Risk08a

- 1. Risk and Return The cost of Capital

- 2. Return on a Share or Stock Return or holding period return on a share is simply: P -P +D t t -1 t P t -1

- 3. Expected Return is E ( Pt +1) - Pt + E ( Dt +1) E ( Rt ) = Pt The lower the current price – other things being equal The greater the expected return

- 4. Rates of Return: Single Period Example Pt Ending Price = 48 Pt-1 Beginning Price = 40 Dividend = 2 The holding period return is HPR = (48 - 40 + 2 )/ (40) = 50/40 = 25%

- 5. The Value of an Investment of $1 in 1926 5520 S&P Small Cap 1828 1000 Corp Bonds Long Bond T Bill 55.38 Index 39.07 10 14.25 1 0.1 1925 1933 1941 1949 1957 1965 1973 1981 1989 1997 Source: Ibbotson Associates Year End

- 6. The Value of an Investment of $1 in 1926 S&P Real returns Small Cap 1000 Corp Bonds 613 Long Bond T Bill 203 Index 10 6.15 4.34 1 1.58 0.1 1925 1933 1941 1949 1957 1965 1973 1981 1989 1997 Source: Ibbotson Associates Year End

- 7. Volatility of Rates of Return 1926-1997 60 Percentage Return 40 20 0 -20 Common Stocks -40 Long T-Bonds T-Bills -60 26 30 35 40 45 50 55 60 65 70 75 80 85 90 95 Source: Ibbotson Associates Year

- 8. Risk A risky investment is one which has a range or spread of possible outcomes whose probabilities are known. A probability represents the chance or “odds” of a particular outcome to the investment. If something is certain it to occur is has a probability of one. If something is certain not to occur is has a probability of 0.

- 9. Probability If an outcome is uncertain it has a probability that is greater than 0 and less than 1. The probability of the total number of possible outcomes is 1 or 100%. The probability of an outcome or outcomes from the total number of possibilities is between 0% and 100% (0 and 1). The sum of the probabilities of all outcomes is 1.

- 10. Probability It may be helpful to think of probability in terms of the frequency of an outcome. the probability of getting a 6 when one throws a die is 1/6 or 0.1667. If you threw a die 600 times you would expect to throw 100 sixes.

- 11. Risk Free and Risky Projects Table 1 Project t0 t1 Prob. Expected Outlay Pay-off Return Certain A 100 120 1 20% Risky B 100 80 0.5 20% 160 0.5

- 12. Computation of Expected Return The expected return on a project is computed by taking the individual returns of A and B and multiplying them by their respective probabilities and summing them i.e. (-20%*0.5) + (60%*0.5) = -10%+30% = 20%.

- 13. Measuring Expected Return: Scenario or Subjective Returns Subjective returns s E (r ) = ∑ p s r s 1 p(s) = probability of a state r(s) = return if a state occurs 1 to s states

- 14. Investors' Attitudes to Risk We assume that investors are risk averse. This means that investors prefer an investment with a certain return to a risky one with the same expected return. A risk averse investor would prefer project A in Table 1 above to project B.

- 15. Will anyone invest in B? If the price of B falls its expected return will increase. Eventually the return will rise sufficiently for some investors to choose B rather than A. The rate of return of B at which the investor is indifferent between B and the risk free project A is called the certainty equivalent rate of return. If more than an investor’s certainty equivalent rate of return can be earned on B she will choose it over A.

- 16. Risk and Return Unless risky investments are likely to offer greater returns than relatively safe ones nobody will hold them. If markets are competitive investors are unlikely to be able to increase expected returns without investing in assets which bear additional risk.

- 17. A Premium for Risk Therefore any asset that is traded in a competitive market will have an expected return that is increasing in risk. We can characterise the expected return on any asset traded in the capital markets in the form: Expected rate of return = risk-free rate + risk premium.

- 18. Measurement of Risk In Finance risk is usually measured by the amount of dispersion or variability in the value of an asset. Thus, risky assets can have very positive outcomes as well as very negative ones. One has upside risk (potential) and downside risk

- 19. Measuring Risk Variance - Average value of squared deviations from mean. A measure of volatility. Standard Deviation – The square root of the average value of squared deviations from mean. a measure of volatility. Has advantage of being measured in the same dimension as the mean.

- 20. Characteristics of Probability Distributions 1) Mean: most likely value 2) Variance or standard deviation – measure of spread 3) Skewness – refers to the tendency to have extreme outliers either at the top or bottom of the distribution. * If a distribution is approximately normal, the distribution is described by characteristics 1 and 2.

- 21. Random Variable A random variable is a variable which can take on a range of different values and we are never certain which value it is going to take on at a particular time. The return on a risky project or investment can be perceived as a random variable.

