Pega Consumer Report

- 1. © 2018 Pegasystems Inc. CONFIDENTIAL Pega Consumer Report February 2019

- 2. Methodology This research was conducted by Censuswide on behalf of Pegasystems. Data was collected online between 12.21.2018 - 01.02.2019 among the total sample of 2,018 US consumers aged 18+. Note: The research conducted adheres to the MRS Codes of Conduct and ICC/ESOMAR World Research Guidelines. Censuswide is registered with the Information Commissioner's Office and is fully compliant with GDPR (2018). © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 3. Question One Q1. To what extent do you agree or disagree with the following statements? 67% 80% 46% 50% 71% 58% 60% 55% 78% 42% 10% 5% 18% 17% 7% 11% 12% 21% 7% 19% I am more likely to focus on my health and well-being when I feel financially stable I have easy access to healthy food in my community My family and friends (social circle) help me make better choices about my health I find my doctor to be readily available to me (online portal, hotline, open appointments) My doctor is always fully informed of my medical history I am open to giving my doctor access to my mobile health application data I am open to giving my doctor real-time access to my digital health information via connected devices and apps to improve my health outcomes I am open to virtual appointments with my doctor via webcam/Skype/Facetime for appointments that might not require an in-person visit I would switch doctors due to poor communication or engagement I am comfortable with my doctor using artificial intelligence to make better decisions about my care Overall Agree (top2) Overall Disagree (bottom2) More than a fifth of US consumers are not open to virtual appointments with their doctor via webcam/skype/facetime for appointments that might not require an in-person visit. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 4. 28% 39% 22% 7% 3% 1% Strongly agree Agree I am more likely to focus on my health and well-being when I feel financially stable Two thirds (67%) of US consumers agree with this, and more than a quarter (28%) ‘strongly’ agree with this. Q1. To what extent do you agree or disagree with the following statements? Question One © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 5. 35% 45% 14% 4% 1% 1% Strongly agree Agree I have easy access to healthy food in my community 4 in 5 (80%) US consumers agree with this, and 2 in 5 (40%) ‘strongly’ agree with this. Q1. To what extent do you agree or disagree with the following statements? Question One © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 6. 11% 35% 34% 13% 5% 2% Strongly agree Agree My family and friends (social circle) help me make better choices about my health Almost half (46%) of US consumers agree that their family and friends (social circle) help them make better choices about their health , with 1 in 9 (11%) ‘strongly’ agreeing with this. Q1. To what extent do you agree or disagree with the following statements? Question One © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 7. 16% 34% 28% 13% 4% 6% Strongly agree Agree I find my doctor to be readily available to me (online portal, hotline, open appointments) Half (50%) of US consumers agree that they find their doctor to be readily available to them (online portal, hotline, open appointments), with 16% saying they ‘strongly’ agree with this. Q1. To what extent do you agree or disagree with the following statements? Question One © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

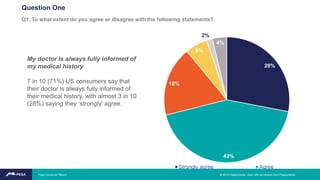

- 8. 28% 43% 18% 6% 2% 4% Strongly agree Agree My doctor is always fully informed of my medical history 7 in 10 (71%) US consumers say that their doctor is always fully informed of their medical history, with almost 3 in 10 (28%) saying they ‘strongly’ agree. Q1. To what extent do you agree or disagree with the following statements? Question One © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 9. 20% 38% 25% 7% 4% 7% Strongly agree Agree I am open to giving my doctor access to my mobile health application data 58% of US consumers agree that they are open to giving their doctor access to their mobile health application data, with a fifth (20%) saying that they ‘strongly’ agree with this. Q1. To what extent do you agree or disagree with the following statements? Question One © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

