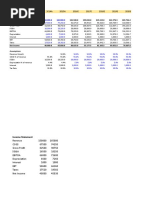

Cost Allocation To Divisions

Cost Allocation To Divisions

Download as docx, pdf, or txt

You might also like

- Case 5Document12 pagesCase 5JIAXUAN WANGNo ratings yet

- Finm1416 Individual Compenent 4Document5 pagesFinm1416 Individual Compenent 4Ma HiNo ratings yet

- Nandita Summers Works at ModusDocument3 pagesNandita Summers Works at ModusElliot RichardNo ratings yet

- The Central Valley Company Has Prepared Department Overhead Budgets For BudgetedDocument4 pagesThe Central Valley Company Has Prepared Department Overhead Budgets For BudgetedElliot RichardNo ratings yet

- The IVplast Corporation Uses An Injection Molding Machine To Make A Plastic ProductDocument2 pagesThe IVplast Corporation Uses An Injection Molding Machine To Make A Plastic ProductElliot RichardNo ratings yet

- IProtect Produces Covers For All Makes and Models of IPadsDocument2 pagesIProtect Produces Covers For All Makes and Models of IPadsElliot Richard0% (1)

- Regression Line of Overhead Costs On LaborDocument3 pagesRegression Line of Overhead Costs On LaborElliot Richard100% (1)

- Session 7 - Cost Allocation - Canvas - TeachingDocument57 pagesSession 7 - Cost Allocation - Canvas - Teaching長長No ratings yet

- Financial StatementDocument36 pagesFinancial StatementJigoku ShojuNo ratings yet

- Discounted Cash Flows at WACCDocument11 pagesDiscounted Cash Flows at WACCapi-15357496No ratings yet

- Fatima FertilizersDocument18 pagesFatima FertilizersBarira AkhtarNo ratings yet

- ABC Financial AnalysisDocument22 pagesABC Financial AnalysisDR.TATA FON EMMANUELNo ratings yet

- Revenue Projection:: 47.6 Accounts Receivable 37.6 Inventory Accounts PayableDocument8 pagesRevenue Projection:: 47.6 Accounts Receivable 37.6 Inventory Accounts Payablesaqibriaz8771No ratings yet

- hitungan quiz 6 dan 7Document26 pageshitungan quiz 6 dan 7Christina IndrawatiNo ratings yet

- Fin 600 - Radio One-Team 3 - Final SlidesDocument20 pagesFin 600 - Radio One-Team 3 - Final SlidesCarlosNo ratings yet

- 2008-2-00474-TI LampiranDocument3 pages2008-2-00474-TI LampiranMuhamad AzwarNo ratings yet

- Apartment Excel AnalysisDocument234 pagesApartment Excel AnalysisCeline TeeNo ratings yet

- JaletaDocument8 pagesJaletaአረጋዊ ሐይለማርያምNo ratings yet

- AFS (Word File)Document7 pagesAFS (Word File)HussainNo ratings yet

- Income Based Valuation Unit Exam Answer Key NewDocument6 pagesIncome Based Valuation Unit Exam Answer Key NewAMIKO OHYANo ratings yet

- Enterprise ValuationDocument3 pagesEnterprise ValuationParth MalikNo ratings yet

- Current Year Data:: Calculating Enterprise ValueDocument3 pagesCurrent Year Data:: Calculating Enterprise ValueParth MalikNo ratings yet

- Advisory Finance Week 11Document6 pagesAdvisory Finance Week 11atilatoplaneNo ratings yet

- 2024 Apr - Palma Real Lot Only ComputationDocument1 page2024 Apr - Palma Real Lot Only ComputationsapunganljoyNo ratings yet

- FM 2 AssignmentDocument4 pagesFM 2 AssignmentTestNo ratings yet

- 2014A 2015A 2016E 2017E 2018E 2019E 2020E: Income Statement Revenue 181,500.0 199,650.0 219,615.0 241,576.5 265,734.2Document2 pages2014A 2015A 2016E 2017E 2018E 2019E 2020E: Income Statement Revenue 181,500.0 199,650.0 219,615.0 241,576.5 265,734.2raskaNo ratings yet

- Aplg 2014Document25 pagesAplg 2014api-53711077No ratings yet

- Criterion Weight Word In-House Press Financial Third PartyDocument9 pagesCriterion Weight Word In-House Press Financial Third PartyArdia salsabilaNo ratings yet

- Financial Analysis ModelDocument5 pagesFinancial Analysis ModelShanaya JainNo ratings yet

- CF Hansson 23P254 Akash BhandariDocument7 pagesCF Hansson 23P254 Akash Bhandaribiju.mahapatra23No ratings yet

- Income Tax Computation OptionsDocument2 pagesIncome Tax Computation OptionsSHIRLYNo ratings yet

