Petrochemical Feedstock Outlook - A Tale of Two Markets: 7 November 2019 - Singapore

Petrochemical Feedstock Outlook - A Tale of Two Markets: 7 November 2019 - Singapore

Download as pdf or txt

At a glance

Powered by AI

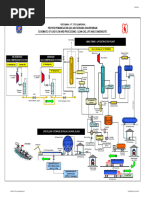

The key takeaways from the document are that naphtha demand will continue to rise due to strong petrochemicals demand growth, though gasoline demand declines may offset this. Refinery integration with petrochemicals will be important for competitiveness. Significant changes are expected in refining and petrochemical operations in the long term.

The main drivers of olefins demand are increasing use of light naphtha as a feedstock and robust demand growth. Ethylene production from naphtha is projected to increase its share substantially through 2040.

While naphtha demand will continue to rise with petrochemicals growth, supply increases will slow as refined products demand declines. Refineries will still be the primary source but growth will depend on downstream demand. Alternative supply sources may emerge.

You might also like

- Organic Chemistry Practice Question 0002Document11 pagesOrganic Chemistry Practice Question 0002JasonTenebroso100% (4)

- Ige TD 13Document73 pagesIge TD 13Anant RubadeNo ratings yet

- Unit 02 Karbala Refinery Project - Oct 3 17Document37 pagesUnit 02 Karbala Refinery Project - Oct 3 17noor taha100% (2)

- Uniflex Eliminate Fuel OilDocument20 pagesUniflex Eliminate Fuel Oilsantoso hadiNo ratings yet

- Pengenalan PLTU Teluk Sirih PDFDocument19 pagesPengenalan PLTU Teluk Sirih PDFDinata Putra100% (1)

- Steam AccumulatorsDocument3 pagesSteam Accumulatorsedi mambang daengNo ratings yet

- Corrosion Inhibitors For Refinery OperationsDocument15 pagesCorrosion Inhibitors For Refinery OperationsAnik AichNo ratings yet

- Petroleum Refining Process: Source: U.S. Department of LaborDocument2 pagesPetroleum Refining Process: Source: U.S. Department of LaborAmmr MahmoodNo ratings yet

- Trislot Reactor Internal Part PDFDocument12 pagesTrislot Reactor Internal Part PDFjonathanNo ratings yet

- Complex Refinery Flowchart - 2Document1 pageComplex Refinery Flowchart - 2Bilal AhmadNo ratings yet

- 4 FINAL Solvent de Asphalting Conversion VCMStudyDocument20 pages4 FINAL Solvent de Asphalting Conversion VCMStudyebik440No ratings yet

- CDUDocument41 pagesCDUsidhuysn100% (2)

- RIL JamnagarDocument21 pagesRIL JamnagarPiyu Sol100% (2)

- BFD of Kurnell RefineryDocument1 pageBFD of Kurnell RefineryMuhammad Ibad AlamNo ratings yet

- 3B 17644019 Proses MeroxDocument1 page3B 17644019 Proses MeroxMohammad Rezza PachruraziNo ratings yet

- Technology, Energy Efficiency and Environmental Externalities in The Pulp and Paper Industry - AIT, ThailandDocument140 pagesTechnology, Energy Efficiency and Environmental Externalities in The Pulp and Paper Industry - AIT, ThailandVishal Duggal100% (1)

- Air Liquide Syngas ProcessDocument1 pageAir Liquide Syngas ProcessAntonio MendesNo ratings yet

- BFD VgoDocument1 pageBFD VgoSALES OFFICER HPCLNo ratings yet

- Layout Zona Pengawasan K3LDocument1 pageLayout Zona Pengawasan K3Lpik.rijalpelangiNo ratings yet

- Overview KilangDocument6 pagesOverview KilangArShyhy Citcuit ArsyamaliaNo ratings yet

- MCR ProjectDocument40 pagesMCR ProjectHumair AhmedNo ratings yet

- Hydroprocessing: Hydrocracking & HydrotreatingDocument45 pagesHydroprocessing: Hydrocracking & HydrotreatingRobin ZwartNo ratings yet

- K131 312 CN 0003 01 - BDocument4 pagesK131 312 CN 0003 01 - BiffatNo ratings yet

- P&ID - EngDocument7 pagesP&ID - EngKanad PNo ratings yet

- Urea Process Split Flow LoopDocument7 pagesUrea Process Split Flow LoopCarlos A. VillanuevaNo ratings yet

- UOP Hydrocracking Technology: Upgrading Fuel Oil To Euro V FuelsDocument37 pagesUOP Hydrocracking Technology: Upgrading Fuel Oil To Euro V FuelsHimanshu Sharma100% (2)

- PFD LPG Limau TimurDocument1 pagePFD LPG Limau TimurwahyuNo ratings yet

- BFD of Lima RefineryDocument1 pageBFD of Lima RefineryMuhammad Ibad Alam100% (1)