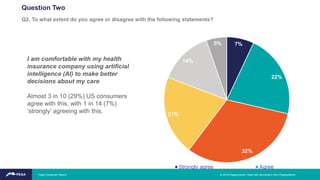

- 10. 22% 39% 24% 7% 4% 4% Strongly agree Agree I am open to giving my doctor real- time access to my digital health information via connected devices and apps to improve my health outcomes 3 in 5 (60%) US consumers are open to giving their doctor real-time access to their digital health information via connected devices and apps to improve their health outcomes, with over a fifth (22%) ‘strongly’ agreeing with this. Q1. To what extent do you agree or disagree with the following statements? Question One © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 11. 19% 36% 22% 13% 8% 3% Strongly agree Agree I am open to virtual appointments with my doctor via webcam/Skype/Facetime for appointments that might not require an in-person visit 55% of US consumers agree that they are open to virtual appointments with their doctor via webcam/Skype/Facetime for appointments that might not require an in-person visit, with just under a fifth (19%) saying they ‘strongly’ agree with this. Q1. To what extent do you agree or disagree with the following statements? Question One © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 12. 36% 42% 14% 4% 3% 2% Strongly agree Agree I would switch doctors due to poor communication or engagement More than three quarters (78%) of US consumers agree that they would switch doctors due to poor communication or engagement, with just over a third (36%) saying they ‘strongly’ agree with this. Q1. To what extent do you agree or disagree with the following statements? Question One © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 13. 11% 31% 35% 11% 8% 4% Strongly agree Agree I am comfortable with my doctor using artificial intelligence to make better decisions about my care Just over 2 in 5 (42%) US consumers are comfortable with their doctor using artificial intelligence to make better decisions about their care, with 1 in 9 (11%) saying they strongly agree with this. Q1. To what extent do you agree or disagree with the following statements? Question One © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