- Advanced Corporate Finance Case 2Document3 pagesAdvanced Corporate Finance Case 2Adrien PortemontNo ratings yet

- Total PHP 5,200,000 PHP 5,200,000 Table 5.1.22 Salaries ExpenseDocument3 pagesTotal PHP 5,200,000 PHP 5,200,000 Table 5.1.22 Salaries Expenserjay manaloNo ratings yet

- J and J Medical ClinicDocument17 pagesJ and J Medical ClinicHarold Kent MendozaNo ratings yet

- Essay FIN202Document5 pagesEssay FIN202thaindnds180468No ratings yet

- FM Assaignment Second SemisterDocument9 pagesFM Assaignment Second SemisterMotuma Abebe100% (1)

- Amway New PlanDocument19 pagesAmway New PlanPradipNo ratings yet

- Amway New Plan Sep 2019Document22 pagesAmway New Plan Sep 2019PradipNo ratings yet

- Team Kingdom of Mesopotamia - Round 1Document4 pagesTeam Kingdom of Mesopotamia - Round 1KapishNo ratings yet

- HDocument8 pagesHvipul_malhotra_3No ratings yet

- Manisha Haldar - The Fashion Channel IIMT 2019 Student WorksheetDocument2 pagesManisha Haldar - The Fashion Channel IIMT 2019 Student WorksheetyyyNo ratings yet

- Book1Document2 pagesBook1Amadou MokshaNo ratings yet

- Financial ModelingDocument4 pagesFinancial ModelingUsha KarkiNo ratings yet

- Answer Exercise567Document4 pagesAnswer Exercise567khang300705No ratings yet

- Cosmetic SolutionDocument1 pageCosmetic SolutionpoggiolilaureNo ratings yet

- Axisbank Financial Statements Summary AJ WorksDocument12 pagesAxisbank Financial Statements Summary AJ WorksSoorajKrishnanNo ratings yet

- Activity 2 MIlca BSA 3 3Document6 pagesActivity 2 MIlca BSA 3 3kyrie IrvingNo ratings yet

- Puma R To L 2020 Master 3 PublishDocument8 pagesPuma R To L 2020 Master 3 PublishIulii IuliikkNo ratings yet

- Ms. Excel International Brews: Income StatementDocument9 pagesMs. Excel International Brews: Income StatementAphol Joyce MortelNo ratings yet

- Bank A and B - Bank XDocument4 pagesBank A and B - Bank XSoleil SierraNo ratings yet

- NPV IRR CalculatorDocument3 pagesNPV IRR CalculatorAli TekinNo ratings yet

- Cortez Exam in Business FinanceDocument4 pagesCortez Exam in Business FinanceFranchesca CortezNo ratings yet

- Financial AnalysisDocument9 pagesFinancial AnalysisSam SumoNo ratings yet

- Excel Crash Course - Book1 - Blank: Strictly ConfidentialDocument4 pagesExcel Crash Course - Book1 - Blank: Strictly ConfidentialtehreemNo ratings yet

- Financial StatementsDocument10 pagesFinancial StatementsAirah MondonedoNo ratings yet

- Scenario Summary: Changing CellsDocument10 pagesScenario Summary: Changing Cellsjerrynguyen291No ratings yet

- 1.1 - Whatif &PTDocument28 pages1.1 - Whatif &PTSalman AhmadNo ratings yet

- Claim Balai Harta (Perhitungan) 3Document14 pagesClaim Balai Harta (Perhitungan) 3hari natoNo ratings yet

- Scenario Summary: Changing Cells: Result CellsDocument9 pagesScenario Summary: Changing Cells: Result CellsatpugajoopNo ratings yet

- Cost ModellingDocument10 pagesCost ModellingRESMITA DASNo ratings yet

- Excel Crash Course - Book1 - Complete: Strictly ConfidentialDocument5 pagesExcel Crash Course - Book1 - Complete: Strictly ConfidentialGaurav KumarNo ratings yet

- Copy of ANS Basic Decision Making With Spreadsheet_B TECH MBA TECH_30.04.2024(TEE_Synoptics_Set1_2324) (1)Document14 pagesCopy of ANS Basic Decision Making With Spreadsheet_B TECH MBA TECH_30.04.2024(TEE_Synoptics_Set1_2324) (1)siddhantpatil560No ratings yet

- CiplaDocument9 pagesCiplaShivam GoelNo ratings yet

- Itemized: Gross Income From OperationsDocument9 pagesItemized: Gross Income From OperationsLyka RoguelNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionNo ratings yet

- Prescott Manufacturing Evaluates The Performance of Its Production Managers Based On A Variety of FactorsDocument3 pagesPrescott Manufacturing Evaluates The Performance of Its Production Managers Based On A Variety of FactorsElliot RichardNo ratings yet

