European Union survey of digital banking progress

- 1. www.ecb.europa.eu © Take-aways from the horizontal assessment of the survey on digital transformation and the use of fintech ECB Banking Supervision 15 February 2023 ECB-CONFIDENTIAL ECB-PUBLIC

- 2. www.bankingsupervision.europa.eu © Contents ECB-PUBLIC 2 1. Overview 2. Horizontal assessment of the digital transformation survey I. Digital strategy and KPI steering II. Digital business III. Investments and resources IV. Governance and cooperation V. Use of innovative technologies VI. Risks/challenges 3. Concluding remarks and supervisory focus

- 3. www.bankingsupervision.europa.eu © 3 1. Overview – six focus points for digital transformation strategies ECB Banking Supervision (ECB and NCAs) conducted the first Single Supervisory Mechanism (SSM)-wide data collection on digital transformation and fintech based on banks’ self assessments and combined this with market intelligence initiatives to build knowledge on this evolving field of expertise. This led to some preliminary insights: • Digital transformation is relevant for all SSM banks, and most of them have a digital transformation strategy in place. • Digital transformation can be defined as a bundle of business model, processes and cultural transformation, enabled by technologies. • There is a high degree of heterogeneity in banks’ submissions and further dialogue is needed to validate them. Digital strategy and KPI steering Governance and cooperation Digital business Investments and resources Risks/ challenges Use of innovative technologies ECB-PUBLIC ECB Banking Supervision identified six focus points to shape a framework for supervisors when looking into digital transformation strategies:

- 4. www.bankingsupervision.europa.eu © 4 1st focus point : Digital strategy and KPI steering The majority of banks only started to develop their digital transformation strategy in recent years, targeting revenues and cost objectives. • The most important digital projects carried out by SSM banks are broadly in line with the key objectives of digital strategies: attract and retain market share and achieve efficiency gains. • 43% of banks’ top-5 projects are aimed at revenue/ customer experience enhancement. • 83% of banks see process automation as a key lever to reduce costs (mainly through IT legacy transformation). • Banks develop KPIs to monitor customers’ preferences. • However, even given the multi-faceted nature of digital transformation, banks still find it difficult to isolate and quantify the cost and revenue impacts of their digital transformation strategies and processes. Categorisation of banks’ KPIs Objectives of key digital projects ECB-PUBLIC 62% 18% 5% 3% 12% Customers Tech and Processes Costs Revenues Others

- 5. www.bankingsupervision.europa.eu © 14% 23% 35% 59% 23% 34% 51% 22% 29% 50% 38% 26% 34% 27% 31% 36% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Internet Mobile 44% 50% 32% 11% 49% 19% 46.0% 5 Internet vs mobile customers (% of total customers) Digitally concluded loans (% of total loans) 2nd focus point: Digital business Most digital strategies are customer-centric, but keeping track of digital customers and sales remains heterogeneous • There is widespread willingness to improve customer experience by conducting business digitally: banks identify almost half of their customer base as digital. • The mobile channel is more popular than internet banking, especially for bigger banks: 36% of bank customers use mobile banking while 21% use internet banking. • Monitoring the actual use and contribution of digital channels is heterogeneous: • Half of the sampled banks do not monitor the number of customers digitally onboarded. • Only one in four banks can quantify the volume of digital sales. • Half of the sampled banks monitor the number of digitally concluded loans (e.g. pre-decided loans, consumer credit), which stands at around 45% of their total loan portfolio. ECB-PUBLIC