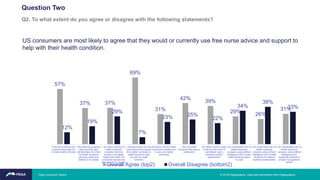

- 14. Question Two Q2. To what extent do you agree or disagree with the following statements? 57% 37% 37% 69% 31% 42% 39% 29% 26% 31% 12% 19% 29% 7% 23% 25% 22% 34% 38% 33% Financial incentives and rewards encourage me to make healthy choices I find wellness programs (step counting, gym memberships, etc.) from my health insurance company useful and tailored to my needs I am open to giving my health insurance company real-time access to my digital health information via connected devices and apps in order to improve my health outcomes I would/currently use free nurse advice and support (from either my doctor or health insurer) to help me with my health condition My doctor and my health insurance company are in sync and closely connected I find my health insurance bills easy to understand My health insurer is able to tell me how much Ill owe before I get a procedure and/or appointment I am comfortable with my health insurance company using artificial intelligence (AI) to make better decisions about my care I am comfortable with my health insurance company using artificial intelligence (AI) to make decisions for medical treatment authorization I am comfortable with my health insurance company using artificial intelligence (AI)- supported chatbots to answer my questions online? Overall Agree (top2) Overall Disagree (bottom2) US consumers are most likely to agree that they would or currently use free nurse advice and support to help with their health condition. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 15. Question Two Q2. To what extent do you agree or disagree with the following statements? 18% 39% 26% 9% 4% 5% Strongly agree Agree “Financial incentives and rewards encourage me to make healthy choices” 57% of US consumers agree with this, and almost a fifth (18%) say they ‘strongly’ agree with this. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 16. Question Two Q2. To what extent do you agree or disagree with the following statements? 10% 27% 32% 13% 6% 12% Strongly agree Agree I find wellness programs (step counting, gym memberships, etc.) from my health insurance company useful and tailored to my needs 37% of US consumers agree with this, and 1 in 10 (10%) say they ‘strongly’ agree with this. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 17. Question Two Q2. To what extent do you agree or disagree with the following statements? 10% 27% 28% 17% 11% 6% Strongly agree Agree I am open to giving my health insurance company real-time access to my digital health information via connected devices and apps in order to improve my health outcomes 37% of US consumers agree with this, and 1 in 10 (10%) say they ‘strongly’ agree with this. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 18. Question Two Q2. To what extent do you agree or disagree with the following statements? 19% 50% 21% 5% 3% 3% Strongly agree Agree I would/currently use free nurse advice and support (from either my doctor or health insurer) to help me with my health condition More than two thirds (69%) of US consumers agree with this, and 1 in 10 (10%) say they ‘strongly’ agree with this. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 19. Question Two Q2. To what extent do you agree or disagree with the following statements? 8% 23% 39% 16% 7% 8% Strongly agree Agree My doctor and my health insurance company are in sync and closely connected Almost a third (31%) of US consumers agree with this, and 1 in 12 (8%) ‘strongly’ agree with this. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 20. Question Two Q2. To what extent do you agree or disagree with the following statements? 10% 32% 25% 19% 7% 7% Strongly agree Agree I find my health insurance bills easy to understand More than 2 in 5 (42%) US consumers agree with this, with 1 in 10 (10%) ‘strongly’ agreeing with this. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 21. Question Two Q2. To what extent do you agree or disagree with the following statements? 10% 29% 31% 15% 7% 8% Strongly agree Agree My health insurer is able to tell me how much I’ll owe before I get a procedure and/or appointment Almost 2 in 5 (39%) US consumers agree with this, with 1 in 10 (10%) ‘strongly’ agreeing with this. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 22. Question Two Q2. To what extent do you agree or disagree with the following statements? 7% 22% 32% 21% 14% 5% Strongly agree Agree I am comfortable with my health insurance company using artificial intelligence (AI) to make better decisions about my care Almost 3 in 10 (29%) US consumers agree with this, with 1 in 14 (7%) ‘strongly’ agreeing with this. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 23. Question Two Q2. To what extent do you agree or disagree with the following statements? 7% 19% 30% 21% 17% 5% Strongly agree Agree I am comfortable with my health insurance company using artificial intelligence (AI) to make decisions for medical treatment authorization More than a quarter (26%) of US consumers agree with this, and 1 in 14 (7%) ‘strongly’ agree with this. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 24. Question Two Q2. To what extent do you agree or disagree with the following statements? 7% 24% 30% 21% 13% 6% Strongly agree Agree I am comfortable with my health insurance company using artificial intelligence (AI)-supported chatbots to answer my questions online Almost a third (31%) of US consumers agree with this and 1 in 14 (7%) ‘strongly’ © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 25. Question Three Q3. I track my eating habits and exercise on mobile applications 33% 67% Yes No More than two thirds of US consumers track their eating habits and exercise on mobile applications. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 26. Question Four A Q4a. Aside from in person appointments/procedures, how do you like to interact with the following health organizations? (Select all that apply) 38% 24% 41% 30% 26% 15% 14% 23% 11% 10% 71% 46% 54% 39% 36% 27% 19% 28% 18% 15% 1% 1% 1% 1% 1% 17% 9% 9% 14% 13% 3% 2% 2% 2% 1% 5% 4% 5% 4% 3% 7% 5% 7% 7% 5% Doctor's office Local Hospital Primary Health Insurer Pharmacy Benefit Manager/Prescription Mail Order pharmacy Pharmaceutical/Drug company Email Mail Phone Web/online portal Fax Text Messaging app (Facebook, WhatsApp, etc.) Chat Mobile App Options hidden: ‘N/A I have no relationship with this health organization’, ‘No preference’ and ‘Other’ Email is the second most popular way that US consumers like to interact with all healthcare organizations, and fax is the least popular method. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 27. Doctor’s Office The top three ways that US consumers like to interact with their doctor’s office are; phone (71%), email (38%) and web/online portal (27%). 38% 15% 71% 27% 1% 17% 3% 5% 7% 2% 5% Email Mail Phone Web/online portal Fax Text Messaging app (Facebook, WhatsApp, etc.) Chat Mobile App Question Four A Q4a. Aside from in person appointments/procedures, how do you like to interact with the following health organizations? (Select all that apply) © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 28. Local Hospital The top three ways that US consumers like to interact with their local hospital are; phone (46%), email (24%) and web/online portal (19%). 24% 14% 46% 19% 1% 9% 2% 4% 5% 2% 10% 0% Email Mail Phone Web/online portal Fax Text Messaging app (Facebook, WhatsApp, etc.) Chat Mobile App Question Four A Q4a. Aside from in person appointments/procedures, how do you like to interact with the following health organizations? (Select all that apply) © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 29. Primary Health Insurer The top three ways that US consumers like to interact with their primary health insurer are; phone (54%), email (41%) and web/online portal (28%). 41% 23% 54% 28% 1% 9% 2% 5% 7% 1% 6% Email Mail Phone Web/online portal Fax Text Messaging app (Facebook, WhatsApp, etc.) Chat Mobile App Question Four A Q4a. Aside from in person appointments/procedures, how do you like to interact with the following health organizations? (Select all that apply) © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 30. Pharmacy Benefit Manager/Prescription Mail Order pharmacy The top three ways that US consumers like to interact with their doctor’s office are; phone (39%), email (30%) and web/online portal (18%). 30% 11% 39% 18%1% 14% 2% 4% 7% 1% 6% 27% Email Mail Phone Web/online portal Fax Text Messaging app (Facebook, WhatsApp, etc.) Chat Mobile App Question Four A Q4a. Aside from in person appointments/procedures, how do you like to interact with the following health organizations? (Select all that apply) © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 31. Pharmaceutical/Drug company The top three ways that US consumers like to interact with their doctor’s office are; phone (36%), email (26%) and web/online portal (15%). 26% 10% 36% 15% 1% 13% 1%3% 5% 1% 8% 30% Email Mail Phone Web/online portal Fax Text Messaging app (Facebook, WhatsApp, etc.) Chat Mobile App Question Four A Q4a. Aside from in person appointments/procedures, how do you like to interact with the following health organizations? (Select all that apply) © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

