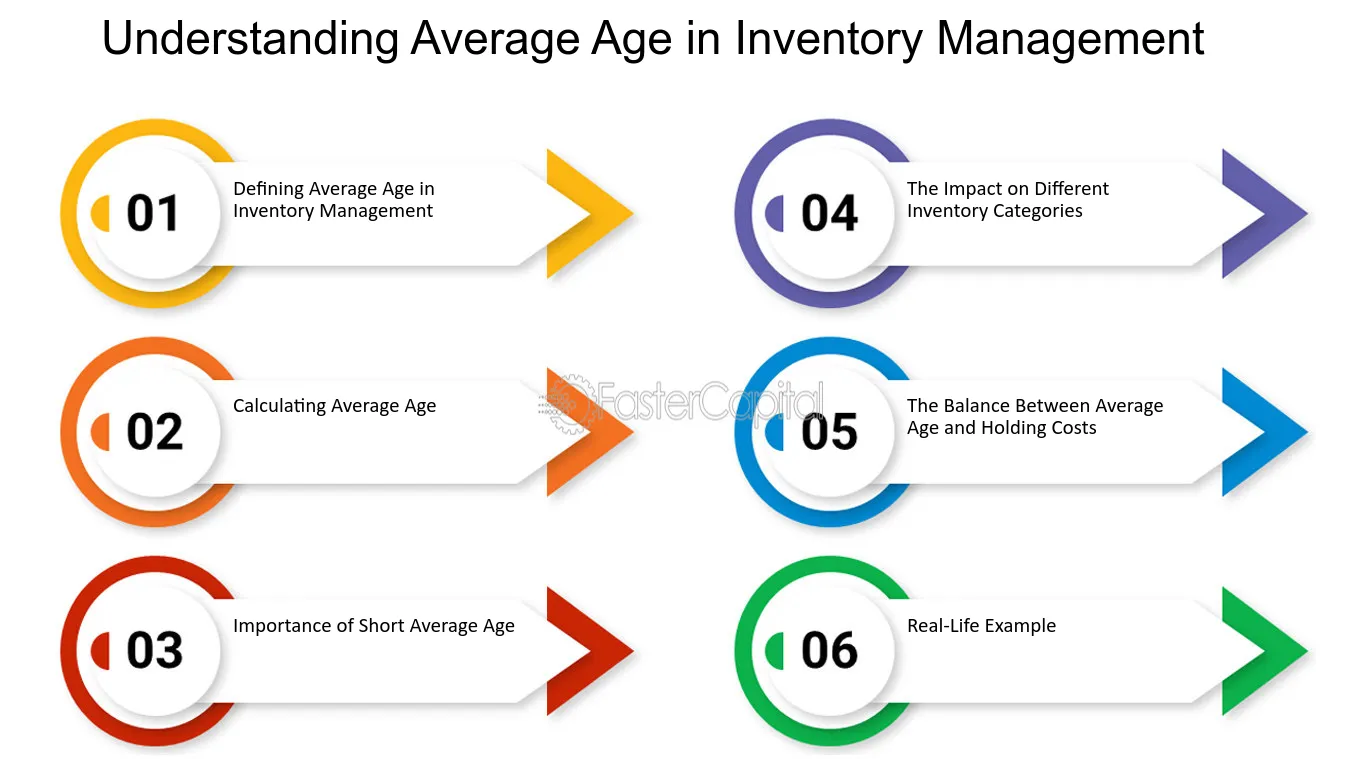

1. Understanding Average Age in Inventory Management

In the realm of inventory management, understanding the concept of average age is vital for optimizing the allocation and movement of goods. It plays a pivotal role in the ABC analysis method, a renowned strategy for categorizing inventory items into different classes based on their importance and value. This blog section delves deep into the intricacies of average age, shedding light on why it matters, how it's calculated, and the impact it has on your inventory management decisions.

1. Defining average Age in inventory Management:

Average age, also known as the average holding period or average age of inventory, refers to the mean time an item stays in your inventory before being sold or used. It is a crucial metric as it offers insights into the efficiency of your inventory turnover. The shorter the average age, the faster your goods are moving, which can free up capital and reduce holding costs.

2. Calculating Average Age:

Calculating average age is relatively straightforward. You sum the number of days each item spends in your inventory, and then divide this total by the number of items. Here's an example: If you have three items with ages of 10 days, 20 days, and 30 days, the average age would be (10 + 20 + 30) / 3 = 20 days.

3. Importance of Short Average Age:

Shortening the average age of inventory is often a goal for businesses aiming to optimize their inventory management. This directly impacts your cash flow by reducing the amount of capital tied up in unsold goods. It also minimizes the risk of obsolescence and spoilage, as fresher items are less likely to become outdated.

4. The Impact on Different Inventory Categories:

Different categories of inventory items are affected by average age in distinct ways. For instance, fast-moving products, categorized as "A" items in the ABC analysis, benefit from shorter average ages. This ensures that popular items remain in stock and readily available to meet customer demand. On the other hand, slow-moving items ("C" items) might have a longer average age, as they don't sell as quickly.

5. The Balance Between Average Age and Holding Costs:

While a short average age is desirable for improved cash flow, it's essential to strike a balance with holding costs. You may need to hold some items for a longer time due to seasonality, supplier lead times, or other factors. Careful analysis of each inventory item's specific requirements is necessary to optimize the average age effectively.

6. Real-Life Example:

Let's consider an electronics retailer. High-end smartphones ("A" items) should have a short average age to meet the ever-changing consumer demand. In contrast, accessories like phone cases ("C" items) can have a longer average age since they don't become obsolete as quickly.

In summary, understanding and managing the average age of inventory is a critical aspect of efficient inventory management. It impacts your cash flow, holding costs, and the availability of products to meet customer demand. Different categories of items require different average ages, and finding the right balance can be a key factor in your business's success. The ABC analysis method helps categorize items and prioritize efforts to manage average age effectively.

Understanding Average Age in Inventory Management - ABC analysis: Prioritizing Inventory Management for Average Age

2. Understanding Average Daily Float

The average daily float is the amount of time between when a check is deposited and when the funds become available in the account. It is an important factor to consider when it comes to check clearing because it affects the speed at which funds can be accessed. Understanding average daily float is essential for businesses and individuals who rely on checks as a form of payment. In this section, we will discuss the different aspects of average daily float and how it impacts check clearing.

1. Definition of Average Daily Float

Average daily float is the amount of time between when a check is deposited and when the funds become available in the account. It is calculated by taking the total amount of checks deposited and dividing it by the number of days it takes for the funds to become available. For example, if a business deposits $10,000 worth of checks and it takes five days for the funds to become available, the average daily float would be $2,000 ($10,000 divided by five days).

2. Factors that affect Average daily Float

There are several factors that can affect average daily float, including the type of check, the financial institution, and the deposit method. For instance, government checks and cashier's checks typically have a shorter float time compared to personal checks. The financial institution also plays a role in determining the float time, as some banks have longer processing times than others. The deposit method can also impact the float time, with in-person deposits typically having a shorter float time than mobile or ATM deposits.

3. Importance of Average Daily Float

Understanding average daily float is essential for businesses and individuals who rely on checks as a form of payment. It can help them plan their cash flow and avoid overdraft fees. For businesses, a longer float time can impact their ability to pay bills and make payroll on time. By understanding the average daily float, they can plan accordingly and avoid cash flow issues.

4. Strategies to Reduce Average Daily Float

There are several strategies that businesses and individuals can use to reduce their average daily float. One option is to use electronic payments, such as ACH or wire transfers, instead of checks. Electronic payments have a shorter processing time and funds are typically available within one to two days. Another option is to use remote deposit capture, which allows businesses to deposit checks electronically using a scanner. This method can reduce the float time and improve cash flow.

