Business Examples 2021

Business Examples 2021

Download as pdf or txt

You might also like

- Final Accounts SumDocument2 pagesFinal Accounts SumRohit Aswani25% (4)

- TAX 667 TOPIC 7 Trade Association & ClubsDocument51 pagesTAX 667 TOPIC 7 Trade Association & Clubszarif nezuko100% (2)

- Business PlanDocument19 pagesBusiness PlanSimona PatrascuNo ratings yet

- 01 - FINC 0200 IP - Assignment Units 1 - 6 Questions - Winter 2022Document6 pages01 - FINC 0200 IP - Assignment Units 1 - 6 Questions - Winter 2022hermitpassiNo ratings yet

- Topic 3 Tutorial Questions PDFDocument15 pagesTopic 3 Tutorial Questions PDFKim FloresNo ratings yet

- Advance Tax FullDocument5 pagesAdvance Tax FullParthiban BanNo ratings yet

- Compre Audit Cieloflawless Q PDFDocument3 pagesCompre Audit Cieloflawless Q PDFCarina Mae Valdez ValenciaNo ratings yet

- Trial Balance Adjustments Profit or Loss Financial Position Account Title Debit Credit Debit Credit Debit Credit Debit CreditDocument2 pagesTrial Balance Adjustments Profit or Loss Financial Position Account Title Debit Credit Debit Credit Debit Credit Debit CreditMichelle BabaNo ratings yet

- Accounting TestDocument4 pagesAccounting Testdinda ardiyaniNo ratings yet

- Retained Earning Opening Balance - Net Income For The Year Ended 2017 2370 Dividend Paid (2,500)Document21 pagesRetained Earning Opening Balance - Net Income For The Year Ended 2017 2370 Dividend Paid (2,500)Umar Razi QasimNo ratings yet

- Assignment-5-Single-Entry-Method-students-DAVID FinalDocument11 pagesAssignment-5-Single-Entry-Method-students-DAVID FinalJOY MARIE RONATONo ratings yet

- Income Tax Revision QuestionsDocument13 pagesIncome Tax Revision QuestionsMbeiza MariamNo ratings yet

- Financial Statement Assignment 1Document3 pagesFinancial Statement Assignment 1tahasafdari772No ratings yet

- Final Activity 3 QuestionDocument2 pagesFinal Activity 3 QuestionSze ChristienyNo ratings yet

- Af 314 Corporate Accounting FLEXI-SCHOOL: 2022 Individual AssignmentDocument6 pagesAf 314 Corporate Accounting FLEXI-SCHOOL: 2022 Individual AssignmentShiv AchariNo ratings yet

- Lt234. Tvp. (Il-II) Solution Cma May-2023 Exam.Document5 pagesLt234. Tvp. (Il-II) Solution Cma May-2023 Exam.Arif HossainNo ratings yet

- IAS 1 TutorialsDocument3 pagesIAS 1 Tutorialsmosesnation43No ratings yet

- Westmont PLCDocument5 pagesWestmont PLCmutuamutisya306No ratings yet

- Team Criminal NuisanceDocument4 pagesTeam Criminal NuisanceShreya ShrivastavaNo ratings yet

- Ferrari Group CaseDocument11 pagesFerrari Group Casemkdhali526No ratings yet

- Accounts Practice ProblemsDocument45 pagesAccounts Practice Problemsloveumona1970No ratings yet

- Cash Flow Statement (BBA-H)Document5 pagesCash Flow Statement (BBA-H)asiharry037No ratings yet

- Financial Analysis ProblemDocument16 pagesFinancial Analysis ProblemShreyashi DasNo ratings yet

- AccountsDocument4 pagesAccountsVencint LaranNo ratings yet

- Chapter-1 Homework Basic Concepts Part 1Document4 pagesChapter-1 Homework Basic Concepts Part 1Kenneth Christian WilburNo ratings yet

- Ast 2.1Document5 pagesAst 2.1Patrick Alvin100% (1)

- Final PDFDocument4 pagesFinal PDFNirranjana shreeNo ratings yet

- Abdul Ghaffar F2020277002 (Assigment#2)Document3 pagesAbdul Ghaffar F2020277002 (Assigment#2)MUDASSAR ZEESHANNo ratings yet

- Cash Flow Excercise Questions-Set-2Document2 pagesCash Flow Excercise Questions-Set-2AgANo ratings yet