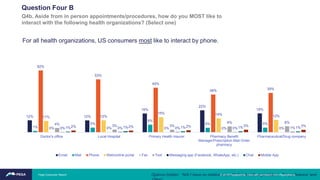

- 32. Question Four B Q4b. Aside from in person appointments/procedures, how do you MOST like to interact with the following health organizations? (Select one) 12% 12% 19% 22% 19% 1% 5% 8% 5% 5% 62% 53% 45% 38% 39% 11% 12% 15% 14% 12% 0% 0% 0% 0% 0% 4% 3% 3% 6% 6% 0% 0% 0% 0% 1%1% 1% 1% 1% 1%2% 2% 2% 3% 3% Doctor's office Local Hospital Primary Health Insurer Pharmacy Benefit Manager/Prescription Mail Order pharmacy Pharmaceutical/Drug company Email Mail Phone Web/online portal Fax Text Messaging app (Facebook, WhatsApp, etc.) Chat Mobile App Options hidden: ‘N/A I have no relationship with this health organization’, ‘No preference’ and For all health organizations, US consumers most like to interact by phone. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 33. Doctor’s Office The phone is the way US consumers most likely to interact with their doctor’s office (62%). 12% 1% 62% 11% 0% 4% 0% 1% 2% 1% 5% Email Mail Phone Web/online portal Fax Text Messaging app (Facebook, WhatsApp, etc.) Chat Mobile App Question Four B Q4b. Aside from in person appointments/procedures, how do you MOST like to interact with the following health organizations? (Select one) © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 34. Local Hospital The phone is the way US consumers most likely to interact with their local hospital (53%). 12% 5% 53% 12% 0% 3% 0% 1% 2% 2% 10%Email Mail Phone Web/online portal Fax Text Messaging app (Facebook, WhatsApp, etc.) Chat Mobile App Question Four B Q4b. Aside from in person appointments/procedures, how do you MOST like to interact with the following health organizations? (Select one) © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 35. Primary Health Insurer The phone is the way US consumers most likely to interact with their primary health insurer (45%). 19% 8% 45% 15% 0% 3% 0% 1% 2% 1% 7% Email Mail Phone Web/online portal Fax Text Messaging app (Facebook, WhatsApp, etc.) Chat Mobile App Question Four B Q4b. Aside from in person appointments/procedures, how do you MOST like to interact with the following health organizations? (Select one) © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

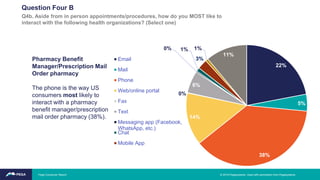

- 36. Pharmacy Benefit Manager/Prescription Mail Order pharmacy The phone is the way US consumers most likely to interact with a pharmacy benefit manager/prescription mail order pharmacy (38%). 22% 5% 38% 14% 0% 6% 0% 1% 3% 1% 11% Email Mail Phone Web/online portal Fax Text Messaging app (Facebook, WhatsApp, etc.) Chat Mobile App Question Four B Q4b. Aside from in person appointments/procedures, how do you MOST like to interact with the following health organizations? (Select one) © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 37. Pharmaceutical/Drug company The phone is the way US consumers most likely to interact with a pharmaceutical/drug company (39%). 19% 5% 39% 12% 0% 6% 1% 1% 3% 1% 14%Email Mail Phone Web/online portal Fax Text Messaging app (Facebook, WhatsApp, etc.) Chat Mobile App Question Four B Q4b. Aside from in person appointments/procedures, how do you MOST like to interact with the following health organizations? (Select one) © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 38. Question Five Q5. Do you want more or less communication from the following health organizations? 27% 12% 19% 12% 10% 66% 65% 67% 62% 59% 2% 6% 5% 6% 9% 5% 17% 8% 21% 22% Doctor's office Local Hospital Primary Health Insurer Pharmacy Benefit Manager/Prescription Mail Order pharmacy Pharmaceutical/Drug company More Same Less N/A US consumers are most likely to want more communication from their primary health insurer, and most likely to want less communication from their doctor’s office. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 39. Doctor’s Office Most commonly, US consumers want the same amount of communication from their doctor’s office (66%), however over a quarter (27%) want more communication from them. 27% 66% 2% 5% More Same Less N/A Question Five Q5. Do you want more or less communication from the following health organizations? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 40. Local Hospital Most commonly, US consumers want the same amount of communication from their local hospital (65%), however 1 in 8 (12%) want more communication from them. 12% 65% 6% 17% More Same Less N/A Question Five Q5. Do you want more or less communication from the following health organizations? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