- Block Flow Diagram of Lima PDFDocument1 pageBlock Flow Diagram of Lima PDFMuhammad Ibad AlamNo ratings yet

- LAY OUT PIPA CO2 RISE FLOOR Rev.1Document1 pageLAY OUT PIPA CO2 RISE FLOOR Rev.1dyashuntingNo ratings yet

- Project 1Document1 pageProject 1Yasir ShahzadNo ratings yet

- EXPO 2017 Airbus MBSE PDFDocument28 pagesEXPO 2017 Airbus MBSE PDFDebanand SinghdeoNo ratings yet

- Hydroprocessing: Hydrotreating & Hydrocracking: Chapters 7 & 9Document54 pagesHydroprocessing: Hydrotreating & Hydrocracking: Chapters 7 & 9Mo OsNo ratings yet

- 02 Feedstocks & Products PDFDocument124 pages02 Feedstocks & Products PDFdimasNo ratings yet

- Chemistry NoteDocument4 pagesChemistry Notevivektpramod3No ratings yet

- Fwmagpart 2 Q42013Document8 pagesFwmagpart 2 Q42013bourabiaazizNo ratings yet

- Delayed Coking: Chapter 5Document34 pagesDelayed Coking: Chapter 5Arumugam Ramalingam100% (1)

- No Jenis Crude Oil Cutting TBP (%) Gas-Light Gasoline Light Naptha Medium Naptha Heavy Naptha 1 Alc 9 5 8 8 2 Boni LT 9 7 10 10 3 BCF-17 4 1 1 4Document2 pagesNo Jenis Crude Oil Cutting TBP (%) Gas-Light Gasoline Light Naptha Medium Naptha Heavy Naptha 1 Alc 9 5 8 8 2 Boni LT 9 7 10 10 3 BCF-17 4 1 1 4popoNo ratings yet

- PhD. Victor Alva, Conferencia-Hydrocarbon Fundamentals San MarcosDocument62 pagesPhD. Victor Alva, Conferencia-Hydrocarbon Fundamentals San Marcosdaniel100% (1)

- Organic Conversion Ka DadaDocument7 pagesOrganic Conversion Ka Dadaxk71mqnecpNo ratings yet

- Adsorbents Solutions Refining Brochure PDFDocument2 pagesAdsorbents Solutions Refining Brochure PDFSALAM ALINo ratings yet

- HGU, DHT Units OverviewDocument36 pagesHGU, DHT Units OverviewTirumala SaiNo ratings yet

- First Upstream Projects-Epc PlanDocument13 pagesFirst Upstream Projects-Epc PlanRccg DestinySanctuaryNo ratings yet

- Plan of Eletrical PowerDocument3 pagesPlan of Eletrical PoweradventmanurungNo ratings yet

- Learning About The of Nghi Son Refinery: Rude Istillation NitDocument17 pagesLearning About The of Nghi Son Refinery: Rude Istillation NitTrường Tùng LýNo ratings yet

- Power Generation: Product Application NotesDocument6 pagesPower Generation: Product Application NotesmetkarchetanNo ratings yet

- 05 Delayed CokingDocument52 pages05 Delayed CokingRobin ZwartNo ratings yet

- Steam and Water Flow Circuit: Talwandi Sabo Power Limited 3 660Mw ProjectDocument2 pagesSteam and Water Flow Circuit: Talwandi Sabo Power Limited 3 660Mw ProjectHemantNo ratings yet

- 13 - fcc1Document28 pages13 - fcc1ananth2012No ratings yet

- Safety in Operations - Human Aspect - DorcDocument119 pagesSafety in Operations - Human Aspect - DorcAdanenche Daniel Edoh100% (1)

- Abs Sheets University Ar21060Document2 pagesAbs Sheets University Ar21060omkar surveNo ratings yet

- Gas Processing Operations Processing Plants: Prepared By: DSC PHD Dževad Hadžihafizović (Deng) Sarajevo 2024Document78 pagesGas Processing Operations Processing Plants: Prepared By: DSC PHD Dževad Hadžihafizović (Deng) Sarajevo 2024Ambreen SheikhNo ratings yet

- Wahyu Triaji Rahadianto NIM 061540411904 Dosen Pembimbing: Ahmad Zikri, S.T., M.TDocument15 pagesWahyu Triaji Rahadianto NIM 061540411904 Dosen Pembimbing: Ahmad Zikri, S.T., M.TfadilahNo ratings yet

- Pre-Treatment: Distilate HydrotreatingDocument2 pagesPre-Treatment: Distilate HydrotreatingTio BudiartoNo ratings yet

- Praktikum ToksikologiDocument3 pagesPraktikum ToksikologiIin Sakinah DewiNo ratings yet

- LNG Process OverviewDocument59 pagesLNG Process OverviewNhật Quang PhạmNo ratings yet

