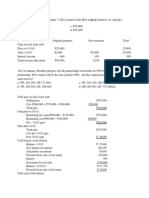

Partnership Formation111

Partnership Formation111

Download as doc, pdf, or txt

You might also like

- BSBCRT611 Assessment 2 - FelipeDocument27 pagesBSBCRT611 Assessment 2 - FelipeAna Martinez86% (21)

- Chapter 1 Partnership Formation Test BanksDocument46 pagesChapter 1 Partnership Formation Test BanksRaisa Gelera92% (24)

- Solution Manual - Partnership & Corporation, 2014-2015 PDFDocument77 pagesSolution Manual - Partnership & Corporation, 2014-2015 PDFRomerJoieUgmadCultura78% (88)

- Partnership Midterm Set BDocument10 pagesPartnership Midterm Set BLene100% (1)

- 1 1 4-Partnership-LiquidationDocument7 pages1 1 4-Partnership-LiquidationCundangan, Denzel Erick S.67% (3)

- Partnership Liquidation. Alynna Joy P. IbanezDocument32 pagesPartnership Liquidation. Alynna Joy P. IbanezAllynna Joy83% (6)

- Chapter 1 - PartnershipDocument72 pagesChapter 1 - PartnershipJohn Lloyd Yasto100% (5)

- Quiz Liquidation and DissolutionDocument30 pagesQuiz Liquidation and DissolutionIan RanilopaNo ratings yet

- Partnership Problems Partnership Problems: Accountancy (La Consolacion College) Accountancy (La Consolacion College)Document35 pagesPartnership Problems Partnership Problems: Accountancy (La Consolacion College) Accountancy (La Consolacion College)MIKASA67% (3)

- Quiz-1 ILUSORIODocument5 pagesQuiz-1 ILUSORIOGlennizze Galvez100% (5)

- Partnership Formation111Document6 pagesPartnership Formation111Rhoiz75% (8)

- 2016 Jan 1 Cash Computer Equipment Lok, Capital: General Journal Date ParticularsDocument25 pages2016 Jan 1 Cash Computer Equipment Lok, Capital: General Journal Date ParticularsMoon Binn100% (2)

- Ansay, Allyson Charissa T - Activity 4Document14 pagesAnsay, Allyson Charissa T - Activity 4Allyson Charissa AnsayNo ratings yet

- Practical Accounting 2: Theory & Practice Advanced Accounting Partnership Liquidation & IncorporationDocument41 pagesPractical Accounting 2: Theory & Practice Advanced Accounting Partnership Liquidation & Incorporationsino ako100% (1)

- Afar ParcorDocument271 pagesAfar Parcorawesome bloggers50% (2)

- B.) CC, P25,000: PP, P21,000 Aa, P38,000Document22 pagesB.) CC, P25,000: PP, P21,000 Aa, P38,000Wendelyn TutorNo ratings yet

- ST Chapter 1 2Document3 pagesST Chapter 1 2Joresol AlorroNo ratings yet

- Partnership Operations Enabling AssessmentDocument6 pagesPartnership Operations Enabling AssessmentVon Andrei MedinaNo ratings yet

- Partnership Formation Enabling AssessmentDocument7 pagesPartnership Formation Enabling AssessmentVon Andrei Medina100% (2)

- PARTNERSHIP Questions Problems With AnswersDocument11 pagesPARTNERSHIP Questions Problems With AnswersFlor Danielle Querubin100% (5)

- Partnership AcctgDocument4 pagesPartnership Acctgcessbright100% (1)

- Reviewer On Partnership Problems - Q2 PDFDocument3 pagesReviewer On Partnership Problems - Q2 PDFAdrian Montemayor33% (3)

- RMC 46-99Document7 pagesRMC 46-99mnyng100% (1)

- Solutions For Midterm Exam Part 2 Selected RroblemsDocument10 pagesSolutions For Midterm Exam Part 2 Selected RroblemsJeane Mae BooNo ratings yet

- Partnership 2222Document2 pagesPartnership 2222Rhoiz71% (7)

- Partnership ContinuationDocument3 pagesPartnership ContinuationRhoiz100% (2)

- Part 5555Document2 pagesPart 5555Rhoiz80% (5)

- Partnership ExercisesDocument37 pagesPartnership ExercisesVilma TayumNo ratings yet