5. Conclusion

Understanding average daily float is essential for businesses and individuals who rely on checks as a form of payment. By understanding the factors that impact float time and using strategies to reduce it, they can improve their cash flow and avoid overdraft fees. Using electronic payments and remote deposit capture can be effective ways to reduce average daily float and speed up check clearing.

Understanding Average Daily Float - Accelerating Check Clearing: Insights into Average Daily Float

3. Understanding the Average Cost Basis Method

1. The Average Cost Basis Method: A Comprehensive Overview

Understanding the Average Cost Basis Method is crucial for accurate portfolio valuation. This method, often employed by investors and financial professionals, calculates the average cost of acquiring assets over time. By using this method, individuals can accurately determine their capital gains or losses when selling a portion of their investments. Let's delve into the intricacies of this method and explore its advantages and disadvantages.

2. How Does the Average Cost Basis Method Work?

The Average Cost Basis Method calculates the average cost of all shares or units purchased over time, including any additional investments or reinvested dividends. This method is particularly useful for investments such as mutual funds or exchange-traded funds (ETFs) that involve periodic contributions.

For instance, imagine an investor who purchases 100 shares of a mutual fund at $10 per share. After a year, the investor decides to buy an additional 50 shares at $12 per share. The average cost per share under the Average Cost Basis Method would be calculated as follows:

(100 shares $10 per share + 50 shares $12 per share) / (100 shares + 50 shares) = $10.67 per share

3. Advantages of the Average Cost Basis Method

- Simplicity: The Average Cost Basis Method is straightforward and easy to understand. Investors can simply track their purchases and calculate the average cost per share, eliminating the need for complex calculations.

- Tax Efficiency: This method can be tax-efficient since it allows investors to minimize their capital gains taxes. By calculating the average cost basis, investors can accurately determine the cost of their shares and reduce the taxable amount when selling.

- Automatic Reinvestment: The Average Cost Basis Method is particularly beneficial for investments that offer automatic reinvestment of dividends. This method automatically factors in reinvested dividends when calculating the average cost basis, providing a more accurate valuation.

4. Disadvantages of the Average Cost Basis Method

- Limited Customization: The Average Cost Basis Method does not allow for customization based on specific share lots. This means that investors cannot choose which shares they sell to optimize their tax liabilities or maximize gains.

- Potential for Higher Taxes: In some cases, the Average Cost Basis Method may result in higher taxes compared to other methods, such as specific identification. This is especially true for investments with significant appreciation over time, as the average cost basis may be higher than the actual cost of the shares sold.

5. Alternatives to the Average Cost Basis Method

- Specific Identification: Unlike the Average Cost Basis Method, specific identification allows investors to select which shares they want to sell. This method offers more flexibility in managing capital gains and losses, but it requires meticulous record-keeping and may not be suitable for all investors.

- First-In, First-Out (FIFO): FIFO assumes that the first shares purchased are the first ones sold. This method is simple to implement and may provide tax advantages, particularly in a rising market. However, it may not always reflect the investor's actual intent or investment strategy.

6. Choosing the Best Option

Ultimately, choosing the best cost basis method depends on the investor's goals, tax situation, and investment strategy. While the Average Cost Basis Method offers simplicity and tax efficiency, specific identification may be more suitable for investors seeking greater control over their tax liabilities. FIFO can be a viable option for those looking for a straightforward approach.

Understanding the Average Cost Basis Method empowers investors to make informed decisions regarding their investments and accurately calculate their gains or losses. By considering the advantages and disadvantages of different cost basis methods, individuals can optimize their portfolio valuation and effectively manage their tax liabilities.

Understanding the Average Cost Basis Method - Accurate Portfolio Valuation with Average Cost Basis Method

4. Understanding the Average Cost Basis Method

Understanding the Average Cost Basis Method

When it comes to managing investments, tax efficiency is an important factor to consider. One method that can help achieve tax efficiency is the average cost basis method. This method allows investors to calculate the average cost of their investments over time, which can be particularly useful when dealing with mutual funds or other investments that involve regular purchases or sales. By understanding how the average cost basis method works and its potential benefits, investors can make informed decisions that can help minimize their tax liabilities.

1. What is the average cost basis method?

The average cost basis method is a way to determine the cost of an investment by calculating the average price paid for all shares or units owned. Instead of tracking the cost of each individual purchase, this method takes into account the total cost of all purchases and divides it by the total number of shares or units owned. This approach provides a simplified way to determine the cost basis of investments, especially for those with a long history of purchases and sales.

2. How does the average cost basis method work?

Let's consider an example to better understand how the average cost basis method works. Suppose an investor purchases 100 shares of a mutual fund at $10 per share in Year 1 and an additional 100 shares at $12 per share in Year 2. The total cost of the investment would be $2,200 ($1,000 in Year 1 + $1,200 in Year 2). The average cost per share would then be $11 ($2,200 / 200 shares). If the investor decides to sell 50 shares in Year 3 when the market price is $15 per share, the cost basis for those shares would be $550 (50 shares x $11). As a result, the capital gain would be $200 (50 shares x ($15 - $11)).

3. How does the average cost basis method compare to other methods?

The average cost basis method is just one of several methods used to calculate the cost basis of investments. Other methods include specific identification and first-in, first-out (FIFO). Specific identification allows investors to choose which shares to sell when making a sale, which can help optimize tax outcomes. FIFO, on the other hand, assumes that the first shares purchased are the first ones sold. While each method has its own advantages, the average cost basis method provides a simplified approach that can be particularly beneficial for investors who regularly purchase or sell shares.

4. What are the benefits of using the average cost basis method?

Using the average cost basis method can offer several benefits. Firstly, it simplifies the calculation of the cost basis by taking into account the total cost of all purchases. This can save time and effort, especially for investors with a long history of transactions. Additionally, the average cost basis method can help minimize the tax liability by spreading out the gains or losses over time, potentially reducing the impact of short-term capital gains taxes. This can be advantageous for investors who hold their investments for the long term.

5. Is the average cost basis method the best option for everyone?

While the average cost basis method can be a helpful tool for many investors, it may not be the best option for everyone. Investors who prefer to have more control over their tax outcomes may find specific identification or FIFO methods more suitable. Specific identification allows investors to strategically choose which shares to sell, potentially minimizing tax liabilities. FIFO, on the other hand, may be preferred by those who want a straightforward and transparent approach. Ultimately, the best method depends on individual circumstances and preferences.

Understanding the average cost basis method can empower investors to make more informed decisions when managing their investments. By considering the benefits and drawbacks of different cost basis calculation methods, investors can select the approach that aligns with their goals and helps them achieve tax efficiency. Whether it's using the average cost basis method or exploring other alternatives, being aware of the available options is crucial for maximizing investment returns while minimizing tax liabilities.

Understanding the Average Cost Basis Method - Achieving Tax Efficiency with Average Cost Basis Method

5. Understanding Average Daily Trading Volume

1. Understanding Average Daily Trading Volume

The average daily trading volume is a crucial metric used by investors and traders to analyze market activity. It represents the number of shares or contracts traded on average in a particular security or market over a specified time period. This metric provides valuable insights into the liquidity and overall interest in a stock, bond, or commodity.

From an investor's perspective, understanding the average daily trading volume helps determine the ease with which one can buy or sell a security without significantly impacting its price. Higher trading volumes generally indicate greater market liquidity, making it easier to enter or exit a position without causing significant price fluctuations. On the other hand, lower trading volumes can indicate illiquidity, potentially resulting in wider bid-ask spreads and difficulty in executing trades.

