loans for unproductive purposes, which is detrimental to the interest of the borrower as well as the economy. 8/3/2019 56Pankaj Saikia-2015

- 57. Do Credit is always beneficial? Credit somtimes may be a burden for the borrower and may lead to debt trap. Credit can be a burden mostly in the following circumstances. • If borrowed at a very high rate of interest. • If borrowed money used for unproductive purpose. • If invested in a business with high risk of failure. • Delay in repayment of loan increases the burden as the amount grow in cumulative interest. • Failure to repay the loan may cause charge on the property of the borrower which has been kept as security against the loan. • Taking fresh loan to repay the previous loan and fall in debt trap, recovery from which becomes very difficult. 8/3/2019 57Pankaj Saikia-2015

- 58. Status of Lending and borrowing in India • In India both formal and informal sources of credit is working simulteniously. • Major part of the formal sector lending goes to the large industrial sector. • Small borrowers ie. small farmers, labour class and small articians and businessmen, etc. mostly borrows from informal sector. 8/3/2019 58Pankaj Saikia-2015

- 59. Problems of borrowing from Informal Sector • High rate of interest. • Though conditions for repayment. • Undue and unnecessary interferance in utilisation of fund. • Unjust and unethical means of recovery of loan if the borrower fails to repay. • Failure to repay loan amount may lead to loss of property and further detoriation of economic condition.8/3/2019 59Pankaj Saikia-2015

- 60. Why Small farmers Borrow from Informal Sector • Hesitation to go to the bank. • lliteracy • Lack of awareness. • Lack of Colletoral. • Borrowing for Unproductive Purposes. • Unability to fulfil Documentation needed. • Poor Accessability to Banks. • Easy Accessability to Money Lenders. 8/3/2019 60Pankaj Saikia-2015

- 61. Is it important to protect the borrower of Informal Sector • Majority of the borrowers of the informal sector are poor who need financial protection. • To protect the borrowers from the exploitation of the speculative moneylenders. • Informal sector lending and the interest earned on it is not taxed and therefore these are black money. • This often leads to conflect between borrower and the lender which sometimes creats critical law and order situation. • Unproductive loans can be used to finance illigal business.. 8/3/2019 61Pankaj Saikia-2015

- 62. Measures to protect the borrowers of Informal sector. • Increasing the accessibility of formal sector lending by expanding banking network. • Easy and liberal documentation. • Flexible ( size and duration) loan arrangement. • Reserved and compulsory lending for rural and small scale industry . • Awareness cappaigning. 8/3/2019 62Pankaj Saikia-2015

- 63. Co-operative Society. • Organisation of people joins for mutual help. • Development of the members is the main purpose not earning profit. • Registered under Cooperative Societies Act. • Minimum 10 members are required to form a co operative. 8/3/2019 63Pankaj Saikia-2015

- 64. Types of Cooperative • Farmers Cooperative Society. • Producers Cooperative Society. • Weavers Cooperative Society. • Customers Cooperative Society. • Cooperative Credit Society. 8/3/2019 64Pankaj Saikia-2015

- 65. Role of Cooperative Society in Capital formation.. • Cooperatives accumulates its capital with the contribution of members. Sometimes they takes loans from the Banks and NBFIs in the name of cooperative and use the fund either in collective investment or grants loans to the needy members of the society. They charges a low rate of interest as their motive is not to earn profit but the development of economic condition of its members. 8/3/2019 65Pankaj Saikia-2015

- 66. Self Help Group ( SHG) • It is a small group of 10-20 people belonging from the same locality. • The main purpose of such group is to help its members for their economic welbeing. • They either carry on some collective business or creats a fund to lend to the needy members. • Government encourages such groups by arranging bank loan at subdised rate of interest. 8/3/2019 66Pankaj Saikia-2015

- 67. Origin of Self Help Group ( SHG) Concept of SHGs developed in Bangladesh. Gramin Bank of Bangladesh is the biggest success story in reaching the poor to meet their credit needs at reasonable rates through the idea of SHG. Most of the borrowers are women and belong to poorest section of the society. ------------------------------------------------------------- The idea is the Brain Child of (developed by) renowned economist Prof. Mohammed Yunus recipient of Nobel Prize for peace in 1996. 8/3/2019 67Pankaj Saikia-2015

- 68. Thank You Your criticism and suggestion for betterment worth a lot. 8/3/2019 68Pankaj Saikia-2019