- 6. www.bankingsupervision.europa.eu © 6.5% 5.6% 2.9% 4.8% 3.0% 3.4% 3.8% 5.2% 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0% 9.0% 10.0% 2.9% 3.3% 2.1% 2.0% 2.0% 3.1% 1.2% 2.8% 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 6 3rd focus point: Investments and resources The self-assessment provided a very preliminary estimate of banks’ digital spending at the end of 2021 • On average, banks invested 2.8% of their operating income1 in digital transformation projects in 2021. • 61% of banks reported having a digital transformation budget embedded in the IT budget. For these banks, their digital transformation budget is reported to be 22% of the IT budget. • On average, banks allocated 5.2% of their workforce2 to digital transformation projects at the end of 2021. • The heterogeneity in the answers provided may result in a diverging image for individual banks, particularly as digitalisation is on average found to be more advanced in retail oriented business. 1 Finrep – Net operating income {F.02.00 - R.0355 ; C.0010} 2 Finrep – Total staff {F.44.04 - R.0050 ; C.0020} Digital transformation budget as % of operating income ECB-PUBLIC Digital transformation FTEs as % of total staff

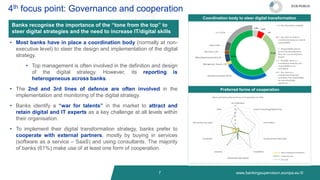

- 7. www.bankingsupervision.europa.eu © 7 4th focus point: Governance and cooperation Banks recognise the importance of the “tone from the top” to steer digital strategies and the need to increase IT/digital skills • Most banks have in place a coordination body (normally at non- executive level) to steer the design and implementation of the digital strategy. • Top management is often involved in the definition and design of the digital strategy. However, its reporting is heterogeneous across banks. • The 2nd and 3rd lines of defence are often involved in the implementation and monitoring of the digital strategy. • Banks identify a “war for talents” in the market to attract and retain digital and IT experts as a key challenge at all levels within their organisation. • To implement their digital transformation strategy, banks prefer to cooperate with external partners, mostly by buying in services (software as a service – SaaS) and using consultants. The majority of banks (61%) make use of at least one form of cooperation. Coordination body to steer digital transformation Preferred forms of cooperation ECB-PUBLIC

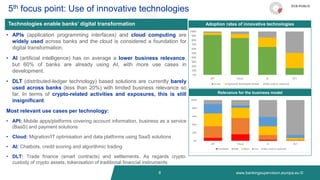

- 8. www.bankingsupervision.europa.eu © 8 5th focus point: Use of innovative technologies Technologies enable banks’ digital transformation • APIs (application programming interfaces) and cloud computing are widely used across banks and the cloud is considered a foundation for digital transformation. • AI (artificial intelligence) has on average a lower business relevance, but 60% of banks are already using AI, with more use cases in development. • DLT (distributed-ledger technology) based solutions are currently barely used across banks (less than 20%) with limited business relevance so far. In terms of crypto-related activities and exposures, this is still insignificant. Most relevant use cases per technology: • API: Mobile apps/platforms covering account information, business as a service (BaaS) and payment solutions • Cloud: Migration/IT optimisation and data platforms using SaaS solutions • AI: Chatbots, credit scoring and algorithmic trading • DLT: Trade finance (smart contracts) and settlements. As regards crypto: custody of crypto assets, tokenisation of traditional financial instruments Adoption rates of innovative technologies Relevance for the business model ECB-PUBLIC

- 9. www.bankingsupervision.europa.eu © 9 Banks identify key risks and challenges triggered by digital transformation • Risks associated with digital transformation are mainly perceived as cyber risk, increased third-party dependency, AML/fraud and potential loss of customers. • Key challenges to digital transformation are having the relevant experience and cybersecurity. • In addition, complexity, legacy IT and lack of internal skills are leading to dependency on third parties and are perceived as a challenge. • Cost management is a further challenge as digital transformation is often run under tight investment constraints. Key risks Key challenges 6th focus point: Key risks/challenges and risk management ECB-PUBLIC

- 10. www.bankingsupervision.europa.eu © 10 3. Concluding remarks and supervisory focus • ECB Banking Supervision’s focus is on the assessment of the impact of digital transformation on risks in terms of: • strategic risk (e.g. sustainability of the digital transformation strategy, consistency with the business model, capabilities building and adequacy); • governance and risk management framework; • IT and operational risks; • potential new/emerging risks. • The SSM remains business model and technology neutral, while acknowledging the importance of enhancing understanding of the impact of digital transformation on banks’ business model sustainability and risk management. ECB-PUBLIC