1.1 Factors Influencing Average Daily Trading Volume

Several factors can influence the average daily trading volume of a security. These factors can vary depending on the specific market or instrument being analyzed. Here are some key factors to consider:

1. Market conditions: Economic events, news releases, and market sentiment can significantly impact trading volumes. For example, during periods of heightened market volatility, trading volumes tend to increase as investors react to news and adjust their positions.

2. Company-specific factors: Earnings announcements, mergers and acquisitions, product launches, or regulatory events can drive trading volumes in individual stocks. For instance, when a company reports better-than-expected earnings, it often attracts higher trading volumes as investors rush to capitalize on the positive news.

3. Seasonality: Some securities may exhibit seasonal patterns in trading volumes. For instance, retail stocks may experience higher volumes during the holiday shopping season.

1.2 Interpreting Average Daily Trading Volume

To effectively interpret average daily trading volume, it's essential to compare it against historical data and similar securities. Here are a few considerations when analyzing this metric:

1. Relative volume analysis: Comparing the average daily trading volume of a security to its historical average or the average volume of peer securities can provide insights into whether current trading activity is above or below normal levels. Significant deviations from the norm can indicate increased investor interest or potential market manipulation.

2. Volume patterns: Examining volume patterns over time can reveal valuable information. For example, a consistent increase in trading volume over several days may indicate growing momentum or a potential trend reversal. Conversely, declining volume during a price rally might suggest weakening investor interest and a possible market correction.

3. Confirmation of price movements: Volume often confirms price movements. If a stock experiences a significant price increase accompanied by above-average trading volume, it suggests strong buying interest and reinforces the bullish sentiment. Conversely, a price decline on high trading volume may indicate increased selling pressure and further downside potential.

1.3 Best Practices for utilizing Average daily Trading Volume

When utilizing average daily trading volume for market analysis, it's important to keep the following best practices in mind:

1. Compare across timeframes: Analyzing average daily trading volume across multiple timeframes (e.g., daily, weekly, monthly) allows for a comprehensive assessment of market activity. This helps identify short-term fluctuations and long-term trends in trading volumes.

2. Use volume in conjunction with other indicators: Average daily trading volume should be used in conjunction with other technical and fundamental indicators to gain a holistic view of market activity. Combining volume analysis with price patterns, moving averages, and fundamental data can enhance the accuracy of trading decisions.

3. Consider sector-specific characteristics: Different sectors may have distinct average daily trading volume patterns. For example, technology stocks often exhibit higher trading volumes compared to utility stocks due to their higher volatility and investor interest. Understanding sector-specific characteristics helps in setting realistic expectations when evaluating trading volumes.

Understanding average daily trading volume empowers investors and traders to make informed decisions based on market activity. By considering the factors influencing volume, interpreting its patterns, and following best practices, individuals can effectively utilize this metric to analyze market trends and optimize their trading strategies.

Understanding Average Daily Trading Volume - Analyzing Market Activity through Average Daily Trading Volume

6. Understanding Average Variable Cost and Marginal Cost

In the world of economics, it is crucial to have a clear understanding of various cost concepts to make informed decisions and analyze the impact of these costs on business operations. Two such important concepts are average variable cost (AVC) and marginal cost (MC). In this section, we will delve into the meaning and significance of these costs and explore their relationship.

To start off, let's define average variable cost (AVC). This cost refers to the average cost incurred in producing each unit of output, considering only the variable costs involved. Variable costs are expenses that change in direct proportion to the level of production. They include costs such as raw materials, direct labor, and utilities. By calculating the AVC, businesses can determine the cost per unit of production and assess their efficiency in utilizing resources.

On the other hand, marginal cost (MC) represents the cost of producing one additional unit of output. It is derived by calculating the change in total cost resulting from producing one more unit. Marginal cost helps businesses determine the optimal level of production and make decisions regarding increasing or decreasing output.

To better understand the relationship between AVC and MC, let's consider an example. Imagine a bakery that produces cakes. The variable costs involved in cake production include the cost of ingredients, labor, and electricity. As the bakery increases its production, it needs to hire more workers, purchase additional ingredients, and use more electricity. The AVC would be calculated by dividing the total variable costs by the number of cakes produced. Meanwhile, the MC would be determined by the change in total cost resulting from producing one more cake.

It is important to note that AVC and MC are closely related. In fact, the MC curve is derived from the AVC curve. The AVC curve usually decreases initially due to economies of scale, where the cost per unit decreases as production increases. However, as production continues to increase, the AVC curve starts to rise due to diminishing returns. The MC curve intersects the AVC curve at its lowest point, which represents the level of production where the AVC is at its minimum.

Understanding the relationship between AVC and MC can provide invaluable insights for businesses. By analyzing these costs, businesses can optimize their production processes, identify cost-saving opportunities, and make informed pricing decisions. For instance, if the MC exceeds the AVC, it indicates that producing one more unit would result in higher costs than the average cost per unit. In such cases, businesses may consider reducing production or increasing prices to maintain profitability.

In conclusion, understanding average variable cost (AVC) and marginal cost (MC) is essential for businesses to analyze their cost structures and make informed decisions. By calculating the AVC and MC, businesses can assess their efficiency, determine the optimal level of production, and identify cost-saving opportunities. By leveraging these cost concepts, businesses can strive for greater profitability and sustainability in today's competitive market.

7. Understanding Average Annual Returns

When it comes to measuring investment performance, average annual returns are one of the most important metrics to understand. It is a measure of the average rate at which an investment grows or declines over a certain period of time, and it is a key factor in determining how much money you make or lose on your investments. Understanding average annual returns is crucial for investors, as it helps them to make informed investment decisions, assess risk, and evaluate the performance of their portfolio.

Here are some key insights to help you better understand average annual returns:

1. average annual returns are calculated by taking the total return of an investment over a certain period of time and dividing it by the number of years in that period. For example, if an investment returned 20% over a five-year period, its average annual return would be 4%.

2. Average annual returns can be calculated for different types of investments, such as stocks, bonds, mutual funds, and exchange-traded funds (ETFs). It is important to note that different types of investments may have different levels of risk and return, which can affect their average annual returns.

3. Average annual returns can be affected by market volatility. For example, if an investment experiences a large gain one year and a large loss the next year, its average annual return may be lower than if it had experienced more consistent returns over the same period.

4. It is important to consider the time period over which average annual returns are calculated. Short-term performance may not be indicative of long-term performance, and investors should consider the historical performance of an investment over a longer period of time.

5. Average annual returns do not take into account the effects of taxes and fees on investment returns. It is important for investors to consider the impact of taxes and fees when evaluating the performance of an investment.

Understanding average annual returns is a key factor in evaluating investment performance. By calculating and analyzing average annual returns, investors can make informed decisions about their investments and assess the risk and return of their portfolio.

Understanding Average Annual Returns - Average Annual Returns: Measuring Money Weighted Returns

8. Understanding Average Cost Flow Method

Understanding Average Cost Flow Method

In the realm of inventory management, businesses often grapple with the challenge of choosing the right cost flow method to effectively manage their inventory and financial records. One such method is the Average Cost Flow method, which, alongside LIFO (Last-In, First-Out), is commonly employed by businesses to determine the cost of goods sold (COGS) and the value of ending inventory. In this section, we will delve into the intricacies of the Average Cost Flow method, exploring its advantages, disadvantages, and how it compares to other methods.

1. Calculation of Average Cost:

- The Average Cost Flow method, as the name suggests, calculates the cost of inventory by taking the average of the unit costs over a specific accounting period.

- To calculate the average cost, you sum up the total cost of all units in stock and divide it by the total number of units.

- For instance, if a business has 100 units of a product with a total cost of $1,000, the average cost per unit would be $10 ($1,000 ÷ 100).