- PID Ver 1Document1 pagePID Ver 1Gillian AmbaNo ratings yet

- Zero Gasolene Refinery Configuration With SDA (Solvent Deashphaltene)Document9 pagesZero Gasolene Refinery Configuration With SDA (Solvent Deashphaltene)s k kumarNo ratings yet

- P 1 February 01Document1 pageP 1 February 01hlaldinmawiaNo ratings yet

- Roza Savitri - Tugas1Document1 pageRoza Savitri - Tugas1Roza SavitriNo ratings yet

- Imagining the Nation in Nature: Landscape Preservation and German Identity, 1885–1945From EverandImagining the Nation in Nature: Landscape Preservation and German Identity, 1885–1945No ratings yet

- Experiment 5 Chem 26.1Document2 pagesExperiment 5 Chem 26.1Collin Reyes HuelgasNo ratings yet

- Module 20 Reading AssignmentDocument2 pagesModule 20 Reading AssignmentDana M.No ratings yet

- 2014 Organogenesis in A Dish Modeling Development and Disease Using Organoid TechnologiesDocument10 pages2014 Organogenesis in A Dish Modeling Development and Disease Using Organoid TechnologiesDito AnurogoNo ratings yet

- Photosynthesis and The Carbon Cycle: Lower Secondary Checkpoint Year 8Document20 pagesPhotosynthesis and The Carbon Cycle: Lower Secondary Checkpoint Year 8Youssef MohamedNo ratings yet

- Anthesia Answer 2Document14 pagesAnthesia Answer 2Hamdy GowefilNo ratings yet

- IC Accounts Payable Ledger Template Updated 8552Document2 pagesIC Accounts Payable Ledger Template Updated 8552M Monjur MobinNo ratings yet

- Transport Safety Management (RR)Document16 pagesTransport Safety Management (RR)Andriy ShevaNo ratings yet

- The Effects of A Mobile Application For Patient Participation To Improve Patient SafetyDocument18 pagesThe Effects of A Mobile Application For Patient Participation To Improve Patient Safety'Amel'AyuRizkyAmeliyahNo ratings yet

- Comprehensive Neurology Board Review Flash CardsDocument202 pagesComprehensive Neurology Board Review Flash CardsDr. Chaim B. Colen78% (9)

- Elementary Firs AidDocument56 pagesElementary Firs AidSaptarshi BasuNo ratings yet

- Fit 111 Contents and Assessments (2)Document60 pagesFit 111 Contents and Assessments (2)quentkarl8No ratings yet

- 5 Rhenocure TMTD CDocument3 pages5 Rhenocure TMTD CKeremNo ratings yet

- Jfe 680Document94 pagesJfe 680harbhajan singhNo ratings yet

- Horizon Power Testing and Commissioning Manual PDFDocument78 pagesHorizon Power Testing and Commissioning Manual PDFmasimaha1379No ratings yet

- Calculations For Safe Bearing CapacityDocument3 pagesCalculations For Safe Bearing Capacityimran khanNo ratings yet

- Physioex Lab Report: Pre-Lab Quiz ResultsDocument5 pagesPhysioex Lab Report: Pre-Lab Quiz ResultsPavel Milenkovski100% (1)

- Bread and Pastry Production (Exploratory) : I. Introductory ConceptDocument3 pagesBread and Pastry Production (Exploratory) : I. Introductory ConceptJonaiza PangandianNo ratings yet

- Entropy EdexcelDocument6 pagesEntropy EdexcelKevin The Chemistry TutorNo ratings yet

- National Cheese Pizza DayDocument64 pagesNational Cheese Pizza Day018-2A Liensi PutriNo ratings yet

- Smart Walking Stick For Visually ImpairedDocument16 pagesSmart Walking Stick For Visually ImpairedAshwati Joshi100% (1)

- High Profits by Producing EggsDocument12 pagesHigh Profits by Producing EggsDonasian Mbonea Elisante MjemaNo ratings yet

- PHD Review LiteratureDocument27 pagesPHD Review LiteraturesalmanNo ratings yet

- Exercises Developing or Displaying Physical Agility and CoordinationDocument24 pagesExercises Developing or Displaying Physical Agility and CoordinationJhun PobleteNo ratings yet

- Effortless English: Lifestyle DiseasesDocument2 pagesEffortless English: Lifestyle DiseasesPedro De Oliveira AguiarNo ratings yet

- TBoxMS Technical Specification 2.15Document123 pagesTBoxMS Technical Specification 2.15eftamargoNo ratings yet

- Final Examination Rubric On The Zumba Exercises RoutineDocument1 pageFinal Examination Rubric On The Zumba Exercises RoutinePizzaTobacco123100% (1)

- आदिवासी PDFDocument122 pagesआदिवासी PDFSunNo ratings yet