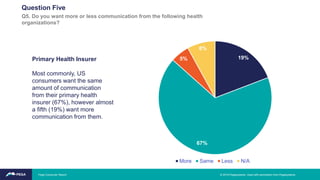

- 41. Primary Health Insurer Most commonly, US consumers want the same amount of communication from their primary health insurer (67%), however almost a fifth (19%) want more communication from them. 19% 67% 5% 8% More Same Less N/A Question Five Q5. Do you want more or less communication from the following health organizations? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

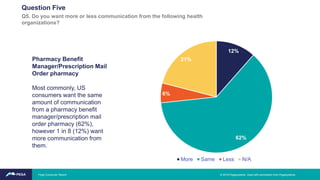

- 42. Pharmacy Benefit Manager/Prescription Mail Order pharmacy Most commonly, US consumers want the same amount of communication from a pharmacy benefit manager/prescription mail order pharmacy (62%), however 1 in 8 (12%) want more communication from them. 12% 62% 6% 21% More Same Less N/A Question Five Q5. Do you want more or less communication from the following health organizations? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

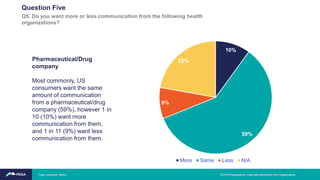

- 43. Pharmaceutical/Drug company Most commonly, US consumers want the same amount of communication from a pharmaceutical/drug company (59%), however 1 in 10 (10%) want more communication from them, and 1 in 11 (9%) want less communication from them. 10% 59% 9% 22% More Same Less N/A Question Five Q5. Do you want more or less communication from the following health organizations? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 44. Question Six Q6. How valued do communications from the following organizations make you feel? 73% 48% 54% 39% 35% 4% 6% 8% 6% 10% Doctor's office Local Hospital Primary Health Insurer Pharmacy Benefit Manager/Prescription Mail Order pharmacy Pharmaceutical/Drug company Overall Valued (top2) Overall Not Valued (bottom2) US consumers are most likely to feel valued by their doctor’s office, and least likely to feel valued by a pharmaceutical/drug company. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 45. Doctor’s Office Almost three quarters (73%) of US consumers feel valued by their doctor’s office, and 1 in 9 (11%) feel ‘highly’ valued. 35% 37% 19% 3% 2% 4% Highly valued Somewhat Valued Neither valued or not valued Somewhat not valued Not valued at all N/A Question Six Q6. How valued do communications from the following organizations make you feel? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 46. Local Hospital Almost half (48%) of US consumers feel valued by their local hospital, and almost a fifth (18%) feel ‘highly’ valued. 18% 30% 32% 3% 3% 14% Highly valued Somewhat Valued Neither valued or not valued Somewhat not valued Not valued at all N/A Question Six Q6. How valued do communications from the following organizations make you feel? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

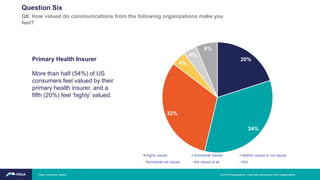

- 47. Primary Health Insurer More than half (54%) of US consumers feel valued by their primary health insurer, and a fifth (20%) feel ‘highly’ valued. 20% 34% 32% 4% 4% 6% Highly valued Somewhat Valued Neither valued or not valued Somewhat not valued Not valued at all N/A Question Six Q6. How valued do communications from the following organizations make you feel? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