2. Smoothed Cost Fluctuations:

- One of the key advantages of using the Average Cost Flow method is that it smoothens out the fluctuations in the cost of inventory.

- This can be particularly beneficial for businesses dealing with products that experience frequent price changes.

- For example, if a company sells electronics, where prices can fluctuate due to market demand and supply, using the Average Cost Flow method can provide a more stable and predictable cost base.

3. Simplicity and Ease of Use:

- The Average Cost Flow method is relatively simple to apply and does not require complex tracking of individual inventory purchases.

- This simplicity can be advantageous for small businesses or those with limited resources for sophisticated inventory management systems.

4. Disadvantages of Average Cost Flow:

- While the method offers simplicity, it may not always reflect the actual cost of goods sold accurately.

- For businesses with inventory items that vary significantly in cost, the average cost may not represent the current market value of their products.

- This can lead to potential inaccuracies in financial reporting.

5. Comparing Average Cost Flow to LIFO:

- When comparing Average Cost Flow to LIFO, the choice depends on various factors, including the nature of the inventory and the desired financial outcomes.

- LIFO assumes that the last items purchased are the first to be sold, which can provide tax advantages by lowering reported income during periods of rising costs.

- However, LIFO may not always align with the physical flow of inventory and may not be permitted under certain accounting standards.

6. Best Option for Your Business:

- The best cost flow method for your business depends on your specific circumstances and objectives.

- Smaller businesses with relatively stable inventory costs may find the Average Cost Flow method more suitable due to its simplicity.

- Conversely, larger businesses with fluctuating inventory costs and a need to manage tax implications may prefer LIFO or other methods.

Understanding the Average Cost Flow method is crucial for businesses looking to make informed decisions regarding their inventory management and financial reporting. While it offers simplicity and smooths out cost fluctuations, it may not always provide the most accurate representation of inventory costs. Choosing the best method, whether it's Average Cost Flow, LIFO, or another, should be based on a careful assessment of your business's unique needs and goals.

Understanding Average Cost Flow Method - Average Cost Flow vs: LIFO: Choosing the Right Method for Your Business

9. Understanding the Average Cost Method

Understanding the Average Cost Method

When it comes to inventory valuation, businesses have several methods at their disposal. One such method is the average cost method, which calculates the cost of inventory by taking the average of the costs of all units in stock. This approach provides a balanced view of inventory value that can be advantageous in certain situations. In this section, we will delve into the intricacies of the average cost method, exploring its benefits, drawbacks, and how it compares to other valuation methods.

1. Simplicity and Ease of Calculation:

One of the key advantages of the average cost method is its simplicity. calculating the average cost of inventory is relatively straightforward, as it involves taking the total cost of all units and dividing it by the total number of units. This ease of calculation can save time and effort, especially for businesses with a large number of inventory items. Additionally, the simplicity of the average cost method makes it accessible to small businesses with limited resources or accounting expertise.

2. Smoothing Out Price Fluctuations:

Another benefit of the average cost method is its ability to smooth out price fluctuations. By taking the average cost of all units, this method can help mitigate the impact of sudden price changes on inventory valuation. For example, if a business purchases units at varying prices over time, the average cost method will provide a more stable and consistent valuation compared to other methods that rely on specific purchase prices.

3. Reflecting Market Conditions:

The average cost method also has the advantage of reflecting market conditions more accurately. As the average cost is derived from the actual cost of inventory units, it takes into account the prevailing market prices at the time of purchase. This can be particularly beneficial in industries where prices are volatile or subject to frequent changes. By using the average cost method, businesses can ensure that their inventory valuation aligns with the current market value of their goods.

4. Comparison with Other Valuation Methods:

While the average cost method offers simplicity and stability, it is important to compare it with other valuation methods to determine the best option for a particular business. Two common alternatives to the average cost method are the first-in, first-out (FIFO) and last-in, first-out (LIFO) methods.

- FIFO: The FIFO method assumes that the first units purchased are the first to be sold. This method can be advantageous during periods of rising prices, as it assigns the lowest cost to units sold, resulting in higher reported profits. However, it may not accurately reflect the current market value of inventory.

- LIFO: In contrast to FIFO, the LIFO method assumes that the last units purchased are the first to be sold. This method can be beneficial during periods of inflation, as it assigns the highest cost to units sold, reducing taxable income. However, it may not provide an accurate representation of the actual cost of inventory.

When comparing the average cost method with FIFO and LIFO, it becomes clear that each method has its own strengths and weaknesses. The best option for a business depends on various factors such as industry dynamics, pricing trends, and tax implications.

The average cost method is a valuable tool for inventory valuation, offering simplicity, stability, and a reflection of market conditions. By understanding the different valuation methods available and considering their pros and cons, businesses can make informed decisions about which method best suits their needs. Ultimately, selecting the most appropriate valuation method is crucial for accurate financial reporting and effective inventory management.

Understanding the Average Cost Method - Average cost method: A Closer Look at Inventory Valuation

10. Understanding Average Inventory and Inventory Turnover

Inventory is one of the most sensitive aspects of any business. In fact, it is the backbone of many industries. However, not all businesses know how to manage their inventory. As a result, they might end up with piles of unsold items that eat up their resources and reduce their profitability. To avoid this scenario, it is important to understand the concept of average inventory and inventory turnover. These two concepts work hand in hand to help businesses optimize their profitability through efficient inventory management.

Here are some insights on average inventory and inventory turnover:

1. Average inventory refers to the average value of the inventory over a specific period. This period could be a month, a quarter, or a year. To calculate the average inventory, you need to add the beginning inventory value and the ending inventory value, then divide the result by two. This provides a more accurate representation of the inventory value compared to only looking at the beginning or ending inventory.

2. Inventory turnover, on the other hand, measures the number of times the inventory is sold and replaced during a specific period. It is calculated by dividing the cost of goods sold by the average inventory. A high inventory turnover means that a business is selling its inventory quickly, which is a good sign. However, a low inventory turnover could indicate that a business is holding too much inventory or is not selling its products as quickly as it should.

3. By understanding average inventory and inventory turnover, businesses can make informed decisions about their inventory management. For example, a business with a high inventory turnover might want to reduce its inventory levels to avoid overstocking and tying up its resources. On the other hand, a business with a low inventory turnover might want to focus on increasing its sales or improving its marketing efforts to sell its products faster.

4. Efficient inventory management can also help businesses save costs. For example, by reducing the amount of inventory, a business can reduce its storage and handling costs. Additionally, by selling products faster, a business can reduce the risk of obsolescence and spoilage, which could result in significant losses.

Understanding average inventory and inventory turnover is crucial for businesses that want to optimize their profitability through efficient inventory management. By calculating and analyzing these metrics, businesses can make informed decisions about their inventory levels, sales strategies, and cost-saving measures.

Understanding Average Inventory and Inventory Turnover - Average inventory: Optimizing Profitability through Inventory Turnover

11. Understanding Average Selling Prices

Understanding Average Selling Prices

When delving into the complex world of Average Selling Prices (ASPs), one quickly realizes that these figures serve as vital barometers of economic activity across various industries. ASPs are the financial heartbeat of businesses, offering valuable insights into the health of markets and the changing dynamics of supply and demand. In this section, we will unravel the layers of Average Selling Prices, exploring them from different perspectives to grasp their significance in the broader economic landscape.

1. Definition of Average Selling Prices: To begin our journey, it's crucial to establish what ASPs are. An average Selling price is the mean value at which a product or service is sold within a specific time frame. This is typically calculated by dividing the total revenue generated from sales by the quantity of items sold. For instance, if a tech company sold 1,000 smartphones for a total revenue of $500,000, the ASP for those smartphones would be $500.