- 1.1.1partnership FormationDocument12 pages1.1.1partnership FormationCundangan, Denzel Erick S.100% (3)

- Part 3333Document2 pagesPart 3333Rhoiz100% (2)

- NSBZDocument6 pagesNSBZKenncy100% (4)

- Mid Term Exam Oct 2016 With SolDocument11 pagesMid Term Exam Oct 2016 With Solsunflower33% (3)

- Pwala 2Document20 pagesPwala 2navie V100% (4)

- Problem Solving: A: Purchasing Which of The Following Statements Is CorrectDocument6 pagesProblem Solving: A: Purchasing Which of The Following Statements Is CorrectActg SolmanNo ratings yet

- 001 Partnership Formation ActivityDocument9 pages001 Partnership Formation ActivityKenncy100% (1)

- Parcor CaseletsDocument13 pagesParcor CaseletsErika delos Santos100% (2)

- 1Document4 pages1sushi100% (1)

- Partnership DissolutionDocument17 pagesPartnership DissolutionMich Salvatorē0% (1)

- PracticeProblems Set1withAnswersDocument5 pagesPracticeProblems Set1withAnswersRoselle Jane LanabanNo ratings yet

- Partnership Dissolution MCQ Reviewer Partnership Dissolution MCQ ReviewerDocument9 pagesPartnership Dissolution MCQ Reviewer Partnership Dissolution MCQ ReviewerKarl Wilson Gonzales100% (1)

- Ac Far Quiz7Document4 pagesAc Far Quiz7Kristine Joy Cutillar100% (1)

- Finals Quiz Dissolution To LiquidationDocument6 pagesFinals Quiz Dissolution To LiquidationJeane Mae Boo75% (4)

- Partnership Formation Answer KeyDocument8 pagesPartnership Formation Answer KeyNichole Joy XielSera TanNo ratings yet

- 1 - PDFsam - 01 Partnership Formation & Admission of A Partnerxx PDFDocument43 pages1 - PDFsam - 01 Partnership Formation & Admission of A Partnerxx PDFnash67% (3)

- Partnership MyDocument13 pagesPartnership MyHoneylyne PlazaNo ratings yet

- Blue and Rubi Are Partners Who Share Profits and Losses in The Ratio of 6Document7 pagesBlue and Rubi Are Partners Who Share Profits and Losses in The Ratio of 6Mark Edgar De Guzman100% (1)

- PartnershipDocument10 pagesPartnershipMark Joseph Urmeneta Fernando80% (5)

- Quiz 2 Problem 1Document4 pagesQuiz 2 Problem 1Mitch Tokong MinglanaNo ratings yet

- Multiple Choice Questions: Partnership FormationDocument118 pagesMultiple Choice Questions: Partnership Formationfghhnnnjml100% (1)

- Quiz in PartnershipDocument13 pagesQuiz in PartnershipDonalyn BannagaoNo ratings yet

- Module 1 Partnerships Basic Considerations and OrganizationsDocument48 pagesModule 1 Partnerships Basic Considerations and Organizationscha11No ratings yet

- Ac Far Quiz8Document4 pagesAc Far Quiz8Kristine Joy CutillarNo ratings yet

- 139Document9 pages139Allynna JoyNo ratings yet

- P2 AnswerKey PDFDocument9 pagesP2 AnswerKey PDFJay Mark DimaanoNo ratings yet

- Partnership Formation111 PDF FreeDocument6 pagesPartnership Formation111 PDF FreeMAG MAGNo ratings yet

- AFAR DAYAG - Anna Joy S. TalanDocument129 pagesAFAR DAYAG - Anna Joy S. TalanAllynna Joy62% (13)

- 핸드아웃Document9 pages핸드아웃hanselNo ratings yet

- Partnership Formation and OperationsDocument60 pagesPartnership Formation and OperationsMiquel Villamarin50% (2)

- Bsa Partnership Multiple Choice QuestionsDocument42 pagesBsa Partnership Multiple Choice QuestionsKath CamacamNo ratings yet

- Partnership FormationDocument13 pagesPartnership FormationGround ZeroNo ratings yet

- Accounting For Special TransactionsDocument43 pagesAccounting For Special TransactionsNezer VergaraNo ratings yet

- Accounting For Special TransactionsDocument43 pagesAccounting For Special Transactionsjohnpenielmontales0% (1)