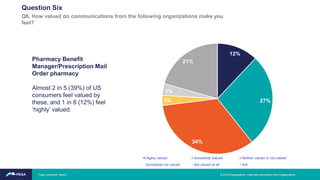

- 48. Pharmacy Benefit Manager/Prescription Mail Order pharmacy Almost 2 in 5 (39%) of US consumers feel valued by these, and 1 in 8 (12%) feel ‘highly’ valued. 12% 27% 34% 3% 3% 21% Highly valued Somewhat Valued Neither valued or not valued Somewhat not valued Not valued at all N/A Question Six Q6. How valued do communications from the following organizations make you feel? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 49. Pharmaceutical/Drug company More than a third (35%) of US consumers feel valued by their primary health insurer, and 1 in 9 (11%) feel ‘highly’ valued. 11% 24% 35% 5% 5% 20% Highly valued Somewhat Valued Neither valued or not valued Somewhat not valued Not valued at all N/A Question Six Q6. How valued do communications from the following organizations make you feel? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 50. Question Seven Q7. To what extent do you agree or disagree that the way these organizations communicate motivate you to engage more with the organization? 57% 36% 41% 29% 26% 7% 9% 11% 10% 12% Doctor's office Local Hospital Primary Health Insurer Pharmacy Benefit Manager/Prescription Mail Order pharmacy Pharmaceutical/Drug company Overall Agree (top2) Overall Disagree (bottom2) US consumers are most likely to agree that the way their doctor’s office communicates with them, motivates them to engage more with the organization. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 51. Doctor’s Office Almost 3 in 5 (57%) US consumers agree that the way their doctor’s office communicates with them motivates them to engage more with the organization, with almost a fifth (19%) ‘strongly’ agreeing with this. 19% 38% 32% 5% 2% 5% Strongly agree Agree Neither agree nor disagree Disagree Strongly disagree N/A Question Seven Q7. To what extent do you agree or disagree that the way these organizations communicate motivate you to engage more with the organization? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 52. Local Hospital More than a third (36%) of US consumers agree that the way their local hospital communicates with them motivates them to engage more with the organization, with 1 in 10 (10%) ‘strongly’ agreeing with this. 10% 26% 41% 7% 3% 14% Strongly agree Agree Neither agree nor disagree Disagree Strongly disagree N/A Question Seven Q7. To what extent do you agree or disagree that the way these organizations communicate motivate you to engage more with the organization? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 53. Primary Health Insurer More than 2 in 5 (41%) US consumers agree that the way their primary health insurer communicates with them motivates them to engage more with the organization, with 1 in 9 (11%) ‘strongly’ agreeing with this. 11% 30% 41% 8% 3% 7% Strongly agree Agree Neither agree nor disagree Disagree Strongly disagree N/A Question Seven Q7. To what extent do you agree or disagree that the way these organizations communicate motivate you to engage more with the organization? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

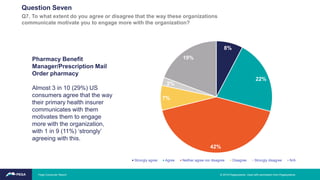

- 54. Pharmacy Benefit Manager/Prescription Mail Order pharmacy Almost 3 in 10 (29%) US consumers agree that the way their primary health insurer communicates with them motivates them to engage more with the organization, with 1 in 9 (11%) ‘strongly’ agreeing with this. 8% 22% 42% 7% 2% 19% Strongly agree Agree Neither agree nor disagree Disagree Strongly disagree N/A Question Seven Q7. To what extent do you agree or disagree that the way these organizations communicate motivate you to engage more with the organization? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 55. Pharmaceutical/Drug company More than a quarter (26%) of US consumers agree that the way a pharmaceutical/drug company communicates with them motivates them to engage more with the organization, with 1 in 14 (7%) ‘strongly’ agreeing with this. 7% 19% 43% 9% 4% 19% Strongly agree Agree Neither agree nor disagree Disagree Strongly disagree N/A Question Seven Q7. To what extent do you agree or disagree that the way these organizations communicate motivate you to engage more with the organization? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 56. Question Eight Q8. To what extent do you agree or disagree that the communications by these organizations make you want to do more to improve your health? 65% 40% 45% 27% 24% 6% 9% 11% 12% 15% Doctor's office Local Hospital Primary Health Insurer Pharmacy Benefit Manager/Prescription Mail Order pharmacy Pharmaceutical/Drug company Overall Agree (top2) Overall Disagree (bottom2) US consumers are most likely to agree that communications by their doctor’s office would make them want to do more to improve their health. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 57. Doctor’s Office 65% of US consumers agree that communications by their doctor’s office makes them want to do more to improve their health, with almost a quarter (24%) ‘strongly’ agreeing with this. 24% 41% 25% 4% 2% 4% Strongly agree Agree Neither agree nor disagree Disagree Strongly disagree N/A Question Eight Q8. To what extent do you agree or disagree that the communications by these organizations make you want to do more to improve your health? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