- Description (1) Amount (2) Percentage of Total COQ (3) (2) ÷ $1,820,000 Percentage of Revenues (4) (2) ÷ $45,000,000Document3 pagesDescription (1) Amount (2) Percentage of Total COQ (3) (2) ÷ $1,820,000 Percentage of Revenues (4) (2) ÷ $45,000,000Elliot RichardNo ratings yet

- This Question Asks Which of A Series of Statements With Respect To Quality Control IsDocument2 pagesThis Question Asks Which of A Series of Statements With Respect To Quality Control IsElliot RichardNo ratings yet

- Average Waiting Time For An Order of Z39Document2 pagesAverage Waiting Time For An Order of Z39Elliot RichardNo ratings yet

- Give Two Examples of Appraisal CostsDocument1 pageGive Two Examples of Appraisal CostsElliot RichardNo ratings yet

- The Brandt Corporation Makes Wire Harnesses For The Aircraft Industry Only Upon Receiving Firm Orders From Its CustomersDocument3 pagesThe Brandt Corporation Makes Wire Harnesses For The Aircraft Industry Only Upon Receiving Firm Orders From Its CustomersElliot RichardNo ratings yet

- Chunky Meatbots Produces A Wide Variety of Unorthodox Bread SaucesDocument3 pagesChunky Meatbots Produces A Wide Variety of Unorthodox Bread SaucesElliot RichardNo ratings yet

- To Determine How Much QwakSoda Corporation Is Worse Off by Producing A Defective Bottle in The Bottling DepartmentDocument2 pagesTo Determine How Much QwakSoda Corporation Is Worse Off by Producing A Defective Bottle in The Bottling DepartmentElliot RichardNo ratings yet

- The Brightlight Corporation Uses Multicolored Molding To Make Plastic LampsDocument2 pagesThe Brightlight Corporation Uses Multicolored Molding To Make Plastic LampsElliot RichardNo ratings yet

- IVplast Is Still Debating Whether It Should Introduce Y28Document2 pagesIVplast Is Still Debating Whether It Should Introduce Y28Elliot RichardNo ratings yet

- Calculate The Average Waiting Time Per OrderDocument3 pagesCalculate The Average Waiting Time Per OrderElliot RichardNo ratings yet

- The Tristan Corporation Sells 250Document2 pagesThe Tristan Corporation Sells 250Elliot RichardNo ratings yet

- At 420 Students Seen A DayDocument2 pagesAt 420 Students Seen A DayElliot RichardNo ratings yet

- Weston Corporation Manufactures Auto Parts For Two Leading Japanese AutomakersDocument2 pagesWeston Corporation Manufactures Auto Parts For Two Leading Japanese AutomakersElliot RichardNo ratings yet

- Because The Expected Relevant Benefits ofDocument2 pagesBecause The Expected Relevant Benefits ofElliot RichardNo ratings yet

- Plots and Regression Lines ForDocument2 pagesPlots and Regression Lines ForElliot RichardNo ratings yet

- QwakSoda Corporation Makes Soda in Three DepartmentsDocument2 pagesQwakSoda Corporation Makes Soda in Three DepartmentsElliot RichardNo ratings yet

- Describe Two Benefits of Improving QualityDocument1 pageDescribe Two Benefits of Improving QualityElliot RichardNo ratings yet

- Calculus Company Makes Calculators For StudentsDocument2 pagesCalculus Company Makes Calculators For StudentsElliot RichardNo ratings yet

- Which Basis of Allocation Makes The Most Sense in This SituationDocument2 pagesWhich Basis of Allocation Makes The Most Sense in This SituationElliot RichardNo ratings yet

- KidsTravel Produces Car Seats For Children From Newborn To 2 Years OldDocument2 pagesKidsTravel Produces Car Seats For Children From Newborn To 2 Years OldElliot Richard0% (1)

- Preston Department Store Has A New Promotional Program That Offers A Free GiftDocument3 pagesPreston Department Store Has A New Promotional Program That Offers A Free GiftElliot RichardNo ratings yet

- Terry LawlerDocument2 pagesTerry LawlerElliot RichardNo ratings yet

- Possible Alternative Specifications That Would Better Capture The Link Between SpiritDocument2 pagesPossible Alternative Specifications That Would Better Capture The Link Between SpiritElliot RichardNo ratings yet

- Essence Company Blends and Sells Designer FragrancesDocument2 pagesEssence Company Blends and Sells Designer FragrancesElliot Richard100% (1)

- Transfer ReceiptDocument2 pagesTransfer Receiptkimhendricks187No ratings yet

- Cheng Kate Hoi Yiu CV (SBMT)Document2 pagesCheng Kate Hoi Yiu CV (SBMT)26w2ww7j9pNo ratings yet

- Statement of Comprehensive Income - Ia3Document16 pagesStatement of Comprehensive Income - Ia3SharjaaahNo ratings yet