2. Supply and Demand Dynamics: ASPs are intimately linked to the principles of supply and demand. When demand for a product exceeds its supply, ASPs tend to rise as consumers are willing to pay more. Conversely, when supply outstrips demand, ASPs tend to decline as businesses lower prices to entice buyers. Consider the case of a limited-edition collectible toy; its ASP could skyrocket as collectors compete to own a rare item.

3. Industry Variations: ASPs vary greatly across industries. For instance, in the real estate sector, ASPs reflect the cost of homes in a particular market, influenced by factors like location, size, and demand. In contrast, the technology industry experiences rapid price fluctuations due to constant innovations and competition. A smartphone's ASP may drop significantly from one year to the next as new models are introduced.

4. Market Positioning: Businesses strategically set their ASPs to position themselves within the market. A high ASP can signify a premium offering, targeting a more affluent customer base. On the other hand, a lower ASP can attract budget-conscious consumers. For example, luxury car manufacturers intentionally price their vehicles with high ASPs to maintain their exclusive status.

5. Economic Indicators: Economists and financial analysts closely monitor ASP trends as leading economic indicators. Rising ASPs can indicate inflationary pressures, while falling ASPs may suggest deflation. For instance, if the ASP of essential goods like food and fuel significantly rises, it can lead to cost-of-living concerns for consumers.

6. Global and Regional Variances: ASPs also exhibit regional and global variations. A product may have a higher ASP in one country due to import tariffs, taxes, or exchange rates. This creates price differences for consumers and challenges for international businesses striving for global consistency.

7. Technological Advances: Technological advances can significantly impact ASPs. Consider the case of smartphones, where new features and capabilities often drive prices higher. The introduction of 5G connectivity or improved camera technology can lead to higher ASPs, reflecting increased production costs.

8. Consumer Behavior: consumers' preferences and purchasing behavior can strongly influence ASPs. Brands offering sustainable or environmentally friendly products may command higher ASPs, catering to a growing market segment of eco-conscious consumers.

In summary, Average Selling Prices serve as powerful metrics, offering a window into the financial health and dynamics of various industries. They are shaped by factors like supply and demand, industry-specific considerations, market positioning, and the broader economic landscape. As we continue our exploration of ASP trends in this blog, we'll dive deeper into the intricacies of this vital economic indicator.

Understanding Average Selling Prices - Average Selling Price Trends: Exploring the Numbers

12. Understanding Average Velocity

Average velocity is a key concept for many fields, including physics, engineering, and mathematics. Understanding average velocity is essential for solving problems that involve motion, as it provides a way to describe how quickly an object moves over a period of time. From a physics perspective, velocity is a vector quantity that describes an object's speed and direction. Engineers use average velocity to design and analyze systems that involve moving parts, such as vehicles, robots, and machines. Mathematicians use average velocity to describe the rate of change of a function over a specific interval. In this section, we will explore the concept of average velocity in more detail, including its definition, units of measurement, and examples of how it is used in various fields.

Here are some key points to keep in mind as we dive deeper into the topic of average velocity:

1. Definition: Average velocity is defined as the displacement of an object over a specific time interval. Displacement is the change in position of an object, measured in a straight line from its starting point to its ending point. Average velocity is calculated by dividing the displacement by the time interval.

2. Units of measurement: The SI unit for displacement is meters (m), while the SI unit for time is seconds (s). Therefore, the SI unit for average velocity is meters per second (m/s). However, other units of measurement, such as miles per hour (mph) or kilometers per hour (km/h), are also commonly used in everyday life.

3. Positive and negative velocity: Velocity can be positive or negative, depending on the direction of the displacement. If an object moves in the positive direction (i.e., to the right or up), its velocity is positive. If an object moves in the negative direction (i.e., to the left or down), its velocity is negative.

4. Instantaneous velocity: Average velocity provides a way to describe an object's motion over a specific time interval, but it does not provide information about how the object moves during that interval. Instantaneous velocity, on the other hand, describes an object's velocity at a specific moment in time. It is calculated by taking the limit of the average velocity as the time interval approaches zero.

Overall, understanding average velocity is essential for analyzing motion and solving problems in physics, engineering, and mathematics. By knowing the definition, units of measurement, and examples of how it is used in various fields, we can gain a deeper understanding of this important concept.

Understanding Average Velocity - Average velocity: Exploring Average Velocity: Beyond the Basics

13. Understanding Average Life Analysis

As part of our discussion on bond yield and maximizing returns, we will delve into the concept of average life analysis. Understanding this concept is crucial for investors who want to make informed decisions on their investments. Average life analysis is a tool used to estimate the expected cash flow of a bond, taking into account the timing and amount of payments.

1. What is average life analysis?

Average life analysis is a calculation that estimates the average time a bond will be outstanding. It considers the timing and amount of all future cash flows, including interest and principal payments. The calculation is based on the assumption that the bond will be paid off earlier than its maturity date, either through early redemption or default. Average life analysis is used to assess the risk and return of a bond investment.

2. How is average life analysis calculated?

The calculation of average life analysis involves determining the present value of all future cash flows and dividing it by the present value of the bond. The resulting figure represents the average time that the bond will be outstanding. This calculation can be done manually or by using specialized software.

3. Why is average life analysis important?

Average life analysis helps investors to understand the expected cash flow of a bond investment. By estimating the average time that the bond will be outstanding, investors can assess the risk and return of the investment. This information is essential for making informed decisions about the allocation of investment funds.

4. What are the benefits of using average life analysis?

Using average life analysis can help investors to identify bonds with attractive risk and return profiles. By comparing the average life of different bonds, investors can determine which ones are likely to generate the highest returns over a given period. This information is particularly useful when investing in a portfolio of bonds.

5. What are the limitations of using average life analysis?

Average life analysis is based on assumptions about interest rates, default rates, and other factors that are subject to change. As a result, the estimated average life of a bond may not be accurate. Additionally, average life analysis does not take into account the impact of changes in interest rates on the value of the bond.

6. What are the alternative methods to average life analysis?

Alternative methods to average life analysis include duration analysis and convexity analysis. Duration analysis measures the sensitivity of a bond's price to changes in interest rates, while convexity analysis measures the curvature of the relationship between a bond's price and its yield. These methods provide additional information about the risk and return of a bond investment.

Average life analysis is an important tool for investors who want to maximize returns through bond investments. By understanding this concept and using it in conjunction with other analytical tools, investors can make informed decisions about their investments. However, it is important to remember that average life analysis is just one of many factors to consider when evaluating a bond investment.

Understanding Average Life Analysis - Bond yield: Maximizing Returns through Average Life Analysis

14. Understanding Average Total Cost Drivers

Understanding the drivers behind average total costs is crucial for businesses to effectively manage their expenses and make informed decisions. average total cost (ATC) is the total cost per unit of output produced, and it encompasses both fixed and variable costs. By identifying and analyzing the key drivers that impact ATC, companies can optimize their operations and improve their profitability. In this section, we will explore some of the important factors that contribute to average total cost and provide examples, tips, and case studies to illustrate their significance.

2. Economies of Scale

One of the primary drivers of average total cost is economies of scale. As a company increases its production and expands its operations, it often experiences lower average costs per unit. This is because fixed costs, such as rent and equipment, are spread over a larger output. For example, a manufacturing company that produces 1,000 units of a product may have higher fixed costs per unit compared to a company that produces 10,000 units. The latter benefits from economies of scale, resulting in lower average total costs.

Tip: To leverage economies of scale, businesses should carefully plan their production levels and aim to maximize their output without compromising quality. By increasing production volume, companies can reduce their average total costs and gain a competitive advantage in the market.