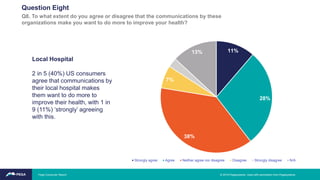

- 58. Local Hospital 2 in 5 (40%) US consumers agree that communications by their local hospital makes them want to do more to improve their health, with 1 in 9 (11%) ‘strongly’ agreeing with this. 11% 28% 38% 7% 3% 13% Strongly agree Agree Neither agree nor disagree Disagree Strongly disagree N/A Question Eight Q8. To what extent do you agree or disagree that the communications by these organizations make you want to do more to improve your health? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

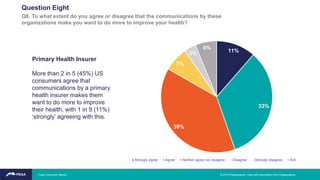

- 59. Primary Health Insurer More than 2 in 5 (45%) US consumers agree that communications by a primary health insurer makes them want to do more to improve their health, with 1 in 9 (11%) ‘strongly’ agreeing with this. 11% 33% 39% 7% 3% 6% Strongly agree Agree Neither agree nor disagree Disagree Strongly disagree N/A Question Eight Q8. To what extent do you agree or disagree that the communications by these organizations make you want to do more to improve your health? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

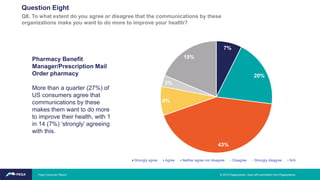

- 60. Pharmacy Benefit Manager/Prescription Mail Order pharmacy More than a quarter (27%) of US consumers agree that communications by these makes them want to do more to improve their health, with 1 in 14 (7%) ‘strongly’ agreeing with this. 7% 20% 43% 8% 3% 19% Strongly agree Agree Neither agree nor disagree Disagree Strongly disagree N/A Question Eight Q8. To what extent do you agree or disagree that the communications by these organizations make you want to do more to improve your health? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

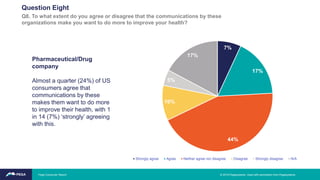

- 61. Pharmaceutical/Drug company Almost a quarter (24%) of US consumers agree that communications by these makes them want to do more to improve their health, with 1 in 14 (7%) ‘strongly’ agreeing with this. 7% 17% 44% 10% 5% 17% Strongly agree Agree Neither agree nor disagree Disagree Strongly disagree N/A Question Eight Q8. To what extent do you agree or disagree that the communications by these organizations make you want to do more to improve your health? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 62. Question Nine Q9. To what extent do you agree or disagree that you receive inconsistent information (i.e. wellness program information that is not personalized or that might provide conflicting guidance for multiple chronic conditions) from any of the following healthcare organizations? 26% 22% 28% 21% 23% 39% 27% 28% 22% 21% Doctor's office Local Hospital Primary Health Insurer Pharmacy Benefit Manager/Prescription Mail Order pharmacy Pharmaceutical/Drug company Overall Agree (top2) Overall Disagree (bottom2) US consumers are most likely to agree that they receive inconsistent information from their primary health insurer, and least likely to agree that they receive inconsistent information from their pharmacy benefit manager/prescription mail order pharmacy. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 63. Doctor’s Office More than a quarter (26%) of US consumers agree that they receive inconsistent information from their doctor’s office, and 1 in 12 (8%) strongly agree with this. 8% 18% 28% 27% 12% 8% Strongly agree Agree Neither agree nor disagree Disagree Strongly disagree N/A Question Nine Q9. To what extent do you agree or disagree that you receive inconsistent information (i.e. wellness program information that is not personalized or that might provide conflicting guidance for multiple chronic conditions) from any of the following healthcare organizations? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 64. Local Hospital Over a fifth (22%) of US consumers agree that they receive inconsistent information from their local hospital, and 7% ‘strongly’ agree with this. 7% 15% 33% 21% 7% 17% Strongly agree Agree Neither agree nor disagree Disagree Strongly disagree N/A Question Nine Q9. To what extent do you agree or disagree that you receive inconsistent information (i.e. wellness program information that is not personalized or that might provide conflicting guidance for multiple chronic conditions) from any of the following healthcare organizations? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 65. Primary Health Insurer Almost 3 in 10 (28%) US consumers agree that they receive inconsistent information from these, and 1 in 12 (8%) ‘strongly’ agree that they do. 8% 20% 34% 22% 7% 10% Strongly agree Agree Neither agree nor disagree Disagree Strongly disagree N/A Question Nine Q9. To what extent do you agree or disagree that you receive inconsistent information (i.e. wellness program information that is not personalized or that might provide conflicting guidance for multiple chronic conditions) from any of the following healthcare organizations? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 66. Pharmacy Benefit Manager/Prescription Mail Order pharmacy Just over a fifth (21%) of US consumers agree that they receive inconsistent information from these, and 1 in 16 (6%) ‘strongly’ agree that they do. 6% 15% 34%17% 5% 23% Strongly agree Agree Neither agree nor disagree Disagree Strongly disagree N/A Question Nine Q9. To what extent do you agree or disagree that you receive inconsistent information (i.e. wellness program information that is not personalized or that might provide conflicting guidance for multiple chronic conditions) from any of the following healthcare organizations? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