- Midterm Exam Part 2 Short Problems RemovalDocument6 pagesMidterm Exam Part 2 Short Problems RemovalJeane Mae BooNo ratings yet

- Accounting For Partnership FARDocument31 pagesAccounting For Partnership FARlousevero10No ratings yet

- Midterm Exam Part 2 Short ProblemsDocument5 pagesMidterm Exam Part 2 Short Problemsdagohoy kennethNo ratings yet

- Slide Presentation - Lesson 1Document17 pagesSlide Presentation - Lesson 1RhoizNo ratings yet

- Five Basic Skills of BasketballDocument10 pagesFive Basic Skills of BasketballRhoiz100% (4)

- Part 5555Document2 pagesPart 5555RhoizNo ratings yet

- Part 3333Document2 pagesPart 3333Rhoiz100% (2)

- The Importance and Characteristics of Life InsuranceDocument3 pagesThe Importance and Characteristics of Life InsuranceGowsik kumar palanisamyNo ratings yet

- IFM TB ch18Document9 pagesIFM TB ch18Faizan Ch100% (1)

- How To Control InflationDocument3 pagesHow To Control InflationShingirayi MazingaizoNo ratings yet

- Maximize Efficiency How Automation Can Improve Your Loan Origination ProcessDocument7 pagesMaximize Efficiency How Automation Can Improve Your Loan Origination ProcessShakil ChowdhuryNo ratings yet

- TFC Company ProfileDocument13 pagesTFC Company ProfileNagapraneethNo ratings yet

- Business RiskDocument4 pagesBusiness Riskrotsacreijav66666No ratings yet

- Mar 2024Document3 pagesMar 2024jatinarts123No ratings yet

- Igcse Accounting Paper 1 + Marking Scheme February March 2022Document15 pagesIgcse Accounting Paper 1 + Marking Scheme February March 2022AHMADNo ratings yet

- WILL FormatDocument3 pagesWILL FormatBrig. Baldev SinghNo ratings yet

- Corporate Social Irresponsibility Towards Investors-A Case Analysis of Sahara GroupDocument2 pagesCorporate Social Irresponsibility Towards Investors-A Case Analysis of Sahara GroupVaibhav SalaskarNo ratings yet

- Cost Accounting - Job Process Costing Flashcards - QuizletDocument56 pagesCost Accounting - Job Process Costing Flashcards - QuizletReicci Lisette JumalonNo ratings yet

- SBLCwayDocument2 pagesSBLCwayswiftcenterNo ratings yet

- GainesboroDocument21 pagesGainesboroBayu Aji PrasetyoNo ratings yet

- Capital BudgetingDocument9 pagesCapital BudgetingSEKEETHA DE NOBREGANo ratings yet

- BA WorkbookDocument36 pagesBA Workbookchaitanyavashishth1No ratings yet

- Special Incentive LawsDocument5 pagesSpecial Incentive LawsCrizryshel Loreen P. DeramaNo ratings yet

- Session 11Document88 pagesSession 11Tram AnhhNo ratings yet

- Chapter 4 - Time Value of MoneyDocument76 pagesChapter 4 - Time Value of Moneyshyam9876278551No ratings yet

- TCH White Paper The Custody Services of BanksDocument46 pagesTCH White Paper The Custody Services of BanksMax muster WoodNo ratings yet

- Solutions of Revision Session by AMK Sept 2020 AttemptDocument13 pagesSolutions of Revision Session by AMK Sept 2020 AttemptShehrozSTNo ratings yet

- Payment-Rs 83000-State Bank of IndiaDocument1 pagePayment-Rs 83000-State Bank of IndiaJanmendraNo ratings yet

- Blackbook Project RahulDocument42 pagesBlackbook Project Rahulpiyushborade143No ratings yet

- Cargo Handling MNSDocument7 pagesCargo Handling MNSVashishtNo ratings yet

- Final Defense ScriptDocument4 pagesFinal Defense Scriptandeng100% (1)

- Buisness IsuDocument2 pagesBuisness Isuapi-443367376No ratings yet

- Tax Bar QsDocument56 pagesTax Bar QsXyra BaldiviaNo ratings yet

- Damodaran PDFDocument97 pagesDamodaran PDFAnonymous xjWuFPN3iNo ratings yet