- ISSo FPDocument6 pagesISSo FPabbeangedesireNo ratings yet

- MOJAKOE AK1 UTS 2012 GasalDocument15 pagesMOJAKOE AK1 UTS 2012 GasalVincenttio le CloudNo ratings yet

- Statement of Financial PositionDocument3 pagesStatement of Financial PositionMaxine Shia TyNo ratings yet

- Business Income TutorialDocument5 pagesBusiness Income TutorialzulfikriNo ratings yet

- Fimd Training Unit 1 - Financial Analysis-ActivitiesDocument8 pagesFimd Training Unit 1 - Financial Analysis-ActivitiesErrol ThompsonNo ratings yet

- BSBFIN401 Assessment 3Document6 pagesBSBFIN401 Assessment 3Kitpipoj PornnongsaenNo ratings yet

- Taxation Mid 2 Solution NUBDocument4 pagesTaxation Mid 2 Solution NUBNiizamUddinBhuiyanNo ratings yet

- Mellisa O'Connor Statement of Profit or Loss For Year Ended March 31, 2016 $ $ $Document3 pagesMellisa O'Connor Statement of Profit or Loss For Year Ended March 31, 2016 $ $ $Debbie DebzNo ratings yet

- Book 1Document6 pagesBook 1chrstncstlljNo ratings yet

- Karkits Corporation Excel Copy PasteDocument2 pagesKarkits Corporation Excel Copy PasteCoke Aidenry SaludoNo ratings yet

- Qau Memo 2019-03. Pfrs 16 Leases Annex A EntriesDocument2 pagesQau Memo 2019-03. Pfrs 16 Leases Annex A EntriesMikx LeeNo ratings yet

- ACCY200, Autumn, 2011 Past Exam QuestionsDocument21 pagesACCY200, Autumn, 2011 Past Exam QuestionsJohn TomNo ratings yet

- Chapter Seventeen IA3Document4 pagesChapter Seventeen IA3Hania M. CalandadaNo ratings yet

- Schedule 3Document8 pagesSchedule 3Hilary GaureaNo ratings yet

- Accounting Assignment Q-4Document5 pagesAccounting Assignment Q-4Ueamraan MartNo ratings yet

- Viray, Nhicole S. Asynchronous Quiz 2 - Accounting Changes and ErrorsDocument5 pagesViray, Nhicole S. Asynchronous Quiz 2 - Accounting Changes and ErrorsZeeNo ratings yet

- 01 Basic Audit AdjustmentsDocument3 pages01 Basic Audit AdjustmentslyannaairalacostalesNo ratings yet

- A211 MC 2 - StudentDocument6 pagesA211 MC 2 - StudentWon HaNo ratings yet

- Simple Final Accounts Past Paper Solutions Q # 1 & 3 & 7Document11 pagesSimple Final Accounts Past Paper Solutions Q # 1 & 3 & 7Masood Ahmad AadamNo ratings yet

- Advanced Taxation QuestionsDocument5 pagesAdvanced Taxation QuestionsMagoha GeofreyNo ratings yet

- 8447809Document11 pages8447809blackghostNo ratings yet

- Trial BalanceDocument4 pagesTrial BalanceRonnie Lloyd JavierNo ratings yet

- Special Liabilities - Income Taxes: Income Tax Rate Is 40% and Is Not Expected To Change in The FutureDocument5 pagesSpecial Liabilities - Income Taxes: Income Tax Rate Is 40% and Is Not Expected To Change in The FutureClarisse AlimotNo ratings yet

- Solution NIngDocument3 pagesSolution NIngfahim tusarNo ratings yet

- Handouts - CHAPTER 4-3 - ACC117Document3 pagesHandouts - CHAPTER 4-3 - ACC117taerrybombNo ratings yet

- Review Accounting 1Document9 pagesReview Accounting 1jhouvanNo ratings yet

- Item (A) Type of Adjustment (B) Accounts Before AdjustmentDocument11 pagesItem (A) Type of Adjustment (B) Accounts Before Adjustmentsuci monalia putriNo ratings yet

- Corporate Financial Reporting PDFDocument3 pagesCorporate Financial Reporting PDFIshan SharmaNo ratings yet

- Feu Fundact 2 Reviewer 2Document40 pagesFeu Fundact 2 Reviewer 2anneNo ratings yet

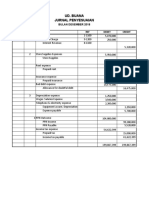

- Ud. Buana Jurnal Penyesuaian: Bulan Desember 2018 TGL REF Debet CreditDocument1 pageUd. Buana Jurnal Penyesuaian: Bulan Desember 2018 TGL REF Debet Creditangelina putriNo ratings yet