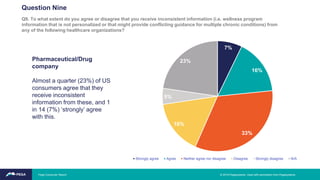

- 67. Pharmaceutical/Drug company Almost a quarter (23%) of US consumers agree that they receive inconsistent information from these, and 1 in 14 (7%) ‘strongly’ agree with this. 7% 16% 33% 16% 5% 23% Strongly agree Agree Neither agree nor disagree Disagree Strongly disagree N/A Question Nine Q9. To what extent do you agree or disagree that you receive inconsistent information (i.e. wellness program information that is not personalized or that might provide conflicting guidance for multiple chronic conditions) from any of the following healthcare organizations? © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 68. Question Ten Q10. What level of trust/confidence do you have in the following healthcare organizations? 78% 63% 52% 38% 33% 6% 9% 16% 13% 25% Doctor's office Local Hospital Primary Health Insurer Pharmacy Benefit Manager/Prescription Mail Order pharmacy Pharmaceutical/Drug company Overall Confident (top2) Overall Not Confident (bottom2) US Consumers have the most trust/confidence in the doctor’s office and the least trust/confidence in pharmaceutical/drug companies. © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 69. Question Ten Q10. What level of trust/confidence do you have in the following healthcare organizations? Doctor’s Office More than three quarters (78%) of US consumers are confident/trust their doctor’s office, and just over a third (36%) are ‘extremely’ confident in this. 36% 42% 14% 4% 2% 2% Extremely confident Somewhat confident Neutral Somewhat unconfident Extremely unconfident N/A © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 70. Question Ten Q10. What level of trust/confidence do you have in the following healthcare organizations? Local Hospital Almost two thirds (63%) of US consumers are confident/trust their local hospital, and just over a fifth (22%) are ‘extremely’ confident in it. 22% 41% 22% 6% 3% 6% Extremely confident Somewhat confident Neutral Somewhat unconfident Extremely unconfident N/A © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

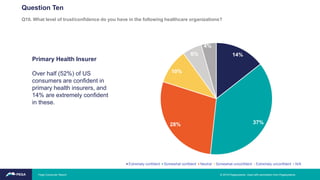

- 71. Question Ten Q10. What level of trust/confidence do you have in the following healthcare organizations? Primary Health Insurer Over half (52%) of US consumers are confident in primary health insurers, and 14% are extremely confident in these. 14% 37%28% 10% 6% 4% Extremely confident Somewhat confident Neutral Somewhat unconfident Extremely unconfident N/A © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 72. Question Ten Q10. What level of trust/confidence do you have in the following healthcare organizations? Pharmacy Benefit Manager/Prescription Mail Order pharmacy 38% of US consumers are confident in these with 1 in 9 (11%) saying they are ‘extremely’ confident. 11% 27% 31% 10% 4% 17% Extremely confident Somewhat confident Neutral Somewhat unconfident Extremely unconfident N/A © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report

- 73. Question Ten Q10. What level of trust/confidence do you have in the following healthcare organizations? Pharmaceutical/Drug company A third (33%) of US consumers are confident in these with 1 in 11 (9%) saying they are ‘extremely’ confident. 9% 24% 30% 15% 9% 12% Extremely confident Somewhat confident Neutral Somewhat unconfident Extremely unconfident N/A © 2019 Pegasystems. Used with permission from Pegasystems.Pega Consumer Report