Case Study: Walmart is a prime example of a company that has successfully utilized economies of scale to lower its average total costs. Through its massive purchasing power and efficient supply chain management, Walmart has been able to negotiate lower prices from suppliers and maintain a lean cost structure. This has allowed the retail giant to offer competitive prices to customers while still generating substantial profits.

3. Input Costs

Another significant driver of average total cost is input costs, including raw materials, labor, energy, and other resources required for production. Fluctuations in input costs can directly impact a company's ATC. For instance, if the price of raw materials increases, it will raise the average total cost per unit. Conversely, if input costs decrease, the ATC will decrease as well.

Tip: To mitigate the impact of volatile input costs, businesses can explore alternative suppliers, negotiate favorable contracts, or invest in technologies that improve efficiency and reduce resource consumption. Additionally, diversifying the supplier base can help minimize the risk of supply chain disruptions and price fluctuations.

Case Study: The airline industry is highly sensitive to fluctuations in fuel prices, which significantly affect their average total costs. When oil prices surge, airlines face higher fuel costs, leading to an increase in their ATC. To manage this cost driver, airlines often hedge fuel prices by entering into futures contracts or adopting fuel-efficient aircraft to reduce consumption.

4. Technological Advancements

Technological advancements can greatly influence average total costs by increasing efficiency and reducing labor or material requirements. By adopting innovative technologies, businesses can automate processes, streamline operations, and lower their ATC. For example, implementing robotic automation in a manufacturing plant can reduce labor costs and improve productivity, resulting in a lower average total cost per unit.

Tip: It is essential for companies to stay updated with the latest technological advancements in their industry. By regularly assessing their operations and identifying areas where technology can be integrated, businesses can optimize their processes, reduce costs, and enhance their competitiveness.

Case Study: Amazon's extensive use of automation and robotics in its fulfillment centers has significantly contributed to the company's ability to offer competitive prices and fast delivery to its customers. By leveraging advanced technologies, Amazon has achieved higher efficiency, decreased labor costs, and ultimately lowered its average total costs.

Understanding the drivers of average total costs is vital for businesses to make informed decisions and optimize their operations. By considering factors such as economies of scale, input costs, and technological advancements, companies can identify opportunities to reduce costs, improve efficiency, and enhance their overall profitability.

Understanding Average Total Cost Drivers - Cost drivers: Identifying Average Total Cost Drivers: Key Factors to Consider

15. Understanding Average Total Cost

When it comes to cost optimization, understanding the concept of average total cost is crucial. Average total cost (ATC) is a measure that helps businesses determine the average cost per unit produced. By analyzing and minimizing ATC, companies can identify strategies to reduce expenses and maximize profitability. In this section, we will delve deeper into the concept of ATC and explore how it can be effectively managed.

1. Calculating Average Total Cost:

To calculate ATC, you need to consider both fixed and variable costs. Fixed costs are expenses that do not change with the level of production, such as rent or equipment maintenance. Variable costs, on the other hand, fluctuate based on the quantity of units produced, like raw materials or labor costs. To determine ATC, divide the total cost (fixed cost + variable cost) by the number of units produced. For example, if a company produces 100 units with a total cost of $10,000, the ATC would be $100.

Understanding the factors that drive costs is essential for cost optimization. By identifying the key cost drivers, businesses can focus their efforts on reducing expenses in those areas. For instance, if a manufacturing company realizes that the cost of raw materials is a significant driver of their ATC, they can explore options such as finding alternative suppliers or negotiating better deals to lower their average costs.

3. Economies of Scale:

Economies of scale play a vital role in cost optimization. This concept refers to the cost advantages gained when production increases. As a company produces more units, the fixed costs are spread over a larger output, resulting in lower ATC. For example, a printing company can achieve economies of scale by increasing their printing volume, which allows them to reduce their average costs per printed page.

4. Case Study - Amazon:

Amazon is a prime example of a company that effectively manages its average total cost. By leveraging economies of scale, Amazon has been able to reduce its ATC significantly. The company's massive fulfillment centers and efficient supply chain management allow them to handle a high volume of orders at a lower cost per unit. This cost optimization strategy has contributed to Amazon's success in offering competitive prices to customers while maintaining profitability.

5. Tips for Cost Optimization:

- Continuously analyze your cost structure to identify potential areas for improvement.

- Explore outsourcing opportunities to reduce labor costs.

- Negotiate with suppliers to obtain better pricing or terms.

- Embrace technology and automation to streamline operations and reduce manual labor costs.

- Invest in employee training and development to enhance productivity and efficiency.

Understanding and managing average total cost is essential for cost optimization. By calculating ATC, identifying cost drivers, leveraging economies of scale, and implementing effective strategies, businesses can reduce expenses and improve their bottom line. Stay tuned for the next section, where we will explore more strategies for cost optimization.

Understanding Average Total Cost - Cost minimization: Minimizing Average Total Cost: Strategies for Cost Optimization

16. Understanding Average Ticket Size and Its Importance

Understanding average Ticket size (ATS) is crucial to any business owner who wants to maximize their profits. ATS is the average amount of money a customer spends in a single transaction. It's a metric that helps businesses determine their sales trends, identify their top-selling products, and measure the effectiveness of their marketing campaigns. By understanding ATS, businesses can improve their sales strategies and increase their profits.

From the customer’s perspective, ATS is the amount of money they spend per visit, which can be influenced by various factors such as product pricing, quality, and availability. A customer may also be more inclined to spend more money if they receive exceptional customer service or if they are offered an irresistible deal.

Here are some in-depth insights on why ATS is important:

1. Identifying Top-Selling Products: By analyzing ATS, businesses can identify their top-selling products and focus on promoting them. This can help generate more sales and increase the overall ATS.

2. Improving Marketing Strategies: Analyzing ATS can help businesses determine the effectiveness of their marketing campaigns. If the ATS increases after a particular campaign, it indicates that the campaign was successful in driving sales.

3. Creating Targeted Promotions: Businesses can create targeted promotions based on ATS data to encourage customers to spend more money. For example, offering a discount for customers who spend a certain amount of money can motivate them to spend more.

4. Increasing Profits: By increasing the ATS, businesses can increase their profits without necessarily acquiring new customers. For example, if a business has an ATS of $50 and they manage to increase it to $60, they have effectively increased their revenue by 20%.

Understanding ATS is essential for businesses that want to maximize their profits. By analyzing ATS data, businesses can identify their top-selling products, improve their marketing strategies, create targeted promotions, and increase their profits.

Understanding Average Ticket Size and Its Importance - Customer spending: Unleashing the Power of Average Ticket Size

17. Understanding Average Inventory Levels

Average inventory levels are a crucial aspect of inventory management, and understanding them is essential for any business that wants to optimize its operations and profitability. The average inventory level is the average value of inventory over a specific period, typically a month, quarter, or year. It is calculated by adding the beginning inventory value to the ending inventory value and dividing the result by two.

1. Importance of Average Inventory Levels

Average inventory levels are essential for several reasons. First, they help businesses determine the amount of inventory they need to keep on hand to meet customer demand. Second, they help businesses manage their cash flow by ensuring that they have enough inventory to meet demand while minimizing the amount of cash tied up in inventory. Finally, average inventory levels can help businesses identify trends and patterns in their inventory management, allowing them to make more informed decisions about future inventory purchases.

2. Factors Affecting Average Inventory Levels

Several factors can affect average inventory levels, including seasonality, lead times, and demand variability. Seasonality refers to the fact that some products sell better at certain times of the year than others. Lead times refer to the time it takes to receive inventory after placing an order. Demand variability refers to the fact that customer demand for a product can fluctuate over time.

