Asia Pac J Manag (2012) 29:303–329

DOI 10.1007/s10490-011-9281-5

Ownership structure, family leadership,

and performance of affiliate firms in large family

business groups

Hsi-Mei Chung & Shu-Ting Chan

Published online: 4 February 2012

# Springer Science+Business Media, LLC 2012

Abstract Utilizing the agency viewpoint, this research attempts to shed light on

the issue of family leadership by examining ethnic Chinese family business

groups in Taiwan. The study examines the performance implications of this

kind of leadership under the ownership structure concern. The research results

indicate that the ownership structure of the affiliate firm influences the likelihood that family leadership will be used. Specifically, if the founding family

owns more direct ownership of the affiliate firm, the family will be likely to

appoint a family leader at the affiliate firm. However, when the founding family

has a greater degree of pyramidal ownership of an affiliate firm, family

leadership will be less likely at that affiliate firm. Additionally, family leadership mediates the relationship between ownership structure and affiliate firm

performance in a family business group. Family leadership positively affects the

effect of direct family ownership on affiliate firm performance but does not

significantly affect the negative relationship between pyramidal ownership and

affiliate firm performance. The implications of these findings for future research

on leadership in family business groups are discussed.

Keywords Agency theory . Family business groups . Family leadership .

Family ownership structure

The current authors greatly appreciate the comments from the Special Issue Editors and the discussants at

the Special Issue Conference, and also sincerely appreciate the sponsorship provided to this study by “Aim

for the Top University Plan” of the National Sun Yat-sen University and Ministry of Education, Taiwan,

R.O.C., and National Science Council, Executive Yuan, Taiwan, R.O.C. (grant no. NSC 99-2410-H-214007-MY2, 2010/08–2012/07).

H.-M. Chung (*)

Department of Business Administration, I-Shou University, Kaohsiung 840, Taiwan

e-mail: smchung@isu.edu.tw

S.-T. Chan

Department of Business Management, National Sun Yat-sen University, Kaohsiung 804, Taiwan

e-mail: shuting0607@gmail.com

�304

H.-M. Chung, S.-T. Chan

Outside of Japan, almost all large publicly traded firms in Asia are family businesses

(Claessens, Djankov, & Lang, 2000; La Porta, Lopez-de-Silanes, & Shleifer, 1999; La

Porta, Lopez-de-Silanes, Shleifer, & Vishny, 2002; Young, Peng, Ahlstrom, Bruton,

& Jiang, 2008). In North America and Europe, families enjoy a large degree of

ownership of some publicly traded firms, but the control mechanisms on which such

firms rely are substantively different than in Asia. For example, in publicly traded

family firms in North America and Europe, the presence of independent directors on a

board of directors partially mitigates the influence of the founding family, ensuring

that the firm is managed in a way that is in the best interests of all shareholders

(Anderson & Reeb, 2003; Miller & Le Breton-Miller, 2005). In contrast, in Asia, a

large firm that is publicly traded will have a board of directors made up of family

members and close friends (Claessens et al., 2000; La Porta et al., 1999, 2002; Peng

& Jiang, 2010). Similarly, whereas publicly traded family businesses in North

America and Europe rely on senior management teams not dominated by family

members, one of the central control and coordination strategies that family businesses

in Asia employ is the positioning of family members in key leadership positions

(Claessens et al., 2000; Luo & Chung, 2005; Morck, Wolfenzon, & Yeung, 2005).

Despite these clear differences between family businesses in Asia and North American

or Europe, there has been little effort made to understand how families ensure coordination and control in affiliate firms in the Asian context. Again, one coordination and

control mechanism that has been identified is the designation of family members as the

heads of business units. However, the number of family members who might be

available to fill such leadership positions is finite. As a result, families must choose

where to position family members with the aim of maximizing their impact on the

affiliate firm. This issue is particularly difficult for large family business groups with

control of multiple, diverse affiliate firms (Almeida & Wolfenzon, 2006; Luo & Chung,

2005; Morck, 1996; Young et al., 2008). Therefore, to better understand the performance implications of choices regarding coordination and control in family business

groups, we examine the placement of family members as leaders of affiliate firms in

large groups of this type in the Chinese context.

This research will employ agency theory and utilize multi-level, longitudinal data to

examine this important topic. The key question addressed in this paper is the performance implications of family leadership in affiliate firms under the ownership structure

consideration in large family business groups. The founding family in a large family

business group usually utilizes the direct and pyramidal ownership structures at the

same time. Previous studies have examined the performance implications of ownership structure for family business groups with public affiliate firms (Chang, 2003;

Claessens et al., 2000). However, the relationships between different ownership

structures, family leadership, and performance in affiliate firms have not been

sufficiently analyzed (Carney, Gedajlovic, Heugens, van Essen, & van Oosterhout,

2011). Agency theory is widely employed to examine issues related to coordination

and control because it can be theoretically expected that as investment increases,

issues of coordination and control will be more closely addressed because of information asymmetry and risk (Eisenhardt, 1989; Jensen & Meckling, 1976). However,

researchers have tended to use agency theory in the same manner for different

institutional contexts (Eisenhardt, 1989; Fama & Jensen, 1983; Jensen & Meckling,

1976; Sanders & Hambrick, 2007). At the same time, scholars have increasingly

�Ownership structure, family leadership, and performance…

305

recognized that this sort of universal approach to agency theory is not appropriate

(Granovetter, 1985). Rather, as some have suggested, direct or pyramidal family

ownership structures are associated with different risk considerations, and thus, the

form of ownership used may encourage different coordination and control decisions

by affiliate firms in family business groups (Almeida & Wolfenzon, 2006; Chang,

2003; Kim & Sung, 2009). Previous studies have usually assumed that ownership and

management manifest in the same way in affiliate firms in family business groups

(Hamilton, 1997; Luo & Chung, 2005). However, the strategic importance and the

risk that each affiliate firm poses for family members are not equally distributed, and

as a result, the level of control that a family business group has over its affiliate firms

may vary (e.g., Carney et al., 2011; Kim & Sung, 2009). Therefore, this research aims

to investigate the possible relationships between family ownership structures, family

leadership decisions, and the performance of affiliate firms in large family business

groups.

This research will make several contributions to the academic literature. First,

although researchers have recognized that family businesses are likely to utilize

family ownership and family leadership as key control mechanisms (i.e., Cruz,

Gómez-Mejía, & Becerra, 2010; Luo & Chung, 2005; Peng & Jiang, 2010; Villalonga

& Amit, 2006), there has been little prior research conducted on the diversity of

ownership and management configurations used in family business groups. This

study will fill that gap. Second, we will use agency theory to expand knowledge of

family business groups and the coordination and control mechanisms that they use

with affiliate firms. Business groups are the dominant form of business organization

outside North America, but they remain poorly understood (Chang, 2006; Yiu, Lu,

Bruton, & Hoskisson, 2007; Young et al., 2008). The examination of the issue of

affiliate control will have strategic implications for business group management

around the world (Carney et al., 2011; Chang, 2003). Moreover, examining the

performance implications of family leadership and differential ownership structure will help to expand knowledge of ownership and management issues for

family business groups. Finally, the multi-level and longitudinal data used in

this research will provide insight into whether and how the founding family in

a large family business group makes leadership decisions spanning multiple

industries. To date, this longitudinal approach to leadership issues in family

business groups has been rare.

Hypothesis development

Leadership in Asian family business groups

The many complex institutional developments that have occurred in Asia offer

researchers an opportunity to expand their theories, originating fresh insights based

on context-specific considerations (Leung, 2007; Meyer, 2006). However, in addressing the issue of leadership in Asia, researchers have created fruitful theories and

models but have focused too much on simplistic comparisons between Asia and

Western societies (Tjosvold, Wong, & Hui, 2004; White, 2001). Typically, this crosscultural leadership research considers the role of cultural context in determining

�306

H.-M. Chung, S.-T. Chan

leadership effectiveness but provides insufficient evidence of whether and in what

ways leadership matters to specific businesses in the Asian context (Bruton & Lau,

2008; White, 2001). Moreover, previous studies indicate that at the micro-level of

analysis, leadership and trust issues for groups and teams are prominent topics in

Asian management research (Bruton & Lau, 2008; Meyer, 2006; Tjosvold et al.,

2004). Working with data from within different Asian countries, researchers usually

employ mainstream leadership theories and examine issues such as the Asian leadership style (Ismail & Ford, 2010), guanxi and trust (Chen, Chen, & Xin, 2004; Lau,

Liu, & Fu, 2007), leader-team member exchanges and the relationship between

leadership and performance (Wang, Law, Hackett, Wang, & Chen, 2005), and the

development of leadership in the Asian context (e.g., Leung, 2007; Meyer, 2006). In

addition to the prominent micro-level leadership research, an increasing amount of

research has addressed the leadership issues in Asia from a macro-level perspective—

for instance, by exploring the role of leadership in the business group or network

context (Bruton & Lau, 2008).

A business group is a collection of legally independent firms that are linked by

multiple ties, including ownership, economic connections (such as inter-firm transactions), and/or social relationships (family, kinship, friendship). Through these

connections, the firms in question coordinate to achieve mutual objectives (Granovetter,

1995; Khanna & Rivkin, 2001; Yiu et al., 2007). In Asia, family ownership is the

most prominent governance structure in business groups (La Porta et al., 1999; Morck

et al., 2005; Young et al., 2008). As with other kinds of family businesses, one

distinctive aspect of family business groups that results from their ownership structure is that their firms emphasize family leadership and trust among family members

in decision-making (Almeida & Wolfenzon, 2006; Luo & Chung, 2005). Thus,

assigning family members to appropriate leadership roles is a key strategic decision,

one that ensures that family business groups achieve their goals (Morck et al., 2005;

Peng & Jiang, 2010; Young et al., 2008). However, as family business groups become

larger and/or grow internationally, they may find that they no longer have sufficient

family members to serve as the leaders of their affiliate firms. Therefore, to achieve

the mutual objectives of the affiliate firms in a family business group, the controlling

family must consider whether and where to assign each family member as a leader

within the formal ownership structure so as to ensure that each affiliate’s strategic

direction is consistent with the goals of the family business group.

Compared to the research in Asian leadership at the micro-level of analysis, the

research on the antecedents and consequences of family leadership in family business

groups is scarcer. Family leadership is strategically necessary to achieve family

control and wealth (Arregle, Hitt, Sirmon, & Very, 2007; Cruz et al., 2010; GómezMejía, Haynes, Núñez-Nickel, Jacobson, & Moyano-Fuentes, 2007; Miller & Le

Breton-Miller, 2005). In addressing family leadership-outcomes issues, previous

research indicates that different types of family leadership may influence distinctive

outcomes (e.g., Dyer, 1986; Pellegrini & Scandura, 2008; Sorenson, 2000). For

example, based on family businesses in Western society, the participative leadership

compared with the autocratic and expert leadership is positively related to both family

and business financial outcomes as well as to employee satisfaction and commitment

(Sorenson, 2000). Additionally, in the Asia Pacific, paternalistic leadership style is

found to be one of the most remarkable dimensions in Chinese family business

�Ownership structure, family leadership, and performance…

307

leadership studies (Pellegrini & Scandura, 2008). Research indicates that the unidimensional construct of paternalistic leadership can be delineated into three dimensions, that is, benevolence, authoritarianism, and morality (Cheng, Chou, & Farh,

2000). Prior studies have examined how these different dimensions of paternalistic

leadership in Chinese family business affect subordinates’ organizational commitment, satisfaction with a team’s leader, and the commitment to the team (e.g., Cheng,

Huang, & Chou, 2002a; Cheng, Shieh, & Chou, 2002b; Farh, Cheng, Chou, & Chu,

2006).

However, as we argued before, previous research in addressing the family

leadership-macro outcomes issues has under-explored the role of family leadership

in the business group or network context (Bruton & Lau, 2008). Thus, although

Vallejo (2009) argued that leadership is more transformational in family businesses

than in non-family businesses, he also indicated that it still needs much effort to

further the current research work of leadership and its possible consequences in the

family business context. Therefore, this research will fill the gap in examining the

possible influence of family leadership on performance under various ownership

structures in family business groups. Agency theory provides a good perspective

from which to examine the issue above, especially in a family business group context

characterized by multiple links among affiliate firms. Thus, the following will

examine the relationships between ownership structure, family leadership decisions,

and performance implications in family business groups from the agency theory

viewpoint.

Ownership structure and family leadership

Family ownership is a key characteristic that distinguishes the structure of family

governance from that of more widely held and non-family firms (Anderson & Reeb,

2003; Villalonga & Amit, 2006). In addressing the strategic issues associated with

ownership structures in family businesses, previous studies have usually examined

the performance implications of such structures (e.g., Anderson & Reeb, 2003;

Miller, Le Breton-Miller, & Scholnick, 2008; Peng & Jiang, 2010). Evidence derived

by examining family businesses in developed economies indicates that family ownership will generate a greater level of motivation to manage firms, helps to monitor

managers, and thus has positive implications for performance (Anderson & Reeb,

2003; Demsetz & Lehn, 1985; Miller et al., 2008). However, we know that family

members usually exert control over businesses through both ownership structure and

family leadership. Thus, whether and how the ownership structure will influence

family leadership decisions is a key issue for family businesses (Peng & Jiang, 2010;

Villalonga & Amit, 2006). Furthermore, in those family business groups in emerging

economies, the founding family usually relies on a pyramidal ownership structure to

control its multiple affiliate firms (Almeida & Wolfenzon, 2006; Claessens et al.,

2000; La Porta et al., 1999, 2002; Morck et al., 2005; Young et al., 2008). Compared

with the evidence from the family businesses in developed economies indicating that

family ownership generates positive motivation, whether and how the utilization of

family direct ownership and pyramidal ownership in family business groups in

emerging economics will influence family leadership decisions has not been sufficiently explored. This research will fill that gap.

�308

H.-M. Chung, S.-T. Chan

The different ownership structures of family business groups, which include both

direct family ownership and the pyramidal ownership structure, may generate distinctive

effects on the strategy and power of family business groups (Claessens, Djankov, Fan, &

Lang, 2002; Kim & Sung, 2009; La Porta et al., 2002). From the agency theory

viewpoint, the founding family’s ownership structure entails distinctive risk and thus

may influence the coordination and control mechanisms used (Demsetz & Lehn,

1985; Fama & Jensen, 1983). The key concern in agency theory is contract design, as

contracts should minimize possible agency costs (Eisenhardt, 1989; Fama & Jensen,

1983; Jensen & Meckling, 1976). Given that agency relationship exists under the

attitudinal and information consideration, the principal should choose an incentive

contract or a monitoring mechanism to reduce agency cost (Eisenhardt, 1989; Fama

& Jensen, 1983; Jensen & Meckling, 1976; Sanders & Hambrick, 2007). Family

businesses—or more specifically, family business groups as a subset of family

businesses—rely on trust relationships to manage their business and overcome

possible transaction uncertainty and risk (Anderson & Reeb, 2003; Cruz et al.,

2010; Fama & Jensen, 1983). Family members focus primarily on running the

business to generate wealth for the family; thus, in contrast to non-family managers,

family members have a greater incentive to obey the instructions of the business

group leader and do not necessarily require close monitoring (Arregle et al., 2007;

Cruz et al., 2010; Gómez-Mejía et al., 2007).

Previous research indicates that when a founding family has majority shareholdings,

the family has a greater incentive to serve as good stewards in its businesses and is

motivated to monitor non-family managers. Thus, the agency problem should be less

acute in family businesses (Anderson & Reeb, 2003; Demsetz & Lehn, 1985; Fama &

Jensen, 1983). From an agency perspective, it appears that trust relationships among

family members will reduce the need to monitor a unit’s decisions closely because family

members will have a unique incentive to maximize the founding family’s wealth (Cruz et

al., 2010; Fama & Jensen, 1983). In other words, the combination of founding family

shareholdings and family leadership will lessen the agency problem for founding

family managers as opposed to non-family managers (Anderson & Reeb, 2003;

Demsetz & Lehn, 1985; Fama & Jensen, 1983). Following this logic, with reference

to family business groups, we argue from the agency theory viewpoint that direct

founding family ownership may increase the likelihood of family leadership in family

business groups and generate better performance (Claessens et al., 2002).

Compared with these arguments regarding motivation and direct family ownership, the strategic implications of the pyramidal ownership structure are controversial

(Almeida & Wolfenzon, 2006; Claessens et al., 2002; Kim & Sung, 2009). In this

type of pyramidal ownership structure, the founding family achieves control of the

constituent firms via a chain of ownership relationships: the family directly controls a

firm, which in turn controls another firm, which might itself control other firms

(Almeida & Wolfenzon, 2006: 1). The pyramidal ownership structure allows a

founding family to control a chain of affiliate firms based on a relatively small

investment (La Porta et al., 1999). By utilizing this ownership structure, family

members can leverage their financial risk by expanding their businesses; they can

exert control over multiple affiliate firms without providing larger financial inputs

(Chang, 2003; Kim & Sung, 2009; Morck et al., 2005). Thus, a founding family can

utilize the pyramidal ownership structure to meet its financial requirements if

�Ownership structure, family leadership, and performance…

309

external funds are more costly than internal funds. Furthermore, such an

ownership structure constitutes an optimal financial choice when family members

expect a higher return on costs associated with an affiliate firm (Almeida & Wolfenzon,

2006; Young et al., 2008).

The family business group must also confront increases in uncertainty and risk as it and

its firms grow in size and further diversify, creating coordination and control problems

(Claessens et al., 2002; Levy, 2009). This issue is a particularly difficult problem for

family business groups because there are limits to the number of family members who

can be called on to manage multiple affiliate firms (Morck, 1996; Morck et al., 2005).

If the founding family utilizes the pyramidal ownership structure, the investment risk

for the family business group will be less substantial than under direct ownership

(Morck, 1996). The use of this ownership structure will generate a weaker incentive

for founding families to assign family members to management positions because the

potential loss and risk under this structure are smaller for them (Almeida &

Wolfenzon, 2006; Levy, 2009). Thus, one could expect that the founding family in

a family business group would choose a non-family manager to head such an affiliate

firm because the potential loss of wealth and potential risk would be smaller.

In other words, from the agency theory viewpoint, the direct and pyramidal forms of

family ownership have differential strategic implications for coordination and control

mechanism such as leadership decisions made by family business groups (Claessens et al.,

2002; Kim & Sung, 2009; Levy, 2009). The following hypotheses are thus presented:

Hypothesis 1 The greater the degree of direct ownership of an affiliate firm by

members of a family business group, the higher the likelihood that this affiliate firm

will be headed by a family member.

Hypothesis 2 The greater the degree of pyramidal ownership of an affiliate firm by

members of a family business group, the lower likelihood that this affiliate firm will

be headed by a family member.

Ownership structure, family leadership, and affiliate firm performance

Family members usually play a strategic role in coordination and control in family

businesses (Anderson & Reeb, 2003; Arregle et al., 2007; Cruz et al., 2010; GómezMejía et al., 2007). Assigning family members to key decision-making positions can

ensure coherence and solidarity in family businesses and facilitate family goal

achievement (Arregle et al., 2007; Cruz et al., 2010; Gómez-Mejía et al., 2007).

From the agency theory viewpoint, family leadership can be helpful because it can

mitigate the possible conflict of interest between controlling shareholders and nonfamily professional managers in family businesses, thus improving performance

(Anderson & Reeb, 2003; Fama & Jensen, 1983). However, previous research has

also indicated that family leadership may cause entrenchment and issues with selfcontrol in family businesses and may thus be detrimental to performance (GómezMejía, Núñez-Nickel, & Gutierrez, 2001; Morck, 1996; Schulze, Lubatkin, Dino, &

Buchholtz, 2001). Indeed, prior research shows that family leadership can simultaneously generate both positive management motivation and issues with self-control

(Miller et al., 2008; Morck, 1996; Villalonga & Amit, 2006). Ownership structure is

�310

H.-M. Chung, S.-T. Chan

thus a key concern when researchers address the performance of family leadership in

family businesses (Claessens et al., 2002; Miller et al., 2008; Villalonga & Amit,

2006).

The relationship among ownership structure, family leadership, and performance

is a key issue in family business field (Miller et al., 2008; Peng & Jiang, 2010;

Villalonga & Amit, 2006). In the family business group context, it seems difficult to

tell a priori whether the benefits of family control—through family leadership or

pyramidal ownership structure—in large firms outweigh the costs, or vice versa

(Carney et al., 2011; Peng & Jiang, 2010). In this study, we propose that when a

founding family owns the majority share of a family business, it will hope to preserve

its social-emotional wealth while also helping the business to grow (Arregle et al.,

2007; Gómez-Mejía et al., 2001, 2007). Agency theory suggests the more shares

owned by the founding family, the higher resource commitment for the founding

family in this family business (Anderson & Reeb, 2003; Fama & Jensen, 1983).

Therefore, if the founding family has higher ownership, it will increase the founding

family’s risk of loss and thus the higher positive motivation in management (GómezMejía et al., 2001, 2007; Mishra & McConaughy, 1999). In explaining the relationship between family ownership and performance, previous studies indicate that the

more shares owned by family members the better performance in this family business

(Anderson & Reeb, 2003; Chu, 2011; Cruz et al., 2010). Others also argue that

founding family ownership will generate greater goal achievement and management

motivation, and accordingly better strategic decisions and performance implications

(Gómez-Mejía et al., 2001; Mishra & McConaughy, 1999; Villalonga & Amit, 2006).

Whereas it would seem that direct family ownership creates greater motivation for

founding families with regard to management, a pyramidal ownership structure should

generate a situation in which family members and family business groups can reduce

their financial and loss risk (Claessens et al., 2000, 2002). The choice of pyramidal

ownership is based on financial concerns related to expansion (Almeida & Wolfenzon,

2006). Previous literatures indicate that the use of the pyramidal ownership structure

may be detrimental to performance under some conditions, such as insufficient

shareholder protection or inefficient financial markets in institutional environments

(Morck et al., 2005; Young et al., 2008). In these under-developed institutional

environments, a lower investment by the founding family under the pyramidal

ownership structure will generate a separation between cash flow rights and control

rights in public affiliate firms and thus is bad for minority shareholders’ interests

(La Porta et al., 1999, 2002; Morck et al., 2005; Young et al., 2008). Therefore, the

use of pyramidal ownership will be detrimental to the public affiliate firm’s performance in a family business group (Claessens et al., 2000; La Porta et al., 1999).

Besides the distinctive relationship between family ownership and performance,

furthermore, it is argued that if the founding family does not assign qualified family

members to manage its business, the poor management of the business will be more

detrimental to the family’s goals and social-emotional wealth in family businesses

(Demsetz & Lehn, 1985; Gómez-Mejía et al., 2007). Thus, the founding family’s

ownership will decide whether to choose a family manager or a non-family manager

to manage the family business, as we argue previously. Agency theory suggests that

in a family business context, family leadership compared with the non-family management is helpful to mitigate the agency problem between managers and

�Ownership structure, family leadership, and performance…

311

shareholders since the founding family can maintain control over non-family managers (Chu, 2011; Cruz et al., 2010; Demsetz & Lehn, 1985). In general situations,

family leadership will have positive performance implications (Anderson & Reeb,

2003; Chu, 2011; Fama & Jensen, 1983). Furthermore, for those family business

groups that are embedded in an under-developed institutional environments, family

leadership may help to access to unique resources through kinship networks (Liu,

Yang, & Zhang, 2012). Family leadership will contribute to the family business

group’s performance during market-oriented institutional transition (Luo & Chung,

2005). In a large family business group, the family members can utilize both direct

and pyramidal ownership to control the public and private affiliate firms, and the

different ownership structure will decide whether the founding family will rely on a

family member to lead this affiliate firm or not, as we argued before. Thus, no matter

the affiliate firm is owned by family members directly or indirectly in a pyramidal

ownership structure, family leadership will impose authorized power in strategic

decisions (Chang, 2003; Morck et al., 2005), and accordingly influence the performance in family businesses or family business groups in a positive manner (Anderson

& Reeb, 2003; Cruz et al., 2010; Luo & Chung, 2005).

Following the logic above, in a family business group, the more founding family’s

direct ownership on an affiliate firm, this affiliate will perform better. The use of

pyramidal ownership structure on the other hand will generate negative affiliate firm

performance implications in a family business group. Since the founding family’s

ownership in an affiliate firm will decide whether this affiliate firm is headed by a

family member or not, the family leadership decision will influence affiliate firm

performance in family business groups. Thus, we expect family leadership will mediate

the positive relationship between family ownership and performance in an affiliate firm

in a family business group. Furthermore, since family business under pyramidal ownership is less likely to appoint family members, we expect family leadership to mediate

the negative relationship between pyramidal ownership and affiliate firm performance in

a family business group. The following hypotheses are presented accordingly:

Hypothesis 3 Family leadership will mediate the relationship between ownership

structure and affiliate firm performance in family business groups.

Hypothesis 3a Family leadership will mediate the positive relationship between

direct family ownership and affiliate firm performance in family business groups.

Hypothesis 3b Family leadership will mediate the negative relationship between the

pyramidal ownership structure and affiliate firm performance in family business groups.

Research method

Sample and data

The current research uses longitudinal, multi-level data from 1988 to 2004 to

examine the relationship between ownership structures, family leadership, and the

performance of affiliate firms in Taiwan’s family business groups. We chose to focus

�312

H.-M. Chung, S.-T. Chan

on business groups in Taiwan because Taiwan is one of the world’s 25 largest

economies despite having a relatively small population of less than 30 million

(IMD, 2006). The island also has well-established legal traditions that help to ensure

that the public data reported by the business groups are reliable (IMD, 2006). Taiwan

is representative of a number of other newly industrialized economies with a history

of dominant business groups, including South Korea, Hong Kong, and Singapore

(Chang, 2006; Lasserre & Schütte, 2006). Taiwan is also suitably representative of

other nations with many Chinese residents, including Hong Kong, the People’s

Republic of China, Singapore, Malaysia, and other Asian countries (Lasserre &

Schütte, 2006). The data for the largest 100 business groups in Taiwan from 1988

to 2004 were derived from the China Credit Information Service (1990, 1992, 1994,

1996, 1998, 2000, 2001, 2002, 2003, 2004). Moreover, since there was a marketoriented institutional transition in Taiwan in 1988 (Luo & Chung, 2005), the years

examined in this study are helpful to understand the role of family control in

performance in large family business groups after the institutional transition in

Taiwan. The data culled from this resource have also been employed in previous

studies of Taiwan’s business groups and have proven reliable (e.g., Chung, 2003; Luo

& Chung, 2005). The directory of Taiwanese business groups was published every

two years prior to 1999; thus, 12 yearly datasets were examined for the 16-year period

(1988, 1990, 1992, 1994, 1996, 1998, 1999, 2000, 2001, 2002, 2003, and 2004).

Our focus is on family business groups in the textile, electronic and household

appliance, financial service, and constructing investment industries, which play a

critical economic role in both the domestic and export markets in Taiwan, making up

more than 50% of the island’s export market during the time period examined

(Ministry of Finance, 2008). We classified a business group as family-owned if it

was managed and controlled by a specific family or set of families at that time and if a

previous generation of the same family (or families) had owned that business. As in

previous studies, a business was considered a family business only when there was

more than one family member involved (Cruz et al., 2010; Miller & Le Breton-Miller,

2005). However, the use of longitudinal data can result in family business groups

moving in and/or dropping out of the top-100 business groups. To ensure that any

effects on performance were long-term and not a product of misleading accounting

practices, we required that the family business groups be part of the top-100 business

groups for at least 10 years during the 16 years examined. In this way, we derived a

sample of 21 family business groups.

The analysis was conducted at the affiliate firm level. Because multiple affiliate

firms are nested in one family business group, the data analysis addressed the multilevel nature of the data; we considered the influence of both group-level and affiliate

firm-level variables on the dependent variable (Rabe-Hesketh & Skrondal, 2008).

Moreover, the longitudinal and multi-level nature of the data made it appropriate to

use a hierarchical linear model (Bryk & Raudenbush, 1992) to consider the growth

pattern of the outcomes. The benefits and importance of longitudinal data analysis in

strategic management analysis (Certo & Semadeni, 2006) and business group

research (i.e., Khanna & Rivkin, 2001; Luo & Chung, 2005) is widely recognized.

During the 12 yearly datasets examined, 252 family business groups were employed

in this research (21 [number of family business groups] × 12 [number of year

�Ownership structure, family leadership, and performance…

313

datasets] 0 252). Again, the level of analysis that we used was the affiliate firms in

each family business group. Thus, the 252 family business groups provided us with

the opportunity to investigate 6,916 affiliate firms.

Variables

Dependent variable (Y): Affiliate firm’s performance We considered data for all

affiliate firms in these family business groups, including both public and private

affiliate firms. Because the data explored in the database were limited, we considered

the financial performance of each affiliate firm to indicate whether this affiliate firm

performs efficiently or is adequately productive (Pfeffer, 1997). Thus, we utilized

sales revenue as a proxy for affiliate firm performance when a standard public

performance index was not available (Miller et al., 2008). The sales revenue of each

affiliate firm can indicate the affiliate firm’s efficiency and the outcomes for operation

(Pfeffer, 1997; Scott, 1977).

Mediating variable (M): Family leadership The mediating variable is family leadership in an affiliate firm. In this research, we used the information available on whether

the affiliate head is a family member as a proxy for this variable (e.g., Anderson &

Reeb, 2003; Miller & Le Breton-Miller, 2005). We identified a family member as the

affiliate head based on data from the China Credit Information Service and other

public information. For example, if the affiliate head is described in such data sources

as “having kinship relationships with the founding family members in the group,” we

classified this affiliate head as a family member. The dependent variable was dummycoded as “1” if the affiliate head was a family member and as “0” otherwise.

Independent variables (X1–X2): Affiliate ownership structure To calculate the affiliate

ownership structure used by each family business group, we used data from the China

Credit Information Service for the 12 datasets (1988, 1990, 1992, 1994, 1996, 1998,

1999, 2000, 2001, 2002, 2003, 2004). In distinguishing between direct and pyramidal

family ownership structure, we followed Claessens et al. (2000, 2002) and La Porta

et al. (1999, 2002), who defined control by computing the voting and cash-flow

ownership of the controlling shareholder (or family) based on their direct and indirect

rights. Here, we extended this concept by dividing family ownership into two

categories: direct and pyramidal.

We identified the affiliates’ major shareholders and their shares using multiple

secondary databases, including the China Credit Information Service and other public

databases. The data from the China Credit Information Service indicate most of each

affiliate firm’s major shareholders and their shares. Affiliate firms’ major shareholders may be individuals, firms, or both. If the data on how many shares the main

shareholders had were missing, we attempted to use the appropriate annual reports to

determine this information. In this study, family direct ownership (X1) is the sum of

the following two types of ownership (Claessens et al., 2000, 2002; La Porta et al.,

1999, 2002): (1) the shares directly owned by family members, and (2) the shareholdings of the nominal agents controlled by the family—for example, through nonprofit organizations such as universities and hospitals.

�314

H.-M. Chung, S.-T. Chan

In family business groups, family members can exert overall control over

their group by using both the direct and the pyramidal ownership structures. In

definition, an affiliate firm is controlled by a founding family (or the ultimate

owner) if this founding family’s direct and indirect voting rights in this affiliate

firm exceeds the direct votes controlled by this family (La Porta et al., 2002).

For the founding family in a large family business group, this family’s control over

the cash-flow rights and the voting rights are separate since the founding family can

use relatively smaller cash-flow rights to control higher percentages of voting rights

in an affiliate firm in this family business group (Claessens et al., 2000; La Porta et

al., 1999). Information about the actual ultimate owner’s voting rights, cash-flow

rights, and the pyramidal ownership structure is limited since previous research has

only examined the public affiliate firms in family business groups (Claessens et al.,

2000, 2002; La Porta et al., 1999, 2002). Thus, this approach may create a bias in

terms of ownership structure and firm valuation and thus underestimate the

effect of ownership structure on firm valuation (Claessens et al., 2002: 2747).

Claessens, La Porta, and their colleagues’ measurements only used information about

public affiliate firms to estimate the controlling shareholder’s voting rights and cashflow rights and did not estimate the pyramidal structure in a business group with both

public and private affiliate firms (Claessens et al., 2000, 2002; La Porta et al., 1999,

2002).

Therefore, in calculating the pyramidal ownership structure, we revised the

limitation in the previous calculation (Claessens et al., 2000, 2002; La Porta et

al., 1999, 2002) and redefined the founding family’s (or the ultimate owner’s)

weakest link in the chain of voting rights among the public and private affiliate firms

in a family business group. As in prior research (Claessens et al., 2000, 2002; La

Porta et al., 1999, 2002), a founding family has x percent indirect control over firm A

under the following situations: (1) if this founding family directly controls firm B,

which in turn directly controls x percent of the votes for firm A; or (2) if this founding

family directly controls firm C, which in turn controls x percent of the votes for firm

B, and if firm B directly controls x percent of the votes for firm A. Thus, when the

founding family has personal shareholders or institutional shareholders in the control

chain, and accordingly these multiple shareholders have different percentages of the

votes in the voting rights of control chain, we select the weakest link in the chain of

voting rights (Claessens et al., 2000, 2002). The rationale to pick up the weakest link

in the chain of voting rights is that this founding family can utilize the weakest votes

to control the target affiliate firm (i.e., firm A). Therefore, pyramidal ownership

structure (X2) is the sum of the cross-held shares held by more than one public

affiliate firm in the same family business group. For example, suppose that family

members have directly 25% of the voting rights for firm A, and firm A owns 100% of

firm B. On the other hand, firm B in turn owns 17% of firm A. Thus, in this simple

case, the founding family has 42% of the control rights in firm A, 25% directly and

17% through a pyramidal chain. For more details, please refer to the Appendix for a

more complex case in pyramidal chain.

Control variables The database used contains cross-sectional dominant data (e.g.,

N > T, N 0 6916, T 0 12). To control for possible contemporaneous correlation (i.e.,

the residuals of the units observed in each time period being correlated),

�Ownership structure, family leadership, and performance…

315

following Khanna and Rivkin (2001), we used 12 dummy-coded year variables

(y1988, y1990, y1992, y1994, y1996, y1998, y1999, y2000, y2001, y2002, y2003,

and y2004). Because of collinearity, y1988 and y2004 were dropped from the

statistical model.

Again, this research was conducted at the affiliate firm level, and each affiliate firm

is nested in a specific business group. Thus, we were obliged to control for the

influence of group-level variables. In this paper, we also controlled for business group

size and age (Khanna & Rivkin, 2001). In addition, we controlled for the possible

influence of the number of group affiliates in the 12 year-long sets (Luo & Chung,

2005). Furthermore, in this study, we controlled two variables related to the influence

of the family at the group level. One variable, named “Founding family leadership,”

indicates whether the founder still holds a key leadership position in the family

business group (e.g., Anderson & Reeb, 2003; Cruz et al., 2010). This variable was

dummy-coded, with “1” indicating that the founder still served as the CEO or chair of

the family business group’s core company during the time period examined. Additionally, we also controlled for “Family members in the inner circle” to address

whether each family controlled the strategic direction of the business group (Hamilton,

1997; Luo & Chung, 2005). Family members in the inner circle were identified based

on whether they had ties to the particular family.

In addition to controlling for the influence of group-level variables, we also

controlled for the possible influence of affiliate-level variables, including each foreign affiliate’s industry, age, assets, and location. Whether a firm engages in manufacturing or provides services can influence the characteristics of that firm’s

resources, which in turn can influence the firm’s staffing decisions or even performance (e.g., Cruz et al., 2010). Furthermore, the affiliate’s assets, age, and location

influence the firm’s accumulation of experience and the process of knowledge

transfer from the core company to the affiliate, thus also impacting what coordination

and control mechanisms are chosen (e.g., Anderson & Reeb, 2003; Chang, 2003).

Therefore, we controlled for these characteristics.

Data analysis

The family member assigned as the affiliate head and the structure governing the

family ownership of the affiliate firms are determined based on strategic decisions

that occur at the affiliate firm level. However, the character of the nested family

business group will influence each affiliate decision (Dansereau, Yammarino, &

Kohles, 1999). Thus, in this type of research, the statistical model must be sufficient

to address multi-level issues and to account for the characteristics of the longitudinal

data. We used a growth model for this purpose (Bryk & Raudenbush, 1992; RabeHesketh & Skrondal, 2008), with the multi-level mixed-effects maximum likelihood

model (ML model) together with the STATA 9.0 software. Researchers use the ML

model in regressions when the data are characterized by both random effects generated by the nested group-level variables and fixed effects associated with the affiliatelevel independent variables (Bryk & Raudenbush, 1992; Rabe-Hesketh & Skrondal,

2008). The repeated affiliate observations from the same family business group may

lead to the affiliate observations nested in the same group (Dansereau et al., 1999).

The ML model is a variance-components model that can be used to compensate for

�316

H.-M. Chung, S.-T. Chan

the possible nested effects that occur with variables with two or more levels.

Moreover, the ML model also assumes the variables at the affiliate level to have an

effect on the dependent variable only via the residual term, which has a different

value for each firm-group combination (Rabe-Hesketh & Skrondal, 2008). Thus, the

ML model is a version of a hierarchical linear model (Bryk & Raudenbush, 1992) that

has allowed us to consider the growth patterns in the data and address the possible

intra-level correlation problems that occur in multi-level data. Additionally, to ensure

that homoskedasticity did not negatively impact our analysis, we conducted the test

suggested by Brown and Forsythe (1974) to test the null hypothesis of equality of

variances across groups. The test results led us to reject the null assumption of

homoskedasticity across the panel. Therefore, it is clear that the ML model allowed

us to control for heteroskedasticity, intra-correlation problems that might have occurred with the longitudinal, multi-level data.

Results

Correlation analysis

The results presented in Table 1 indicate that the dependent variable, the affiliate

firm’s performance, is positively correlated with the mediating variable: family

leadership (p ≤ .01). Moreover, affiliate firm performance is positively correlated

with direct family ownership in affiliate firms (p ≤ .05) and negatively correlated with

pyramidal family ownership in affiliate firms (p ≤ .01). Table 1 indicates that family

leadership is positively correlated with direct family ownership of affiliate firms and

negatively correlated with pyramidal family ownership of affiliate firms (p ≤ .01 for

both correlation relationships). The mean and standard deviations of each variable are

indicated in Table 1. Thus, it is clearly important to control for these variables.

Causal analysis

To determine the antecedents and consequences of family leadership in family

business groups, we used two serial ML models that helped us to understand the

relationship between ownership structure, family leadership, and the performance of

affiliate firms in family business groups (see Figure 1). The first series of ML models

(M1 to M4) was used to test Hypotheses 1 and 2, regarding the relationship between

ownership structure and family leadership with regard to affiliate firms in family

business groups. We used the second series (M5 to M10) to test the mediating effects

of family leadership, examining the role of independent, mediating, and dependent

variables. An influential statistical approach to determining mediation was presented

in Baron and Kenny (1986), with an updated account made by Kenny, Kashy, and

Bolger (1998). The Sobel test was also utilized to illustrate the rigor requirement in

mediating effects (Sobel, 1982). In this study, we follow the instructions discussed

extensively in articles on testing mediation (Baron & Kenny, 1986; Kenny et al.,

1998; Lam, Loi, & Leong, 2012; Lau et al., 2007; Sobel, 1982). First, it is necessary

to show that the independent variables are correlated with the mediator (i.e.,

family leadership in the affiliate firm). Second, the direct effects from

�Mean

1. Affiliate’s performance

S.D.

1

2

3

4

85494.87

523946.51

2. Family leadership in

affiliate firm

.47

.50

.099**

3. Family direct

ownership in affiliate

.04

.16

.012*

4. Family pyramidal

ownership in affiliate

.53

.44 −.103** −.196** −.265**

5. Affiliate asset

263793.05

6. Affiliate age

31.55

1892932.28

.770**

199.39 −.004

.076** −.015

–.100**

.052**

.001

−.003

.154** −.315**

.67

.47

.057**

.050**

8. Manufacturing affiliate

.29

.45

.006

.069** −.019

15482220.51 18748625.77

.070** −.153**

.008

.014

10. Group age

40.13

14.37

11. Number of affiliate

72.56

46.63 −.036** −.187** −.137**

12. Percentage of family

member in inner circle

.78

.27

13. Founder leadership

.34

.47 −.026*

6

7

8

9

10

11

12

.156**

7. Affiliate location

9. Group asset

5

−.004

.077** −.083**

−.118** −.036**

.168**

.031** −.017

−.023*

.073** −.018

.331** −.021*

.239**

−.020

.087** −.030**

.136** −.027*

.129** −.076** −.067** −.014

.022*

.198** −.185**

−.016

.043** −.007

−.015

Ownership structure, family leadership, and performance…

Table 1 Correlation matrix.

−.163**

.177** .058**

−.254** −.083** .513**

.000

.072** −.048**

.254**

−.036** .316** −.026*

.084** .002

.215**

.093** −.077** .089**

*p ≤ .05, ** p ≤ .01 (two-tailed).

Unit of affiliate revenue and asset is USD1,000. (Average exchange rate of USD / NTD is 29.56 from 1988 to 2004; Source: Central Bank of R.O.C. http://www.cbc.gov.tw/

content.asp?CuItem027029).

317

�318

H.-M. Chung, S.-T. Chan

X1: Family direct ownership

H1 (+)

M: Family leadership

H2 (–)

X2: Family pyramidal ownership

H3a & H3b

H3b (–)

D: Affiliate firm’s performance

H3a (+)

Figure 1 Model of mediated role of family leadership on the relationship between ownership structure and

affiliate firm’s performance

Note: Solid paths indicate hypothesized relationships. Dotted paths indicate potential indirect influences in

terms of ownership structure effects on performance.

independent variables on the dependent variable must be statistically significant

to establish that there is an effect that may be mediated. Moreover, we need to

test that the effects from independent variables on the dependent variable are

changed after considering the mediator. In that, if the significant relationship

between the independent variables and the dependent variable is no longer

significant after considering the mediator, it can be concluded that the full

mediation occurs. However, if the significant relationship becomes less significant after considering the mediator, we will conclude that the mediator partially

mediates the relationship between the independent variable and the dependent

variable. Third, the use of the Sobel test provides a more rigorous requirement

in mediating effects (Baron & Kenny, 1986; Sobel, 1982). The Sobel test is

utilized to determine whether the mediator carries the effects of the independent

variables on to the dependent variables. In this study, we use the Sobel test to judge

whether the ownership structures, including direct and pyramidal family ownership,

influence family leadership, which in turn influences affiliate firm performance. In

this study, the Wald Chi-square values were significant for all models. Therefore, the

model fitness and setting were deemed satisfactory.

Regarding the influence of the group- and affiliate-level control variables on

family leadership within an affiliate firm, there are several key control variables.

The nested effects of group-level variables including business group size, age, and the

degree of family control are significant. Furthermore, in addressing the influence of

affiliate-level control variables, Table 2 demonstrates that some of the affiliates’

characteristics significantly influence the family leadership of those affiliate firms

in family business groups. Specifically, an affiliate firm’s assets and age have a

positive effect on family leadership decisions, and thus, the larger and older an

affiliate firm is, the more likely it is that a family member will head it (p ≤ .01 for

both the influence from the affiliate firm’s assets and age on performance). Furthermore, if the affiliate firm is based domestically, it is more likely that a family member

will be assigned as the affiliate firm’s leader. Finally, in the particular years examined,

�Ownership structure, family leadership, and performance…

319

Table 2 Relationship between ownership structure and family leadership of affiliate firms in family

business groups.

Family Leadership

Constant

M1

.102 (.054)†

M2

.064 (.051)

M3

.226 (.057)**

M4

.176 (.055)**

Independent Variables

X1: Family direct

ownership

.466 (.050)**

X2: Family

pyramidal

ownership

.418 (.050)**

−.125 (.016)**

−.107 (.016)**

Control Variables

Year 1990

.026 (.046)

.027 (.045)

.013 (.046)

.015 (.045)

Year 1992

−.011 (.042)

.002 (.042)

−.019 (.042)

−.010 (.041)

Year 1994

−.018 (.039)

−.010 (.039)

−.029 (.040)

−.022 (.039)

Year 1996

−.031 (.037)

−.014 (.037)

−.038 (.037)

−.025 (.037)

Year 1998

−.030 (.034)

−.004 (.034)

−.022 (.035)

−.011 (.034)

Year 1999

.005 (.024)

.014 (.024)

.012 (.024)

.015 (.024)

Year 2000

.019 (.020)

.024 (.020)

.024 (.020)

.027 (.020)

Year 2001

.023 (.020)

.028 (.020)

.025 (.020)

.029 (.020)

Year 2002

−.017 (.019)

−.013 (.019)

−.013 (.019)

−.011 (.019)

Year 2003

−.018 (.019)

−.014 (.019)

−.016 (.019)

−.012 (.019)

Affiliate’s assets

.039 (.002)**

.038 (.002)**

.034 (.002)**

.035 (.002)**

Affiliate’s age

.038 (.006)**

.036 (.006)**

.034 (.006)**

.033 (.006)**

Affiliate’s location

−.021 (.013)†

−.028 (.013)*

−.044 (.013)**

−.045 (.013)**

Manufacturing

affiliate

−.043 (.012)**

−.047 (.012)**

−.051 (.012)**

−.053 (.012)**

.008 (.001)**

.007 (.001)**

.008 (.001)**

.007 (.001)**

Control variablesRandom parts

Wald Chi-Square

427.37**

520.21**

495.10**

568.53**

Number of

observations

6,916

6,861

6,861

6,861

Number of Groups

21

21

21

21

The random effect contains group’s size, group’s age, number of affiliates, founding family leadership, and

percentage of family member in inner circle.

Standard deviation data given in parentheses.

†

p ≤ .10, * p ≤ .05, ** p ≤ .01.

if the affiliate firm is in the manufacturing sector, it is less likely for a family member

to be appointed to a leadership position (p ≤ .01).

The results presented in Model 2 (M2) of Table 2 show that the higher the degree

of direct ownership of a founding family in an affiliate firm, the greater the possibility

that the founding family will appoint a family member to a leadership position in the

affiliate firm (β 0 .47, p ≤ .01). Additionally, according to Model 3 (M3) of Table 2, a

greater degree of pyramidal ownership of an affiliate firm has a significantly negative

influence on family leadership decisions regarding the affiliate firm (β 0 −.13, p ≤ .01).

�320

H.-M. Chung, S.-T. Chan

The current data analysis therefore supports the agency theory argument made in

Hypotheses 1 and 2.

Furthermore, following the previous instructions on testing mediation (Baron &

Kenny, 1986; Kenny et al., 1998; Lam et al., 2012; Lau et al., 2007; Sobel, 1982),

Table 3 indicates that family leadership demonstrates differential mediating influence

on the relationship between ownership structure and affiliate firm performance in

family business groups. Specifically, according to Models 6 (M6) and 7 (M7) of

Table 3, during the years examined, family leadership positively mediates the relationship between direct family ownership and affiliate firm performance. In that

period, the higher degree of direct family ownership in an affiliate firm, the higher

possibility that this affiliate firm is headed by a family member, and the family

leadership generates positive performance in this affiliate firm. More importantly,

the significance of family direct ownership on firm performance disappears after

considering family leadership in the regression model (see M7). There are evidences

of mediation according to Baron and Kenny’s test (1986). The Sobel test statistic also

reveals that family leadership mediates the positive effects of family direct ownership

on affiliate firm performance (Z 0 2.94, p < .05). Thus, these results indicate that

Hypothesis 3a is supported. However, according to Models 8 (M8) and 9 (M9) of

Table 3, the founding family’s pyramidal ownership has a more negative impact on

affiliate firm performance when family leadership is included, thus the result definitely does not support Baron and Kenny’s (1986) conditions. Thus, family leadership does not mediate the relationship between family pyramidal ownership and

affiliate firm performance. Moreover, the Sobel test indicates that family leadership

does not significantly mediate the relationship between family pyramidal ownership

and affiliate firm performance (Z 0 −2.85, n.s.). Therefore, Hypothesis 3b is not

supported. These unexpected results are discussed below.

Discussion and conclusion

Family businesses constitute a distinctive worldwide governance system. One of the

key mechanisms through which family businesses (or family business groups as a set

of family businesses) ensure coordination and control is family leadership (Cruz et

al., 2010; Gómez-Mejía et al., 2007; Luo & Chung, 2005; Peng & Jiang, 2010).

However, prior to this research, the academic work done on this control mechanism in

family business groups was limited.

Based on a longitudinal, multi-level analysis of datasets for 12 different years, this

research uses the agency theory viewpoint to address the importance and unique

character of the coordination and control issue for family business groups in Asia.

The results reveal that the different ownership structures of affiliate firms influence

the likelihood that family members will hold leadership positions in firms associated

with a family business group. Specifically, if the founding family enjoys more direct

ownership of the affiliate firm, the family will be likely to appoint a trusted family

member to the leadership position within the affiliate firm. However, when the

founding family has a greater degree of pyramidal ownership of an affiliate firm,

the family will be less likely to appoint a family leader from within. Additionally,

family leadership mediates partially the relationship between the ownership structure

�Affiliate’s Performance

Constant

M5

.039 (.192)

M6

.020 (.193)

M7

−.016 (.193)

M8

.420 (.208)*

.105 (.056)†

M: Family leadership

M9

M10

.416 (.208)*

.406 (.209)†

.128 (.056)*

.132 (.057)*

−.371 (.072)*

−.365 (.072)*

Independent Variables

X1: Family direct ownership

.235 (.216)*

.287 (.217)

X2: Family pyramidal ownership

.140 (.219)

−.342 (.071)**

Control Variables

Year 1990

.518 (.183)**

.513 (.183)**

.522 (.183)**

.464 (.183)*

.472 (.182)**

Year 1992

.475 (.170)**

.463 (.171)**

.468 (.171)**

.409 (.170)*

.411 (.170)*

.469 (.182)**

.411 (.170)*

Year 1994

.578 (.158)**

.580 (.159)**

.584 (.159)**

.523 (.158)**

.524 (.158)**

.523 (.158)**

Year 1996

.565 (.149)**

.576 (.150)**

.573 (.150)**

.527 (.149)**

.520 (.149)**

.522 (.149)**

Year 1998

.504 (.139)**

.494 (.141)**

.496 (.141)**

.459 (.140)**

.459 (.140)**

.459 (.140)**

Year 1999

.091 (.105)

.890 (.106)

.088 (.106)

.085 (.105)

.083 (.106)

.085 (.106)

Year 2000

−.048 (.092)

−.048 (.092)

−.046 (.093)

−.041 (.092)

−.037 (.092)

−.035 (.092)

Year 2001

−.195 (.090)*

−.194 (.091)*

−.196 (.091)*

−.195 (.090)*

−.196 (.090)*

−.194 (.091)*

Year 2002

−.061 (.091)

−.058 (.091)

−.060 (.091)

−.049 (.091)

−.051 (.091)

−.049 (.091)

Year 2003

−.204 (.089)*

−.204 (.089)*

−.203 (.089)*

−.196 (.089)*

−.194 (.089)*

−.193 (.089)*

Affiliate’s assets

.834 (.012)**

.835 (.012)**

.840 (.012)**

−.821 (.012)**

.827 (.012)**

.827 (.012)**

Affiliate’s age

.358 (.027)**

.360 (.028)**

.366 (.028)**

.350 (.028)**

.355 (.028)**

.355 (.028)**

Affiliate’s location

−.086 (.059)

−.092 (.060)

−.091 (.060)

−.150 (.061)*

−.154 (.061)*

Ownership structure, family leadership, and performance…

Table 3 The mediating role of family leadership in ownership structure and affiliate firm’s performance in family business groups.

−.155 (.061)*

Manufacturing affiliate

.747 (.056)**

.745 (.057)**

.741 (.057)**

.726 (.057)**

.720 (.057)**

.720 (.057)**

Control variables-Random parts

.012 (.002)**

.012 (.002)**

.012 (.002)**

.011 (.002)**

.011 (.002)**

.011 (.002)**

321

�322

Table 3 (continued).

Affiliate’s Performance

M5

M6

M7

M8

M9

M10

Wald Chi-Square

7759.73**

7708.06**

7666.69**

7774.79**

7744.44**

7743.77**

Number of Observations

5,892

5,841

5,813

5,840

5,813

5,813

Number of Groups

21

21

21

21

21

21

The random effect contains group’s size, group’s age, number of affiliates, founding family leadership, and percentage of family member in inner circle.

Standard deviation data given in parentheses

†

p ≤ .10, * p ≤ .05, ** p ≤ .01.

H.-M. Chung, S.-T. Chan

�Ownership structure, family leadership, and performance…

323

and an affiliate firm’s performance in a family business group. Family leadership

mediates the positive relationship of direct family ownership on affiliate firm performance; however, family leadership does not mediate the negative relationship between pyramidal ownership and affiliate firm performance in a family business group.

Compared with the direct family ownership, pyramidal ownership will generate a

relatively lower financial risk situation for founding family in a family business

group. The more pyramidal ownership in an affiliate firm will lower the likelihood

of family leadership choice, and accordingly the possibility that family leadership will

generate positive motivation in affiliate firm’s management and performance will be

reduced. Evidences indicate that family leadership cannot account for the negative

affiliate firm performance from pyramidal ownership in a family business group. The

possible solutions in addressing the pyramidal ownership-performance issues will be

raised after.

Contributions

The results, which are consistent with those of previous research (e.g., Chu, 2011;

Cruz et al., 2010), provide further insight into agency theory, expanding it by

explaining the mechanisms of coordination and control in family businesses, especially the complex network among affiliate firms in a family business group. Examining unbalanced control by considering direct and pyramidal ownership at the

affiliate firm level will provide insights into the use of agency theory to analyze

family business groups. The agency or performance issues associated with pyramidal

ownership at the group level are the typical concerns (Almeida & Wolfenzon, 2006;

Morck et al., 2005; Young et al., 2008). Performance issues associated with both

direct and pyramidal ownership at the affiliate firm level are particularly a key

concern in a family business group (Carney et al., 2011; Chang, 2003). Thus,

examining the possible performance implications of family leadership under the

direct and pyramidal ownership structures in a family business group can provide

more information about control and leadership issues in family business groups,

which are the typical governance structure in the Asian context (Carney et al.,

2011; Yiu et al., 2007). In short, the findings presented in this study provide a better

theoretical understanding of leadership issues and results associated with family

business groups.