- 22. Probability analysis •Expected return of a project or investment •Standard deviation of a project or investment •The mean–variance rule

- 23. The expected return n R = Σ R i pi i =1 R = expected return, Ri = return if event i occurs pi = probability of event i occurring, n = number of events

- 24. Standard deviation •Standard deviation, σ, is a statistical measure of the dispersion around the expected value •The standard deviation is the square root of the variance, σ2 – – – Variance of x = σ2 = (x1 –x)2 p1 + (x2 –x)2 p2 + … (xn – x)2 pn x i=n or σ = x 2 Σ i=1 – {(xi – x)2 pi} Standard deviation √Σ i=n √σ 2 σx = or – {(xi – x)2 pi} x i=1

- 25. Standard deviation √Σ n σ = (Ri – Ri)2 pi i =1

- 26. Standard Deviation – historic data Most commonly used measure of variation Shows variation about the mean Is the square root of the variance Has the same units as the original data n ∑ (X − X) i 2 Sample standard deviation: S= i =1 n -1

- 27. Calculation Example: Sample Standard Sample Deviation Data (Xi) : 10 12 14 15 17 18 18 24 n=8 Mean = X = 16 (10 − X)2 +(12 − X)2 +(14 − X)2 + +(24 − X)2 S= n −1 (10 −16)2 +(12 −16)2 +(14 −16)2 + +(24 −16)2 = 8 −1 130 A measure of the “average” = = 4.3095 7 scatter around the mean

- 28. Measuring variation Small standard deviation Large standard deviation

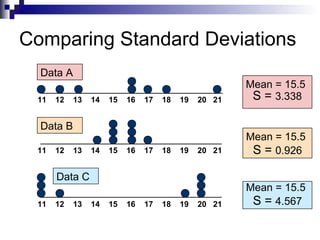

- 29. Comparing Standard Deviations Data A Mean = 15.5 11 12 13 14 15 16 17 18 19 20 21 S = 3.338 Data B Mean = 15.5 11 12 13 14 15 16 17 18 19 20 21 S = 0.926 Data C Mean = 15.5 11 12 13 14 15 16 17 18 19 20 21 S = 4.567

- 30. Advantages of Variance and Standard Deviation Each value in the data set is used in the calculation Values far from the mean are given extra weight (because deviations from the mean are squared)

- 31. The Empirical Rule If the data distribution is approximately bell- shaped, then the interval: μ ± 1σ contains about 68% of the values in the population or the sample 68% μ μ ± 1σ

- 32. The Empirical Rule μ ± 2σ contains about 95% of the values in the population or the sample μ ± 3σ contains about 99.7% of the values in the population or the sample 95% 99.7% μ ± 2σ μ ± 3σ

- 33. Markowitz Portfolio Theory Price changes vs. Normal distribution Microsoft - Daily % change 1986-1997 600 500 (frequency) # of Days 400 300 200 100 0 -10% -8% -6% -4% -2% 0% 2% 4% 6% 8% 10% Daily % Change

- 34. Markowitz Portfolio Theory Price changes vs. Normal distribution 600Microsoft - Daily % change 1986-1997 500 (frequency) # of Days 400 300 200 100 0 -10% -8% -6% -4% -2% 0% 2% 4% 6% 8% 10% Daily % Change

- 35. Bootstrapped history vs. Normal Distribution

- 36. Normal Distribution s.d. s.d. mean Symmetric distribution

- 37. The lower the standard deviation the lower the risk. Investment A is less risky than investment B in the figure 1 below because it has the lower standard deviation

- 38. Figure 1

- 39. Characteristics of Risk Thus, there are at least three aspects to risk that we must capture. First, the probability of having a poor outcome Second the potential size of this poor outcome. Third risky investments must provide the chance of higher returns to compensate for the poor ones and thus give an above average expected return. This is what we mean by the spread of possible outcomes Provided we have symmetric distributions standard deviation will capture all these elements

- 40. Risk is not just the probability of making a loss Consider two investments which have the same probability of making a loss. Are both investments equally risky?

- 41. An investment costs €10,000 Payoffs Investment Probability 0.5 Probability 0.5 A 20,000 9,000 B 20,000 1,000 In terms of percentage return Investment Prob. 0.5 Prob. 0.5 Expected Standard Return Deviation A 100 -10 45 55 B 100 -90 5 95

- 42. The computation of Standard Deviation Computation of Standard Deviation of A Return Mean Ret. X - Mean(X) (xi – x)2 prob 100 45 55 3025 0.5 1512.5 -10 45 -55 3025 0.5 1512.5 Variance 3025 Standard Deviation 55

- 43. The probability of making a loss is the same for each investment but investment B is certainly more risky. This is because the size of the potential loss is greater. Thus, there are at least two aspects to risk that we must capture. First, the probability of having a poor outcome and second the potential size of this poor outcome. A measure of spread or dispersion will embody both of these elements. We note that the standard deviation of B is certainly larger than that of A.

Editor's Notes

- 13

- 13

- 14