3. Calculating Days' Inventory on Hand

Days' Inventory on Hand (DIH) is a metric used to measure the number of days it takes a business to sell its entire inventory. It is calculated by dividing the average inventory value by the cost of goods sold (COGS) per day. DIH is an essential metric for businesses because it helps them determine how quickly they are selling inventory and how much inventory they need to keep on hand to meet customer demand.

4. Best Practices for Managing Average Inventory Levels

To manage average inventory levels effectively, businesses should consider several best practices. First, they should have a clear understanding of their customer demand and their lead times to ensure that they have enough inventory on hand to meet customer demand. Second, they should track their inventory levels regularly to identify any trends or patterns that may require adjustments in their inventory management. Finally, they should consider implementing inventory management software that can help them track their inventory levels and optimize their inventory management processes.

Understanding average inventory levels is critical for any business that wants to optimize its operations and profitability. By considering the factors that affect average inventory levels, calculating days' inventory on hand, and implementing best practices for managing inventory, businesses can ensure that they have enough inventory on hand to meet customer demand while minimizing the amount of cash tied up in inventory.

Understanding Average Inventory Levels - Days: Inventory on Hand: How it Affects Average Inventory Levels

18. Understanding Average Daily Trading Volume

Understanding Average Daily Trading Volume

When it comes to analyzing the movement of share prices, one crucial metric that traders and investors often rely on is the average daily trading volume. This metric provides valuable insights into the level of activity and liquidity in a particular stock or market. By understanding average daily trading volume, market participants can make more informed decisions and gain a better understanding of the dynamics driving price movements.

1. What is Average Daily Trading Volume?

Average daily trading volume refers to the average number of shares traded in a stock or market over a specified period, typically measured in days or weeks. It represents the total volume of shares bought and sold during a trading day, divided by the number of trading days in the period. This metric is a key indicator of the level of interest and participation in a particular stock or market and can help identify trends or anomalies.

2. Importance of Average Daily Trading Volume

A. Liquidity: High average daily trading volume indicates the presence of liquidity in a stock or market. Stocks with high liquidity are generally easier to buy or sell without significantly impacting the share price. Conversely, low average daily trading volume may result in wider bid-ask spreads and increased price volatility.

B. Price Discovery: Average daily trading volume plays a crucial role in price discovery. Higher volume suggests that more market participants are actively buying and selling, leading to a more accurate reflection of a stock's true value. It helps in identifying trends, support and resistance levels, and potential price reversals.

C. Trading Strategies: Understanding average daily trading volume is essential for traders employing various strategies. For example, day traders may prefer stocks with high volume to ensure quick execution of trades, while long-term investors may focus on stocks with consistent volume to ensure liquidity when exiting positions.

3. Factors Influencing Average Daily Trading Volume

A. News and Events: Significant news, earnings releases, or corporate events can lead to a surge in trading volume as market participants react to new information. For example, an unexpected positive earnings report may attract more buyers, resulting in higher average daily trading volume.

B. Market Sentiment: Bullish or bearish market sentiment can impact trading volume. During periods of optimism, more investors may be willing to enter the market, leading to increased volume. Conversely, during pessimistic times, trading volume may decrease as investors become more cautious.

C. Stock Specific Factors: Factors such as company size, industry, and market capitalization can influence average daily trading volume. large-cap stocks tend to have higher volume due to their wider investor base, while stocks in niche sectors may have lower volume.

4. Comparing Average Daily Trading Volume to Historical Data

To gain a better understanding of a stock's average daily trading volume, it is essential to compare it to historical data. By analyzing trends and patterns, traders can identify deviations from the norm and potential opportunities. For example, if a stock's average daily trading volume is significantly higher than its historical average, it may indicate increased market interest or upcoming news.

5. Best Practices for utilizing Average daily Trading Volume

A. Look for Confirmation: When analyzing price movements, it is crucial to confirm any significant changes with corresponding shifts in average daily trading volume. If a stock experiences a sudden price increase but without a corresponding spike in volume, it may indicate a lack of conviction or potential price reversal.

B. Comparative Analysis: Comparing the average daily trading volume of a stock to its industry peers or benchmark index can provide valuable insights. If a stock consistently exhibits higher or lower volume compared to its peers, it may suggest unique factors driving investor interest or apathy.

C. Multiple Timeframes: analyzing average daily trading volume across different timeframes can reveal additional insights. For example, comparing volume on a daily basis to that on a weekly or monthly basis can help identify short-term fluctuations versus long-term trends.

Understanding average daily trading volume is crucial for anyone involved in the stock market. By considering this metric alongside other fundamental and technical indicators, traders and investors can make more informed decisions and gain a deeper understanding of share price movements.

Understanding Average Daily Trading Volume - Decoding Share Price Movement using Average Daily Trading Volume

19. Understanding the Average Selling Price

Understanding the Average Selling Price

When diving into the world of buying and selling, the term "Average Selling Price" (ASP) often emerges as a pivotal metric. ASP is a crucial indicator that holds significance for both buyers and sellers in various industries. It's not merely a number; it represents a complex web of factors that can reveal much about the dynamics of a market. In this section, we'll dissect the concept of Average Selling Price, exploring what it entails and why it matters to different stakeholders. Let's delve into the world of ASP and see why it's more than just numbers on a spreadsheet.

1. Definition of Average Selling Price

To grasp the importance of ASP, one must first understand what it means. ASP is the average price at which a product or service is sold within a given time frame. This metric is particularly useful for businesses to gauge their pricing strategies. It reflects the balance between affordability and profitability. For buyers, knowing the ASP can provide insights into market trends and potential savings.

2. Seller's Perspective

From a seller's viewpoint, ASP is a vital performance indicator. It helps businesses assess the effectiveness of their pricing strategies. If the ASP is increasing, it could signify an opportunity to raise prices, potentially increasing revenue. Conversely, a declining ASP might indicate the need to reevaluate pricing or sales tactics. For example, a luxury fashion brand might see a rising ASP as a sign that their high-end products are in demand, allowing them to maintain or even increase their prices.

3. Buyer's Perspective

For buyers, understanding the ASP can be a strategic advantage. It aids in making informed purchasing decisions. If the ASP is higher than one's budget, it might be wise to look for alternatives or wait for discounts. Conversely, a lower ASP can indicate a buyer's market, where consumers have the upper hand. For instance, a savvy car buyer might wait for the end of the year when dealers often lower ASP to clear out old inventory.

4. Market Trends

ASP also plays a crucial role in tracking market trends. A rising ASP may suggest increased demand or a shift towards premium products. In contrast, a falling ASP might indicate market saturation or the introduction of more affordable alternatives. For instance, the technology industry frequently experiences falling ASP for electronic devices as new models are introduced with enhanced features at similar or lower prices.

5. Competitive Analysis

Analyzing the ASP can help both buyers and sellers assess the competitive landscape. A higher ASP compared to competitors might suggest a more premium product, while a lower ASP could indicate a cost-effective alternative. Buyers can use this information to find the best value for their money, while sellers can fine-tune their pricing strategies to remain competitive.

6. Geographical Variances

It's essential to consider regional or geographical variations in ASP. Prices can significantly differ from one location to another, influenced by local economic conditions and consumer preferences. For instance, a coffee shop chain may charge a higher ASP in a bustling urban center compared to a small town.

ASP is more than just a number; it's a dynamic metric that reflects the ever-changing dynamics of supply and demand, competition, and consumer behavior. By understanding ASP from various perspectives, buyers and sellers can make more informed decisions, whether it's about a big-ticket purchase or pricing strategy adjustments. In the world of commerce, ASP is the compass that guides stakeholders towards making smarter choices.

