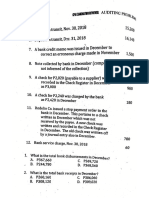

FAR 1 Reviewer

FAR 1 Reviewer

Download as docx, pdf, or txt

You might also like

- 3rd ActivityDocument2 pages3rd Activitydar •No ratings yet

- Answer The Following Questions and Provide The Necessary RequirementsDocument11 pagesAnswer The Following Questions and Provide The Necessary RequirementsKervin Rey JacksonNo ratings yet

- Physical Science: Quarter 3 - Module 7: Energy SourcesDocument16 pagesPhysical Science: Quarter 3 - Module 7: Energy SourcesFRECY MARZAN100% (4)

- Chapters 10 and 11Document51 pagesChapters 10 and 11Carlos VillanuevaNo ratings yet

- Variable Costing ReviewerDocument3 pagesVariable Costing Reviewerdaniellejueco1228No ratings yet

- Property, Plant and EquipmentDocument40 pagesProperty, Plant and EquipmentNatalie SerranoNo ratings yet

- 5Document11 pages5shayn delapenaNo ratings yet

- Mas 9303 - Standard Costs and Variance AnalysisDocument21 pagesMas 9303 - Standard Costs and Variance AnalysisJowel BernabeNo ratings yet

- Cash & Cash Equivalent: If The Problem Is Silent, Daily, They Are Part of Cash and Cash EquivalentsDocument30 pagesCash & Cash Equivalent: If The Problem Is Silent, Daily, They Are Part of Cash and Cash EquivalentsKim Audrey JalalainNo ratings yet

- Module 8 - Inventories Part IDocument12 pagesModule 8 - Inventories Part IMark Christian BrlNo ratings yet

- 20-1 To 20-13Document16 pages20-1 To 20-13Jesica Vargas0% (2)

- Exercise 1: Required: Classify The Reports in Part A-E Into One of The Three Major Purposes of Accounting Systems OnDocument2 pagesExercise 1: Required: Classify The Reports in Part A-E Into One of The Three Major Purposes of Accounting Systems OnMyunimintNo ratings yet

- Sol. Man. - Chapter 3 - Bank Reconciliation - Ia Part 1aDocument16 pagesSol. Man. - Chapter 3 - Bank Reconciliation - Ia Part 1aMiguel AmihanNo ratings yet

- FAR 2 Q2 - Sample Problems With Solutions - FOR EMAILDocument11 pagesFAR 2 Q2 - Sample Problems With Solutions - FOR EMAILJoyce Anne GarduqueNo ratings yet

- 21 Financial Assets at Fair Value: Solution 21-1 Answer CDocument30 pages21 Financial Assets at Fair Value: Solution 21-1 Answer CLayNo ratings yet

- MiyawwDocument9 pagesMiyawwjessa mae zerdaNo ratings yet

- Prelim Exam Accounting 2Document3 pagesPrelim Exam Accounting 2JM Singco Canoy100% (1)

- PPE Part 1 ModuleDocument11 pagesPPE Part 1 ModuleNatalie SerranoNo ratings yet

- Partnership Dissolution 3Document10 pagesPartnership Dissolution 3Jamaica RumaNo ratings yet

- Problem 14-5: Kayla Cruz & Gabriel TekikoDocument7 pagesProblem 14-5: Kayla Cruz & Gabriel TekikoNURHAM SUMLAYNo ratings yet

- Chapter 28Document6 pagesChapter 28Shane Ivory ClaudioNo ratings yet

- Handout - CashDocument17 pagesHandout - CashPenelope PalconNo ratings yet

- Finman 01 Short-Term FinancingDocument13 pagesFinman 01 Short-Term FinancingDoromal, Jerome A.No ratings yet

- Chapter 3 (IA Proof Od Cash) PDFDocument6 pagesChapter 3 (IA Proof Od Cash) PDFBaby MushroomNo ratings yet

- FAR04-08 - Government Grant & Borrowing CostsDocument7 pagesFAR04-08 - Government Grant & Borrowing CostsAi NatangcopNo ratings yet

- Ais Chapter 5 ReviewerDocument9 pagesAis Chapter 5 ReviewerAngela Erish CastroNo ratings yet

- Charisma Company Required 1 Date Interest Received Interest Income Discount Amortization Carrying AmountDocument2 pagesCharisma Company Required 1 Date Interest Received Interest Income Discount Amortization Carrying AmountAnonnNo ratings yet

- Ia MCQ ComputationalDocument56 pagesIa MCQ ComputationalRomcel FlorendoNo ratings yet

- Policy Options On Income Inequality and Poverty: Some Basic ConsiderationsDocument10 pagesPolicy Options On Income Inequality and Poverty: Some Basic Considerationskath100% (1)

- Cost Accounting DrillsDocument13 pagesCost Accounting DrillsViky Rose EballeNo ratings yet

- IA 2 Chapter 5 ActivitiesDocument12 pagesIA 2 Chapter 5 ActivitiesShaina TorraineNo ratings yet

- TAX - Pinnacle Oct2024 1st PB AnskeyDocument13 pagesTAX - Pinnacle Oct2024 1st PB Anskeykomiryt143No ratings yet

- This Study Resource Was: InvestmentsDocument9 pagesThis Study Resource Was: InvestmentsMs VampireNo ratings yet

- Pract 1Document159 pagesPract 1bonnyme.00No ratings yet

- Chaps567 MCQ ReviewerDocument3 pagesChaps567 MCQ Reviewerdaniellejueco1228No ratings yet

- Problem No 5 (Acctg. 1)Document5 pagesProblem No 5 (Acctg. 1)Ash imoNo ratings yet

- MODULE 9 - Partnership Liquidation (Installment)Document9 pagesMODULE 9 - Partnership Liquidation (Installment)Gab Ignacio100% (1)

- Partnership Dissolution - CompleteDocument44 pagesPartnership Dissolution - CompletechxrlttxNo ratings yet

- CFAS (Review) - Summary CFAS (Review) - Summary: Accounting (Far Eastern University) Accounting (Far Eastern University)Document6 pagesCFAS (Review) - Summary CFAS (Review) - Summary: Accounting (Far Eastern University) Accounting (Far Eastern University)jaymz esperatNo ratings yet

- LTCCDocument16 pagesLTCCandzie09876No ratings yet

- PPE Initial Meas Assignment With Answers FormattedDocument5 pagesPPE Initial Meas Assignment With Answers FormattedCJ IbaleNo ratings yet

- Diana May Company IssuedDocument1 pageDiana May Company IssuedQueen ValleNo ratings yet

- Problem 1Document4 pagesProblem 1redassdawnNo ratings yet

- Exercise 2-5,6, and 7Document7 pagesExercise 2-5,6, and 7Nhel AlvaroNo ratings yet

- Unit 3 - Interim Reporting - 1484598619Document14 pagesUnit 3 - Interim Reporting - 1484598619Charmaine CañeteNo ratings yet

- Cash & Cash EquivalentDocument3 pagesCash & Cash Equivalentdeborah grace sagarioNo ratings yet

- Accounting 102 Bank Reconciliation Group Seatwork: Problem 1Document7 pagesAccounting 102 Bank Reconciliation Group Seatwork: Problem 1Elaisa SebastianNo ratings yet

- Chapter 6 Just in Time and Bacflush AccountingDocument17 pagesChapter 6 Just in Time and Bacflush AccountingだみNo ratings yet

- Illustration: Formation of Partnership Valuation of Capital A BDocument2 pagesIllustration: Formation of Partnership Valuation of Capital A BArian AmuraoNo ratings yet

- Activities KeyDocument7 pagesActivities KeyCassandra Dianne Ferolino MacadoNo ratings yet

- Illustration Chapter 1 1Document7 pagesIllustration Chapter 1 1PrincesipieNo ratings yet

- Far Ii Finals ProblemDocument17 pagesFar Ii Finals ProblemSaeym SegoviaNo ratings yet

- Case 3Document5 pagesCase 3Anna Marie Andal RanilloNo ratings yet

- Local Media4930298822971004354Document17 pagesLocal Media4930298822971004354Haks MashtiNo ratings yet

- WatatapsDocument29 pagesWatatapsjessa mae zerdaNo ratings yet

- Fit 5Document13 pagesFit 5Renalyn Ps MewagNo ratings yet

- Loan ReceivableDocument5 pagesLoan ReceivableJladySilhoutteNo ratings yet

- Lobrigas Unit3 Topic1 AssessmentDocument9 pagesLobrigas Unit3 Topic1 AssessmentClaudine LobrigasNo ratings yet

- Sol. Man. - Chapter 16 - Ppe Part 2 - Ia Part 1B 1Document15 pagesSol. Man. - Chapter 16 - Ppe Part 2 - Ia Part 1B 1Rezzan Joy Camara MejiaNo ratings yet

- Fund and Other InvestmentsDocument4 pagesFund and Other InvestmentslcNo ratings yet

- Accounting ReviewerDocument28 pagesAccounting ReviewerMary Ingrid Arellano RabulanNo ratings yet

- HO, BR, AgencyDocument10 pagesHO, BR, AgencyBlueBladeNo ratings yet

- Audit of PPEDocument4 pagesAudit of PPEBlueBlade100% (1)

- Home Office and BranchDocument3 pagesHome Office and BranchBlueBladeNo ratings yet

- Ethics and Moral Philosophy - General Introduction - 2020 - Lecture 5aDocument3 pagesEthics and Moral Philosophy - General Introduction - 2020 - Lecture 5aBlueBladeNo ratings yet

- Module 1 Financial Statement AnalysisDocument56 pagesModule 1 Financial Statement AnalysisBlueBladeNo ratings yet

- Ethics and Moral Philosophy - General Introduction - 2020 - Lecture 5cDocument3 pagesEthics and Moral Philosophy - General Introduction - 2020 - Lecture 5cBlueBladeNo ratings yet

- Liquidity Ratios: Working Capital To Total Asset RatioDocument3 pagesLiquidity Ratios: Working Capital To Total Asset RatioBlueBladeNo ratings yet

- Ethics and Moral Philosophy - General Introduction - 2020 - Lecture 5bDocument3 pagesEthics and Moral Philosophy - General Introduction - 2020 - Lecture 5bBlueBladeNo ratings yet

- Ethics and Moral Philosophy - General Introduction - 2020 - Lecture 1Document3 pagesEthics and Moral Philosophy - General Introduction - 2020 - Lecture 1BlueBladeNo ratings yet

- Ethics and Moral Philosophy - General Introduction - 2020 - Lecture 4Document3 pagesEthics and Moral Philosophy - General Introduction - 2020 - Lecture 4BlueBladeNo ratings yet

- Reviewer Bond ValuationDocument10 pagesReviewer Bond ValuationBlueBladeNo ratings yet

- Ethics Compilation CompleteDocument92 pagesEthics Compilation CompleteBlueBladeNo ratings yet

- Ethics and Moral Philosophy - General Introduction - 2020 - Lecture 3Document2 pagesEthics and Moral Philosophy - General Introduction - 2020 - Lecture 3BlueBlade100% (1)

- Lecture Notes Valuation of BondsDocument6 pagesLecture Notes Valuation of BondsBlueBlade100% (1)

- Module 5.3 Chapter 5 Answer Key 1Document8 pagesModule 5.3 Chapter 5 Answer Key 1BlueBladeNo ratings yet

- Topic: Using Pascal Triangle in The Derivative FunctionsDocument13 pagesTopic: Using Pascal Triangle in The Derivative FunctionsBlueBladeNo ratings yet

- Ethics and Moral Philosophy - General Introduction - 2020 - Lecture 2Document4 pagesEthics and Moral Philosophy - General Introduction - 2020 - Lecture 2BlueBladeNo ratings yet

- Prelims Finance MergedDocument149 pagesPrelims Finance MergedBlueBladeNo ratings yet

- Ethics General Introduction Lecture 1 - 6Document23 pagesEthics General Introduction Lecture 1 - 6BlueBladeNo ratings yet

- Risk and Rates of Return Problem SolvingDocument7 pagesRisk and Rates of Return Problem SolvingBlueBladeNo ratings yet

- Cfas - Chapter 4 - Exercise 1Document8 pagesCfas - Chapter 4 - Exercise 1BlueBladeNo ratings yet

- Problem Solving 7 Steps of Problem SolvingDocument3 pagesProblem Solving 7 Steps of Problem SolvingBlueBladeNo ratings yet

- Management Science: The Father of Scientific ManagementDocument15 pagesManagement Science: The Father of Scientific ManagementBlueBladeNo ratings yet

- Financial Accounting and Reporting Chapter 2Document9 pagesFinancial Accounting and Reporting Chapter 2BlueBladeNo ratings yet

- GROUP 5 Chapter 1Document11 pagesGROUP 5 Chapter 1BlueBladeNo ratings yet

- Cfas Exercise 2Document7 pagesCfas Exercise 2BlueBladeNo ratings yet

- Unit Vi - : CAPITAL BUDGETING - No Time Value of MoneyDocument6 pagesUnit Vi - : CAPITAL BUDGETING - No Time Value of MoneyBlueBladeNo ratings yet