- Akuntansi Keuangan Menengah 2 Asistensi - Tim Asdos Akm 2Document2 pagesAkuntansi Keuangan Menengah 2 Asistensi - Tim Asdos Akm 2Muhamad Rizal DinyatNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- TAX.3503 Sources of IncomeDocument4 pagesTAX.3503 Sources of IncomeMarinoNo ratings yet

- RESA TAX PreWeek (B43)Document23 pagesRESA TAX PreWeek (B43)MellaniNo ratings yet

- 2307 012023 FlashDocument2 pages2307 012023 FlashGregorio LSNo ratings yet

- Banking Academy: Assignment Financial Statement AnalysisDocument25 pagesBanking Academy: Assignment Financial Statement AnalysisDiệp NguyễnNo ratings yet

- Acca f6 Taxation Vietnam 2012 Jun QuestionDocument12 pagesAcca f6 Taxation Vietnam 2012 Jun QuestionNguyễn GiangNo ratings yet

- Manila Bulletin Publishing Corporation Sec Form 17a 2018Document128 pagesManila Bulletin Publishing Corporation Sec Form 17a 2018Kathryn SantosNo ratings yet

- Philippine Income Taxation For Basic KnowledgeDocument8 pagesPhilippine Income Taxation For Basic KnowledgeAnonymous BvmMuBSwNo ratings yet

- Advance I Ch-IDocument61 pagesAdvance I Ch-IBamlak WenduNo ratings yet

- Entrep Q2 SLM Lesson-4Document5 pagesEntrep Q2 SLM Lesson-4lol nope.No ratings yet

- Tax Reviewer: Law of Basic Taxation in The Philippines Chapter 2: Limitations On The Taxing PowerDocument10 pagesTax Reviewer: Law of Basic Taxation in The Philippines Chapter 2: Limitations On The Taxing Powernewa944No ratings yet

- Informe Ingles Auditoria IntegralDocument9 pagesInforme Ingles Auditoria IntegralEmy FaraNo ratings yet

- Rental Property Investment AnalysisDocument23 pagesRental Property Investment Analysissam100% (1)

- Suraj Sir 1Document8 pagesSuraj Sir 1Avinash YadavNo ratings yet

- MCIT, IAET Handouts Oct 2019Document13 pagesMCIT, IAET Handouts Oct 2019Elsie GenovaNo ratings yet

- BIR Form 2322 Cert of Don - FG Calderon High SchoolDocument3 pagesBIR Form 2322 Cert of Don - FG Calderon High SchoolEdmund G. VillarealNo ratings yet

- 2 Corporation-RevisedDocument8 pages2 Corporation-RevisedSamantha Nicole Hoy100% (2)

- PDF Income Taxation Ampongan SolmanDocument25 pagesPDF Income Taxation Ampongan SolmanDennis AlarconNo ratings yet

- BAM031 P3 Q1 Answer FBT DeductionsDocument12 pagesBAM031 P3 Q1 Answer FBT DeductionsMary Lyn DatuinNo ratings yet

- RMC No. 62-2021Document4 pagesRMC No. 62-2021Mark Ace SubidoNo ratings yet

- 2 Easy Questions - AnswersDocument9 pages2 Easy Questions - AnswersMarj AgustinNo ratings yet

- Chapter 3 IncometaxDocument20 pagesChapter 3 IncometaxLouella CunananNo ratings yet

- Blank Quiz: Activity 3 For Modules 4, 5 and 6Document6 pagesBlank Quiz: Activity 3 For Modules 4, 5 and 6Sevastian jedd EdicNo ratings yet

- Income and Business TaxationDocument138 pagesIncome and Business Taxationjustine reine cornico100% (1)

- Churchill vs. Concepcion, 34 Phil. 969Document6 pagesChurchill vs. Concepcion, 34 Phil. 969Machida AbrahamNo ratings yet

- CTA 8459 (CADPI) - No DST On Bank Loans, Year-End BalanceDocument74 pagesCTA 8459 (CADPI) - No DST On Bank Loans, Year-End BalanceJerwin DaveNo ratings yet

- Oing Business in GuatemalaDocument16 pagesOing Business in GuatemalaJorge Luis Can MonroyNo ratings yet

- WT Tax RatesDocument2 pagesWT Tax RatesericbacsalNo ratings yet