- AB 2343 Analysis: Strengthening Tenant Rights in Eviction Cases (A.Lew)Document10 pagesAB 2343 Analysis: Strengthening Tenant Rights in Eviction Cases (A.Lew)Anthony LewNo ratings yet

- Artificial Sand - A Viable Alternative: An Alternate To River Sand in Concrete and Construction IndustryDocument64 pagesArtificial Sand - A Viable Alternative: An Alternate To River Sand in Concrete and Construction IndustrySimon DaudaNo ratings yet

- Hindustan Unilever LTD: Meeting Employee Expectations: Section - B Group - 10Document8 pagesHindustan Unilever LTD: Meeting Employee Expectations: Section - B Group - 10tanyaNo ratings yet

- 02 The Nature of BusinessDocument3 pages02 The Nature of BusinessCharisse Aro YcongNo ratings yet

- Theorizing Through Literature Reviews: The Miner-Prospector ContinuumDocument29 pagesTheorizing Through Literature Reviews: The Miner-Prospector ContinuumFernando FLNo ratings yet

- Companies in PuneDocument6 pagesCompanies in PuneaitcpurchaseNo ratings yet

- Bharti Airtel Annual Report 2009 10Document172 pagesBharti Airtel Annual Report 2009 10narin_19910% (1)

- Church Corporations Sole - Corporation SolesDocument6 pagesChurch Corporations Sole - Corporation SolesMenjetu33% (3)

- Introduction To TaxationDocument32 pagesIntroduction To TaxationAFIFAH NATASYA MOHD GHAZALINo ratings yet

- 23 Feb ACC 2Document2 pages23 Feb ACC 2Delia LeeNo ratings yet

- Product Info: Innovative Automation Solutions For Textile Fi NishingDocument20 pagesProduct Info: Innovative Automation Solutions For Textile Fi NishingTahir SamadNo ratings yet

- Entrepreneurship in Computer Hardware Servicing (CHS)Document3 pagesEntrepreneurship in Computer Hardware Servicing (CHS)EDMAR POLVOROZANo ratings yet

- Personal Taxation QuestionDocument2 pagesPersonal Taxation QuestionNORZAFIRAH BINTI YUSAININo ratings yet

- Understanding The Benefits and Success Factors of Enterprise ArchitectureDocument10 pagesUnderstanding The Benefits and Success Factors of Enterprise ArchitectureAljan VillosaNo ratings yet

- Big Data ExecutiveSummary2021Document15 pagesBig Data ExecutiveSummary2021DMS APACNo ratings yet

- Test Bank: Risk Return AnalysisDocument2 pagesTest Bank: Risk Return AnalysisSatyam Dixit100% (1)

- FABM 2 Module 9 Income Tax DueDocument11 pagesFABM 2 Module 9 Income Tax DueJOHN PAUL LAGAO100% (2)

- Informatique Mpsi Pcsi Ptsi Tsi MP TPC PC PT PSI 1st Edition Nicolas Audfray Jean Loup Carré Stéphane Legros Vojislav Petrov Marc RezzoukDocument15 pagesInformatique Mpsi Pcsi Ptsi Tsi MP TPC PC PT PSI 1st Edition Nicolas Audfray Jean Loup Carré Stéphane Legros Vojislav Petrov Marc Rezzoukkiwinirisca100% (2)

- Conclusion and Reporting PDFDocument7 pagesConclusion and Reporting PDFRhn Habib RehmanNo ratings yet

- How To Identify Turning PointsDocument11 pagesHow To Identify Turning Pointsceloki5867No ratings yet

- Bcta Advanced Financial Reporting Module 2024-3Document214 pagesBcta Advanced Financial Reporting Module 2024-3annah100% (1)

- An Overview On BFIU Circulars and AML & CFT Acts: William ChowdhuryDocument34 pagesAn Overview On BFIU Circulars and AML & CFT Acts: William ChowdhuryShuvonath100% (1)

- Practice Problem Set #6: Stocks I Theoretical and Conceptual Questions: (See Notes or Textbook For Solutions)Document2 pagesPractice Problem Set #6: Stocks I Theoretical and Conceptual Questions: (See Notes or Textbook For Solutions)raymondNo ratings yet

- Credit Repair SolutionsDocument6 pagesCredit Repair SolutionsCarolNo ratings yet

- Forain Filter To PLTUDocument1 pageForain Filter To PLTUposmarichardNo ratings yet

- 1city of Manila V Estrada - Right To Just Compensation, Just CompensationDocument1 page1city of Manila V Estrada - Right To Just Compensation, Just CompensationIanNo ratings yet

- Entrepreneurship Lecture Notes Part 1Document9 pagesEntrepreneurship Lecture Notes Part 1Peter100% (1)