- Cpale Syllabus 2022Document27 pagesCpale Syllabus 2022BlueBladeNo ratings yet

- Questions On Risk Management With AnswersDocument3 pagesQuestions On Risk Management With AnswersBlueBlade92% (26)

- DLL - Science 3 - Q3 - W7Document2 pagesDLL - Science 3 - Q3 - W7Arci KioperNo ratings yet

- Indic Visions in An Age of Science by Varadaraja VDocument18 pagesIndic Visions in An Age of Science by Varadaraja VHoang NguyenNo ratings yet

- Intellectual Property Law CasesDocument46 pagesIntellectual Property Law CasesShekinah GalunaNo ratings yet

- PAST AND PERFECT TENSES Lesson G7Document1 pagePAST AND PERFECT TENSES Lesson G7Joshua Lander Soquita CadayonaNo ratings yet

- Rubi Vs Provincial Board-DigestDocument2 pagesRubi Vs Provincial Board-DigestJed AdrianNo ratings yet

- GM 2019Document331 pagesGM 2019Peter ParkerNo ratings yet

- The Darby 1884-1890 BibleDocument1,734 pagesThe Darby 1884-1890 BibleKunedog1No ratings yet

- Basketball A Canadians ContributionDocument4 pagesBasketball A Canadians Contributionxmcupv89fmNo ratings yet

- Circle The Word(s) That Indicate How Much You Agree With Each StatementDocument2 pagesCircle The Word(s) That Indicate How Much You Agree With Each StatementMiyNo ratings yet

- Simple SentencesDocument4 pagesSimple SentencesLookAtTheMan 2002No ratings yet

- ECE 521: Microprocessor SystemDocument12 pagesECE 521: Microprocessor SystemAmar MursyidNo ratings yet

- Bastos Silva Santos Nesto PDFDocument14 pagesBastos Silva Santos Nesto PDFStipo LuksicNo ratings yet

- General Knowledge Questions Practice Test 2Document3 pagesGeneral Knowledge Questions Practice Test 2Arnabi DuttaNo ratings yet

- Chapter - 4 Labour Regime Within Sez LawDocument45 pagesChapter - 4 Labour Regime Within Sez LawNagalikar LawNo ratings yet

- Quantitative Research Chapter 3Document3 pagesQuantitative Research Chapter 3Michelle T GomezNo ratings yet

- Imenco ShackleDocument1 pageImenco ShackleimencoNo ratings yet

- Print Culture and Modern World - HistoryDocument6 pagesPrint Culture and Modern World - HistoryYashaswi GargNo ratings yet

- Music 10 - Q4 - M1W12 CO 1Document39 pagesMusic 10 - Q4 - M1W12 CO 1creguerro.13No ratings yet

- Defending A Stand On An Issue by PresentingDocument43 pagesDefending A Stand On An Issue by PresentingMarian Claire TulodNo ratings yet

- 新2上Document205 pages新2上Nguyễn Văn HòaNo ratings yet

- References Pasolini PDFDocument2 pagesReferences Pasolini PDFHamed HoseiniNo ratings yet

- Note On Resources From Living and Non-Living ThingsDocument2 pagesNote On Resources From Living and Non-Living ThingsSamuel AjanaNo ratings yet

- Leadership Skills For Small Group Leaders: Conflict ResolutionDocument28 pagesLeadership Skills For Small Group Leaders: Conflict ResolutionRestua SaraNo ratings yet

- Action Pack 12 TBDocument169 pagesAction Pack 12 TBHoang VânNo ratings yet

- Technical Furniture Motos & ElectrotechnicDocument53 pagesTechnical Furniture Motos & ElectrotechnicAchira DasanayakeNo ratings yet

- AQA A Level Geography RAG Checklist - Paper 1 CombinedDocument7 pagesAQA A Level Geography RAG Checklist - Paper 1 CombinedremesanmeenakshiNo ratings yet

- SET A. Post Test Part 1Document8 pagesSET A. Post Test Part 1Cath EspanolaNo ratings yet

- DC Spec Cu344d6 6ltaa9.5g1Document4 pagesDC Spec Cu344d6 6ltaa9.5g1mktgnextgentNo ratings yet

- Marma Points of Ayurveda Vasant Lad.09673Document18 pagesMarma Points of Ayurveda Vasant Lad.09673prasadmvk50% (2)