Understanding the Average Selling Price - Decoding the Average Selling Price: What it Means for Buyers

20. Understanding the Average Cost Method

When it comes to inventory management, one crucial aspect that businesses need to pay attention to is the costing method they use. The choice of costing method can significantly impact a business's financial statements, which can ultimately affect decision-making processes. One of the most commonly used costing methods is the average cost method, which entails calculating the average cost of all inventory items in stock. This method can be quite beneficial, particularly for businesses that deal with products that have fluctuating costs.

Using the average cost method comes with several advantages. Here are some of the benefits of using this costing method:

1. Simplicity and ease of use - The average cost method is relatively simple and easy to use, even for small business owners who may not have an accounting background. All you need to do is divide the total cost of inventory by the total number of items in stock to determine the average cost per item.

2. Accuracy - The average cost method provides an accurate representation of the cost of goods sold. It eliminates the need to track each item's cost individually, making it a suitable method for businesses that deal with large volumes of inventory.

3. Smoothing of inventory costs - The average cost method can help to smooth out inventory costs, particularly for businesses that deal with products whose prices fluctuate significantly. For example, if a business purchases a product at a high cost and then again at a lower cost, the average cost method will provide a more accurate cost representation than other costing methods.

4. reducing taxes - The average cost method can help businesses reduce their tax bills. By using the average cost of inventory, businesses can avoid overstating profits and reduce the amount of tax they need to pay.

The average cost method is a simple and effective costing method that can help businesses better manage their inventory costs. By using this method, businesses can improve their financial statements' accuracy, reduce tax bills, and make sound business decisions.

Understanding the Average Cost Method - Driving Efficiency: Improving Operations with the Average Cost Method

21. Understanding Average Total Cost

To fully comprehend the concept of economies of scale, it is essential to delve into the concept of average total cost (ATC). Average total cost refers to the average cost incurred per unit of output produced. It is calculated by dividing the total cost by the total quantity of output. Understanding ATC is crucial as it provides insights into the efficiency and profitability of a business.

1. The relationship between average total cost and economies of scale:

The ATC is inversely related to economies of scale. As the scale of production increases, the average total cost decreases, leading to cost savings and increased profitability. This inverse relationship occurs due to the spreading of fixed costs across a larger volume of output. For example, a manufacturing company that produces 1,000 units of a product may have an average total cost of $10 per unit. However, if the production volume doubles to 2,000 units, the average total cost might decrease to $8 per unit due to the economies of scale.

2. Identifying the components of average total cost:

To fully understand the ATC, it is crucial to identify its components. The ATC consists of both variable costs and fixed costs. Variable costs are expenses that change with the level of output, such as raw materials, labor, and energy costs. Fixed costs, on the other hand, remain constant regardless of the level of production, including rent, equipment depreciation, and administrative expenses. By analyzing these components, businesses can identify areas where cost reductions can be made to achieve economies of scale.

3. Tips for leveraging average total cost:

- Streamline operations: Identify areas where inefficiencies exist within the production process. By optimizing operations, businesses can reduce costs and improve the average total cost.

- Negotiate with suppliers: Building strong relationships with suppliers can lead to cost savings through bulk purchasing or favorable pricing agreements. This can further contribute to reducing the average total cost.

- Invest in technology: Embracing technology can enhance productivity and efficiency, leading to cost reductions. Automation, for instance, can minimize labor costs and improve overall operational effectiveness.

4. Case study: Walmart's successful utilization of economies of scale:

Walmart, the multinational retail corporation, is a prime example of a company that leverages economies of scale to its advantage. By purchasing goods in large quantities, Walmart benefits from significant cost savings, which are then passed on to consumers through lower prices. The company's extensive distribution network and efficient inventory management systems further contribute to its ability to achieve economies of scale and maintain a low average total cost.

In conclusion, understanding average total cost is crucial for businesses seeking to unleash economies of scale. By analyzing the relationship between ATC and scale of production, identifying its components, and implementing strategies to leverage it effectively, businesses can achieve cost savings and enhance their competitiveness in the market.

Understanding Average Total Cost - Economies of scale: Leveraging Average Total Cost: Unleashing Economies of Scale

22. Understanding Average Cost Basis Method

1. understanding the Average Cost basis Method

When it comes to effective asset management, one of the key considerations is determining the cost basis of your investments. The average cost basis method is a widely used approach that can help you accurately track your investment costs over time. By understanding how this method works and its advantages, you can make informed decisions about your portfolio. Let's delve into the intricacies of the average cost basis method and explore its various aspects.

2. What is the Average Cost Basis Method?

The average cost basis method is a technique used to calculate the cost basis of an investment by taking the average price of all shares purchased. This method is particularly useful in situations where you acquire shares of the same investment at different prices over time. By averaging the costs, you can determine the average price per share and calculate your gains or losses more accurately.

3. How Does the Average Cost Basis Method Work?

To illustrate the working of the average cost basis method, let's consider an example. Suppose you purchase 100 shares of XYZ stock at $10 per share in January, and then buy an additional 50 shares at $12 per share in March. With the average cost basis method, you would calculate the average price per share by adding the total cost of all shares and dividing it by the total number of shares. In this case, the average price per share would be ($1000 + $600) ÷ (100 + 50) = $9.41.

4. Advantages of the Average Cost Basis Method

The average cost basis method offers several advantages that make it an attractive option for asset management. Here are some key benefits:

- Simplicity: The average cost basis method is straightforward and easy to implement. It eliminates the need to track individual purchase prices and simplifies the calculation of gains or losses.

- Cost Averaging: By averaging the costs over time, this method smooths out the impact of market fluctuations. It allows you to mitigate the risk of buying at a high price and potentially increase your returns.

- Tax Efficiency: The average cost basis method can be tax-efficient, especially in taxable investment accounts. It can help minimize your tax liability by accurately determining your gains or losses when selling investments.

5. comparing the Average Cost basis Method with Other Options

While the average cost basis method is popular, it's essential to be aware of alternative cost basis methods and compare them to make an informed decision. Two commonly used alternatives are the first-in, first-out (FIFO) method and the specific identification method.

- FIFO Method: The FIFO method assumes that the first shares purchased are the first ones sold. This method can be advantageous when you want to realize long-term capital gains or when you are selling shares with a higher cost basis first. However, it may not be ideal if you want to minimize short-term capital gains or have specific tax considerations.

- Specific Identification Method: The specific identification method allows you to choose which shares to sell, which can be beneficial if you want to strategically manage your tax liability. However, this method requires meticulous record-keeping and may not be practical for every investor.

6. The Best Option: Average Cost Basis Method

Considering its simplicity, cost averaging benefits, and tax efficiency, the average cost basis method is often the best option for many investors. It strikes a balance between ease of use and accuracy, making it suitable for both individual investors and financial institutions. However, it's important to consult with a financial advisor or tax professional to determine the most appropriate cost basis method for your specific circumstances.

Understanding the average cost basis method is crucial for effective asset management. By grasping the concept, calculating average prices, and comparing it to alternative methods, you can make informed decisions about your investment portfolio. The average cost basis method offers simplicity, cost averaging benefits, and tax efficiency, making it an attractive option for managing your assets.

Understanding Average Cost Basis Method - Effective Asset Management with Average Cost Basis Method

23. Understanding Average Cost and its Significance

1. Definition and Calculation of Average Cost:

Average cost is a crucial financial metric that helps businesses determine the average expense incurred in producing a unit of a product or service. It is calculated by dividing the total costs (both fixed and variable) by the total quantity produced. For example, if a company produces 1,000 units and incurs total costs of $10,000, the average cost per unit would be $10 ($10,000/1,000 units).

2. Significance of Average Cost: