Academia.edu no longer supports Internet Explorer.

To browse Academia.edu and the wider internet faster and more securely, please take a few seconds to upgrade your browser.

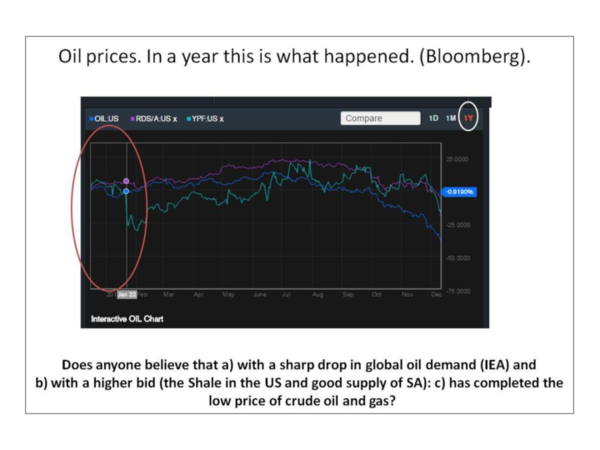

Oil prices

Pedro Dudiuk

Pedro DudiukRelated Papers

PSL Quarterly Review

Oil and its markets2015 •

Oil markets are extremely complex, characterized by an interplay of economic, political, technological and ecological issues. The paper begins by pointing to the high ratio between fixed and variable costs as a characteristic of the oil sector in all its production stages. Then the story of the sector is sketched, since the expansion of Rockefeller's Standard Oil Trust in the late Nineteenth century. Anti-trust intervention and collusion characterize the first part of the story; the notion of "trilateral oligopoly" (oil companies, producing and consuming countries) is then utilized in interpreting the developments since the Second World War. An illustration and a critique of the role played by financial markets in the determination of oil prices is accompanied by a critique of the theories interpreting oil prices as determined by its nature as a scarce natural resource. Recent trends in the oil sector, with the development of shale oil, are briefly considered.

2004 •

Bassam Fattouh , it is possible to draw the following conclusions: Markets with relatively low volumes of production such as WTI, Brent, and Dubai-Oman set the price for markets with higher volumes of production elsewhere in the world but with fewer or none of the commonly accepted conditions to achieve an acceptable „benchmark‟ status. So far the low and continuous decline in the physical base of existing benchmarks has been counteracted by including additional crude streams in an assessed benchmark. Such short-term solutions though successful in alleviating the problem of squeezes should not distract observers from some key questions: What are the conditions necessary for the emergence of successful benchmarks in the most liquid market? Would a shift to assessing price to these markets improve the price discovery process? Such key questions remain heavily under-researched in the energy literature and do not feature in the producer-consumer dialogue. The emergence of the non-OECD as the main source of growth in global oil demand will only increase the importance of such questions. Doubts about the suitability of Dubai as an appropriate benchmark for pricing crude oil exports to Asia have been raised in the past (Horsnell and Mabro, 1993). This raises the question of whether new benchmarks are needed to reflect more accurately the recent shift in trade flows and the rise in importance of the Asian consumer. PRAs play an important role in assessing the price of the key international benchmarks. These assessed prices are central to the oil pricing system and are used by oil companies and traders to price cargoes under long-term contracts or in spot market transactions; by futures exchanges for the settlement of their financial contracts; by banks and companies for the settlement of derivative instruments such as swap contracts; and by governments for taxation purposes. PRAs do not only act as „a mirror to the trade‟. In their attempt to identify the price, PRAs enter into the decision-making territory. The decisions they make are influenced by market participants and market structure while at the same time these decisions influence the trading strategies of the various participants. New markets and contracts may emerge to hedge the risks that emerge from some of the decisions that PRAs make. The accuracy of price assessments heavily depends on a large number of factors including the quality of information obtained by the RPA, the internal procedures applied by the PRAs and the methodologies used in price assessment. The assumption that the process of identifying the price of benchmarks in the current oil pricing system can be isolated from financial layers is rather simplistic. The analysis in this report shows that the different layers of the oil market are highly interconnected and form a complex web of links, all of which play a role in the price discovery process. The information derived from financial layers is essential for identifying the price level of the benchmark. One could argue that without these financial layers it would not be possible to „discover‟ or „identify‟ oil prices in the current oil pricing system. In effect, crude oil prices are jointly co-determined and identified in both layers, depending on differences in timing, location and quality. Since physical benchmarks constitute the basis of the large majority of physical transactions, some observers claim that derivatives instruments such as futures, forwards, options and swaps derive their value from the price of these physical benchmarks i.e. the prices of these physical benchmark drive the prices in paper markets. However, this is a gross over-simplification and does not accurately reflect the process of crude oil price formation. The issue of whether the paper market drives the physical or the other way around is difficult to construct theoretically and test empirically in the context of the oil market. 79 The report also calls for broadening the empirical research to include the trading strategies of physical players. The fact remains though that the participants in many of the OTC markets such as forward markets and CFDs which are central to the price discovery process are mainly „physical‟ and include entities such as refineries, oil companies, downstream consumers, physical traders, and market makers. Financial players such as pension funds and index investors have limited presence in many of these markets. Thus, any analysis limited to non-commercial participants in the futures market and their role in the oil price formation process is incomplete. The analysis in this report emphasises the distinction between trade in price differentials and trade in price levels. We postulate that the level of the price of the main benchmarks is set in the futures markets; the financial layers such as swaps and forwards set the price differentials depending on quality, location and timing. These differentials are then used by oil reporting agencies to identify the price level of a physical benchmark. If the price in the futures market becomes detached from the underlying benchmark, the differentials adjust to correct for this divergence through a web of highly interlinked and efficient markets. Thus, our analysis reveals that the level of oil price, which consumers, producers and their governments are most concerned with, is not the most relevant feature in the current pricing system. Instead, the identification of price differentials and the adjustments in these differentials in the various layers underlie the basis of the current oil pricing system. By trading differentials, market participants limit their exposure to risks of time, location grade and volume. Unfortunately, this fact has received little attention and the issue of whether price differentials between different markets showed strong signs of adjustment in the 2008-2009 price cycle has not yet received its due attention in the empirical literature. But this leaves us with a fundamental question: what factors determine the price level of an oil benchmark in the first place? The crude oil pricing system and its components such as the PRAs reflect how the oil market functions: if oil price levels are set in the futures market and if participants in these markets attach more weight to future fundamentals rather than current fundamentals and/or if market participants expect limited feedbacks from both the supply and demand side in response to oil price changes, these expectations will be reflected in the different layers and will ultimately be reflected in the assessed price. The adjustments in differentials are likely to ensure that these expectations remain anchored in the physical dimension of the market. Transparency in oil markets has more than one dimension. Although improving transparency in the physical dimension of the market is key to understanding oil market dynamics and enhancing the price discovery function, our analysis shows that transparency in the financial layers surrounding the physical benchmarks is as important. In this regards, it is important to emphasize three dimensions to the transparency issue. First, obtaining regular and accurate information on key markets is not straightforward and depends largely on the willingness of PRAs to release or share information. Second, the degree of transparency varies considerably within the different layers in the Brent, WTI and Dubai-Oman complexes as well as across benchmarks. The third dimension of transparency relates to the extent assessed prices are accurate and are reached through a transparent and efficient process. There are two aspects to this issue. The first aspect relates to the structural features of the oil market trading which impose certain constraints on these agencies‟ efforts to report deals and identify the oil price. The second aspect is linked to the internal operations of PRAs. Thus, the degree of price transparency is very much interlinked to the activities of PRAs and the reporting standards and other procedures that they internally set and enforce. The current oil pricing system has now survived for almost a quarter of a century, longer than the OPEC administered system did. While some of the details have changed, such as Saudi Arabia‟s decision to replace Dated Brent with Brent futures price in pricing its exports to Europe and the more recent move to replace WTI with Argus Sour Crude Index (ASCI) in pricing its exports to the US, these changes are

Crude oil prices have trended up since the end of the 1990s, peaking at a historic high in mid-2008 that was followed by a steep price correction with a subsequent rebound. This paper considers major forces behind the evolution of the oil price, using a simple model of supply and demand elasticities as a benchmark, highlights implications for inflation and economic activity and draws some conclusions for macroeconomic policy. The analysis suggests that the run-up in crude oil prices since 2003 was due to both vigorous oil demand growth by emerging markets and, from the middle of the decade onward, a weaker than expected oil supply response to rising prices. Prices are unlikely to fall back to levels seen in the first years of the decade either over the short or medium term. Évolution récente du prix du pétrole : Facteurs explicatifs et questions de politiques économiques Les prix du pétrole brut ont crû régulièrement depuis la fin des années 90, jusqu’à atteindre un plus haut histor...

Oil price volatility shows the degree of rise or fall in oil prices over time. The price of crude oil is highly influenced by the fluctuations in supply–demand gap and global macroeconomic and geopolitical conditions. The Organization of the Petroleum Exporting Countries (OPEC) plays an important role in the global oil supply and demand. The oil price volatility depends on the combined effects of invariant and variable factors. Invariant factors include feedstock prices, exploration costs, drilling costs, chemical composition of oil, production costs, distribution costs, marketing costs, and packaging and storage costs, while the variable factors include global economic activity, level of production, level of consumption , exchange value of the US dollar ($), current supply and demand, geopoli-tical reasons, weather-related developments, and political events. Supply factors have played a more important role than demand factors in driving the 50% drop in the oil price between mid 2014 and early 2015. This paper aims to review the historical change in the crude oil prices, control limits of the OPEC annual price per barrel from 2003 to 2015, and factors affecting the oil price volatility. As a result of the review, a mean and standard deviation for the last 13 years (2003– 2015) was estimated by setting an upper limit (US $ 128.63 per barrel) with ambition that this will support the oil-producing nations in gaining large cash surplus in their fiscal budget. Similarly, a lower control limit can be set at US $ 16.97. However, this will cause a direct loss to crude oil exporters, but the impacts vary from one oil-producing country to another country.

2003 •

Loading Preview

Sorry, preview is currently unavailable. You can download the paper by clicking the button above.

RELATED PAPERS

2023 •

TEORÍA Y PRÁCTICA DEL PRECEDENTE JUDICIAL EN IBEROAMÉRICA

Derogación y resolución de antinomias entre precedentes2022 •

Aferrarse al mundo. historias de lectoras, lectores y sus bibliotecas

El cuarto iluminado2023 •

Banks and Bank Systems

Risk management and performance of deposit money banks in Nigeria: A re-examination2020 •

Finite Mathematics

Finite Mathematics -An Applied Approach. Michael Sullivan2024 •

Etnicidade na América Latina: um debate sobre raça, saúde e direitos reprodutivos

A propósito das relações entre etnicidade, cultura, poder e saúde2004 •

International Journal of Lexicography

A Review of Three Recent Dictionaries of Indigenous Languages Spoken in South America2023 •

British Journal of Political Science

Habit Formation and Political Behaviour: Evidence of Consuetude in Voter Turnout2000 •

JURNAL PEMULIAAN TANAMAN HUTAN

Pengujian Penanda Jenis Spesifik Pada Jamur Yang Berpotensi Sebagai Agens Pengendali Hayati Penyakit Busuk Akar Pada Akasia2018 •

Palgrave Communications

From the exclusion of the people in neoliberalism to publicity without a public2017 •

International Public Management Review

Emerging governances, different perspectives2021 •

Applied and Environmental Microbiology

Rapid Genomic-Scale Analysis of Escherichia coli O104:H4 by Using High-Resolution Alternative Methods to Next-Generation Sequencing2011 •

Jurnal Keperawatan Abdurrab

Fungsi Kognitif Dan Status Gizi Pada Lansia DI Puskesmas Sedayu II Bantul2022 •

2017 •

Frontiers in Psychology

“Where’s Wally?” Identifying theory of mind in school-based social skills interventions2022 •