The findings presented here also indicate the strategic implications of ownership

structure and family leadership in the context of family businesses (e.g., Miller et al.,

2008; Peng & Jiang, 2010; Villalonga & Amit, 2006). Ownership structure and

family leadership need to be considered carefully in addressing performance. The

personal trust established via family ties is good for intra-business and intra-business

group coalitions, and these ties are a strategic choice under different ownership

structures. We know from this study that family leadership will be conducive to

improve the affiliate firm’s shareholder value under specific conditions, such as

family direct ownership concern, in a family business group. However, we also

believe that this kind of leadership is not the only solution to improve affiliate firm

performance in a family business group. Indeed, besides the family leadership

concern on performance issues in family business groups, there are still other kinds

of external and internal governance arrangements, such as independent directors in

�324

H.-M. Chung, S.-T. Chan

board of directors (Anderson & Reeb, 2004), or the presence of legal institutions and

multiple blockholders structure (Jiang & Peng, 2011), that can provide positive

performance implications for majority and minority shareholders in family businesses

or family business groups. The longitudinal evidence from this study indicates that

family leadership can provide positive performance implications in Asian family

business groups, but this study also leaves answers to the advanced performance

issues that concern the relationship between family leadership and institutional

arrangements. Future work can address performance issues to illustrate the interwoven

nature among family business’s ownership structure, leadership choices, performance

implications, and the institutional contexts, especially in the Asian region that is

characterized by divergent cultural backgrounds and institutional contexts (Ahlstrom,

Chen, & Yeh, 2010; Bruton & Lau, 2008; Jiang & Peng, 2011).

The results of this research may also be useful in other domains. One is in

business groups, more broadly, as noted in the introduction. This application is

especially helpful because even though such groups are the dominant organizational form outside North America, they still remain poorly understood. The

evidence presented here facilitates a better understanding of coordination and

control issues in such organizations (Carney et al., 2011). Future work to examine

the relationships among ownership structure, family leadership, and affiliate firm

performance in distinctive institutional contexts can provide more fruitful understandings in coordination and control issues in business groups in Asia or around

the world (Jiang & Peng, 2011; Peng & Jiang, 2010; Yiu et al., 2007). In addition, the

use of longitudinal and multi-level data provides a rare look into the performance of

such business groups over time. To date, there has been little effort to conduct this

type of analysis.

Limitations and future research directions

Since this research relies on secondary data, there are several limitations. For

example, we cannot identify the influence of family dynamics or even the

family leadership style on coordination and control in family business groups.

Future research might consider the family dynamics influence or family leadership style from the questionnaire to create a comprehensive model of control

and coordination within family businesses. Moreover, this research provides

possible answers on addressing the antecedents and consequences of family

leadership in family business groups; future work can address family leadership

types-outcomes issues from questionnaires to advances the understanding of

family leadership styles and the distinctive macro outcomes in family businesses or family business groups. For example, previous studies have provided

fruitful evidences on addressing the paternalistic leadership style-micro outcomes issues in Asian family businesses, especially focusing on Chinese family

businesses (Cheng et al., 2000, 2002a, 2002b; Farh et al., 2006). Future work can

examine the paternalistic leadership style-macro outcomes relationships in Asian

family business enterprises to provide more understanding on family leadership

issues in the Asian Pacific region. Besides the leadership-macro outcomes issues,

what leadership patterns (e.g., transformational, transactional, and ethical leadership)

�Ownership structure, family leadership, and performance…

325

are more conducive in enhancing shareholder’s value when family members are

appointed as leaders is also an advanced issue in the family business field. Additionally, this study’s exclusive use of data from one country may create concerns

regarding generalization. Comparative research on family businesses in Asia may

help researchers to further advance our understanding of coordination and control in

Asian family businesses. Furthermore, comparative studies to address the performance issues by family leadership choice under differential institutional contexts will

be helpful to provide solutions in mitigating the principal-principal concerns in Asian

family business groups.

This research has laid an important foundation for the better understanding of

family businesses, especially in Asia. Future research should continue to expand our

understanding of this issue given that the importance and impact of such firms will

likely only grow in the future as the economic power of this region increases.

Moreover, this research also advances our knowledge of leadership. Future research

can continue to probe the importance of leadership within family enterprises.

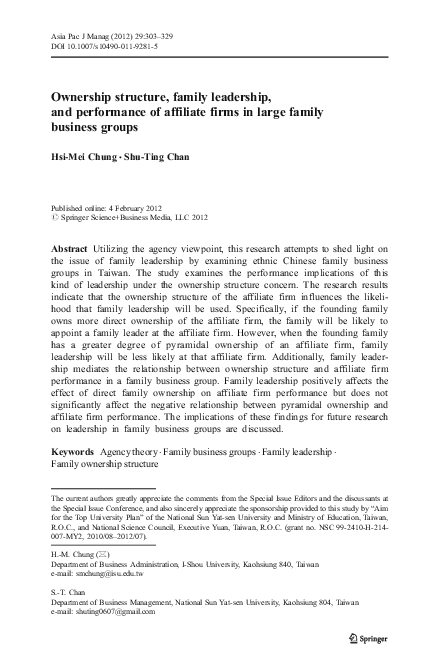

Appendix

Example of direct and pyramidal ownership structure in family business group

In this Appendix, we illustrate the example raised under the Independent variables

section with a picture. The founding family controls the target affiliate firm A by

three kinds of chain in the chain of voting rights (i.e., chain a, chain b, and chain c).

The calculation of family direct ownership and pyramidal ownership structure are

indicated below.

(1) Family direct control (chain a) is the shares directly owned by family members.

Thus, family direct control of firm A is 25%.

(2) Family pyramidal control (chain b and chain c) is the sum of shares that crossshareholding through more than one listed affiliates in the same business group.

In this example, family pyramidal control of firm A includes chain b (in this

chain, family controls 25% rights of firm A which control 100% rights of firm B,

and firm B in turn has 17% rights of firm A) and chain c (in this chain, family

has 25% of firm C, and firm C controls 7% of firm A).

According to La Porta et al. (1999, 2002), the highest minimum voting stake along

the control chain was picked when the firm’s shareholders have over 10% voting

rights. However, because we illustrate all possible controlling situations of family

members and not just focus on large or public firms, we select the minimum voting

rights along the control chain and do not take 10% voting rights as picking limitation.

This argument is similar with Claessens et al.’s (2000, 2002) study. Based on

Claessens et al.’s (2000, 2002) study, the weakest link in the chain of voting rights

means the minimal voting rights across the ownership chain. Therefore, the weakest

link of chain b is 17% (the minimum of 25%, 100%, and 17%) and of chain c is 7%

(the minimum of 25% and 7%). We would say that the family controls 17% of firm A

along the control chain b and 7% of firm A along the control chain c. Thus, the total

�326

H.-M. Chung, S.-T. Chan

family pyramidal control of firm A is 24% which is the sum of 17% from chain b and

7% from chain c.

25

100%

a

Firm A

b

c

Family

7%

25

17

Firm B

Firm C

49

Family direct control (from chain a): 25%

Family pyramidal control (17% from chain b plus 7% from chain c): 24%

References

Ahlstrom, D., Chen, S.-j., & Yeh, K. S. 2010. Managing in ethnic Chinese communities: Culture,

institutions, and context. Asia Pacific Journal of Management, 27(3): 341–354.

Almeida, H., & Wolfenzon, D. 2006. A theory of pyramidal ownership and family business group. Journal

of Finance, 61: 2637–2680.

Anderson, R. C., & Reeb, D. M. 2003. Founding-family ownership and firm performance: Evidence from